The auditor’s tests for proper cutoff of current year acquisitions of property, plant, and

equipment are usually done as part of accounts payable cutoff tests.

Auditors are allowed to have an indirect financial interest in an audit client, such as

ownership of stock in a client’s company by the auditor’s brother, as long as the amount

of the financial interest is immaterial to the brother.

The balance-related audit objective realizable value is not applicable when auditing

notes payable.

Typically, analytical procedures are the primary means of verifying income statement

accounts resulting from allocations.

For a preparation service, each page of the financial statements, should indicate, at a

minimum, that “no assurance is provided” on the financial statements.

Acceptable audit risk and acceptable risk of incorrect acceptance are inversely related;

that is, as AAR increases, ARIA decreases.

Most practitioners allocate the preliminary judgment about materiality to both the

balance sheet and income statement accounts.

A common incentive for companies to manipulate financial statements is a decline in

the company’s financial prospects.

Results from the final analytical procedures may indicate that additional audit evidence

is necessary.

Branch bank accounts are useful for building banking relations in local communities.

It is usually very easy for an auditor to determine if an employee has overstated their

hours worked.

The audit objective of posting and summarization is associated with the management

assertion of accuracy.

In some cases, management can correct deficiencies and material weaknesses before the

auditor does significant testing, which may permit a reduction in control risk.

Tolerable misstatement is inversely related to sample size.

One substantive analytical procedure involves the auditor calculating an expected

balance for an account and then comparing it to the actual account balance.

Adequate documents and records is a subcomponent of the control environment.

Material transactions between the client and the client’s related parties must be

disclosed in the auditor’s report.

Auditors use evidence to help them draw conclusions.

Limited liability companies are structured and taxed like a general partnership, but their

owners have limited personal liability similar to that of a general corporation.

To test the client’s list of outstanding checks on the bank reconciliation for

completeness, the auditor should trace from the list to the checks included with the

cutoff bank statement.

Public companies whose stock is listed on a stock exchange must employ an

independent registrar.

The preparation of a sales invoice is the final step in the sales and collection cycle.

The controls over acquisitions included in the perpetual inventory records are normally

tested as a part of the test of controls and substantive tests of transactions for the sales

and collection cycle.

If the auditor approaches the audit of the accounts in s sequential manner, the findings

of the audit of accounts audited earlier can be used to revise the performance

materiality established for accounts audited later.

The procedures used to gain an understanding of internal control do not vary from

client to client.

A comparison of the current year’s inventory turnover ratio with previous years’ may

indicate the presence of obsolete inventory.

When subsequent events are used to evaluate the amounts included in the year-end

financial statements, auditors must distinguish between conditions that existed at the

balance sheet date and those that came into being after the balance sheet date.

The two main categories of fraud are fraudulent financial reporting and

misappropriation of assets.

The auditors should pay careful attention to accounting principles that involve

subjective measurements or complex transactions.

Separate perpetual records are likely to be kept only for raw materials inventory.

An audit designed to provide reasonable assurance of detecting material misstatements

resulting from noncompliance with provisions of contracts or grant agreements that

have a material and direct effect on the financial statements would be called a(n)

A) performance audit.

B) management audit.

C) operational audit.

D) compliance audit.

Assume you are the partner in charge of the 2016 audit of Becker Corporation, a private

company. The audit report has not yet been prepared. In each independent situation

following (1-8), indicate the appropriate action (a-g) to be taken. The possible actions

are as follows:

a. Issue an unmodified opinion audit report.

b. Qualify both the scope and opinion paragraphs.

c. Qualify the opinion paragraph.

d. Issue an unmodified opinion with an explanatory paragraph.

e. Issue an unmodified opinion with revised wording (no explanatory paragraph).

f. Issue an adverse opinion.

g. Disclaim an opinion.

The situations are as follows:

________ 1. Becker Corporation carries its property, plant, and equipment accounts at

current market values. Current market values exceed historical cost by a highly material

amount, and the effects are pervasive throughout the financial statements.

