Which of the following is not a term related to evaluating results in audit sampling until

after a sample is tested and evaluated?

A) sample exception rate

B) estimated population exception rate

C) computed upper exception rate

D) exception

Some companies have customers send payments directly to an address maintained by a

bank. This is called a(n) ________ system.

A) direct deposit

B) funds transfer

C) lockbox

D) interbank transfer

When positive confirmations are used, auditing standards require alternative procedures

for confirmations not returned by the customer. Which of the following would not be

considered an alternative procedure?

A) Send a second confirmation request.

B) Examine subsequent cash receipts to determine if the receivable has been paid.

C) Examine shipping documents to verify that the merchandise was shipped.

D) Examine sales invoice to verify the actual issuance of a sales invoice and the actual

date of the billing.

When the client’s physical inventory occurs before the last day of the year, it is still

necessary to perform an accounts payable cutoff at the time of the count. In addition,

the auditor must verify whether all acquisitions taking place between the count and the

end of the year were added to

A) the physical inventory.

B) accounts payable.

C) accounts payable and cost of goods sold.

D) the physical inventory and accounts payable.

Which is usually included in an engagement letter?

A)

B)

C)

D)

Which of the following represents all of the ways a CPA firm can be organized?

A) proprietorships and partnerships

B) proprietorships, partnerships, and professional corporations

C) proprietorships, general partnerships, general corporations, professional

corporations, limited liability companies, and limited liability partnerships if permitted

by state law

D) single proprietorships, partnerships, professional corporations if permitted by state

law, or regular corporations

If an auditor is unsuccessful in using the lack of duty defense to have a case dismissed

in a third-party suit, the preferred defense is

A) lack of duty to perform.

B) nonnegligent performance.

C) absence of causal connection.

D) client fraud.

You are performing the audit of Jenkins and Company. Your tests of controls and tests

of transactions for accounts payable demonstrate that the controls are operating

effectively. This would normally allow you to

A) eliminate the need for substantive testing of balances for accounts payable.

B) reduce the need for substantive testing of balances for accounts payable.

C) reduce control tests in other transactions cycles.

D) increase the need for substantive testing of balances for accounts payable.

Records that include data about employees such as employment date, performance

ratings and pay rates are the

A) human resource records.

B) employee screening forms.

C) summary payroll reports.

D) employee folders.

According to the principle established by the Restatement of Torts, foreseen users must

be members of

A) any potential user group.

B) a legally protected class.

C) a reasonably limited and identifiable user group.

D) a reasonably limited and established user group.

Comparing the physical counts with the perpetual inventory master files satisfies the

balance-related audit objective of

A) classification.

B) observation.

C) completeness.

D) accuracy.

________ deals with potential overstatement and ________ deals with understatements

(unrecorded transactions).

A) Occurrence; completeness

B) Completeness; occurrence

C) Accuracy; classification

D) Classification; accuracy

Contingent liability disclosure in the footnotes of the financial statements would

normally be made when

A) the outcome of the accounting event is deemed probable, but a reasonable estimation

as to the amount cannot be made by the client or auditor.

B) a reasonable estimation of the loss can be made, but the outcome is not probable.

C) the outcome of the accounting event is deemed probable, and a reasonable

estimation as to the amount can be made.

D) the outcome of the accounting event as well as a reasonable estimation of the loss

cannot be made.

