A primary concern in reporting on a comprehensive basis is to make sure that the

statements clearly indicate that they are prepared on a basis other than GAAP.

Cutoff for acquisitions of insurance is normally not a significant problem for the

auditors.

Failure to record the acquisition of goods and services received overstates both

accounts payable and net income.

Auditors should issue a disclaimer of opinion when there is a highly material

client-imposed scope restriction.

Acceptable risk of incorrect rejection is the statistical risk that the auditor has concluded

that a population is materially misstated when it is not.

When performing a review of interim information for a public company, the accountant

ordinarily does not perform tests of the accounting records, independent confirmations,

or physical examinations.

Results of compliance audits are typically reported to the company’s management rather

than to a broad spectrum of outside users.

For good internal control, the payroll function should be independent of the human

resources department.

A lawsuit has been filed against your client. If, in the opinion of legal counsel, the

likelihood your client will lose the lawsuit is remote, no financial statement accrual or

disclosure of the potential loss would generally be required.

The Internal Auditing Standards Board issues Statements on Internal Auditing

Standards.

The audit procedure “Review the notes to determine whether any are related party notes

or accounts payable” is performed when verifying the classification objective for notes

payable.

The AU-C number identifies the order in which it was issued in relation to all other

codified auditing standards.

Most accrued liabilities can be identified by the existence of vendors’ invoices for the

obligation.

The Sarbanes-Oxley Act requires the CEO and CFO of a public company to certify the

annual and quarterly financial statements filed with the PCAOB.

Any restrictions on the payment of dividends must be disclosed in the footnotes to the

financial statements.

Auditors are not allowed to make inquires of employees who are not considered

management, such as marketing or sales personnel.

The sales and collection cycle applies to businesses that sell goods to customers or

provide services to customers.

Acceptable risk of overreliance is normally lower for a public company audit than a

private company audit.

The phrase “auditing standards generally accepted in the United States of America” can

be found in the opinion paragraph of a standard unmodified opinion report for a

nonpublic company.

Balance-related audit objectives follow from management assertions.

Auditors should provide debt compliance letters only for clients for whom the auditor

has done an audit of the overall financial statements.

Tests of details of balances emphasize the overall reasonableness of transactions and the

general ledger balances.

A prior period adjustment may result in a debit or credit to a company’s retained

earnings account.

Auditors should determine whether the client has fulfilled its legal obligation in

submitting payments of all payroll withholdings as part of their payroll tests.

Auditors use trends in the inventory turnover ratio to identify potential inventory

obsolescence.

In order to be meaningful, a company’s ratios should be compared to their prior year’s

ratios, not industry benchmarks.

An advantage of specific rules in the Code of Professional Conduct is the enforceability

of minimum behavior and performance standards.

To perform an audit, there must be information in a verifiable form and some criteria by

which the auditor can evaluate the information.

If an auditor believes the client will have financial difficulties after the audit report is

issued, and external users will be relying heavily on the financial statements, the auditor

will probably set acceptable audit risk as low.

Auditor judgment is the primary determinant in determining the amount of evidence

gathered.

For most audits, revenue recognition is considered to be a significant risk.

When labor is a material part of inventory valuation, auditors should emphasize testing

internal controls over proper classification of payroll transactions.

In the AICPA Code of Professional Conduct, the sixth principle of professional conduct,

entitled “Scope and Nature of Services,” applies to members of the AICPA who work in

public practice, business, government, or education.

IT controls are classified as either input controls or output controls.

The audit procedure “foot the schedule of fixed assets acquisitions and trace the total to

the general ledger” relates most closely to the completeness objective for fixed assets

acquisitions.

When an auditor reviews the financial statements to determine if assets are properly

classified between current and noncurrent, he is satisfying the audit objective of

occurrence and rights and obligations.

When analytical procedures in the sales and collection cycle uncover unusual

fluctuations, the auditor should make additional inquiries of management.

Balance-related audit objectives are usually applied to the ending balance in income

statement accounts; transaction-related audit objectives are usually applied to

transactions reflected in balance sheet accounts.