________ 2. Management of Becker Corporation refuses to allow you to observe, or

make, any counts of inventory. The recorded book value of inventory is highly material.

________ 3. You were unable to confirm accounts receivable with Becker’s customers.

However, because of detailed sales and cash receipts records, you were able to perform

reliable alternative audit procedures.

________ 4. One week before the end of fieldwork, you discover that the audit manager

on the Becker engagement owns a material amount of Becker’s common stock.

________ 5. You relied upon another CPA firm to perform part of the audit. Although

you were the principal auditor, the other firm audited a material portion of the financial

statements. You wish to refer to (but not name) the other firm in your report.

________ 6. You have substantial doubt about Becker’s ability to continue as a going

concern.

________ 7. Becker Corporation changed its method of computing depreciation in

2016. You concur with the change and the change is properly disclosed in the financial

statement footnotes.

________ 8. Ten days after the balance sheet date, one of Becker’s buildings was

destroyed by a fire. Becker refuses to disclose this information in a footnote to the

financial statements, but you believe disclosure is required to conform with GAAP. The

amount of the uninsured loss was material, but not highly material.

Auditors frequently refer to the terms audit assurance, overall assurance, and level of

assurance instead of

A) detection risk.

B) audit report risk.

C) acceptable audit risk.

D) inherent risk.

Auditors accumulate evidence to

A) defend themselves in the event of a lawsuit.

B) determine if the financial statements are correct.

C) satisfy the requirements of the Securities Acts of 1933 and 1934.

D) reach a conclusion about the fairness of the financial statements.

Which of the following would be a subsequent discovery of facts which would not

require a response by the auditor?

A) discovery of the inclusion of material nonexistent sales

B) discovery of the failure to write off material obsolete inventory

C) discovery of the omission of a material footnote

D) discovery of management’s intent to increase selling prices in the future

The auditor’s objective in determining whether the client’s computer program correctly

processes valid and invalid transactions is accomplished through the

A) test data approach.

B) generalized audit software approach.

C) microcomputer-aided auditing approach.

D) generally accepted auditing standards.

A(n) ________ total represents the summary total of codes from all records in a batch

that do not represent a meaningful total.

A) record

B) hash

C) output

D) financial

A listing of the balances in the accounts receivable master file at the balance sheet date,

including individual customer balances outstanding and a breakdown of each balance

by the time passed between the date of the sale and the balance sheet date, is the

A) customer list.

B) aged trial balance.

C) accounts receivable ledger.

D) schedule of accounts receivable.

To emphasize the fact that the auditor is independent, a typical addressee of the audit

report could be

A)

B)

C)

D)

Which is not a method used by auditors to generate random numbers?

A) electronic spreadsheets

B) systematic sample generators

C) random number generators

D) generalized audit software

Under the rules and interpretations of the AICPA Code,

A) a CPA can be a client advocate during an audit, but not while performing tax or

management services.

B) staff auditors should always defer to the judgment of their immediate supervisor.

C) a conflict of interest is a relationship that might interfere with objectivity or integrity.

D) even if a conflict of interest is disclosed to the member’s client or employer, it is still

considered a violation of the rules of conduct.

Related party

A) transactions must be disclosed in the footnotes even if the amounts are immaterial.

B) disclosures include the nature of the related party relationship and a description of

the transaction.

C) transactions are considered arm’s-length transactions.

D) disclosures are required only for public companies.

In a financial statement audit, inherent risk is evaluated to help an auditor asses which

of the following?

A) the internal audit department’s objectivity in reporting a material misstatement of a

financial statement assertion it detects to the audit committee

B) the risk the internal control system will not detect a material misstatement of a

financial statement assertion

C) the risk that the audit procedures implemented will not detect a material

misstatement of a financial statement assertion

D) the susceptibility of a financial statement assertion to a material misstatement

assuming there are no related controls

To promote operational efficiency, the internal audit department would ideally report to

A) line management.

B) the PCAOB.

C) the Chief Accounting Officer.

D) the audit committee.

