Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

12-31

12-35 (continued)

Establish standardized programming procedures and have

procedures.

Melinda should reconcile the Job Processed Log to the job

3. Assessment of the strengths of the programming function at

Jacobsons:

The programming staff is experienced with both systems

software and Jacobsons’ application software.

Programmers regularly attend continued professional

education courses.

Extensive logs of tape use and of changes made to programs

are maintained.

Concerns about the programming function:

systems software.

Programmers are responsible for maintaining secondary

storage of live programs and data files. Thus, programmers

at Jacobsons:

Divide programmers into systems programmers and application

programmers. Only assign system software changes to systems

programmers and application software changes to application

programmers.

Reassign responsibility for maintaining secondary storage

4. Assessment of the strengths of the IT operations function at

Jacobsons:

Melinda prepares a job schedule which operators follow to

12-32

12-35 (continued)

Operators perform routine monthly backup procedures.

Input batch controls are generated to verify the accuracy

and completeness of processing.

Concerns about the IS operations function:

risk of data loss.

No one, other than operators, verifies that only jobs included

on the job schedule are processed. Melinda depends totally

exceptions noted by operators.

application programs.

Comparison of batch input control totals to computer processing

is not performed by someone independent of the operator

responsible for the processing.

IS operations function:

Update key data files and program tapes on a more periodic

basis (perhaps daily). Store backup copies offsite.

5. Assessment of the strengths of the IT data control function at

Jacobsons:

Concerns about the IT data control function:

Data control personnel have the authority to approve changes

a non-existent employee.

Recommendations for change related to the management of the

IT data control function:

12-35 (continued)

department authorized changes to master files.

6. Users should be responsible for approving changes to master

files. They should actively compare authorized input to output to

ensure the accuracy, completeness, and authorization of output.

12-36 ACL Problem

a. There are 5,298 records in the “Purchase_orders” dataset, with a

total dollar value for the purchase order amount column of

b. Below is the ACL output from the Stratify command for the

Purchase Order Amount column. The first strata with purchase

12-34

12-36 (continued)

would want to know why there are 343 purchase orders missing,

and whether they were used but not recorded. If they were used but

not recorded, the auditor would be concerned about a potentially

material understatement of purchases. It is possible the purchase

overstatement of purchases if they were being recorded more than

once.

d. Highlighting the “Requisition Number” column, and using the

“Summarize” command, there are 3,097 purchase transactions (out

the client required a purchase requisition for all purchase

transactions, or an indication of why that policy may be violated

(e.g., if a purchase needs to be expedited and no one is available

to approve a requisition). The concern when there is no requisition

for a legitimate business purpose.

e. Use the “Classify” command to classify by vendor number with a

subtotal for purchase amount and save the output to “file.” That

indicates there are 2,823 unique vendor numbers. Performing a

“Quick Sort” of the percent of field column (in descending order) in

VN-0010390476508.

12-35

12-36 (continued)