Which of the following is not a characteristic of a small firm?

A) Most small firms have fewer than 25 professionals.

B) Small firms perform audits on small and not-for-profit businesses.

C) Tax services are more important than auditing services to the small firm.

D) Small firms are prohibited by the SEC from auditing publicly traded companies.

The document used to indicate to the customer the amount of a sale and payment due

date is the

A) sales invoice.

B) bill of lading.

C) purchase order.

D) sales order.

A major difficulty in the verification of inventory cost records for the purpose of

inventory valuation is in determining the reasonableness of the

A) direct labor costs.

B) raw material costs.

C) manufacturing overhead costs.

D) period costs.

Industry comparisons can be used as

A) an aid to understanding the client’s business.

B) an indicator of errors.

C) an indicator of fraud.

D) an aid to internal controls.

The primary concern in testing payroll-related liabilities is to make sure that

A) accruals are properly valued.

B) transactions are recorded in the proper period.

C) there are no understated or omitted accruals.

D) the accruals are not overstated.

As a part of the auditor’s responsibility for ________, the auditor should review the

preparation of at least one of each type of payroll tax form the client is responsible for

filing.

A) fraud awareness

B) doing tests of balances

C) doing tests of transactions

D) understanding the client’s internal controls

The source of debits in the equipment account is the

A) sales schedule.

B) cash disbursements journal.

C) cash receipts journal.

D) acquisitions schedule.

The measurement of the auditor’s assessment of the susceptibility of an assertion to

material misstatement, before considering the effectiveness of related internal controls

is defined as

A) audit risk.

B) inherent risk.

C) sampling risk.

D) detection risk.

As the auditor, you are assessing the proper sample size to use in testing controls. When

using attributes sampling, which of the following is most correct?

A) A 10% change in population size will have the least effect on sample size.

B) A 10% change in the tolerable deviation rate will have the least effect on sample

size.

C) A 10% change in the expected deviation rate will have the least effect on sample

size.

D) A 10% change in the tolerable will have the least effect on sample size.

Which of the following misstatements is most likely to be uncovered during an audit of

a client’s bank reconciliation?

A) duplicate payment of a vendor’s invoice

B) billing a customer at a lower price than indicated by company policy

C) failure to record a collection of a note receivable by the bank on the client’s behalf

D) payment to an employee for more than the hours actually worked

Which of the following is one of the main differences between attributes sampling and

nonstatistical sampling?

A) the number of steps involved

B) the calculation of the initial sample sizes

C) determining the objectives of the audit test

D) defining the population

Which of the following statements regarding inherent risk is correct?

A) Inherent risk is unaffected by the auditor’s experience with client’s organization.

B) Most auditors set a low inherent risk in the first year of an audit and increase it if

experience shows that it was incorrect.

C) Most auditors set a high inherent risk in the first year of an audit and reduce it in

subsequent years as they gain more knowledge about the company.

D) Inherent risk is dependent upon the strengths in client’s internal control system.

When a population is divided into subpopulations, usually by dollar size, and larger

samples are taken from the subpopulation with the larger sizes, ________ is being used.

A) sampling with probability proportional to size

B) stratified sampling

C) block sampling

D) haphazard sampling

The quarterly reports submitted to the SEC by the client

A) have to be audited and the CPA firm must be identified.

B) do not have to be audited, but the CPA firm which does the annual audit must be

identified.

C) have to be audited, but the CPA firm does not have to be identified.

D) do not have to be audited, but the CPA firm which does the annual audit must review

the quarterly statements before they are submitted to the SEC.

While performing a substantive test of details during an audit, the auditor determined

that the sample results supported the conclusion that the recorded account balance was

materially misstated. Which of the following is theleast likely auditorreaction to this

discovery?

A) perform expanded audit tests in the relevant areas

B) increase detection risk in the relevant areas

C) increase the sample size

D) take no action until tests of other audit areas are completed

The expectation gap

A) exists between the auditor and the SEC.

B) exists because auditors guarantee the accuracy of the financial statements.