A CPA may wish to emphasize specific matters regarding the financial statements even

though an unqualified opinion will be issued. Normally, such explanatory information is

A) included in the scope paragraph.

B) included in the opinion paragraph.

C) included in a separate paragraph in the report.

D) included in the introductory paragraph.

Match six of the terms (a-i) used in the capital acquisitions and repayment cycle with

the descriptions provided below (1-6):

a. capital acquisition and repayment cycle

b. capital stock certificate book

c. closely held corporation

d. independent registrar

e. note payable

f. publicly held corporation

g. stock transfer agent

h. schedule of notes payable and accrued interest

i. stock maintenance agent

________ 1. an outside person engaged by a corporation to make sure that its stock is

issued in accordance with capital stock provisions in the corporate charter and

authorizations by the board of directors

________ 2. the normal starting point for the audit of notes payable; includes detailed

information of all transactions related to notes payable that took place during the year

________ 3. a record of the issuance and repurchase of capital stock for the life of the

corporation

________ 4. an outside person engaged by a corporation to maintain the stockholder

records, and often to disburse cash dividends

________ 5. an entity that is required to engage an independent registrar

________ 6. the cycle that concerns the acquisition of capital resources through

interest-bearing debt and owners’ equity and repayment of the capital

When using statistical sampling, the auditor would most likely require a smaller sample

if the

A) population increases.

B) desired reliability decreases.

C) desired precision interval narrows.

D) expected exception rate increases.

When dealing with variables sampling and sampling risk, it is important to understand

that

A) for variables sampling, auditors uses ARIA but not ARIR.

B) ARIR is of serious concern to the auditor because of potential legal implications.

C) ARIA is a one-tailed statistical test.

D) the confidence coefficients for ARIA are the same as the confidence level.

In most audits, the auditor issues a(n)

A) modified opinion audit report.

B) standard unmodified opinion audit report.

C) scope limited audit report.

D) adverse audit report.

Many audits have a ________ risk of misstatement for the payroll cycle.

A) high

B) low

C) moderate

D) zero

Which of the following statements best describes the auditor’s responsibility regarding

the detection of fraud?

A) The auditor is responsible for the failure to detect fraud only when such failure

clearly results from nonperformance of audit procedures specifically described in the

engagement letter.

B) The auditor is required to provide reasonable assurance that the financial statements

are free of both material errors and fraud.

C) The auditor is responsible for detecting material financial statement fraud, but not a

material misappropriation of assets.

D) The auditor is responsible for the failure to detect fraud only when an unqualified

opinion is issued.

At what point in the acquisition and payment cycle do most companies first recognize

the acquisition and related liability on their records?

A) when the purchase requisition is received by the accounting department

B) when the purchase order is prepared

C) when the company receives the invoice from the vendor

D) when the company receives the goods or services from the vendor

Two of the most useful warning signals that can indicate that revenue fraud is occurring

are

A) analytical procedures and documentary discrepancies.

B) analytical procedures and misappropriation of assets.

C) documentary discrepancies and vague responses to inquiries.

D) missing audit evidence and vague responses to inquiries.

Although the financial statements of all companies are potentially subject to

manipulation, the risk is greater for companies that

A) are heavily regulated.

B) have low amounts of debt.

C) have to make significant judgments for accounting estimates.

D) operate in stable economic environments.

Auditing standards require that the audit report must be titled and that the title must

A) include the word “independent.”

B) indicate if the auditor is a CPA.

C) indicate if the auditor is a proprietorship, partnership, or corporation.

D) indicate the type of audit opinion issued.

If the auditor believes that there will be more than just a few exceptions discovered, and

desires an accurate estimate of the dollar value of the exceptions, he or she will use

A) attributes sampling.

B) monetary unit sampling.

C) block sampling.

D) variables sampling.

To determine accounts receivable turnover, net sales is divided by

A) beginning net accounts receivable.

B) average gross receivables.

C) cost of goods sold.

D) 365 days.