po_number

po_date

vendor_number

po_amount

created_on

028493214615

1/19/2014

VN-0010090307334

115183.06

1/19/2014

028493215666

3/26/2014

VN-0010000259877

109933.27

3/26/2014

028493215782

4/5/2014

VN-0010340106140

149638.15

4/5/2014

028493215789

4/1/2014

VN-0010230187330

127375.73

4/1/2014

028493215811

4/7/2014

VN-0010000394772

108840.26

4/7/2014

028493215837

4/5/2014

VN-0010090260265

105883.12

4/5/2014

028493215843

4/6/2014

VN-0010260172176

128973.34

4/6/2014

028493215844

4/7/2014

VN-0010070247341

101968.05

4/7/2014

028493215924

4/14/2014

VN-0010000024372

111524.37

4/14/2014

028493215931

4/9/2014

VN-0010000271470

109810.9

4/9/2014

028493216120

4/20/2014

VN-0010000110409

114456.03

4/20/2014

028493216185

4/26/2014

VN-0010000433003

137635.35

4/26/2014

028493216189

4/26/2014

VN-0010260179830

115138.1

4/26/2014

028493216213

4/28/2014

VN-0010000195648

165841.62

4/28/2014

028493216220

4/30/2014

VN-0010000245035

227778.89

4/30/2014

028493216221

4/27/2014

VN-0010390088981

150800.65

4/27/2014

028493216250

5/3/2014

VN-0010000147105

102095.08

5/3/2014

028493216432

5/12/2014

VN-0010090203173

126002.08

5/12/2014

028493216438

5/7/2014

VN-0010450022589

115068.47

5/7/2014

028493216439

5/10/2014

VN-0010390190953

140503.18

5/10/2014

028493216467

5/12/2014

VN-0010450113576

132830.82

5/12/2014

028493216559

5/18/2014

VN-0010000256594

106881.05

5/18/2014

028493216591

5/20/2014

VN-0010090193739

138132.97

5/20/2014

028493216596

5/18/2014

VN-0010160206123

102713.45

5/18/2014

028493216597

5/18/2014

VN-0010000269163

104790.21

5/18/2014

028493216619

5/19/2014

VN-0010070241895

108725.19

5/19/2014

028493216718

5/26/2014

VN-0010210023460

106386.5

5/26/2014

028493216747

5/26/2014

VN-0010410272994

125765.85

5/26/2014

028493216752

5/27/2014

VN-0010480512685

152527.65

5/27/2014

028493216753

5/25/2014

VN-0010070502023

148475.86

5/25/2014

028493216914

5/31/2014

VN-0010000268675

155921.72

5/31/2014

028493216922

6/4/2014

VN-0010250311629

117570.63

6/4/2014

028493217004

6/7/2014

VN-0010070108651

103041.69

6/7/2014

028493217009

6/4/2014

VN-0010200427270

108830.02

6/4/2014

028493217050

6/8/2014

VN-0010090260265

135321.12

6/8/2014

028493217057

6/8/2014

VN-0010480078505

117350.22

6/8/2014

12-36

12-36 (continued)

028493217135

6/15/2014

VN-0010000267717

200945.74

6/15/2014

028493217142

6/14/2014

VN-0010330031684

199494.08

6/14/2014

028493217274

6/21/2014

VN-0010070241895

110073.07

6/21/2014

028493217278

6/18/2014

VN-0010000259361

117540.23

6/18/2014

028493217392

6/28/2014

VN-0010000087814

111687.45

6/28/2014

028493217398

6/24/2014

VN-0010000102912

101973.45

6/24/2014

028493217423

6/29/2014

VN-0010000147105

108972.1

6/29/2014

028493217431

7/1/2014

VN-0010100020125

107515.38

7/1/2014

028493217544

7/2/2014

VN-0010450319216

139761.96

7/2/2014

028493217715

7/12/2014

VN-0010000281402

164763.19

7/12/2014

028493217722

7/14/2014

VN-0010160228550

122279.13

7/14/2014

028493217723

7/12/2014

VN-0010070052167

127611.4

7/12/2014

028493217815

7/21/2014

VN-0010000108791

143510.51

7/21/2014

028493217822

7/21/2014

VN-0010460029032

141854.71

7/21/2014

028493217823

7/20/2014

VN-0010070059858

102233.56

7/20/2014

028493217938

7/22/2014

VN-0010000273841

115415.65

7/22/2014

028493218094

8/3/2014

VN-0010270141534

127599.74

8/3/2014

028493218180

8/9/2014

VN-0010000430933

101012.03

8/9/2014

028493218187

8/9/2014

VN-0010000282973

149550.22

8/9/2014

028493218224

8/13/2014

VN-0010000270884

148361.72

8/13/2014

028493218231

8/11/2014

VN-0010070344773

104780.65

8/11/2014

028493218275

8/16/2014

VN-0010090168632

118950.76

8/16/2014

028493218346

8/16/2014

VN-0010380323702

273698.86

8/16/2014

028493218353

8/19/2014

VN-0010290049720

143706.72

8/19/2014

028493218354

8/17/2014

VN-0010000268420

132859.03

8/17/2014

028493218453

8/24/2014

VN-0010000233061

119706.99

8/24/2014

028493218549

9/1/2014

VN-0010070241895

142498.05

9/1/2014

028493218555

9/1/2014

VN-0010000249805

182623.85

9/1/2014

028493218556

9/2/2014

VN-0010150116435

145616.81

9/2/2014

028493218579

9/2/2014

VN-0010000207185

113427.53

9/2/2014

12-37

Integrated Case Application

PINNACLE MANUFACTURING―PART IV

Following are control risk matrices and related notes that are used to direct a

discussion of the requirements of the case. It should be understood that

single right answer.

Computer-prepared matrices using Excel (P1237.xls) are contained on

the text web site. They are essentially the same as the matrices on the next

two pages.

