16–11

16–17 (continued)

of controls based upon the selection of the significant controls. The auditor

would then perform the tests of the significant controls to determine the

effectiveness ofthe controls and to plan the substantive tests that are necessary

16–18 The determination of test of details procedures is directly affected by

results from tests of controls and substantive test of transactions. When results

Multiple Choice Questions From CPA Examinations

16–19 a. (4) b. (2) c. (4)

Discussion Questions and Problems

Persuasive evidence of an arrangement exists,

Delivery has occurred or services have been rendered,

requests shipment to designated locations.

16–12

16–23 (continued)

c. Normally, such an arrangement does not qualify as a sale because

d. The SEC states that the following are important criteria:

The risks of ownership must have passed to the buyer;

The customer must have made a fixed commitment to

purchase the goods, preferably in written documentation;

bill and hold basis;

There must be a fixed schedule for delivery of the goods.

The date for delivery must be reasonable and must be

consistent with the buyer’s business purpose (e.g., storage

periods are customary in the industry);

other orders; and

The goods must be complete and ready for shipment.

16–24 a. One of the risks of material misstatement related to notes

receivable generally relates to the existence balance–related audit

of material misstatement, particularly related to whether the

receivable is properly classified as a short–term or long–term

receivable.

misstatement related to the existence balance–related audit

objective might also be considered a significant risk.

16–13

16–24 (continued)

d. Assuming the notes receivable balances are material, the auditor

would send notes receivable confirmations in the current year to

obtain evidence related to the existence and accuracy balance–

e. The confirmation of notes receivable will provide little, if any,

evidence related to the realizable value balance–related audit

objective. While the confirmation would confirm the existence of

16–25 a. 1. Completeness

2. a. Detail tie–in

b. Realizable value

3. Detail tie–in

4. a. Existence

b. The auditor would likely perform the steps in the following order: 4,

3, 2, 1, 6, and 5. The auditor would perform analytical procedures

as part of the planning process to identify potential misstatements.

The auditor would next perform the detail tie–in procedure of

footing and cross–footing the listing of aged accounts receivable

16–25 (continued)

