23-1

Chapter 23

Audit of Cash and Financial Instruments

Concept Checks

P. 748

1. The appropriate tests for the ending balance in the cash accounts depend

heavily on the initial assessment of control risk, tests of controls, and

cutoff at year–end is proper. If the results of the evaluation of internal control,

the tests of controls, and the substantive tests of transactions are adequate,

year–end testing may be necessary.

An example in which the conclusions reached about the controls in cash

disbursements would affect the tests of cash balances would be:

bank reconciliation may be greatly reduced. The year–end outstanding

checks can be verified by testing a sample of checks returned with the

2. The monthly reconciliation of bank accounts by an independent person

is an important internal control over cash balances because it provides an

opportunity for an internal verification of the cash receipts and cash

disbursements transactions, investigation of reconciling items on the

23-2

P. 727

1. An auditor compares the “date of deposit according to the books” to the

“date of disbursement according to the books” to detect kiting carried out by

the payroll account on December 31, but does not record the

disbursement out of the general checking account until January 1, the

record the cash disbursement. When comparing the dates of deposit and

disbursement, the auditor is looking to ensure both were recorded in the

schedule.

2. Accounting standards related to fair value estimates make the audit of

these estimates difficult due to the significant amount of management

judgment involved. Management first applies judgment to determine

whether the fair value estimate will be a level 1, 2, or 3 estimate. If the fair

Review Questions

23–1 The appropriate tests for the ending balance in the cash accounts

of transactions are adequate, it is appropriate to reduce the tests of details of

balances for cash, especially for the detailed tests of bank reconciliations. On

the other hand, if the tests indicate that the client’s controls are deficient,

extensive year–end testing may be necessary.

23-3

Copyright © 2017 Pearson Education, Inc.

23–2 An imprest bank account for a branch operation is one in which a fixed

balance is maintained. After authorized branch personnel use the funds for proper

disbursements, they make an accounting to the home office. After the expenditures

have been approved by the home office, a reimbursement is made to the

branch account from the home office’s general account for the total of the cash

disbursements. The purpose of using this type of account is to provide controls

over cash receipts and cash disbursements by preventing the branch operators

from disbursing their cash receipts directly, and by providing review and

approval of cash disbursements before more cash is made available.

include the following:

a. Examination of all checks clearing with the statement (including

those on the previous month’s outstanding check list) and

comparison of payee and amount to the cash disbursements journal.

reasonable amount of time.

c. Follow–up on old outstanding checks to determine why they are

still outstanding.

23–4 Bank confirmations differ from positive confirmations of accounts

1. The balances in all bank accounts.

2. Restrictions on withdrawals.

3. The interest rate on interest–bearing accounts.

4. Information on liabilities to the bank for notes, mortgages, or other

debt.

Positive confirmations of accounts receivable request the customer to

confirm an account balance stated on the confirmation form or designate a

different amount with an explanation. The auditor anticipates few exceptions to

accounts receivable confirmations, whereas with bank confirmations he expects

differences between the balance per bank and balance per the books that the

client must reconcile. Bank confirmations should be requested for all bank

23-4

23–4 (continued)

The reason why more importance is placed on bank confirmations than

accounts receivable confirmations is that cash, being the most liquid of assets,

must be more closely controlled than accounts receivable. In addition, other

23–5 This is a good auditing procedure that attempts to discover if any

23–6 A cutoff bank statement is a partial period bank statement with the

related cancelled checks, duplicate deposit slips, and other documents included

in bank statements, which is mailed by the bank directly to the auditor. Rather

23–7 Auditors are usually less concerned about the client’s cash receipts cutoff

than the cutoff for sales, because the cutoff of cash receipts affects only cash

For the purpose of detecting a cash receipt cutoff misstatement, there

are two useful audit procedures. The first is to trace the deposits in transit to the

cutoff bank statement to determine the date they were deposited in the bank

account. Because the recorded cash will have to be included as deposits in

transit on the bank reconciliation, the auditor can test for the number of days it

whether the deposits in transit equal the amount recorded.

23–8 The misstatements that are of the greatest concern to auditors in bank

reconciliations are intentional ones to cover up a cash shortage, usually resulting

balance, a highly unlikely occurrence.

23-5

Copyright © 2017 Pearson Education, Inc.

23–9 This question deals with a situation where a company’s bank received

an electronic deposit of cash from credit card agencies making payments on

behalf of customers purchasing products from the company’s online Web site.

