The letter of representation obtained from an audit client should be

A) dated as of the end of the period under audit.

B) dated as of the audit report date.

C) dated as of any date decided upon by the client and auditor.

D) dated as of the issuance of the financial statement.

A client has a calendar year-end. Listed below are four events that occurred after

December 31. Which one of these subsequent events might result in adjustment of the

December 31 financial statements?

A) sale of a major subsidiary

B) adoption of accelerated depreciation methods

C) write-off of a substantial portion of inventory as obsolete

D) collection of 90% of the accounts receivable existing at December 31

A written understanding detailing what the auditor expects from the client in

performing an audit will normally be expressed in the

A) management letter requested by the auditor.

B) engagement letter.

C) audit Plan.

D) audit Strategy for the client.

The overall objective in the audit of the acquisition and payment cycle is

A) to ensure the reliability of the affected accounts.

B) to ensure the accuracy of the affected accounts.

C) to evaluate whether the affected accounts are fairly presented in accordance with

accounting standards.

D) to evaluate whether fraudulent payments were made.

Which of the following computer-assisted auditing techniques inserts an audit module

in the client’s application system to identify specific types of transactions?

A) parallel simulation testing

B) test data approach

C) embedded audit module

D) generalized audit software testing

Firewalls are used to protect from

A) erroneous internal handling of data.

B) insufficient documentation of transactions.

C) illogical programming commands.

D) unauthorized external users.

For public companies, the ________ is responsible for hiring the auditor as required by

the Sarbanes-Oxley Act.

A) client’s management

B) client’s chief executive officer

C) client’s chief financial officer

D) client’s audit committee

Which of the following is not one of the major parts of the AICPA’s Code of

Professional Conduct?

A) principles

B) rules

C) interpretations

D) definitions

According to the profession’s ethical standards, an auditor would be considered

independent in which of the following instances?

A) The auditor’s checking account, which is fully insured by a federal agency, is held at

a client financial institution.

B) The auditor is also an attorney who advises the client as its general counsel.

C) An employee of the auditor serves as treasurer of a charitable organization that is a

client.

D) The client owes the auditor fees for two consecutive annual audits.

In the processing and recording of cash disbursements,

A) after a check includes the signature of an authorized person, it is a liability.

B) when a check cashed by the vendor has cleared the bank, it is called an outstanding

check.

C) in many cases, the company submits payment to the vendor electronically through

an electronic funds transfer (EFT) between the company’s bank and the vendor’s bank.

D) the accounts payable master file is a computer-generated file that includes all cash

disbursement transaction processed by the accounting system for a period.

The most important aspect of evaluating the client’s method of obtaining a reliable

cutoff is to

A) perform extensive detailed testing of cutoff.

B) evaluate the client’s control procedures around cutoff.

C) confirm a sample of transactions near period end with customers.

D) confirm transaction with customers.

Given the economic and time constraints in which auditors can collect evidence

regarding management assertions about the financial statements, the auditor normally

gathers evidence that is

A) irrefutable.

B) conclusive.

C) persuasive.

D) completely convincing.

Which of the following is likely to be determined first when performing tests of details

for accounts receivable?

A) Recorded accounts receivable exist.

B) Accounts receivable in the aged trial balance agree with related master file amounts,

and the total is correctly added and agrees with the general ledger.

C) The client has a right to the accounts receivable.

D) Existing accounts receivable are included.

The auditor’s responsibility for “reviewing the subsequent events” of a public company

that is about to issue new securities is normally limited to the period of time

A) beginning with the balance sheet date and ending with the date of the auditor’s

report.

B) beginning with the start of the fiscal year under audit and ending with the balance

sheet date.

C) beginning with the start of the fiscal year under audit and ending with the date of the

auditor’s report.

D) beginning with the balance sheet date and ending with the date the registration

statement becomes effective.

Fraud awareness training should be

A) broad and all-encompassing.

B) extensive and include details for all functional areas.

C) specifically related to the employee’s job responsibility.

D) focused on employees understanding the importance of ethics.

Without an effective ________, the other components of the COSO framework are

unlikely to result in effective internal control, regardless of their quality.

A) risk assessment policy

B) monitoring policy

C) control environment

D) system of control activities

Which is not an important objective for financial instruments?

