When communicating with the audit committee and management,

A) only material fraud and illegal acts are required by auditing standards to be

communicated.

B) all internal control deficiencies are required by auditing standards to be

communicated.

C) the communications should be made in a timely manner to allow those charged with

governance to take appropriate actions.

D) all communications with the audit committee and management must be in writing.

It is frequently possible to test the physical inventory prior to the balance sheet date

when

A) the perpetual inventory records are accurate and related controls operate effectively.

B) year-end sales are small.

C) the internal control system is no better at year-end than at an earlier point in time.

D) the client counts inventory at interim dates.

Under common law, an individual or company that (1) does not have a contract with an

auditor, (2) is known by the auditor in advance of the audit, and (3) will use the

auditor’s report to make decisions about the client company has:

A) no rights unless an auditor is grossly negligent.

B) no rights unless an auditor is fraudulent.

C) no rights against an auditor.

D) the same rights against an auditor as a client.

Which of the following is not an application control?

A) reprocessing authorization of sales transactions

B) reasonableness test for unit selling price of sale

C) post-processing review of sales transactions by the sales department

D) logging in to the company’s information systems via a password

The auditor needs to gain reasonable assurance that the equipment accounts in the fixed

asset master file are not understated. Which of the following accounts would most

likely be reviewed in making that determination?

A) depreciation expense

B) repairs and maintenance expense

C) gains/losses on sales and retirements

D) cash

Which of the following is an element of the CPA’s quality control system that should be

considered in establishing its quality control policies and procedures?