The company does not have the electronic deposit recorded in the general

ledger. The company’s bank reconciliation should include an adjustment for this

transaction, which would increase the book balance of cash and decrease

accounts receivable from credit card agencies.

23–10 The purpose of the four–column proof of cash is to verify:

Whether all recorded cash receipts were deposited.

records.

Whether all recorded cash disbursements were paid by the bank.

to uncover are:

Cash received that was not recorded in the cash receipts journal.

Checks that cleared the bank but have not been recorded in the

cash disbursements journal.

shifting of shortages from account to account and the crediting of subsequent

receipts to the wrong accounts receivable.

Kiting is a procedure used to conceal cash shortages from employers

and auditors, to conceal bank overdrafts from the bank or banks affected, or to

and the shortage “reappears” unless the process is repeated.

If a depositor desires to write a check for which he does not have funds

on deposit, he can deposit a transfer check large enough to cover the payment,

even though the transfer check itself creates an overdraft. The transfer process

23-6

23–11 (continued)

Kiting to pad a cash position typically occurs at the end of a fiscal

The following audit procedures would be used to uncover lapping:

Confirm accounts receivable and give close attention to

exceptions made by customers about payment dates. The

confirmation procedure is better applied as a surprise at an interim

The deposit of these funds should be made under the auditor’s

control, and the details of the deposit should later be compared

with the cash receipts book and the accounts receivable records.

Compare the details of remittance lists (if prepared), stamped

Compare the check vouchers received with the customers’ checks

with stamped duplicate deposit slips, the entries in the cash book,

Kiting might be uncovered by the following audit procedures:

As a surprise count of cash and customers’ checks on hand is

made as a test for lapping, determine that checks representing

bank statements.

23-7

23–11 (continued)

on the books. Protested (N.S.F.) checks should be investigated to

determine they are not fictitious checks deposited temporarily to

cover a shortage.

This emphasis affects the auditor’s evidence accumulation in auditing

year–end cash as in these examples:

Verifying whether cash transactions are properly recorded

Testing of bank reconciliations

Obtaining bank confirmations

the model used and the reasonableness of estimates. This will require judgment

on the auditor’s part as well as knowledge of valuation techniques and the

market factors that affect assumptions used (e.g., liquidity risk, credit risk, interest

rate risk). The auditor can develop an independent estimate to corroborate the

and compare this to management’s estimate.

If the fair value of the financial instrument has declined, the auditor

must consider whether the financial instrument is other–than–temporarily impaired,

which would require recognition of an impairment loss. This assessment is also

Multiple Choice Questions From CPA Examinations

23–14 a. (4) b. (3) c. (2)

23–15 a. (2) b. (4) c. (2)

23–16 a. (3) b. (2) c. (2)