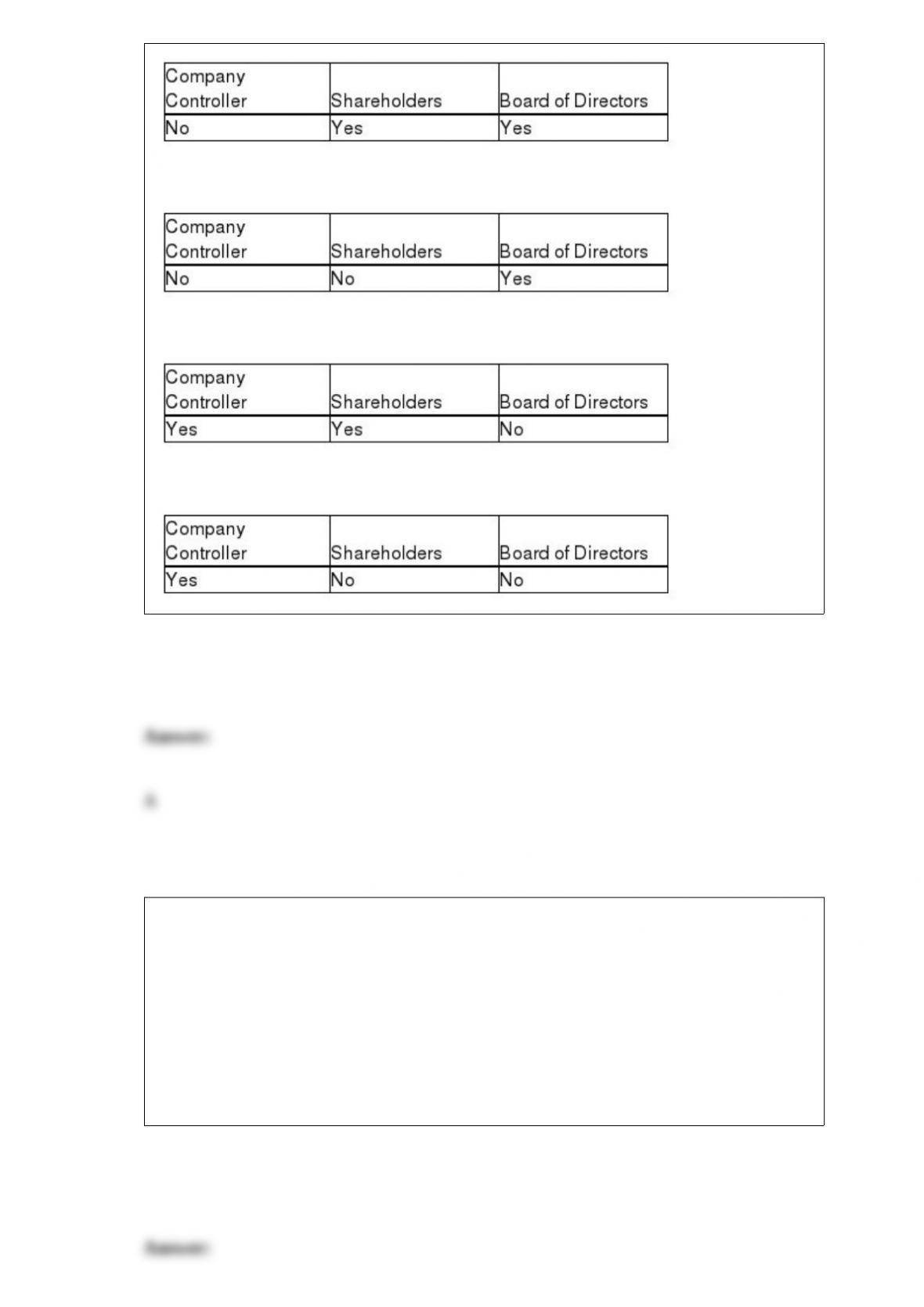

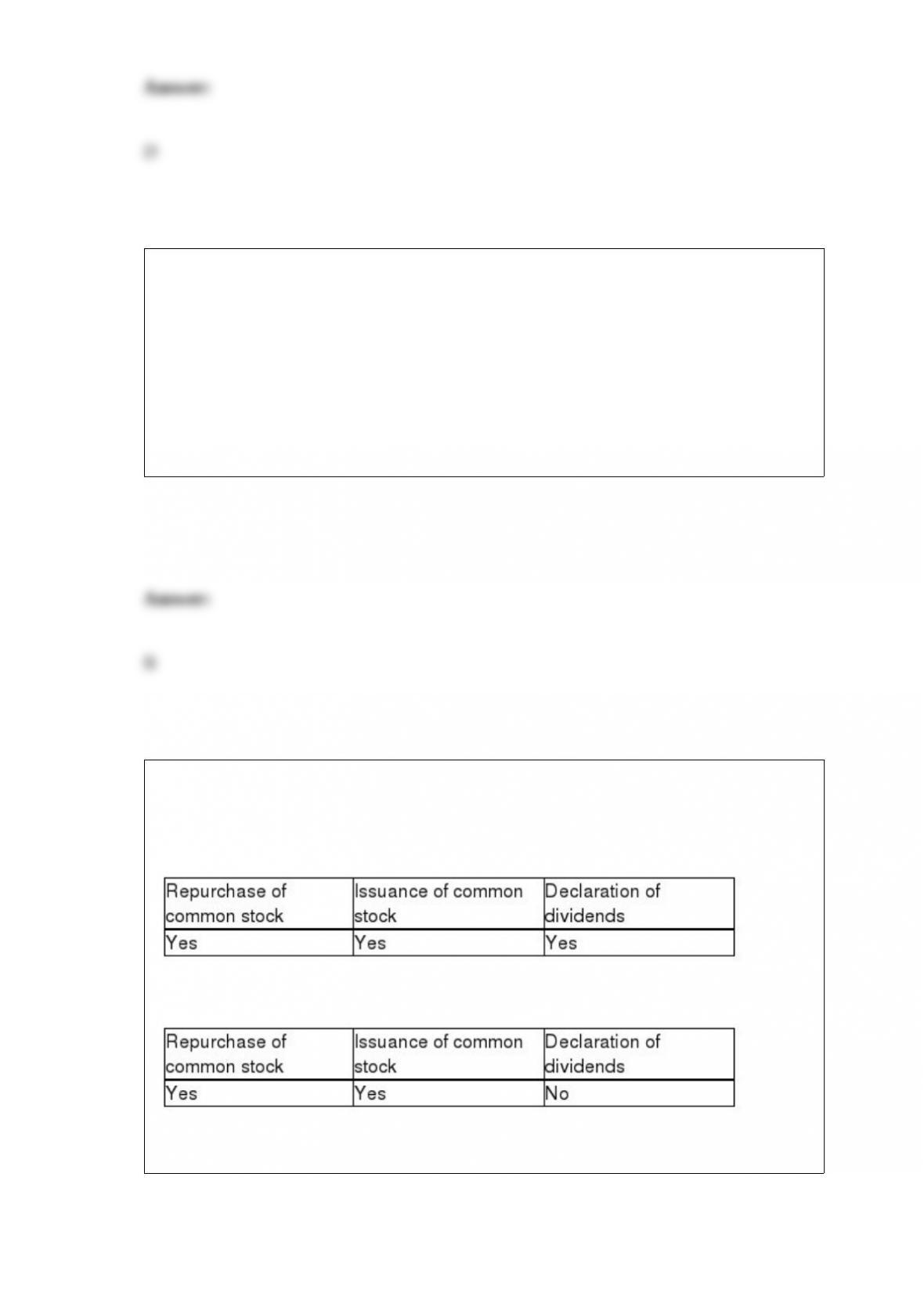

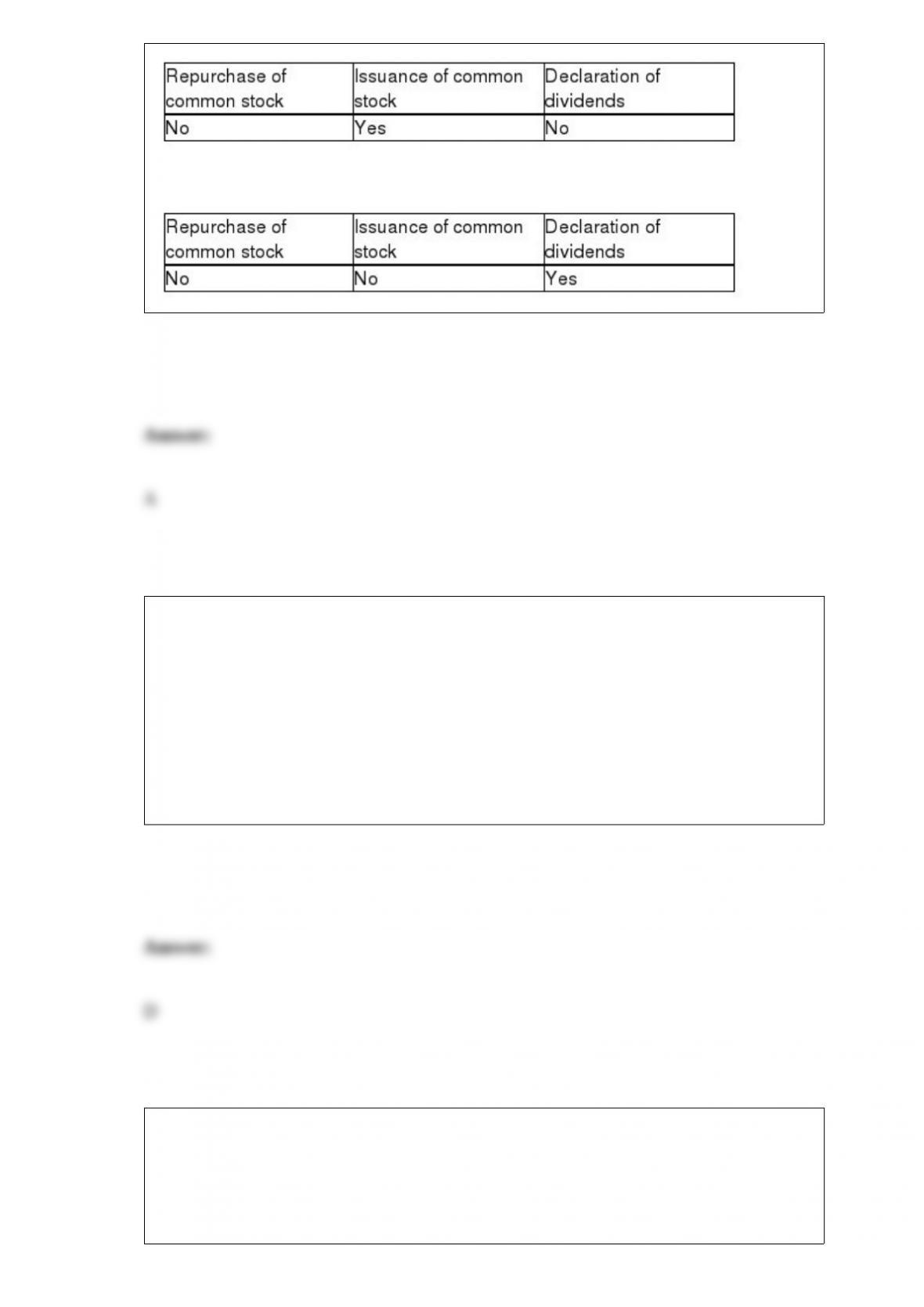

Which of the following owners’ equity transactions usually require specific

authorization from a company’s board of directors?

A)

B)

C)

D)

The ________ is a standard of conduct for all members of the AICPA.