12-37 (continued)

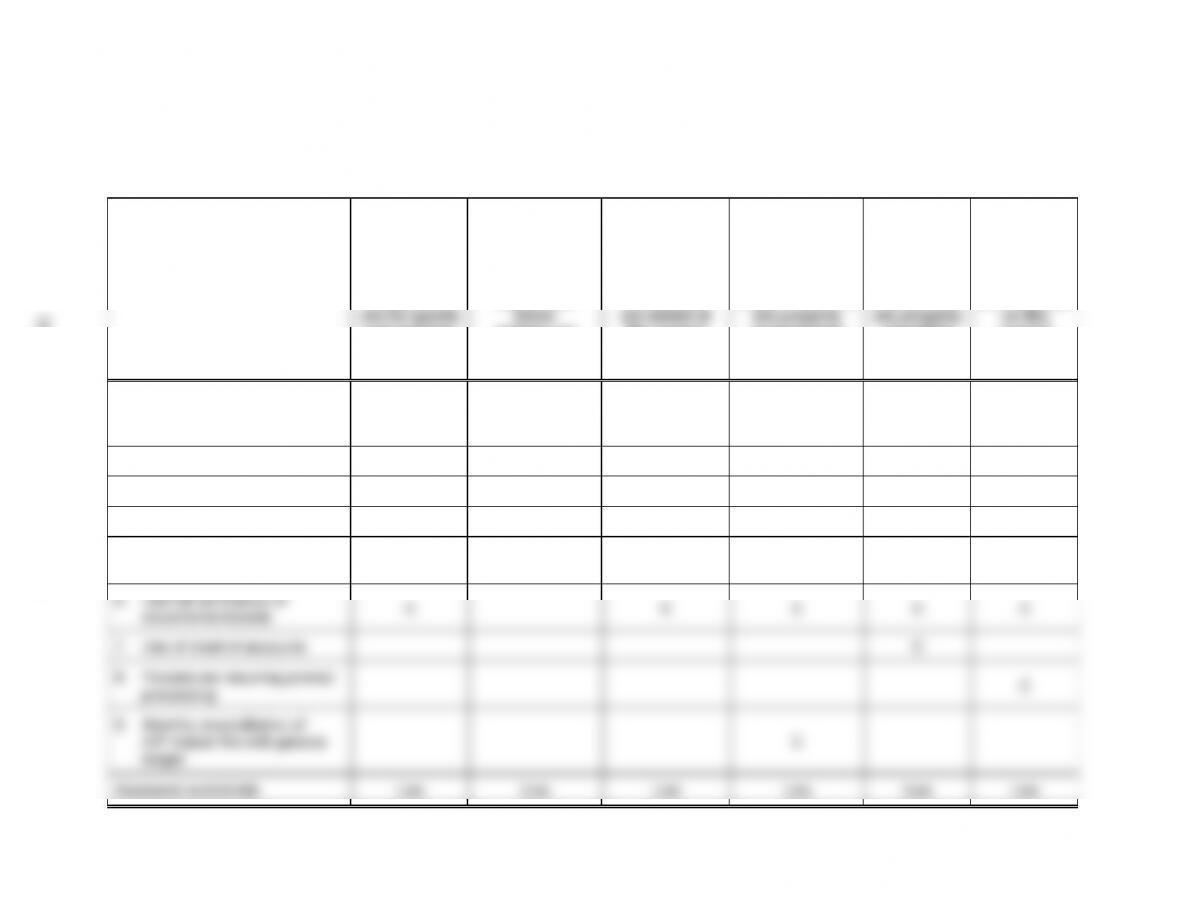

PINNACLE MANUFACTURING - Part IV

Control Risk Matrix – Acquisitions

Transaction-Related

Audit Objective

Internal

Controls

Recorded

acquisitions

and services

received

(occurrence).

Existing

acquisition

actions are

recorded

(completeness).

Recorded

acquisition

transactions

the correct

amounts

(accuracy).

Recorded

acquisition

transactions are

properly

included in the

master files, and

summarized

(posting and

summarization).

Acquisition

transactions

classified

(classifica-

tion).

Acquisition

transactions

are recorded

correct

dates

(timing).

1. Required use of PO and

receiving report with check of

completeness

C

2. Proper approval

C

C

3. Segregation of functions

C

4. Cancellation of documents

C

5. Prenumbering of documents

with accounting for sequence

C

6. Internal verification of

documents/records

C

C

C

C

C

7. Use of chart of accounts

C

8. Procedures requiring prompt

processing

C

9. Monthly reconciliation of

A/P master file with general

ledger

C

Assessed control risk

Low

Low

Low

Low

Low

Low

12-38

Copyright © 2017 Pearson Education, Inc.