A) considering audit risk and materiality

B) using statistical sampling techniques

C) assigning personnel to engagements

D) complying with laws and regulations

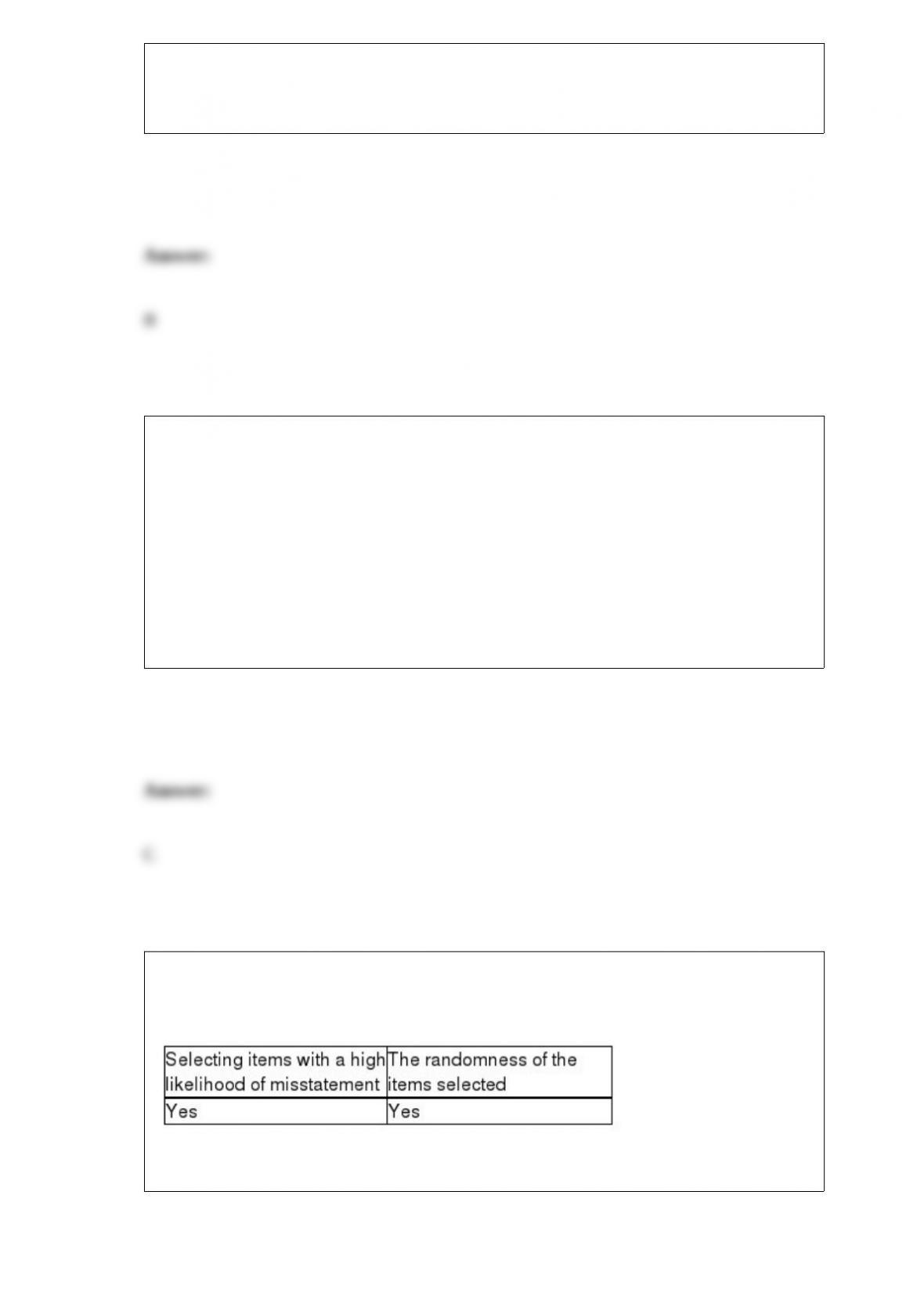

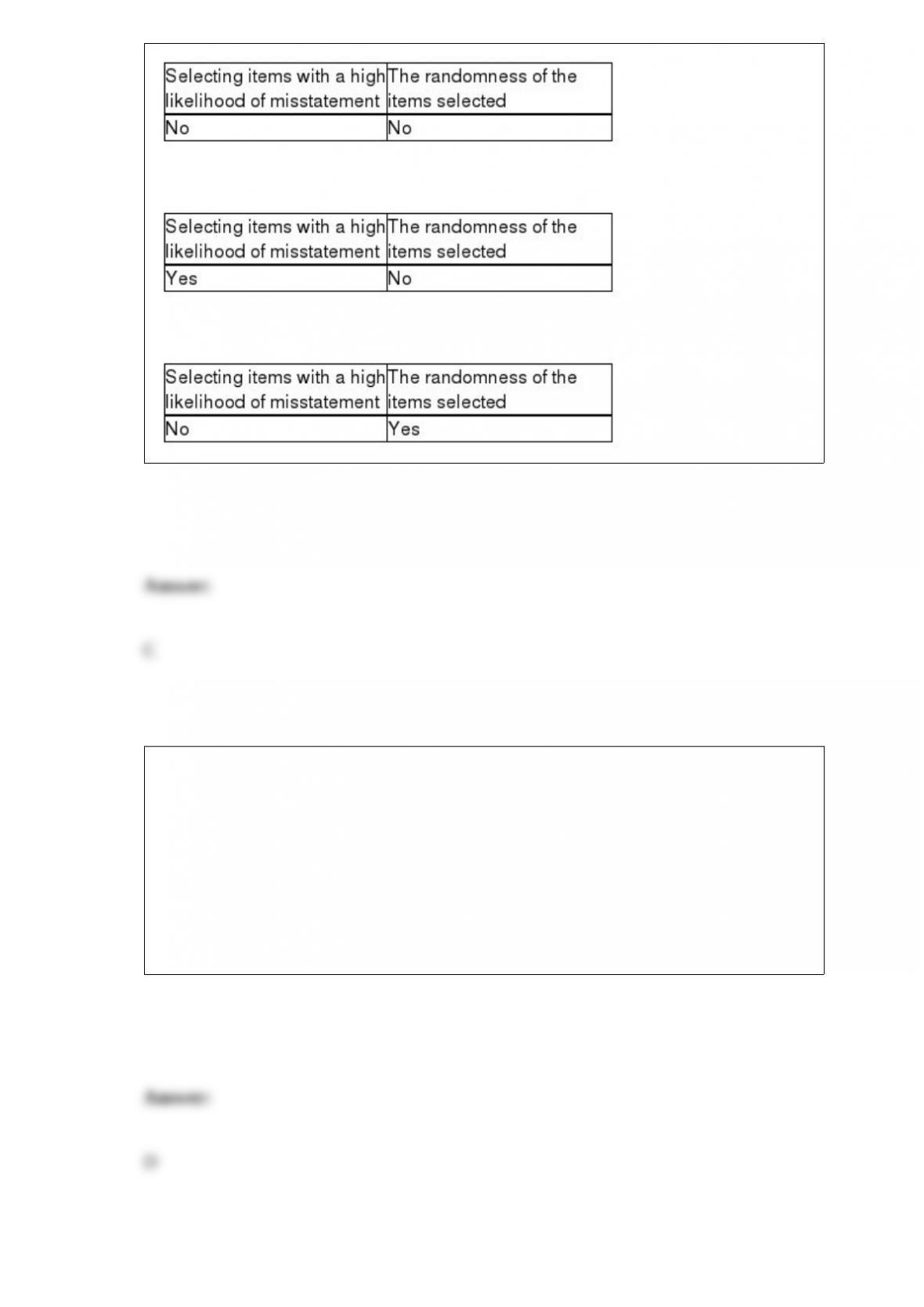

Which items affect the sufficiency of evidence when choosing a sample?

A)

B)

C)

D)

Which of the following must be set prior to testing a sample?

A) sample exception rate

B) achieved upper precision limit

C) computed exception rate

D) tolerable exception rate

Interpretations to the Rules of Conduct permit a CPA firm to do both bookkeeping and

auditing for the same private company client if three criteria are met. Which of the

following is not one of those criteria?

A) The client must accept full responsibility for the financial statements.

B) The client is required to file an annual report, including audited financial statements,

with the Securities and Exchange Commission.

C) The CPA must not assume the role of employee or of manager.

D) The CPA must follow applicable auditing standards.

Items that materially affect the comparability of financial statements generally require

disclosure in the footnotes. If the client refuses to properly disclose the item, the auditor

will most likely issue

A) a disclaimer.

B) an unqualified opinion.

C) a qualified opinion.

D) an adverse opinion.

The accurate recording of sales transactions concerns all of the following except for

A) proper credit authorization.

B) shipping the amount of goods ordered.

C) accurately billing for the amount of goods shipped.

D) accurately recording the amount billed in the accounting records.

In most manufacturing companies, the inventory and warehousing cycle begins with the

A) receipt of a customer’s order.

B) completion of production of a customer’s order.

C) initiation of production of a customer’s order.

D) acquisition of raw materials for production.

Relating to opportunities, why do most people commit fraud?

A) They need to fund an extravagant lifestyle.

B) They feel a sense of superiority.

C) There are weak internal controls.

D) They need to meet pre-specified business targets.

When performing the review and completing the documentation and rationale for the

conclusion step of the professional judgment process, auditors will

A) consider the accounting and auditing standards relevant to the issues.

B) articulate in written form the rationale of their judgment.

C) identify the issue.

D) gather the facts.

Which of the following controls prevent and detect errors while transaction data are

processed?

A) software

B) application

C) processing

D) transaction

Auditors test the quantity of materials charged to work-in-process by tracing these

quantities to

A) cost ledgers.

B) perpetual inventory records.

C) receiving reports.

D) material requisitions.

The positive (as opposed to the negative) form of receivables confirmation may be

preferred when

A) internal control surrounding accounts receivable is considered to be effective.

B) there is reason to believe that a substantial number of accounts may be in dispute.

C) a large number of small balances are involved.