C) often results in unwarranted lawsuits against the auditor.

D) is a legal concept supported by the federal courts.

In order to properly plan and perform an audit, an important fact for both the auditor

and the client to understand is that

A) the internal control policies and procedures are developed by the auditors.

B) the purpose of an audit is to prevent fraud.

C) management is responsible for the preparation of the financial statements.

D) management can restrict the auditor’s access to important information relevant to the

financial statements.

For most audits, a proper cash receipts cutoff is less important than the sales cutoff

because the improper cutoff of cash

A) is detected and correct when cash is separately audited.

B) is unlikely to have a material impact on the balance sheet or the income statement.

C) affects items on the balance sheet but does not affect net income.

D) rarely occurs given the control consciousness of most entities.

Which of the following is an accurate statement regarding audit documentation review?

A) The audit partner must review the work of the least experienced auditor in more

detail than the work of the audit supervisor.

B) The audit senior must review all audit documentation.

C) For larger audits, it is common to have the financial statements and the entire set of

audit files reviewed by someone who has not participated in the audit, but is a member

of the audit firm doing the audit.

D) Checklists can never be used to verify that all financial statement disclosures have

been made.

When the auditor scans the sales journal looking for large and unusual transactions, he

is gathering what type of evidence?

A) inspection

B) recalculation

C) physical examination

D) analytical procedures

When using monetary unit sampling, evaluating the likelihood of unrecorded items in

the population is

A) unnecessary.

B) impossible.

C) possible but difficult.

D) an automatic outcome of the process.

In the context of an audit of financial statements, substantive tests are audit procedures

that

A) may be eliminated under certain conditions.

B) are designed to discover significant subsequent events.

C) are designed to test for dollar misstatements.

D) will increase proportionately with the auditor’s reliance on internal control.

Whenever auditors use sampling, they risk making incorrect conclusions about the

population. The risk that the auditor concludes that controls are more effective than they

actually are is known as the

A) risk of overreliance.

B) risk of underreliance.

C) risk that the sample is not representative of the population.

D) risk that the sample conclusions cannot be useful because of nonprobability

sampling.

Under PCAOB standards

A) the standard unmodified opinion audit report is referred to as an unqualified opinion

audit report.

B) the scope paragraph states that the financial statements are the responsibility of

management.

C) internal controls of a public company must be audited every five years.

D) the scope paragraph is the same as the scope paragraph for private companies.

General controls include all of the following except

A) systems development.

B) online security.

C) processing controls.

D) hardware controls.

Which of the following is the risk that an auditor will reach an incorrect conclusion

because a sample is not representative of the population?

A) sampling risk

B) nonsampling risk

C) audit risk

D) detection risk

The financial interests of a CPA’s family members can affect the CPA’s independence.

Which of the following parties would not be included as a “direct financial interest” of

the CPA?

A) spouse

B) dependent child

C) relative supported by the CPA

D) sibling living in the same city as the CPA

Internal controls can never be regarded as completely effective. Even if company

personnel could design an ideal system, its effectiveness depends on the

A) adequacy of the computer system.

B) proper implementation by management.

C) ability of the internal audit staff to maintain it.

D) competency and dependability of the people using it.

Match nine of the terms (a-k) with the definitions provided below (1-9):

a. foot

b. compute

c. scan

d. inquire

e. count

f. trace

g. reperform

h. read

i. examine

j. observe

k. compare

________ 1. a calculation done by the auditor independent of the client

________ 2. addition of a column of numbers to determine if the total is the same as the

client’s

________ 3. a comparison of information in two different locations

________ 4. a use of the senses to assess certain activities

________ 5. following details of transactions from original documents to journals

________ 6. a less detailed examination of a document or record to determine if there is

something unusual warranting further investigation

________ 7. obtaining information from the client in response to specific questions

________ 8. a determination of assets on hand at a given time

________ 9. an examination of written information to determine facts pertinent to the

audit

An auditor performs interim work at various times throughout the year. The auditor’s

subsequent events work should be extended to the date of

A) the auditor’s report.

B) a post-dated footnote.