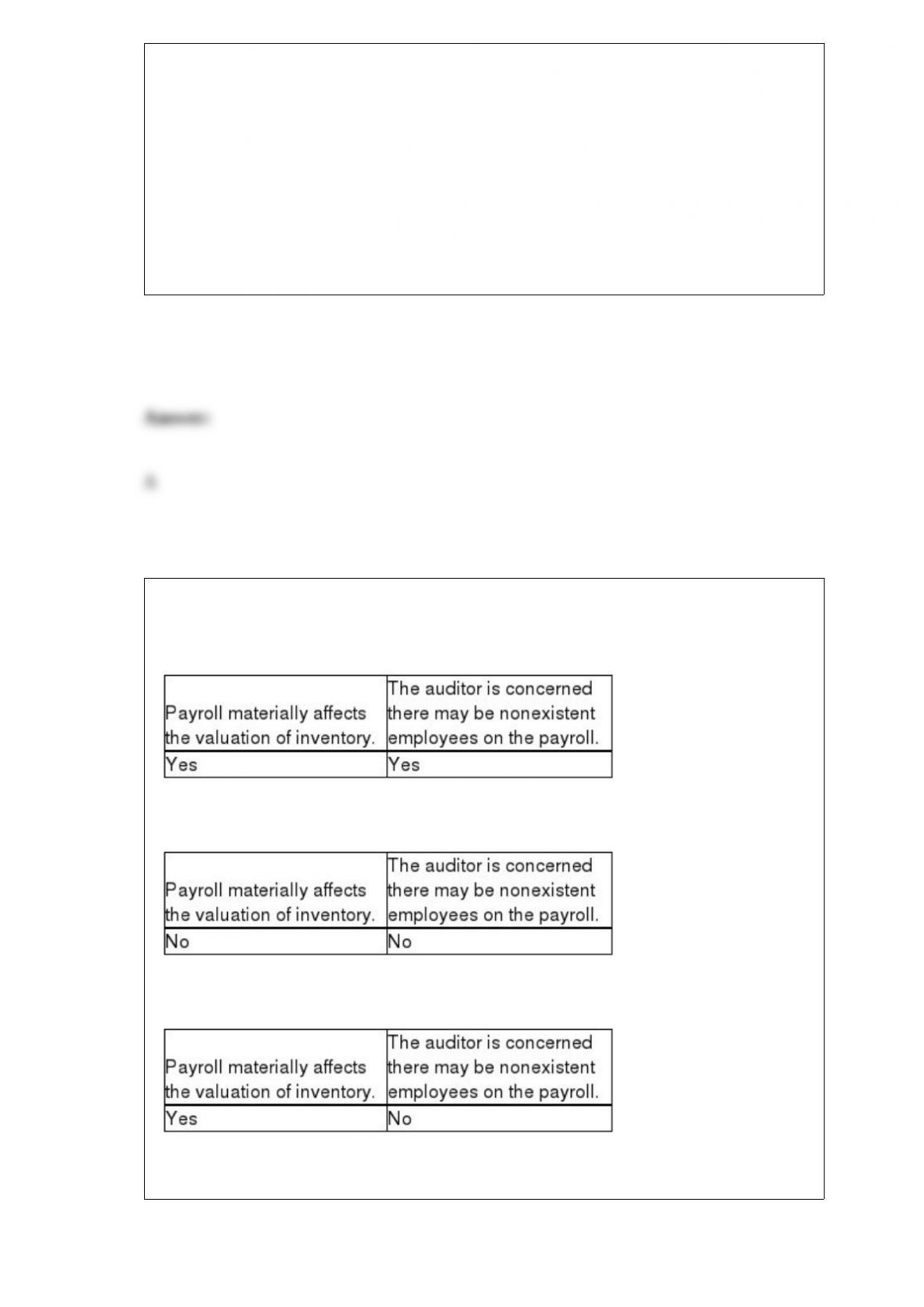

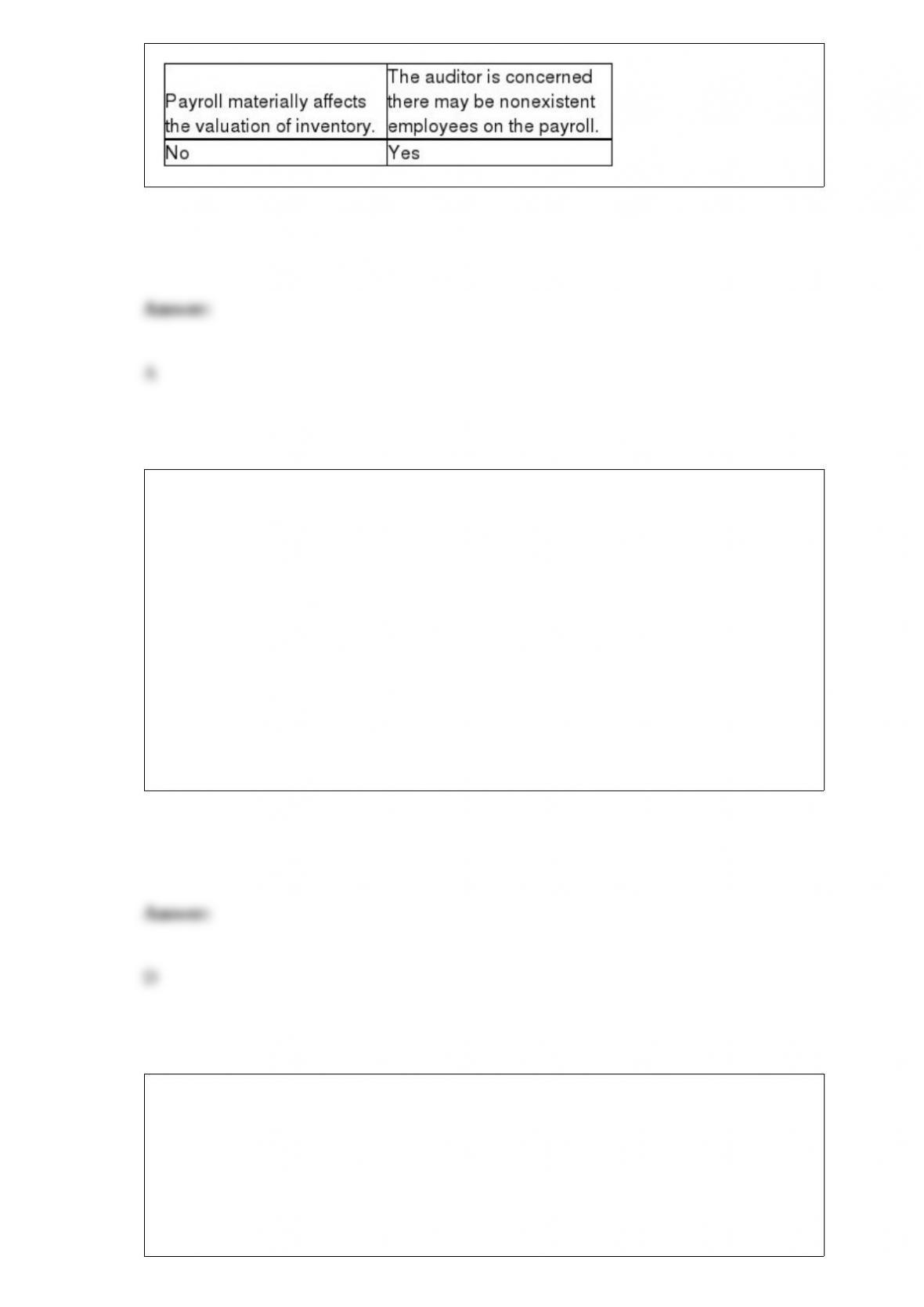

Auditors may extend their tests of payroll in which of the following circumstances?

A)

B)

C)

D)

Which of the following is not a reason why the auditor requests that the client provide a

letter of representation?

A) Professional auditing standards require the auditor to obtain a letter of

representation.

B) It impresses upon management its responsibility for the accuracy of the information

in the financial statements.

C) It provides written documentation of the oral responses already received to inquiries

of management.

D) It determines the type of opinion the auditor will issue on the financial statements.

The WebTrust service requires that a CPA update its testing of the e-commerce aspects

of an entity’s website at least every

A) ninety days.

B) month.

C) six months.

D) twelve months.

Which of the following is not an underlying principle related to risk assessment?