completeness. Next, the auditor would select a sample of accounts

to confirm, mail the confirmations, receive confirmations and

16–26

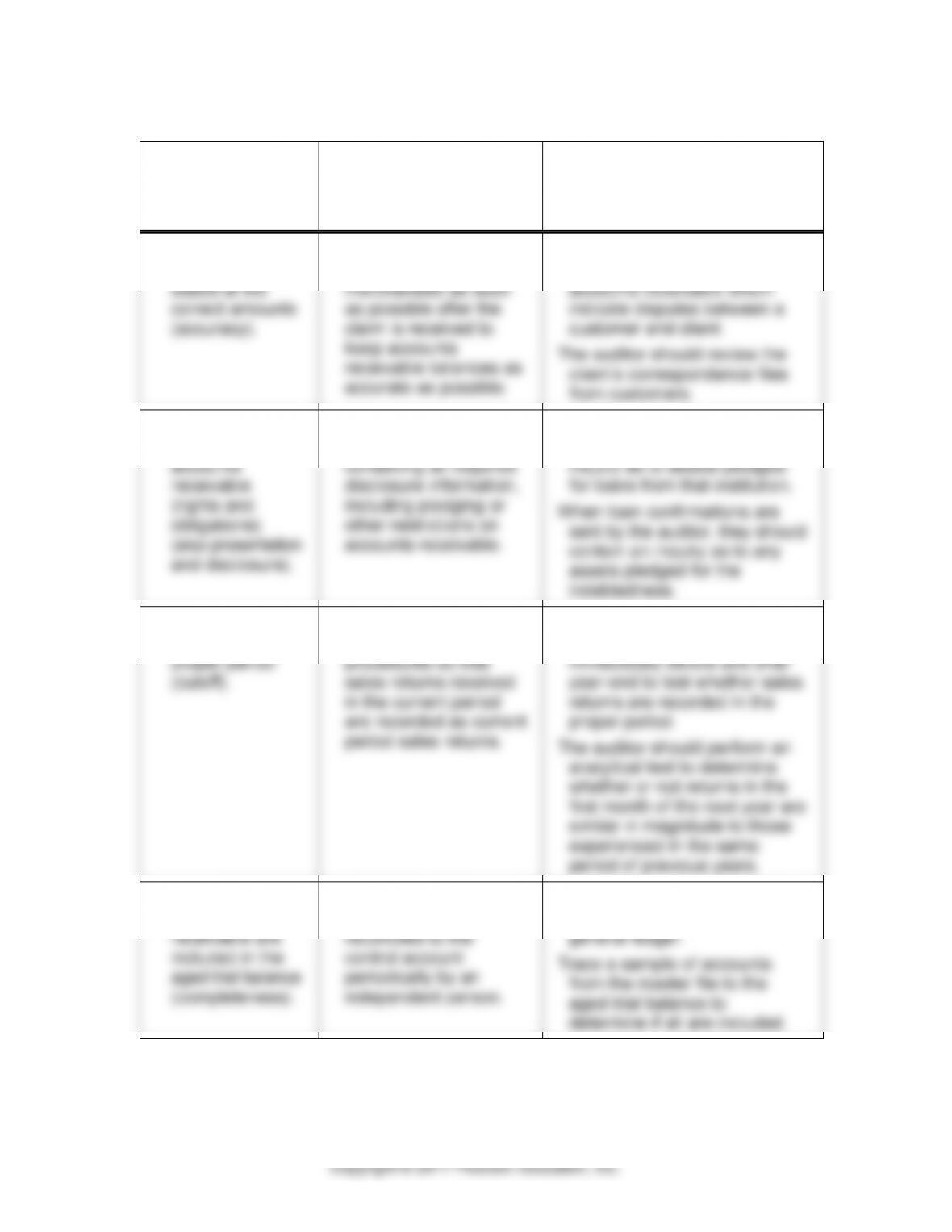

a.

BALANCE–

RELATED AUDIT

OBJECTIVE

b.

PREVENTIVE

INTERNAL CONTROL

c.

TESTS OF DETAILS OF

BALANCES AUDIT

PROCEDURES

1. Customer

balances stated

at the correct

amount

(accuracy).

The client should scan

the remittance advice

returned with the

customer payment

electronically rather

than manually entering

the customer number.

The auditor should note any

replies to the confirmation of

accounts receivable which

indicate disputes between a

customer and client.

2. Transactions are

recorded in the

proper period

(cutoff).

The client should

establish cutoff

procedures so that only

shipments made before

year–end are recorded

as current period sales.

Examine shipping documents

for sales recorded immediately

before and after year–end to

test whether sales are

recorded in the proper period.

3. Accounts

receivable are

stated at

realizable value

(realizable value)

The client should

perform an analysis of

the collectibility of

accounts receivable at

the end of the year and

should communicate

with its customers to

determine the likelihood

of the collectibility of

individual accounts.

The auditor should keep informed

of current economic conditions

and consider their effect on

collectibility of accounts

receivable for the client.

The auditor may compare cash

receipts after year–end to the

cash receipts of the similar

period of the previous year and

consider any changes as to

their effect on the collectibility

of the accounts receivable.

16–26 (continued)

a.

BALANCE–

RELATED AUDIT

OBJECTIVE

b.

PREVENTIVE

INTERNAL CONTROL

c.

TESTS OF DETAILS OF

BALANCES AUDIT

PROCEDURES

4. Accounts

receivable are

stated at the

correct amounts

(accuracy).

The client should record

claims for defective

merchandise as soon

as possible after the

claim is received to

keep accounts

receivable balances as

accurate as possible.

The auditor should note any

replies to the confirmation of

accounts receivable which

indicate disputes between a

customer and client.

The auditor should review the

client’s correspondence files

from customers.

5. The company

has rights to

accounts

receivable

(rights and

obligations)

(also presentation

and disclosure).

The controller should

maintain a schedule

containing all required

disclosure information,

including pledging or

other restrictions on

accounts receivable.

The auditor’s standard bank

confirmation should contain an

inquiry as to assets pledged

for loans from that institution.

When loan confirmations are

sent by the auditor, they should

contain an inquiry as to any

assets pledged for the

indebtedness.

6. Transactions are

recorded in the

proper period

(cutoff).

The client should

establish cutoff

procedures so that

sales returns received

in the current period

are recorded as current

period sales returns.

Examine receiving reports for

sales returns recorded

immediately before and after

year–end to test whether sales

returns are recorded in the

proper period.

The auditor should perform an

analytical test to determine

whether or not returns in the

first month of the next year are

similar in magnitude to those

experienced in the same

period of previous years.

7. Existing

accounts

receivable are

included in the

aged trial balance

(completeness).

The accounts receivable

master file should be

reconciled to the

control account

periodically by an

independent person.

Foot the aged trial balance and

compare the total to the

general ledger.

Trace a sample of accounts

from the master file to the

aged trial balance to

determine if all are included.

16–26 (continued)

a.

BALANCE–

RELATED AUDIT

OBJECTIVE

b.

PREVENTIVE

INTERNAL CONTROL

c.

TESTS OF DETAILS OF

BALANCES AUDIT

PROCEDURES

8. Accounts

receivable exist

(existence).