C) the next scheduled interim visit.

D) the final billing for audit services rendered.

The classification balance-related audit objective

A) involves determining if items included on a client’s listing are included in the correct

general leger accounts.

B) is the counterpart to the management assertion of completeness.

C) involves determining if items included on a client’s listing are disclosed properly in

the financial statements.

D) involves tying in the account balances to the general ledger.

An auditor need not abide by a particular auditing standard if the auditor believes that

A) the issue in question is immaterial in amount.

B) more expertise is needed to fulfill the requirement.

C) the requirement of the standard has not been addressed by the PCAOB.

D) fraud is involved.

Which of the following statements about the Securities Act of 1933 is not true?

A) A third party that purchased securities described in the registration statement may

sue the auditor for material misrepresentations or omissions in the audited financial

statements.

B) A third party user does not have the burden of proof that he/she relied on the

financial statements.

C) A third party user has the burden of proof that the auditor was either negligent or

fraudulent in doing the audit.

D) A third party user does not have the burden of proof that the loss was caused by the

misleading statements.

Which of the following types of audit procedures is ordinarily emphasized the least

when auditing payroll?

A) tests of controls

B) tests of transactions

C) substantive analytical procedures

D) tests of details of balances

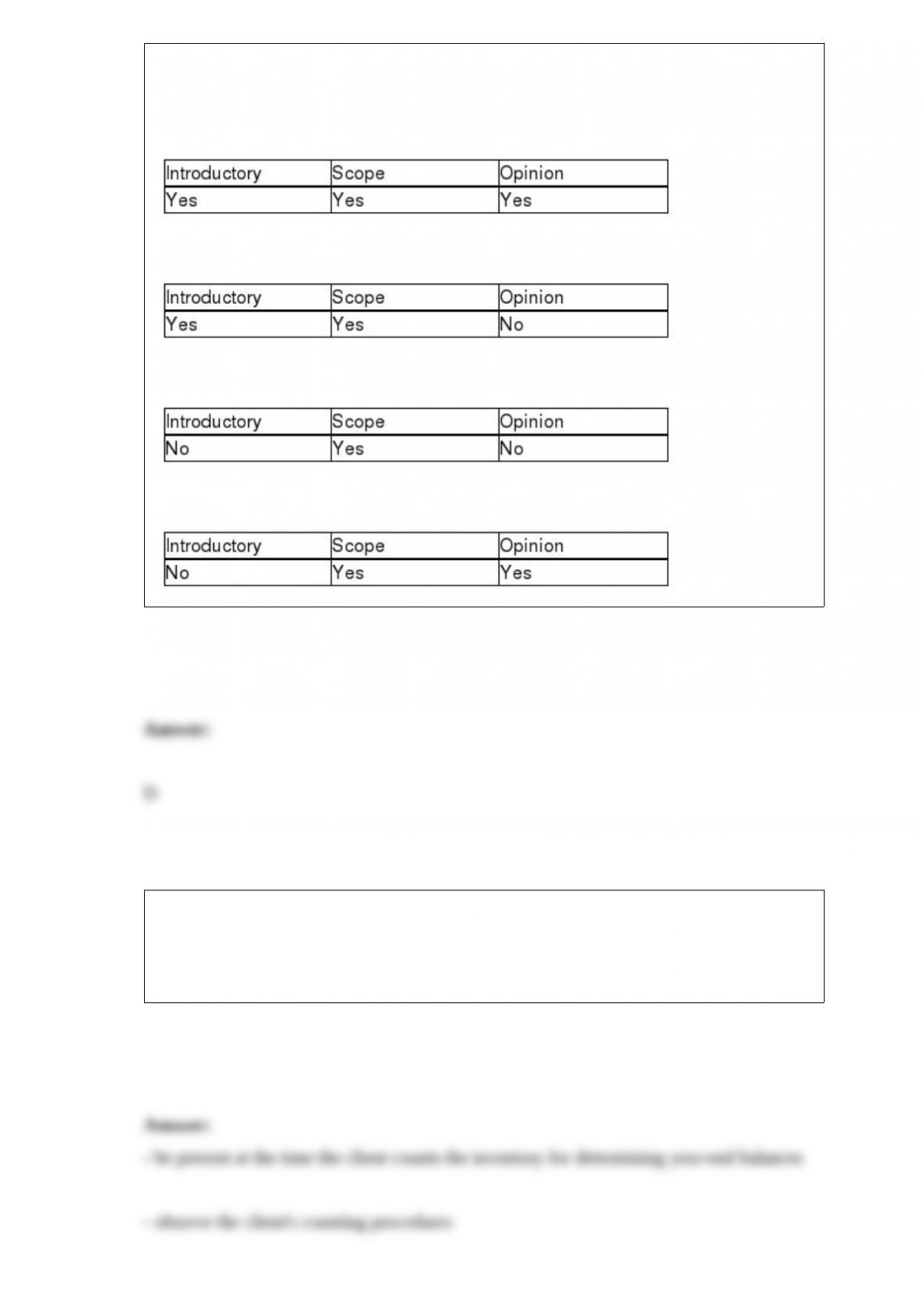

When an auditor issues a qualified report due to a scope limitation an explanatory

paragraph is normally added. Which, if any, of the following paragraphs are also

modified?

A)

B)

C)

D)

Auditing standards require that auditors satisfy themselves about the effectiveness of

the client’s methods of counting inventory and the reliance they can place on the client’s

representations about the quantities and physical condition of the inventories. To meet

this requirement, auditors must perform four activities. List them below.

State four of the seven specific balance-related audit objectives for property, plant, and

equipment additions and, for each objective, describe one common test of details of

balances.

Don Crosby, a partner in a national CPA firm, has just learned that his self-sufficient

daughter has accepted a position as the CFO of Sunglasses, Inc., a current client within

the office with which he is employed. Explain the independence ramifications on 1/

Don’s independence, 2/ his office, and 3/ the firm’s independence.

Who developed the WebTrust service? Briefly explain this service.