Discussion Questions and Problems

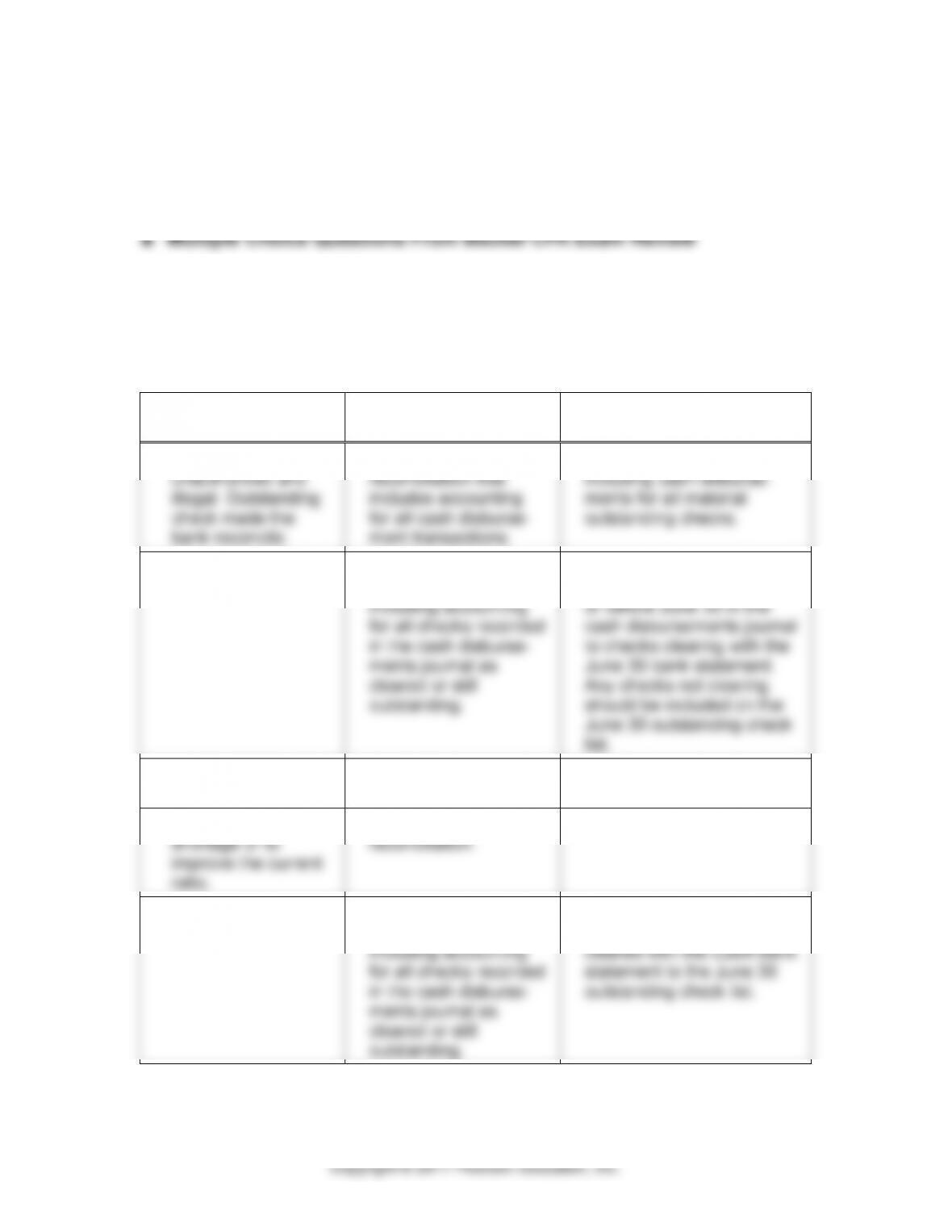

23–17

a.

MOTIVATION

b.

INTERNAL CONTROL

c.

AUDIT PROCEDURE

1. Original check was

unauthorized and

illegal. Outstanding

check made the

bank reconcile.

Independent bank

reconciliation that

includes accounting

for all cash disburse–

ment transactions.

Verify the bank reconciliation,

including cash disburse–

ments for all material

outstanding checks.

2. To cover a shortage.

Internal verification of

bank reconciliation,

including accounting

for all checks recorded

in the cash disburse–

ments journal as

cleared or still

outstanding.

Verify the bank reconciliation

by tracing checks dated on

or before June 30 in the

cash disbursements journal

to checks clearing with the

June 30 bank statement.

Any checks not clearing

should be included on the

June 30 outstanding check

list.

3. To cover a shortage.

Internal verification of

bank reconciliation.

Foot outstanding check list.

4. To cover a cash

shortage or to

improve the current

ratio.

Independent bank

reconciliation.

Obtain bank confirmation.

5. To cover a shortage.

Internal verification of

bank reconciliation,

including accounting

for all checks recorded

in the cash disburse–

ments journal as

cleared or still

outstanding.

Trace all checks dated on

or before June 30 that

cleared with the cutoff bank

statement to the June 30

outstanding check list.

23-9

23-17 (continued)

6. Hold open books

to improve cash

position.

Independent bank

reconciliation.

Trace deposits in transit to

cutoff bank statements to

determine deposit date.

7. Kiting–covering

a defalcation or

padding a cash

position.

Independent bank

reconciliation.

Trace all interbank transfers

to accounting records.

in preparing its reconciliation.

3. To create a list of outstanding checks for follow–up to determine

why they have not cleared and to investigate the possibility of a

misstatement of cash and accounts payable.

4. To assure that all loans, terms, and arrangements with the bank

disclosed in the financial statements.

5. To reconcile the recording of cash receipts and cash disbursements

between the bank and the client’s books and to prepare a bank

misstatement.

8. To verify the valuation of the equity investment.

23-10

23–19 a. Bank reconciliation:

Balance per bank $ 1,522

Add:

Deposits in transit 2,000

Check erroneously charged to Pittsburgh Supply 646

Less: outstanding checks (2,218)

(1) 6/30 DIT 600

July deposits per books 26,874

July deposits per bank (25,474 )

7/31 DIT $ 2,000

(2) 6/30 O/S checks $ 2,578

b. Adjusting entry:

Miscellaneous expense $ 107

Interest expense 400

Note payable 6,000

To record adjustments arising from

7/31/16 bank reconciliation.

cash disbursements journal.