After the accrual and property tax expense for each piece of property has been

recalculated, the totals are added and compared with the general ledger.

Deviation refers to a departure from prescribed controls or amounts that are not

monetarily correct.

The standard of due care to which the auditor is expected to be held is referred to as the

prudent person concept.

Control risk is generally set at minimum for most private companies.

A sample of all items in a population will have a zero sampling risk.

In the fraud triangle, fraudulent financial reporting and misappropriation of assets share

the same conditions and risk factors.

Under the Dodd-Frank federal financial reform legislation, all public companies are

required to obtain an audit report on internal control over financial reporting.

When issuing a debt compliance letter, the auditor’s opinion should be in the form of a

negative assurance.

Estimated misstatement in the population and sample size are inversely related; that is,

as estimated misstatement increases, sample size decreases.

PCAOB standards use the term “unqualified opinion” to refer to the standard

unmodified opinion audit report.

Once set during the planning phase, the audit program cannot be revised.

Auditors strive to maintain a high level of independence to keep the confidence of users

relying on their reports.

The use of haphazard sample selection is encouraged under professional auditing

standards.

When a company designs and implements internal controls, cost of the controls is not a

valid consideration.

The audit procedure “Foot the notes payable list and trace the totals to the general

ledger” is performed when verifying the accuracy objective for notes payable.

One of the main reasons people act unethically is that they choose to act selfishly.

When auditors evaluate sales returns and allowances, a primary emphasis is on the

objective of occurrence.

When the sample exception rate is greater than the tolerable exception rate in attributes

sampling, one possible appropriate course of action is to increase sample size.

For most companies, the only transactions involving retained earnings are net earnings

for the year and dividends declared.

Efficiency refers to the degree to which costs are reduced without changing

effectiveness.

Auditors base their statistical inferences on sampling distributions.

An auditor using nonstatistical sampling cannot formally measure sampling error.

Most frauds are discovered by accident.

If an auditor discovers that previously issued financial statements are misleading, the

most desirable approach to follow is to request that the client issue an immediate

revision of the financial statements containing an explanation of the reasons for the

revision.

Auditing can have a significant effect on both information risk and business risk.

After performing all audit procedures in each area, the auditor must integrate the results

into an overall conclusion about the financial statements.

An imprest payroll account limits the client’s exposure to payroll fraud.

Tests of detail tie-in are normally conducted last in the audit of the sales and collections

cycle.

Examination attestation engagements result in a conclusion that is in a positive form,

whereas review attestation engagements result in a conclusion in the form of a negative

assurance.

The auditor needs to have an understanding of the client’s internal controls over

determining fair value estimates.

Current professional auditing standards make it clear that management, not the auditor,

is responsible for identifying and deciding the appropriate accounting treatment for

contingent liabilities.

Tests related to realizable value will vary according to the type of security and the

associated accounting standard.

When other auditors are involved in the audit and they qualify their portion of the audit,

the principal auditor must decide if the amount in question is material to the financial

statements as a whole.

The relevance of audit evidence depends on the audit objective being tested.

When auditing interest-bearing debt, the auditor should ________ verify the related

interest expense and interest payable.

A) not

B) attempt to

C) simultaneously

D) never

When analyzing misstatements, the auditor will determine

A) the implications of the misstatements on other audit areas.

B) the potential impact on the financial statements.

C) the effect on company operations.

D) all of the above.

An auditor’s decision concerning whether or not to “dual date” the audit report is based

upon the auditor’s willingness to

A) extend auditing procedures and assume responsibility for a greater period of time.

B) accept responsibility for subsequent events.

C) permit inclusion of a footnote captioned: event (unaudited) subsequent to the date of

the auditor’s report.

D) assume responsibility for events subsequent to the issuance of the auditor’s report.

If management insists on financial statement disclosures that the auditor finds

unacceptable, the auditor can withdraw from the engagement or

A)

B)

C)

D)

Which of the following would most likely be deemed a direct effect illegal act?

A) violation of federal employment laws

B) violation of federal environmental regulations

C) violation of federal income tax laws

D) violation of civil rights laws

The provisions of the Sarbanes-Oxley Act are most likely to allow which of the

following non-audit services for audit clients?

A) appraisal or valuation services (e.g., pension, post-employment benefit liabilities)

B) financial information systems design and implementation

C) internal audit outsourcing

D) tax consulting

Under the Securities Act of 1933, the auditor’s responsibility for making sure the

financial statements were fairly stated extends to

A) the date of the financial statements.