A) existence

B) cutoff

C) accuracy

D) realizable value

The auditor’s tour of the client’s inventory facilities should be led by

A) a member of the audit committee.

B) the CFO.

C) a plant supervisor.

D) the company president.

An auditor should recognize that the application of auditing procedures may produce

evidence indicating the possibility of errors of fraud and therefore should

A) plan and perform the engagement with an attitude of professional skepticism.

B) not rely on internal controls that are designed to prevent or detect errors or fraud.

C) design audit tests to detect unrecorded transactions.

D) extend the work to audit the majority of the recorded transactions and records of an

entity.

Which part of the AICPA’s Code of Professional Conduct is enforceable?

A) ethical rulings

B) rules of conduct

C) principles

D) interpretations

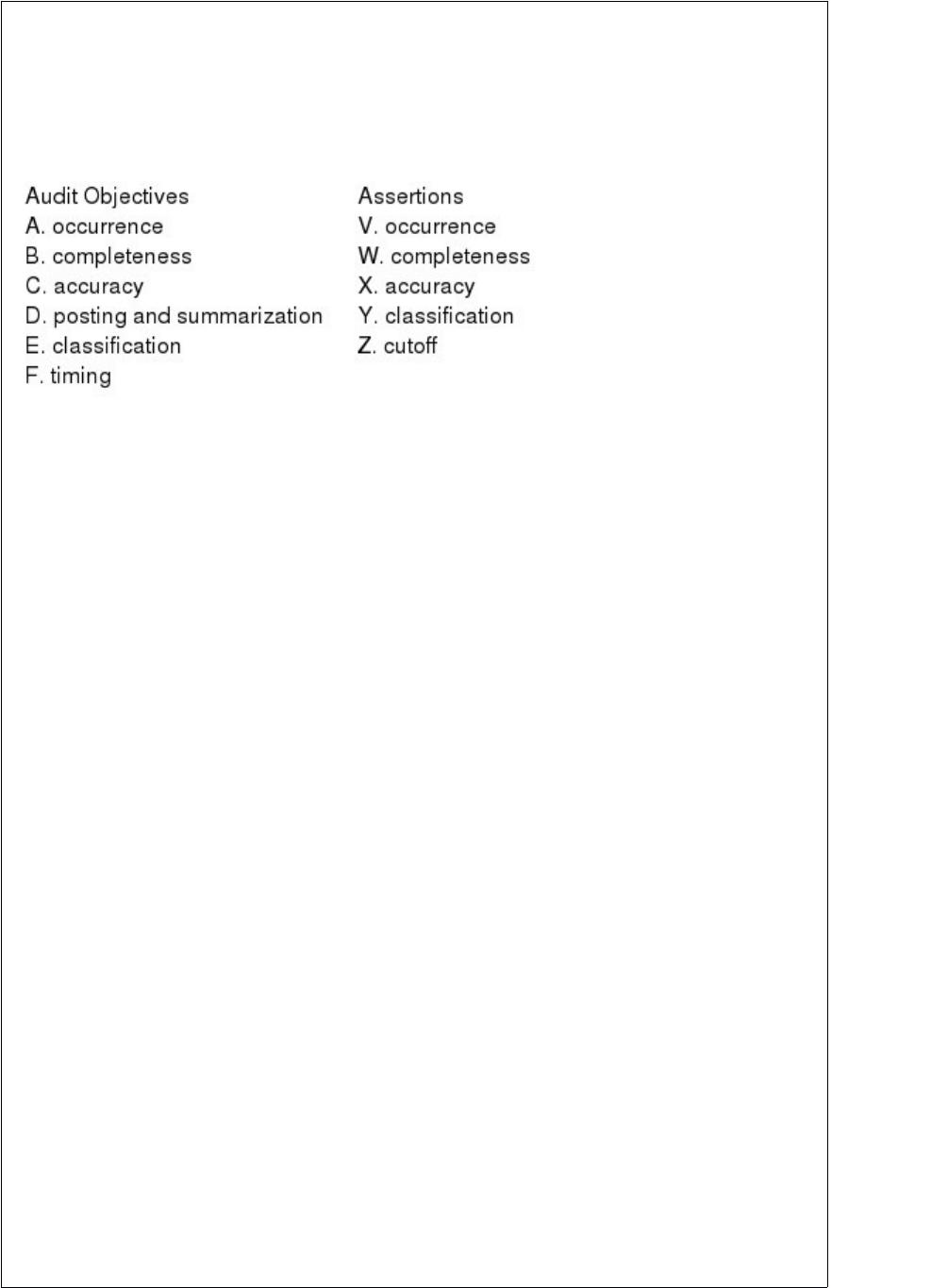

Below are five audit procedures, all of which are tests of transactions associated with

the audit of the sales and collection cycle. Also below are the six general

transaction-related audit objectives and the five management assertions. For each audit

procedure, indicate (1) its audit objective, and (2) the management assertion being

tested.