12-37 (continued)

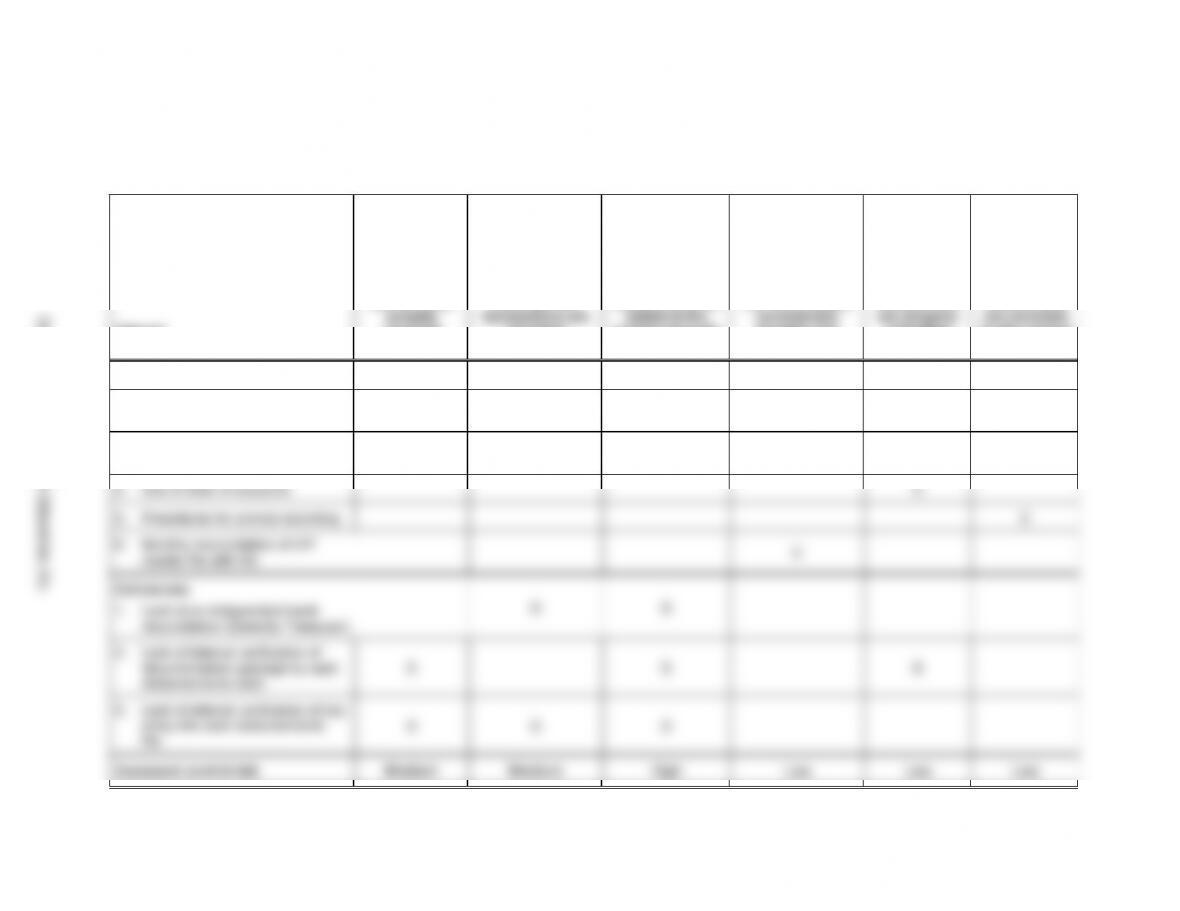

PINNACLE MANUFACTURING - Part IV

Control Matrix - Cash Disbursements

Transaction-Related

Audit Objectives

Internal

Controls

Recorded cash

disbursements

are for goods

and services

received

(occurrence).

Existing cash

disbursement

recorded

(completeness).

Recorded cash

disbursement

transactions are

correct amounts

(accuracy).

Recorded cash

disbursement

transactions are

properly included

in the master file

and are properly

(posting and

summarization).

Cash

disbursement

transactions

classified

(classification).

Cash

disbursement

transactions

on the correct

dates (timing).

1. Segregation of functions

C

2. Review of support, signing of

checks by authorized person

C

3. Prenumbered checks; accounted

for

C

4. Use of chart of accounts

C

5. Procedures for prompt recording

C

6. Monthly reconciliation of A/P

master file with G/L

C

Deficiencies

1. Lack of an independent bank

reconciliation (Done by Treasurer)

D

D

2. Lack of internal verification of

documentation package by cash

disbursements clerk.

D

D

D

3. Lack of internal verification of key

entry into cash disbursements

file.

D

D

D

Assessed control risk

Medium

Medium

High

Low

Low

Low

12-39

Copyright © 2017 Pearson Education, Inc.

12-40

12-37 (continued)

Notes to 12-37, Part IV

cycle,

(b) obtain controls from a flowchart description,

(c) relate controls to objectives,

(d) evaluate a set of controls as a system.

substantive tests of details of balances and/or transactions.

Controls for cash disbursements are not nearly as good, given the

of documents)?