The accounts receivable

master file should be

reconciled to the

control account

periodically by an

independent person.

Foot the aged trial balance and

compare the total to the

general ledger.

Trace from the aged trial

balance to the master file,

looking for duplicates.

9. Accounts

receivable

are properly

classified

(classification).

The client should maintain

separate accounts for

the recording of

receivables due from

affiliated companies.

The auditor should review the

trial balance of accounts

receivable to determine

whether or not accounts from

affiliated companies are

included in the customer

accounts.

The auditor should be aware of

affiliated companies and the

transactions between them

and the client, and should

inquire and follow up to

determine that accounts

receivable from affiliates are

not included in the accounts

receivable from customers.

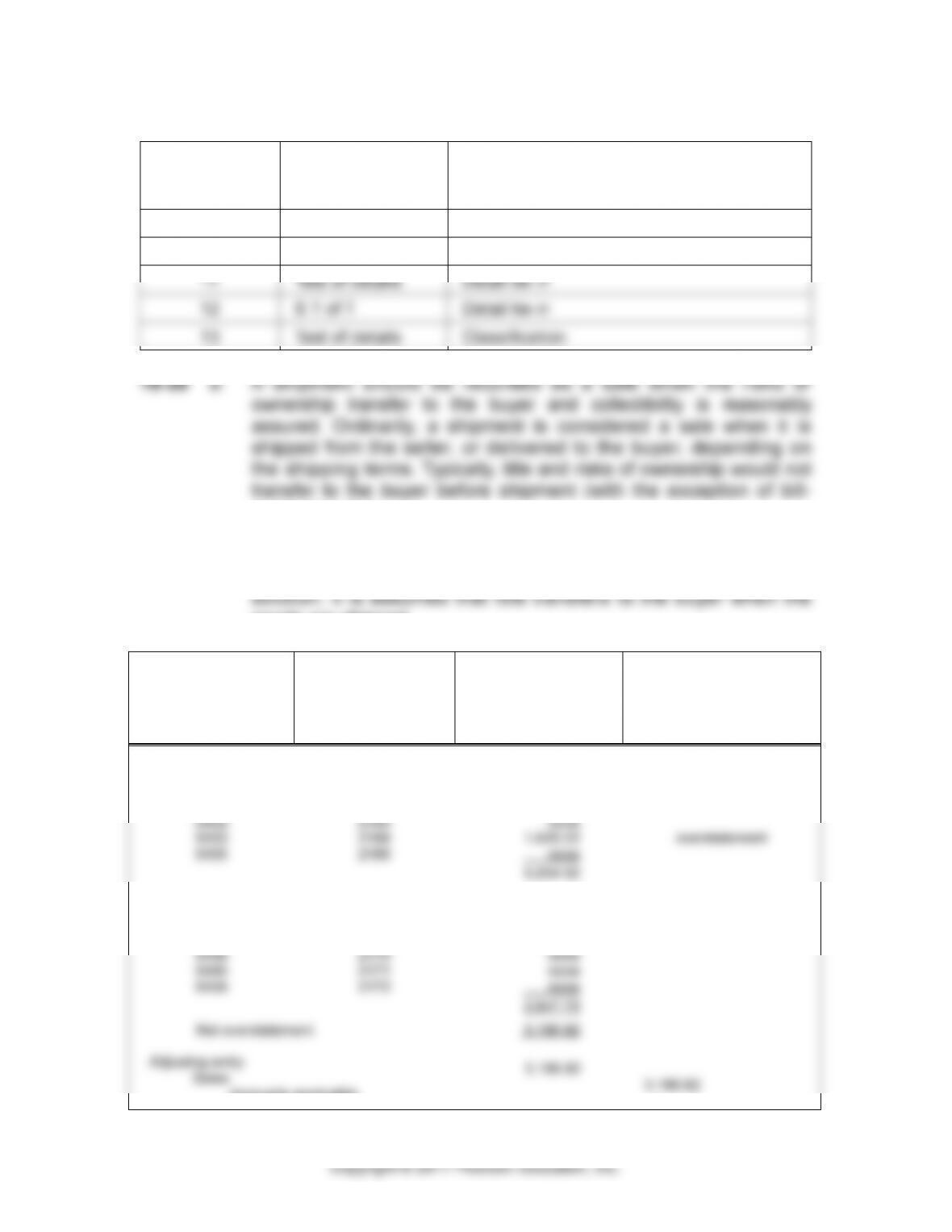

16–27

PROCEDURE

a.

TYPE OF TEST

b.