What are the two software testing strategies that companies typically use? Which

strategy is more expensive?

The starting point for the audit of notes payable is a schedule of notes payable and

accrued interest. Discuss the information typically included in the schedule.

What is one audit procedure that may be used to test for proper handling of terminated

employees?

You are an audit manager for Rodgers & Co. and have recently taken on a new client,

Manufacturing Company. You are in the initial stages of planning the audit and have

decided to start gathering information about the sales/collection cycle of the business.

List below the classes of transactions that you need to gather audit evidence for in

designing your audit procedures.

What are the two most important balance-related audit objectives in notes payable?

What types of inquiry techniques might an auditor use when making inquiries of client

personnel? What are the uses of each technique?

The most important difference among tests of controls, substantive tests of transactions,

and tests of details of balances lies in what the auditor wants to measure. Explain what

each type of test attempts to measure.

List the four characteristics of the capital acquisition and repayment cycle that make it

unique from other cycles.

A financial statement review conducted in compliance with Statements on Standards for

Accounting and Review Services (SSARS) requires the accountant to obtain evidence

to express negative assurance. One of these procedures is to “perform analytical

procedures.” List three other procedures the accountant must perform.

Explain the effect on sample size of increasing each of the following: (1) tolerable

exception rate, (2) estimated population exception rate, (3) acceptable risk of

overreliance, and (4) population size.

Describe the methodology for designing tests of details of balances for accounts

payable.

List the four phases of a financial statement audit.

When determining sufficient and appropriate audit evidence in order to form an opinion

on the client’s financial statements the auditor compiles audit documentation to support

the opinion. The largest portion of audit documentation will include detailed supporting

schedules prepared by the client or the auditor in support of specific accounts on the

financial statements. Two types of supporting schedules are analysis and reconciliation

of amounts. Discuss those two schedules and give an example for each schedule.

Describe the audit risk model and each of its components.

You are employing tests of details of balances for notes payable and interest expense.

Describe below specific audit procedures you would perform for the balance-related

audit objectives of detail tie-in and existence. List at least two for each objective.