The primary concern in determining whether retained earnings is correctly disclosed on

the balance sheet is

A) correct calculation of the net income or loss for the year.

B) correct calculation of dividend payments for the year.

C) whether prior-period adjustments have been made correctly.

D) whether there are any restrictions on the payment of dividends.

Which type of supporting schedule is designed to show the activity in a general ledger

account during the entire period under audit?

A) trial balance

B) reconciliation of amounts

C) summary of procedures

D) analysis

An accountant has accepted an engagement in which the audit procedures of inquiry

and analytical procedures will be employed. These procedures will form the basis for

issuance of

A) a compilation report.

B) an audit report on supplemental information issued by the client.

C) a management advisory report requested by the audit committee.

D) a review report on financial statements for a nonpublic company.

The usual audit test for a public company’s officer compensation is to obtain the

authorized salary of each officer from the minutes of the board of directors and compare

it with

A)

B)

C)

D)

When there are not numerous transactions involving notes payable during the year, the

normal starting point for the audit of notes payable is

A) a schedule of notes payable and accrued interest prepared by the audit team.

B) a schedule of notes payable and accrued interest obtained from the client.

C) a schedule of only those notes with unpaid balances at the end of the year prepared

by the client.

D) the notes payable account in the general ledger.

When the auditor has completed the tests of details of balances and enters phase IV of

the audit process, she must still perform audit procedures for which of the following?

A) contingent liabilities and employee compensation

B) contingent liabilities and subsequent events

C) subsequent events and contractual commitments

D) subsequent events and unrecorded liabilities

Which of the following is the auditor least likely to do when aware of an illegal act?

A) discuss the matter with the client’s legal counsel

B) obtain evidence about the potential effect of the illegal act on the financial

statements

C) contact the local law enforcement officials regarding potential criminal wrongdoing

D) consider the impact of the illegal act on the relationship with the company’s

management

When taken together, the concepts of risk and materiality in auditing

A) measure the uncertainty of amounts of a given magnitude.

B) measure uncertainty only.

C) measure magnitude only.

D) measure inherent risk.

Match seven of the terms for documents and records (a-m) used in the acquisitions and

cash disbursement cycle with the descriptions provided below (1-7):

a. purchase requisition

b. purchase order

c. receiving report

d. acquisitions journal

e. summary acquisitions report

f. vendor’s invoice

g. debit memo

h. voucher

i. accounts payable master file

j. accounts payable trial balance

k. vendor’s statement

l. check

m. cash disbursements journal

________ 1. a document indicating a reduction in the amount owed to a vendor because

of returned goods or an allowance granted

________ 2. a document received from the vendor which shows the amount owed for

an acquisition

________ 3. a document prepared by the purchasing department indicating the

description, quantity, and related information for goods and services that the company

intends to purchase

________ 4. a listing of the amount owed to each vendor at a point in time

________ 5. a document used to establish a formal means of recording and controlling

acquisitions; it includes a cover sheet and a package of relevant documents

________ 6. a document used to request goods and services by an authorized employee

________ 7. the listing or report that includes all cash payments for a given period

Which of the following best describes the test data approach?

A) Auditors process their own test data using the client’s computer system and

application program.

B) Auditors process their own test data using their own computers that simulate the

client’s computer system.

C) Auditors use auditor-controlled software to do the same operations that the client’s

software does, using the same data files.

D) Auditors use client-controlled software to do the same operations that the client’s

software does, using auditor created data files.

An auditor who issues a qualified opinion because sufficient appropriate evidence was

not obtained should describe the limitations in an explanatory paragraph. The auditor

should also modify the

A)

B)

C)

D)

When planning the audit sample,

A) one objective of the tests of controls is to test the effectiveness of the controls.

B) audit sampling applies to analytical procedures.

C) audit sampling generally applies to automated controls.

D) the auditor must generalize from the sample to the population.