D) the auditor believes that the recipients of the confirmations will give the requests

adequate consideration.

Which of the following audit tests both have the effect of simultaneously verifying

balance sheet and income statement accounts?

A) analytical procedures and substantive tests of transactions

B) tests of controls and substantive tests of transactions

C) tests of details of balances and substantive tests of transactions

D) tests of controls and analytical procedures

The auditor traces inventory tags identified as non-owned during the physical

observation to the inventory listing schedule to make sure these have not been included.

This test satisfies the balance-related audit objective of

A) cutoff.

B) rights.

C) accuracy.

D) existence.

When comparing misstatements with a measurement base, the auditor must consider the

pervasiveness of the misstatement. Of the following examples, the most pervasive

misstatement is a(n)

A) understatement of inventory.

B) understatement of retained earnings caused by a miscalculation of dividends

payable.

C) misclassification of notes payable as a long-term liability when it should be current.

D) misclassification of salary expense as a selling expense.

Failure to record the acquisition of goods is a violation of which audit objective?

A) accuracy

B) occurrence

C) authorization

D) completeness

The highest level of materiality exists when

A) users are likely to make incorrect decisions if they rely on the overall financial

statements.

B) there has been a departure from GAAP.

C) amounts are material but do not overshadow the financial statements as a whole.

D) a scope limitation has been imposed.

The highest level of assurance is provided for in which one of the following

engagements?

A) review

B) compilation

C) audit

D) preparation service

In connection with a review of the prepaid insurance account, which of the following

audit procedures would you be least likely to use?

A) Recompute the portion of the premium that expired during the year.

B) Prepare excerpts of insurance policies for audit working papers.

C) Confirm premium rates with an independent insurance broker.

D) Examine support for premium payments.

Auditors often use the ________ to determine the estimated population exception rate.

A) current year’s audit results

B) tolerable exception rate

C) preceding year’s audit results

D) estimated computed by management

Quality control for a CPA firm

A) includes the organizational structure of the firm and the procedures it establishes.

B) is tailored to each specific audit engagement.

C) is a guarantee that auditing standards are followed.

D) is required only for firms auditing SEC companies.

In searching for unrecorded liabilities the purpose of the audit procedure to “examine

underlying documentation for subsequent cash disbursements” is to

A) uncover liabilities on the balance sheet which should not have been recorded until a

subsequent period.

B) find the documentation relating to a cash disbursement.

C) uncover payments made in a subsequent accounting period for liabilities that existed

at the balance sheet date.

D) uncover cash disbursements recorded in a subsequent accounting period which

should be recorded in this period.

Who is responsible for establishing auditing standards for privately held companies?

A) Securities and Exchange Commission

B) Public Company Accounting Oversight Board

C) Auditing Standards Board

D) National Association of Accounting

If the auditor believes that the financial statements are not fairly stated or is unable to

reach a conclusion because of insufficient evidence, the auditor

A) should withdraw from the engagement.

B) should request an increase in audit fees so that more resources can be used to

conduct the audit.

C) has the responsibility of notifying financial statement users through the auditor’s

report.

D) should notify regulators of the circumstances.

From which of the following evidence-gathering audit procedures would an auditor

obtain most assurance concerning the existence of inventories?

A) observation of physical inventory counts

B) written inventory representations from management

C) confirmation of inventories in a public warehouse

D) auditor’s recomputation of inventory extensions

When verifying if capital stock is accurately recorded,

A) the ending balance in the account does not need to verified.

B) the number of shares outstanding at the balance sheet date is verified by examining

the corporate minutes.

C) the recorded par value can be determined by multiplying the number of shares by the

market price of the stock.

D) a confirmation from the transfer agent is the simplest way to verify the number of

shares outstanding at the balance sheet date.

If a population is not considered acceptable, and the analysis indicates an individual

error is unique or most of the misstatements are of a specific type, it may be appropriate

to restrict the additional audit effort to the problem area.