B) the date the registration statement becomes effective.

C) the date of the audit report.

D) one year beyond the date of the financial statements.

When assessing whether the financial statements are auditable, the auditor must

consider

A) that the integrity of management and the adequacy of accounting records are the two

primary factors determining auditability.

B) that the integrity of management and the adequacy of risk management are the two

primary factors determining auditability.

C) that if all of the transaction information is available only in electronic form without a

visible audit trail, the company cannot be audited.

D) the control risk before determining if the entity is auditable.

The main focus taken by the auditor in verifying liability balances is on the discovery of

I. understated liabilities.

II. omitted liabilities.

A) I only

B) II only

C) both I and II

D) neither I nor II

The term audit objective refers to all of the following except for

A) transaction-related audit objectives.

B) presentation and disclosure-related audit objectives.

C) balance-related audit objectives.

D) cycle-related audit objectives.

One of the causes of nonsampling risk is

A) choosing the wrong sample size.

B) ineffective audit procedures.

C) inadequate sample size.

D) exceptions being found in the sample.

When dealing with laws and regulations that do not have a direct effect on the financial

statements, the auditor

A) should inquire of management about whether the entity is in compliance with such

laws and regulations.

B) has no responsibility to determine if any violations of these laws has occurred.

C) must report all violations, including inconsequential violations, to the audit

committee.

D) should perform the same procedures as for violations having a direct effect on the

financial statements.

Inherent risk is ________ related to planned detection risk and ________ related to the

amount of audit evidence.

A) directly; inversely

B) directly; directly

C) inversely; inversely

D) inversely; directly

Which of the following is most correct for audits of non-public companies?

A) An audit of internal control is required.

B) An audit of internal control is not required.

C) An audit of the design of internal controls is required.

D) An audit of the operational effectiveness of internal controls is required.

When defining the population and the sampling unit for tests of details of balances,

A) the population is defined as all of the transactions in the journal for the period.

B) the sampling unit must be the same for all balance sheet accounts.

C) if sampling for completeness, the sampling unit will be customers with zero

balances.

D) if sampling for completeness, the sampling unit will be the items making up the

recorded population.