A) The organization should have clear objectives in order to be able to identify and

assess the risks relating to the objectives.

B) The auditors should determine how the company’s risks should be managed.

C) The organization should consider the potential for fraudulent behavior.

D) The organization should monitor changes that could impact internal controls.

When working with the different variables methods,

A) difference estimation frequently results in larger sample sizes than any other method.

B) ratio estimation is the method preferred by most auditors since it is simpler to

calculate confidence intervals.

C) the difference between the mean-per-unit estimate and the difference estimate is the

definition of what is being measured.

D) stratification can only be used with difference estimation.

The first step to be followed when deciding the appropriate audit report in a given set of

circumstances is to

A) decide the appropriate type of report for the condition.

B) write the report.

C) determine whether any conditions exists requiring a departure from a standard

unmodified opinion audit report.

D) decide the materiality for each condition.

One of the steps involved in planning the sample for the tests of details of balances is to

A) select the sample.

B) perform the audit procedures.

C) define a misstatement.

D) analyze the misstatements.

When the auditor concludes that there is substantial doubt about the entity’s ability to

continue as a going concern, the appropriate audit report could be

I. an unmodified opinion audit report with an explanatory paragraph.

II. a disclaimer of opinion.

A) I only

B) II only

C) I or II

D) Neither I nor II

Which of the following is not a weakness of using industry averages for auditing?

A) The industry data are broad averages.

B) Different companies follow different accounting methods.

C) They can be helpful in identifying potential misstatements.

D) All of the above are weaknesses.

________ is the risk that the auditor or audit firm will suffer harm after the audit is

finished, even though the audit report was correct.

A) Inherent risk

B) Audit risk

C) Engagement risk

D) Control risk

The three requirements for becoming a CPA include all but which of the following?

A) uniform CPA examination requirement

B) education requirements

C) character requirements

D) experience requirement

The extent of a search for unrecorded liabilities largely depends on

A) materiality and inherent risk.

B) materiality and control risk.

C) materiality only.

D) inherent risk only.

The auditor’s responsibility section of the standard unmodified opinion audit report

states that the audit is designed to

A) discover all errors and/or irregularities.

B) discover material errors and/or irregularities.

C) conform to generally accepted accounting principles.

D) obtain reasonable assurance whether the statements are free of material

misstatement.

With which of the following client personnel would it generally not be appropriate to

inquire about commitments or contingent liabilities?

A) controller

B) president

C) accounts receivable clerk

D) vice president of sales

The acceptable risk of overreliance

A) is the risk that the auditor will erroneously conclude that the controls are less

effective than they actually are.

B) is less of a concern to the auditors than the risk of underreliance.

C) represents the auditor’s measure of sampling risk.

D) is determined by a statistical formula, and not by professional judgment.

What type of SOC report is intended to meet the needs of a broad range of users who

need information and assurance about controls at s service organization that affect the

security, availability, and processing integrity of the systems the service organization

uses to process users’ data and the confidentiality and privacy of the information

processed by these systems?