In the performance of an audit, a CPA

A) is legally liable for detecting an immaterial client fraud.

B) must strictly follow GAAP for privately held clients.

C) must exercise constructive professional care in the performance of their audit

responsibilities.

D) must exercise due professional care in the performance of their audit responsibilities.

Lewis Corporation has a few large accounts receivable that total one million dollars,

whereas Clark Corporation has many small accounts receivable that total one million

dollars. Misstatement in any one account is more significant for Lewis corporation

because of the concept of

A) materiality.

B) audit risk.

C) reasonable assurance.

D) comparative analysis.

According to a KPMG survey, most fraud perpetrators

A) are over the age of 65.

B) work on the assembly line.

C) have worked for the company for over ten years.

D) are female.

Which one of the following procedures would not be appropriate for an auditor in

discharging his responsibilities concerning the client’s physical inventories?

A) confirmation of goods in the hands of public warehouses

B) supervising the taking of the annual physical inventory

C) carrying out physical inventory procedures at an interim date

D) obtaining written representation from the client as to the existence, quality, and

dollar amount of the inventory

Which of the following sampling plans would be designed to estimate a numerical

measurement of a population, such as a dollar value?

A) numerical sampling

B) discovery sampling

C) attributes sampling

D) variables sampling

________ are referred to as U.S. generally accepted auditing standards (GAAS).

A) AICPA auditing standards

B) SEC auditing standards

C) PCAOB auditing standards

D) Sarbanes-Oxley standards

________ materiality is materiality for segments of the audit.

A) Segment

B) Individual

C) Financial statement

D) Performance

“Physical examination” is the inspection or count by the auditor of items such as

A) cash, inventory, and payroll timecards.

B) cash, inventory, canceled checks, and sales documents.

C) cash, inventory, canceled checks, and tangible fixed assets.

D) cash, inventory, securities, notes receivable, and tangible fixed assets.

Two key concepts that underlie management’s design and implementation of internal

control are

A) costs and materiality.

B) absolute assurance and costs.

C) inherent limitations and reasonable assurance.

D) collusion and materiality.

To determine if notes payable are included in the proper period, the auditor should

A) trace the cash received from the issuance to the accounting records.

B) examine duplicate copies of notes to determine whether the notes were dated on or

before the balance sheet date.

C) examine duplicate copies of notes for principal and interest rates.

D) trace the individual notes payable to the master file.

The advantage of systematic sample selection is that

A) it is easy to use.

B) there is limited possibility of it being biased.

C) it is unnecessary to determine if the population is arranged randomly.

D) it automatically selects items material to the financial statements.

The permanent audit file would usually include the

A) client’s working trial balance.

B) summary of the risk assessment procedures performed.

C) organizational chart of the company’s employees.

D) summary of the auditors test of controls for the current years audit.

Which of the following is least likely to uncover fraud?

A) external auditors

B) internal auditors

C) internal controls

D) management

The auditor determines that Matthews Company occupies the 3rd floor of an office

tower for which it pays no rent. The most likely explanation is

A) they got lucky the landlord hasn’t noticed the lack of payments.

B) the landlord has weak internal controls over billings.

C) a related party transaction in which a major shareholder owns the office tower.

D) Matthews Company is engaging in fraudulent activities.

To determine if a sample is truly representative of the population, an auditor would be

required to

A) conduct multiple samples of the same population.

B) never use sampling because of the expense involved.

C) audit the entire population.

D) use systematic sample selection.

Membership in the AICPA can be terminated without a hearing for

A) a crime punishable by imprisonment for more than one year.

B) the filing of a fraudulent income tax return on a client’s behalf.

C) the willful failure of a CPA to file their own personal tax return.

D) all of the above.