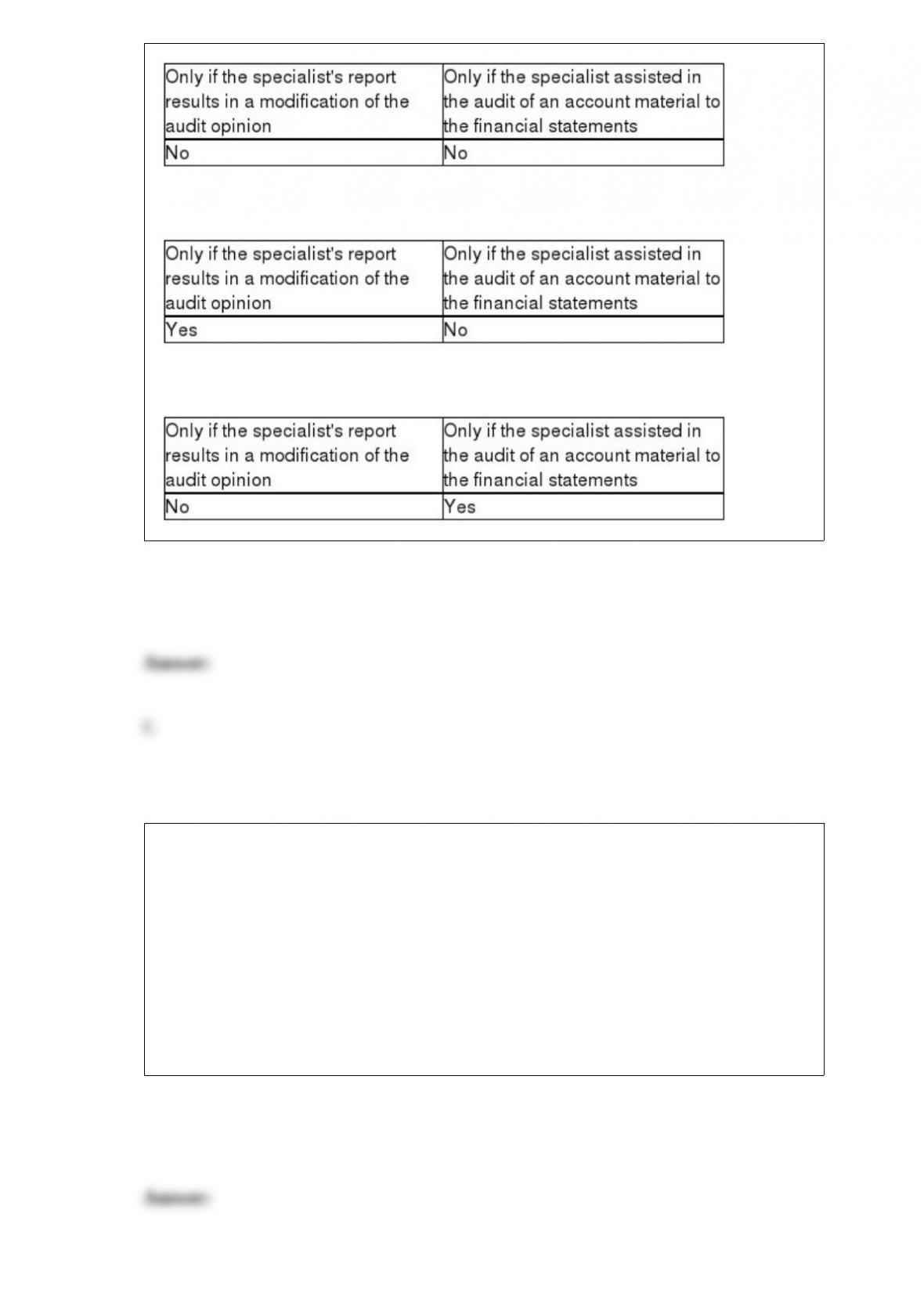

When may the auditor refer to a specialist in the audit report?

A)

B)

C)

D)

If an auditor establishes a relatively high level for materiality, then the auditor will

A) accumulate more evidence than if a lower level had been set.

B) accumulate less evidence than if a lower level had been set.

C) accumulate approximately the same evidence as would be the case were materiality

lower.

D) accumulate an undetermined amount of evidence.

The payroll and personnel cycle ends with which of the following events?