A) SOC 1 report

B) SOC 2 report

C) SOC 3 report

D) none of the above

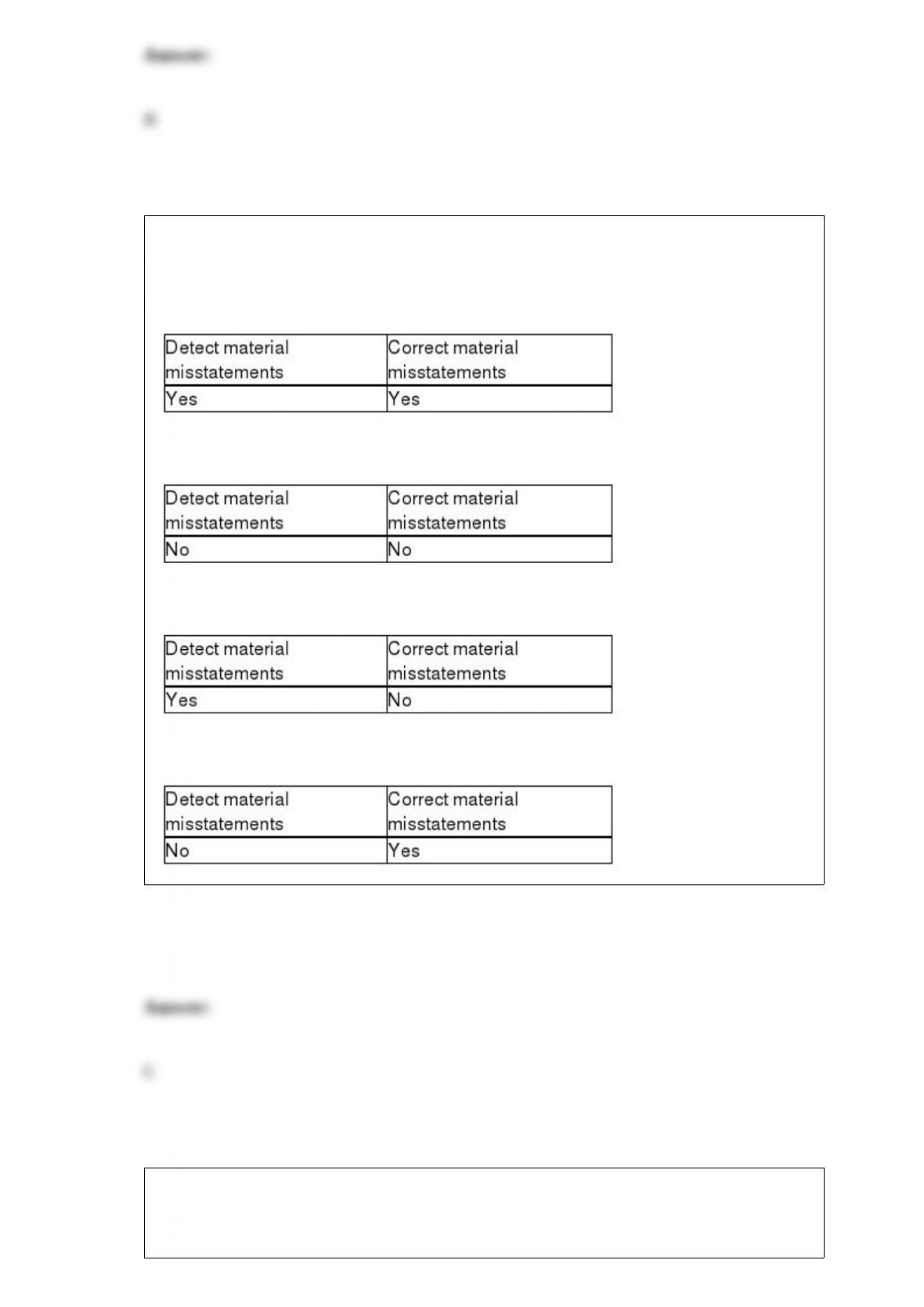

When management is evaluating the design of internal control, management evaluates

whether the control can do which of the following?

A)

B)

C)

D)