1. Vouch recorded sales from the sales journal to the file of bills of lading.

(1) ________

(2) ________

2. Compare dates on the bill of lading, sales invoices, and sales journal to test for delays

in recording sales transactions.

(1) ________

(2) ________

3. Account for the sequence of prenumbered bills of lading and sales invoices.

(1) ________

(2) ________

4. Trace from a sample of prelistings of cash receipts to the cash receipts journal, testing

for names, amounts, and dates.

(1) ________

(2) ________

5. Examine customer order forms for credit approval by the credit manager.

(1) ________

(2) ________

Which one of the following would the auditor consider to be an incompatible operation

if the cashier receives remittances from the mail room?

A) The cashier prepares the daily deposit.

B) The cashier makes the daily deposit at a local bank.

C) The cashier posts the receipts to the accounts receivable subsidiary ledger cards.

D) The cashier endorses the checks.

The auditor must know the client’s capitalization policies to determine whether

acquisitions are

A)

B)

C)

D)

Receipt of ordered materials by the receiving department will generate the completion

of a form called the

A) bill of lading.

B) receiving report.

C) materials requisition.

D) inventory acquisition summary.

When auditing manufacturing overhead costs assigned to inventory, auditors should

keep in mind that

A) GAAP has strict procedures that must be followed when assigning overhead to

work-in-process inventory.

B) overhead costs must be allocated to raw materials, work-in-process, and finished

goods inventory.

C) management typically allocates overhead using total direct labor dollars as the basis

for the allocation.

D) determining the reasonableness of the allocation method is relatively simple for

work-in-process inventory.

When assessing risks affecting cash,

A) if a business defers preparing bank reconciliations for long periods, the value of the

control is reduced and may affect the auditor’s assessment of control risk for cash.

B) most companies are likely to have significant client business risks affecting their

cash balances.

C) there is a low inherent risk for the existence and completeness objectives for cash.

D) all of the above are accurate statements.

Two of the types of services provided in connection with the Statements on Standards

for Accounting and Review Services are

A) audit and examination services.

B) compilation and review services.

C) examination and review services.

D) management advisory services and compilations.

The distribution of which of the following types of reports is unrestricted?

A) examinations and reviews

B) reviews and agreed-upon procedures

C) examinations and agreed-upon procedures

D) examinations, reviews, and agreed-upon procedures

An imprest payroll account that has a significant balance may indicate the presence of

A) employees have not yet cashed their payroll checks.

B) fraudulent transfer of funds by the company.

C) lack of controls over payroll distribution.

D) the company is overpaying its employees.

Your accounting firm has accepted a compilation engagement from a client in which

your firm is not independent. In that case you

A) may not accept the engagement.

B) may accept the engagement and disclose the lack of independence.

C) may accept the engagement and not disclose the lack of independence.

D) may accept the engagement and disclose the lack of independence and the reason for

the lack of independence.

When reporting identified or suspected noncompliance,

A) the auditor must report inconsequential noncompliance to the audit committee.

B) the auditor should communicate all material noncompliance matters to those charged

with governance.

C) any intentional noncompliance must be reported to local law enforcement.

D) all noncompliance, whether material or not, must result in a disclaimer of opinion.

Which of the following types of audit tests is usually emphasized due to a lack of

independent third-party evidence related to payroll transactions?

A) analytical procedures

B) tests of details of balances

C) tests of controls

D) Each of the above is emphasized.

The primary purpose of audit procedures is to

A) detect all errors or fraudulent activities as well as illegal activities.

B) comply with auditing standards promulgated by the PCAOB for publicly held

clients.

C) gather corroborative audit evidence about management’s assertions regarding the

client’s financial statements.

D) determine the amount of errors in the balance sheet accounts in order to adjust the

accounts to actual.