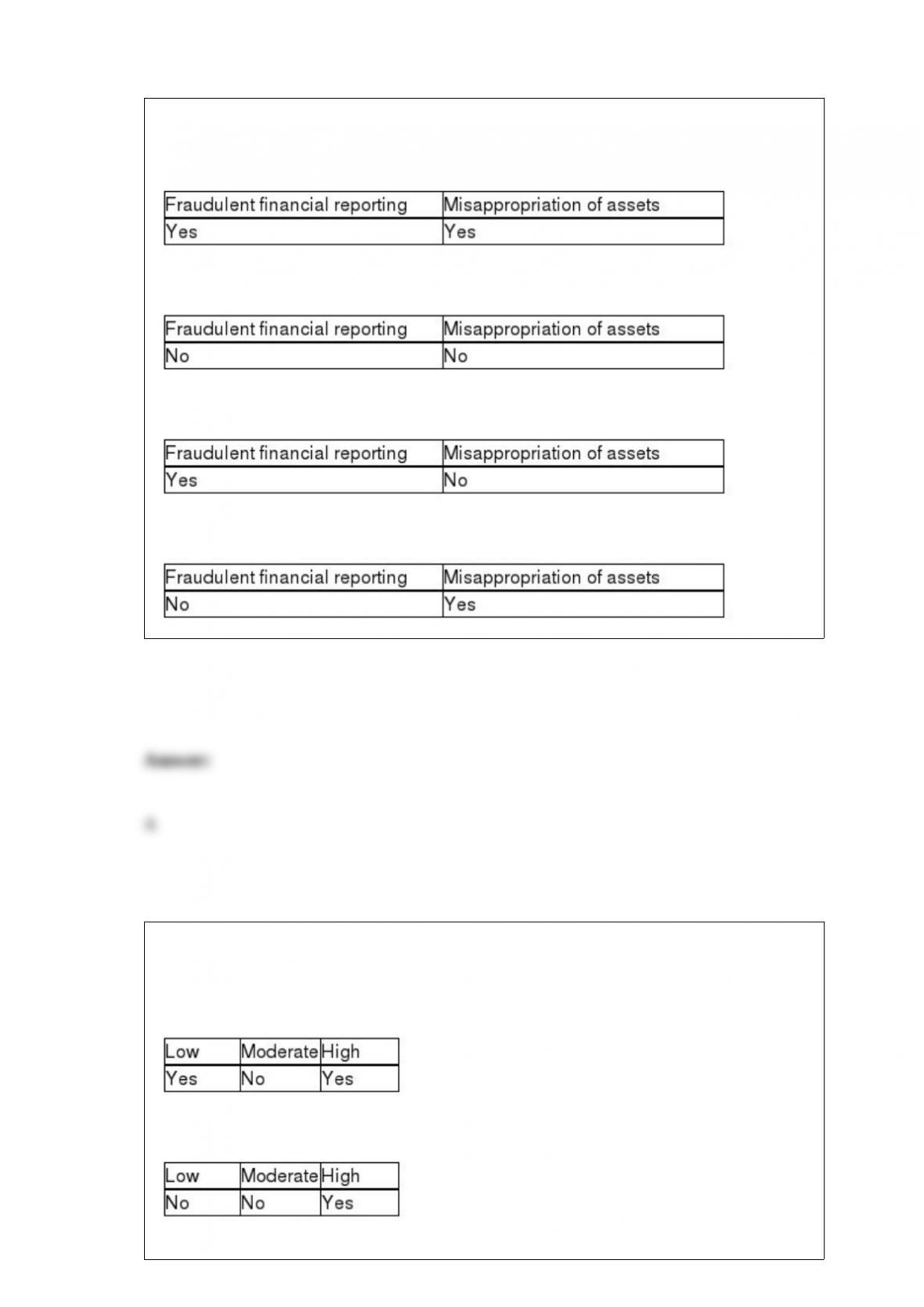

Which of the following is a category of fraud?