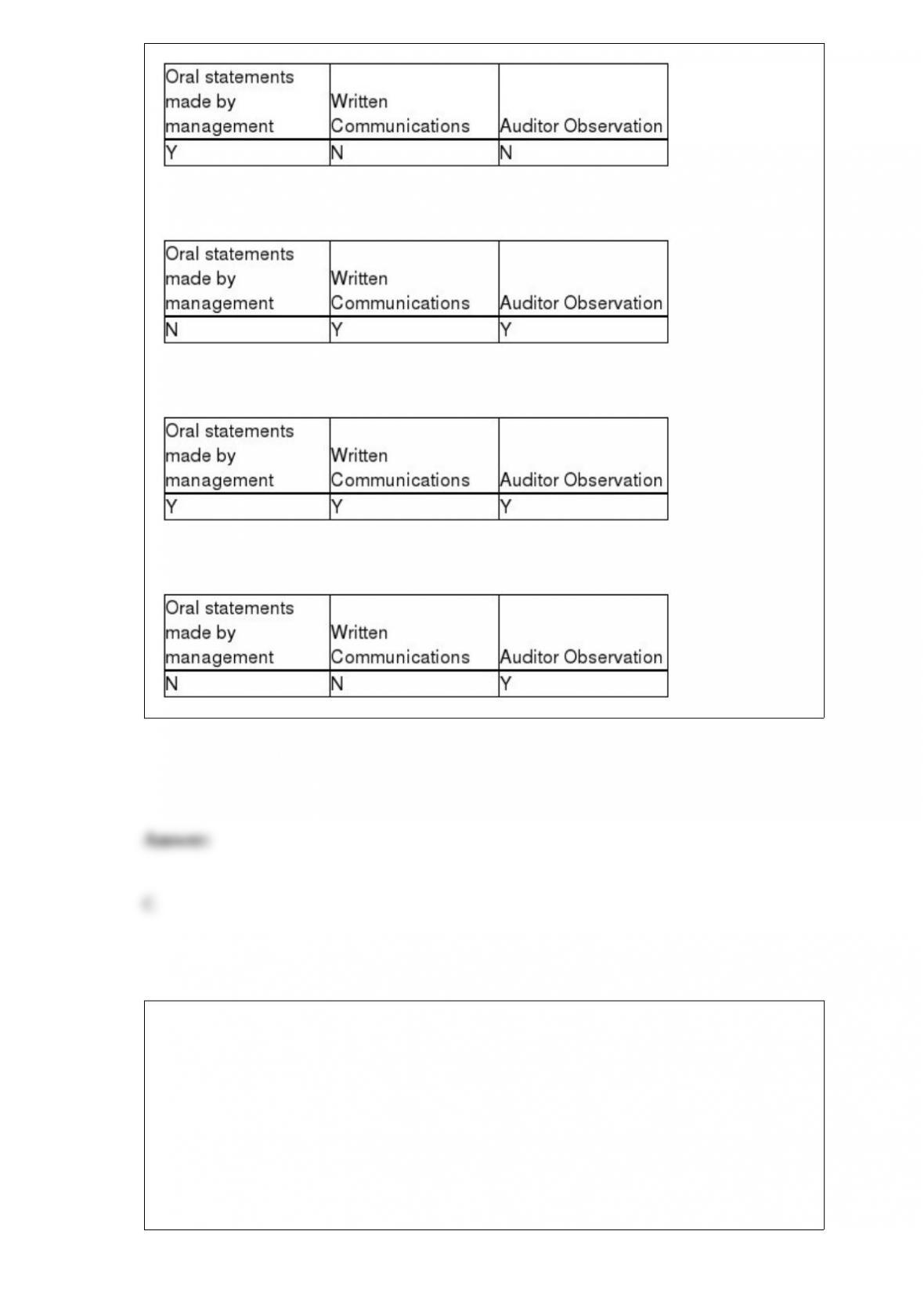

Which of the following is considered audit evidence?

A)

B)

C)

D)

Procedures that may uncover fraud in the cash receipts area include

A) confirmation of accounts payable.

B) comparison of purchase orders to invoices.

C) tests performed to detect lapping.

D) all of the above.

No reference is made in the auditor’s report to other auditors who perform a portion of

the audit when

I. The other auditor audited an immaterial portion of the audit.

II. The other auditor is well known or closely supervised by the principle auditor.

III. The principle auditor has thoroughly reviewed the work of the other auditor.

A) I and II

B) I and III

C) II and III

D) I, II and III

Misappropriation of assets

A) is generally committed by company management.

B) harms the users of the financial statements by providing them incorrect financial

data for their decision making.

C) causes harm to stockholders because the assets are no longer available to their

rightful owners.

D) causes the financial statements to be misstated since the misappropriation usually

involves material amounts.