A) interviewing job candidates

B) hiring a new employee

C) existing employees submitting requests for payment for work performed

D) issuance of paychecks

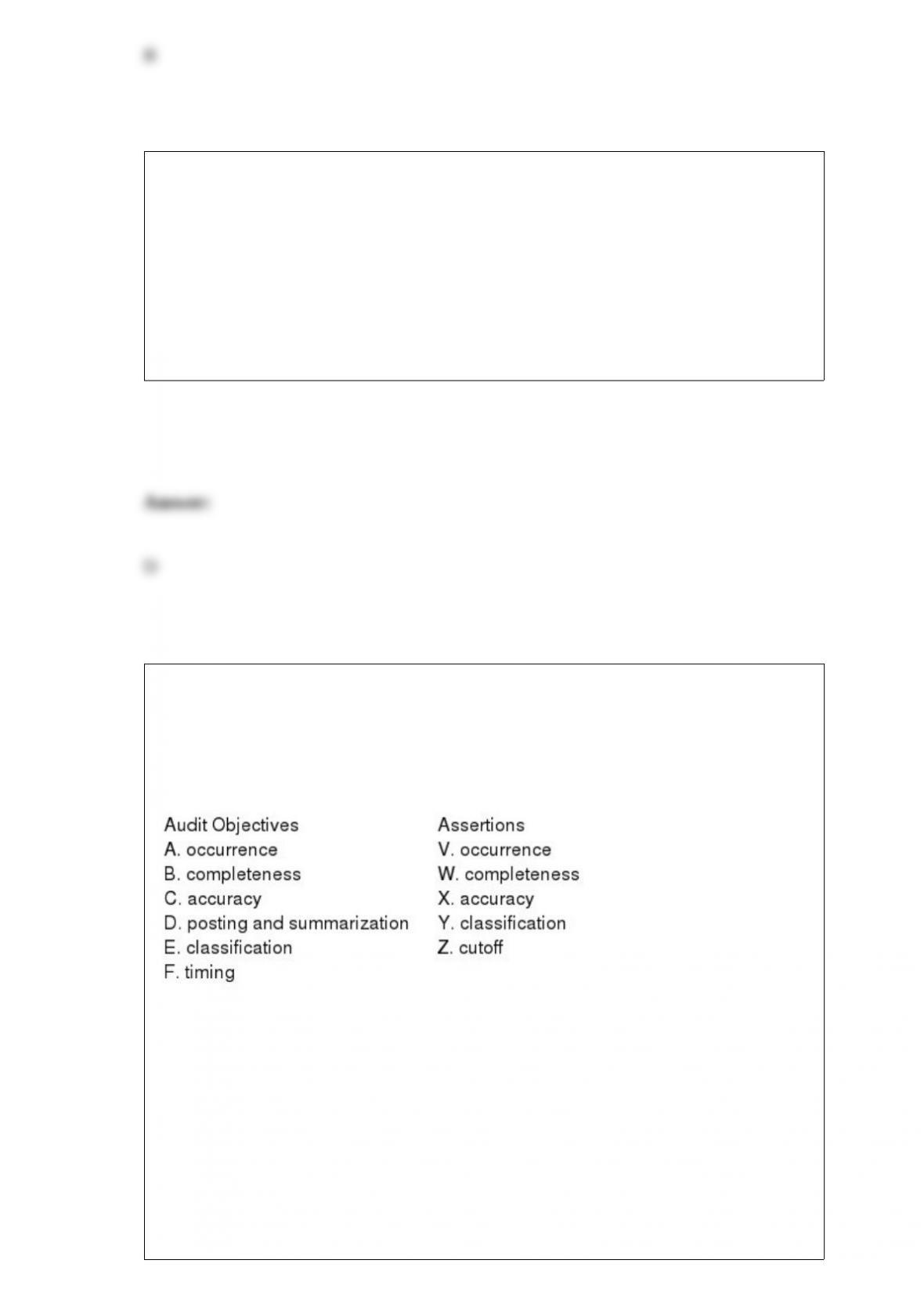

Below are five audit procedures, all of which are tests of transactions associated with

the audit of the acquisition and payment cycle. Also below are the six general

transaction-related audit objectives and the five management assertions. For each audit

procedure, indicate (1) its audit objective, and (2) the management assertion being

tested.

1. Foot the purchases journal and trace the totals to the related general ledger accounts.

(1) ________

(2) ________

2. Recompute the cash discounts taken by the client.

(1) ________

(2) ________

3. Compare dates on cancelled checks with the bank cancellation date.

(1) ________

(2) ________

4. Trace from a sample of cancelled checks to the cash disbursements journal.

(1) ________

(2) ________

5. Examine supporting documentation for a sample of transactions for authorized payee

and amount and to determine services or goods were received.

(1) ________

(2) ________

Which of the following is not an essential component of quality control?

A) policies and procedures to ensure that firm personnel are actively engaged in

marketing strategies

B) policies and procedures to ensure that the work performed by firm personnel meet