A)

B)

C)

D)

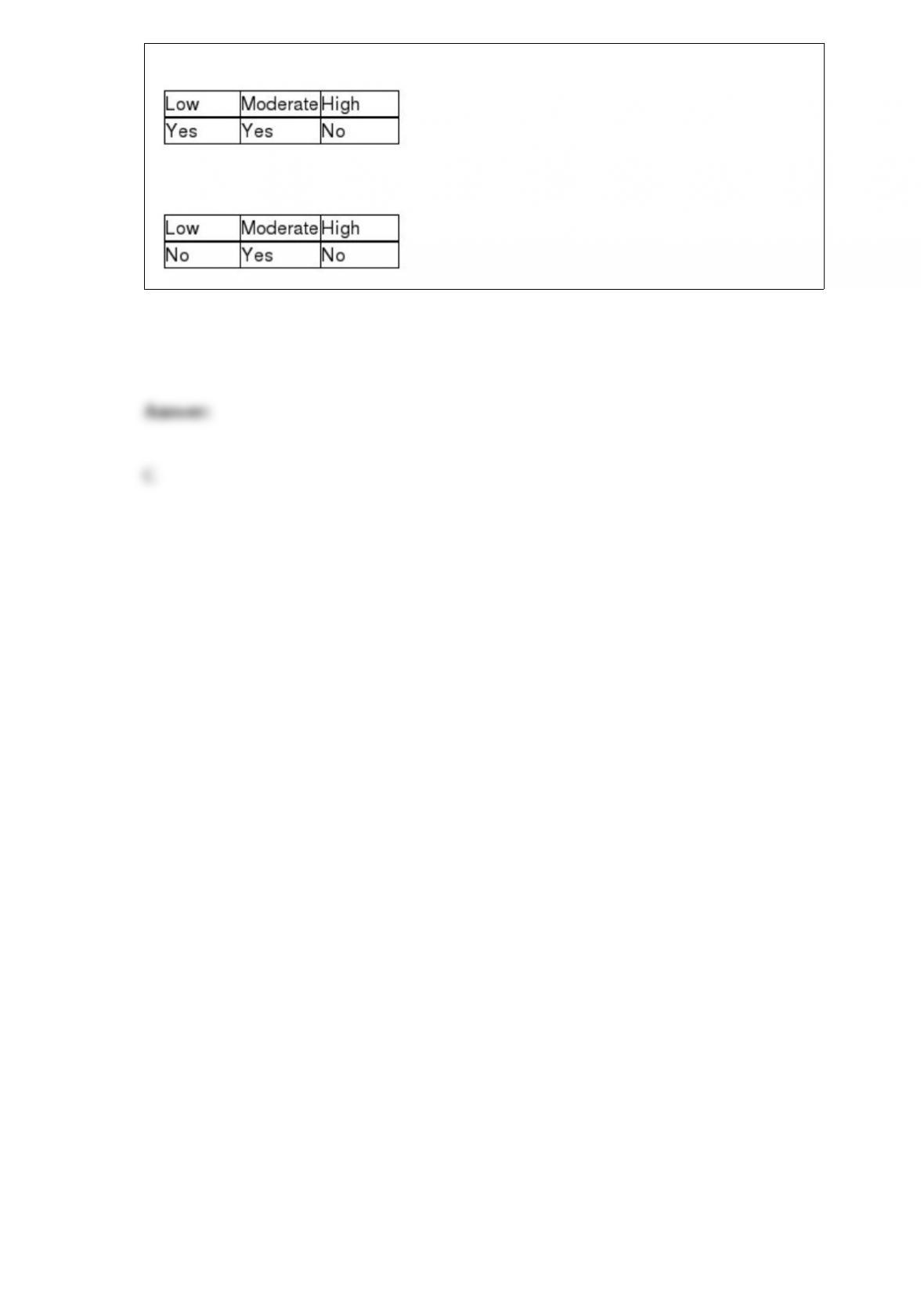

In the audit of a private company, the auditor will test internal controls when control

risk is initially assessed at

A)

B)

C)

D)