A) IESBA Code of Conduct

B) SEC Code of Conduct

C) PCAOB Code of Professional Conduct

D) AICPA Code of Professional Conduct

The audit of year-end physical inventories should include steps to verify that the client’s

purchases and sales cutoffs were adequate. The audit steps should be designed to detect

whether merchandise included in the physical count at year-end was not recorded as a

A) sale in the current period.

B) sale in the subsequent period.

C) purchase in the current period.

D) purchase return in the subsequent period.

You are determining the significance of the following: you set a 5% risk of assessing

control risk too low and your computation of the upper deviation risk is 7%. What could

you conclude?

A) There is a 95% chance the deviation rate is the population is less than 5%.

B) There is a 5% chance the deviation rate in the population is less than 7%.

C) There is a 95% chance the deviation rate in the population exceeds 95%.

D) There is a 5% chance the deviation rate in the population exceeds 7%.

An act of two or more employees to steal assets and cover their theft by misstating the

accounting records would be referred to as

A) collusion.

B) a material weakness.

C) a control deficiency.

D) a significant deficiency.

Which of the following is an accurate statement regarding inventory and risk?

A) Inventory with a high business risk includes products with potential obsolescence.

B) Auditors often have a greater concern for misstatements when inventory is stored in

one warehouse.

C) Inherent risk is generally set at low for manufacturing companies.

D) Performance materiality for inventory is determined before assessing client business

risk.

Fraud is more prevalent in smaller businesses and not-for-profit organizations because it

is more difficult for them to maintain

A) adequate separation of duties.

B) adequate compensation.

C) adequate financial reporting standards.

D) adequate supervisory boards.

State the three purposes of the management representation letter.

Explain acceptable risk of incorrect acceptance and acceptable risk of incorrect

rejection within the context of variables sampling.

What is the difference between an independent registrar and a stock transfer agent?

What are the four categories of attestation services?

Describe the five types of audit tests. Identify which of the five types are substantive

tests, and which are used to reduce assessed control risk.

A proof of cash includes four reconciliation tasks. List below two of those tasks.

There are three conditions necessitating a departure from an unqualified audit report.

Name, discuss and state the appropriate audit report for each of these three conditions.

State the purpose and the information contained on the W-2 Form and on the payroll tax

returns.

Auditors are required to perform certain procedures in every audit to address the risk of

management override of internal controls. What are these procedures?

Discuss each of the six possible courses of action the auditor can take when he or she

has concluded that the population is misstated by more than a tolerable amount.

The following is the introductory paragraph, and the Basis for Qualified Opinion

paragraph for Fast Times Corporation, a nonpublic company.

Independent Auditor’s Report

To the shareholders of Fast Times Corporation

We have audited the accompanying balance sheet of Fast Times Corporation as of

September 30, 2016, and the related statements of income, retained earnings, and cash

flows for the year then ended, and the related notes to the financial statements.

Basis for Qualified Opinion

We were unable to obtain audited financial statements supporting the company’s

investment in a foreign affiliate stated at $1,040,000, or its equity in earnings of that

affiliate of $501,000, which is included in net income, as described in Note 14 to the

financial statements. Because of the nature of the company’s records, we were unable to

satisfy ourselves as to the carrying value of the investment or the equity in its earnings

by means of other auditing procedures.

Required:

Prepare the opinion paragraph for the above audit report. Do not date or sign the report.

One purpose of performing analytical procedures in the planning phase of an audit is to

assess the client’s financial condition. Explain how the assessment of a client’s financial

condition can affect the auditor’s decisions concerning evidence accumulation in later

phases of the audit.

What are the major functions of the AICPA?

State the six functions that make up the inventory and warehousing cycle and, for each

function, identify the related documents that would be used by a manufacturing

company.

Three approaches to the application of the foreseen users’ concept are (1) the Credit

Alliance approach, (2) the Restatement of Torts approach, and (3) the foreseeable user

approach. Summarize each of these three approaches.

Discuss the advantages and disadvantages of using negative accounts receivable

confirmations rather than positive confirmations.

Discuss the four key controls over notes payable.