applicable professional standards

C) policies to ensure that personnel maintain their independence in fact and in

appearance

D) policies that ensure that monitoring activities are effectively applied

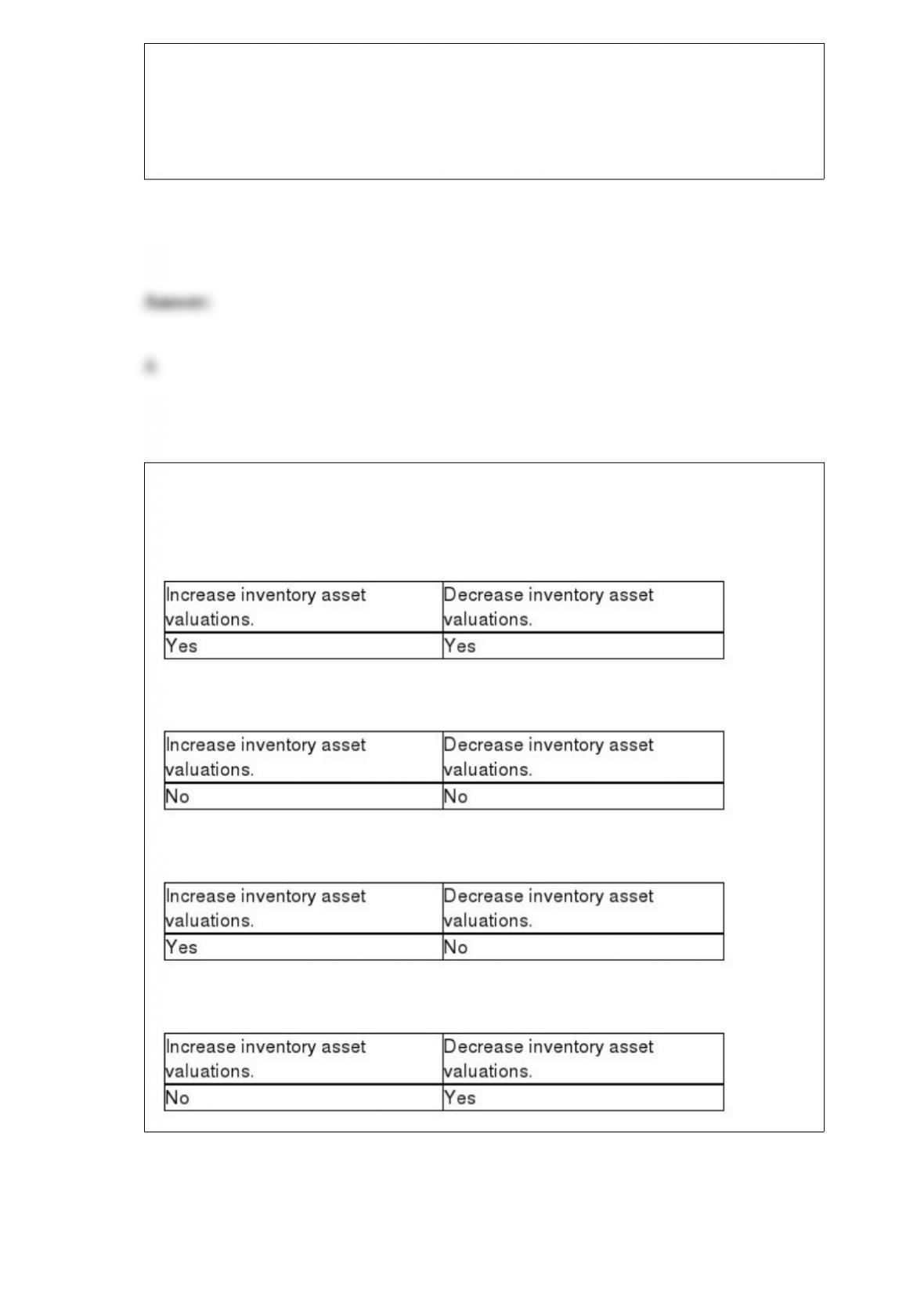

In audits of companies in which payroll is a significant portion of inventory, the

improper account classification of payroll can

A)

B)

C)

D)

The members of a client’s “audit committee” should be

A) members of management.

B) directors who are not a part of company management.

C) non-directors and non-managers.

D) directors and managers.

One of the characteristics of professional skepticism is_______, which is a desire to

investigate beyond the obvious.