BALANCE–RELATED AUDIT OBJECTIVE

1

Test of details

Existence and accuracy

2

Test of details

Cutoff

3

S T of T

Cutoff

4

Test of details

5

S T of T

Classification

Accuracy and existence

(may also include realizable value if cash

6

S T of T

Rights

7

Test of details

Completeness

8

ST of T

Existence

16–17

16-27 (continued)

PROCEDURE

a.

TYPE OF TEST

b.

BALANCE–RELATED AUDIT

OBJECTIVE

9

Test of control

Accuracy

10

S T of T

Completeness

11

Test of details

Detail tie–in

12

S T of T

Detail tie–in

13

Test of details

Classification

and–hold sales).

b. See the table below. The sales invoice number can be ignored,

except to determine the shipping document number. In this

goods are shipped.

INVOICE NO.

SHIPPING

DOCUMENT NO.

MISSTATEMENT

IN SALES

CUTOFF

OVERSTATEMENT

OR

UNDERSTATEMENT

OF AUG. 31 SALES

August sales

5431

5434

5432

5433

5435

2164

2169

2165

2168

2166

none

4,214.30

none

1,620.22

none

5,834.52

overstatement

overstatement

September sales

5437

5436

5438

5440

5439

2163

2167

2170

2171

2172

2,541.31

106.39

none

none

none

2,647.70

understatement

understatement

Net overstatement

3,186.82

Adjusting entry

Sales

Accounts receivable

3,186.82

3,186.82

16–18

16–28 (continued)

Amount of sale

2168 1,620.22

2169 4,214.30

sheet date to determine if they were correctly dated.

An alternative, if there are perpetual records, is to follow up

showed a total of 526, and a shipment of 100 units included on the

perpetual August 31. This is a likely indication of a September

shipment that had been dated August 31.

cutoff.

1. Be present during the physical count on the last day of the

accounting period to determine the shipping document

2. During year–end field work, select a sample of shipping

documents preceding and succeeding those selected in

procedure 1. Generally, shipping documents with the same

3. During year–end field work, select a sample of sales from

the sales journal recorded in the last few days of the

16–19

16–28 (continued)

help prevent cutoff misstatements.

CONTROL

TEST OF CONTROL

(1) Policy requiring the use of

prenumbered shipping documents.

Examine several documents for

prenumbering.

(2) Policy requiring the issuance of

shipping documents sequentially.

Observe recording of documents, examine

document numbers and inquiry.

(3) Policy requiring recording sales

invoices in the same sequence as

shipping documents are issued.

Observe recording of documents, examine

document numbers and inquiry.

(4) Policy requiring dating of shipping

documents, immediate recording

of sales, and dating sales on the

same date as the shipment

(depending on shipping terms).

Observe dating of shipping documents

and sales invoices, and timing of

recording.

(5) Use of perpetual inventory

records and reconciliation of

differences between physical and

perpetual records.

Examine worksheets reconciling physical

counts and perpetual records.

16–29

a.

TYPE OF EVIDENCE

b.

TYPE OF TEST

c. and d.

OBJECTIVE(S)

1. Reperformance

(4) Test of details of

balances

Detail tie–in

2. Inspection

(1) Test of control

Completeness

3. Inquiry

(4) Test of details of

balances

Cutoff

4. Observation

(1) Test of control

Posting and

summarization

5. Inspection

(2) Substantive test of

transactions

Timing

6. Inspection

(1) Test of control

Occurrence

7. Inspection

(4) Test of details of

balances

Cutoff

8. Analytical procedure

(3) Substantive analytical

procedure

N/A

16–20

Copyright © 2017 Pearson Education, Inc.

16–30 a. The two types of confirmations used for confirming accounts

receivable are “positive” and “negative” confirmations. A positive

confirmation is a letter, addressed to the debtor, requesting that the

recipient indicate directly on the letter whether the stated account

balance is correct or incorrect and, if incorrect, by what

amount. A negative confirmation requests a response from the

debtor only when the debtor disagrees with the stated amount.

When deciding which type of confirmation to use, the

auditor should consider the assessed control risk in the sales and

collection cycle, the make–up of the population, cost/benefit

expensive than negative confirmations. Positive confirmations

should be used when the population is comprised of a small

number of large accounts, and when there are suspected

conditions of dispute or inaccuracy. When negative confirmations

are used, the auditor has normally assessed control risk below

from the general public.

b. When evaluating the collectibility of accounts receivable, the

auditor may review the aging of accounts receivable, analyze

subsequent cash receipts from customers, discuss the collectibility

economic conditions.

c. When customers fail to respond to positive confirmation requests,

the CPA may not assume with confidence that these customers

checked the request, found no disagreement, and therefore did

post office as undeliverable. Confirmations returned as

undeliverable by the post office will require appropriate action to

obtain better addresses.

Follow–up is necessary when customers do not reply

to mail second requests.