A) self-esteem

B) an interpersonal understanding

C) a search for knowledge

D) a questioning mindset

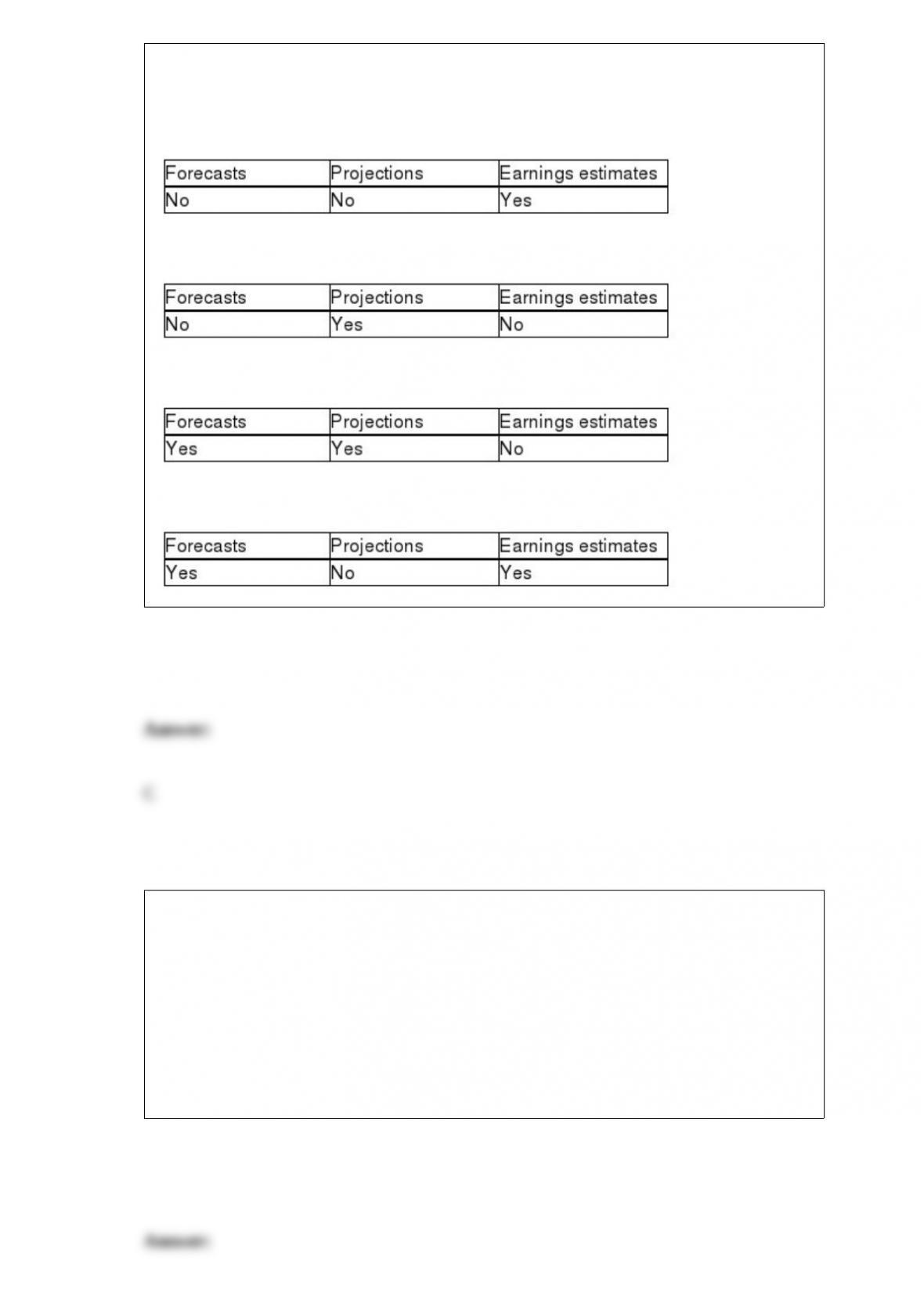

Which of the following is a type of prospective financial statement as defined by the

AICPA attestation standards?

A)

B)

C)

D)

Which of the following audits can be regarded as generally being a compliance audit?

A) IRS agents’ examinations of taxpayer returns

B) GAO auditor’s evaluation of the computer operations of governmental units

C) an internal auditor’s review of a company’s payroll authorization procedures

D) a CPA firm’s audit of a public company

Management furnishes the independent auditor with information concerning litigation,

claims, and assessments. Which of the following is the auditor’s primary means of

initiating action to corroborate such information?

A) Request that client lawyers undertake a reconsideration of matters of litigation,

claims, and assessments with which they were consulted during the period under

examination.

B) Request that client management send a standard inquiry to the client’s attorney letter

to those lawyers with whom management consulted concerning litigation, claims, and

assessments.

C) Request that client lawyers provide a legal opinion concerning the policies and

procedures adopted by management to identify, evaluate, and account for litigation,

claims, and assessments.

D) Request that client management engage outside attorneys to suggest wording for the

text of a footnote explaining the nature and probable outcome of existing litigation,

claims, and assessments.

In monetary unit sampling, a sampling interval of 900 means that

A) every 900th item will be selected.

B) every 900th dollar in the account will be sampled.

C) expected misstatement is 900.

D) tolerable misstatement is 900.

In the auditing process

A) the types and amounts of evidence remain constant from audit to audit.

B) the criteria for evaluating information will not vary depending on the information

being audited.

C) the audit report communicates the auditor’s findings to users.

D) records are gathered by the auditor to determine whether the audited information is

stated in accordance with SEC standards.

A commitment is best described as

A) an agreement to commit the firm to a set of fixed conditions in the future.

B) an agreement to commit the firm to a set of fixed conditions in the future that

depends on company profitability.

C) an agreement to commit the firm to a set of fixed conditions in the future that

depends on current market conditions.

D) a potential future obligation to an outside party for an as yet to be determined

amount.

The preliminary audit strategy

A) is set before the auditor understands the client’s reasons for the audit.

B) guides the development of the audit plan.

C) is determined after the engagement staffing is set.

D) is the detailed steps to be followed for the substantive audit tests.

Which of the following statements is false?

A) The payroll cycle consists of one class of transactions.

B) Balance sheet accounts related to payroll are generally more significant than related

transactions.

C) Internal controls over payroll are effective for most companies.

D) Small companies usually have effective controls over payroll.