18–24 (continued)

MISSTATEMENT

a.

TRANSACTION–

RELATED

AUDIT OBJECTIVE

NOT MET

b.

PREVENTIVE

CONTROL

c.

SUBSTANTIVE

PROCEDURE

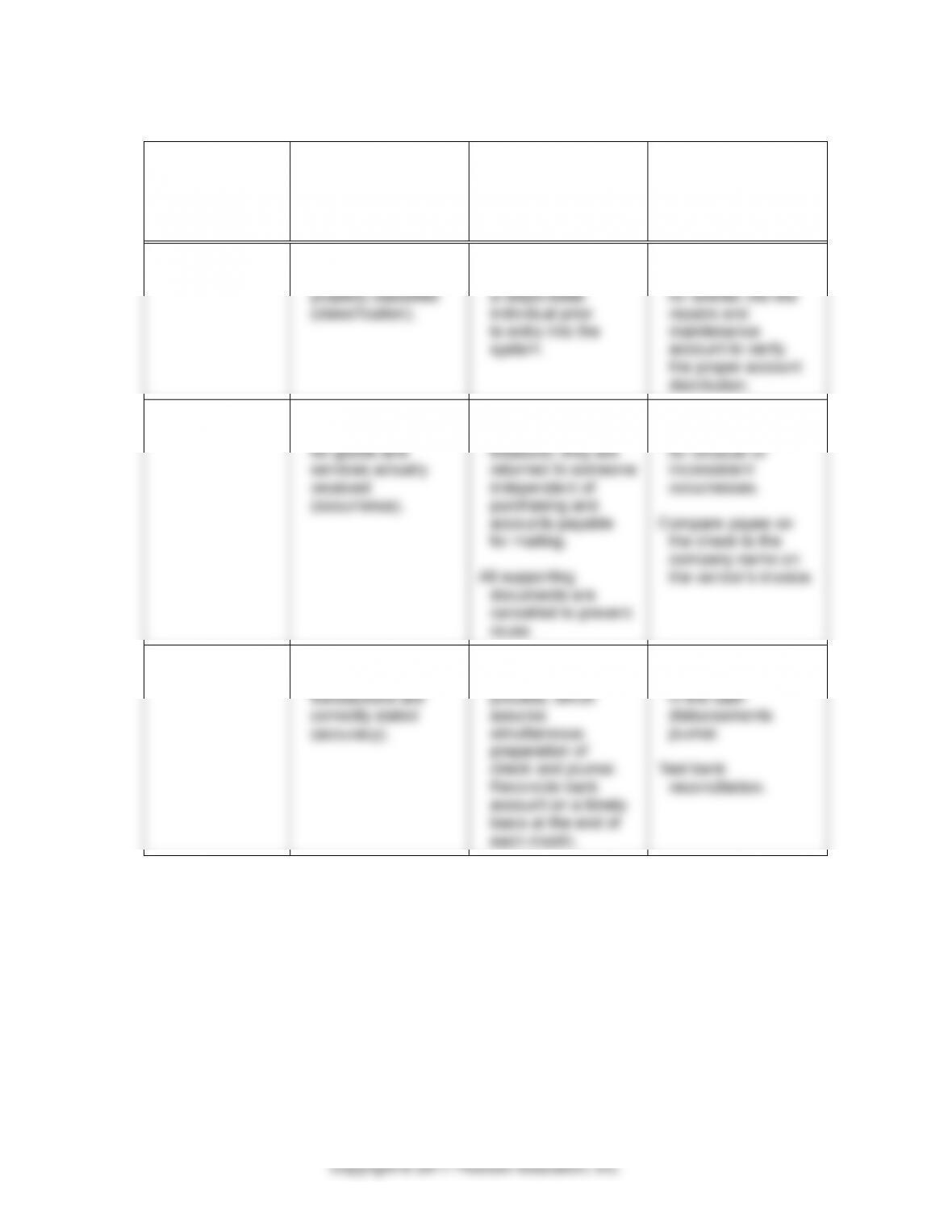

4

Acquisition

transactions are

properly classified

(classification).

Account distributions

are reviewed by

a responsible

individual prior

to entry into the

system.

Examination of

supporting invoices

for entries into the

repairs and

maintenance

account to verify

the proper account

distribution.

5

Recorded cash

disbursements are

for goods and

services actually

received

(occurrence).

Once checks are

signed by the

treasurer, they are

returned to someone

independent of

purchasing and

accounts payable

for mailing.

All supporting

documents are

cancelled to prevent

reuse.

Review physical

inventory shortages

for unusual or

inconsistent

occurrences.

Compare payee on

the check to the

company name on

the vendor’s invoice.

6

Recorded cash

disbursement

transactions are

correctly stated

(accuracy).

Checks are prepared

using a computer

process, which

assures

simultaneous

preparation of

check and journal.

Reconcile bank

account on a timely

basis at the end of

each month.

Compare check

amounts to entries

in the cash

disbursements

journal.

Test bank

reconciliation.

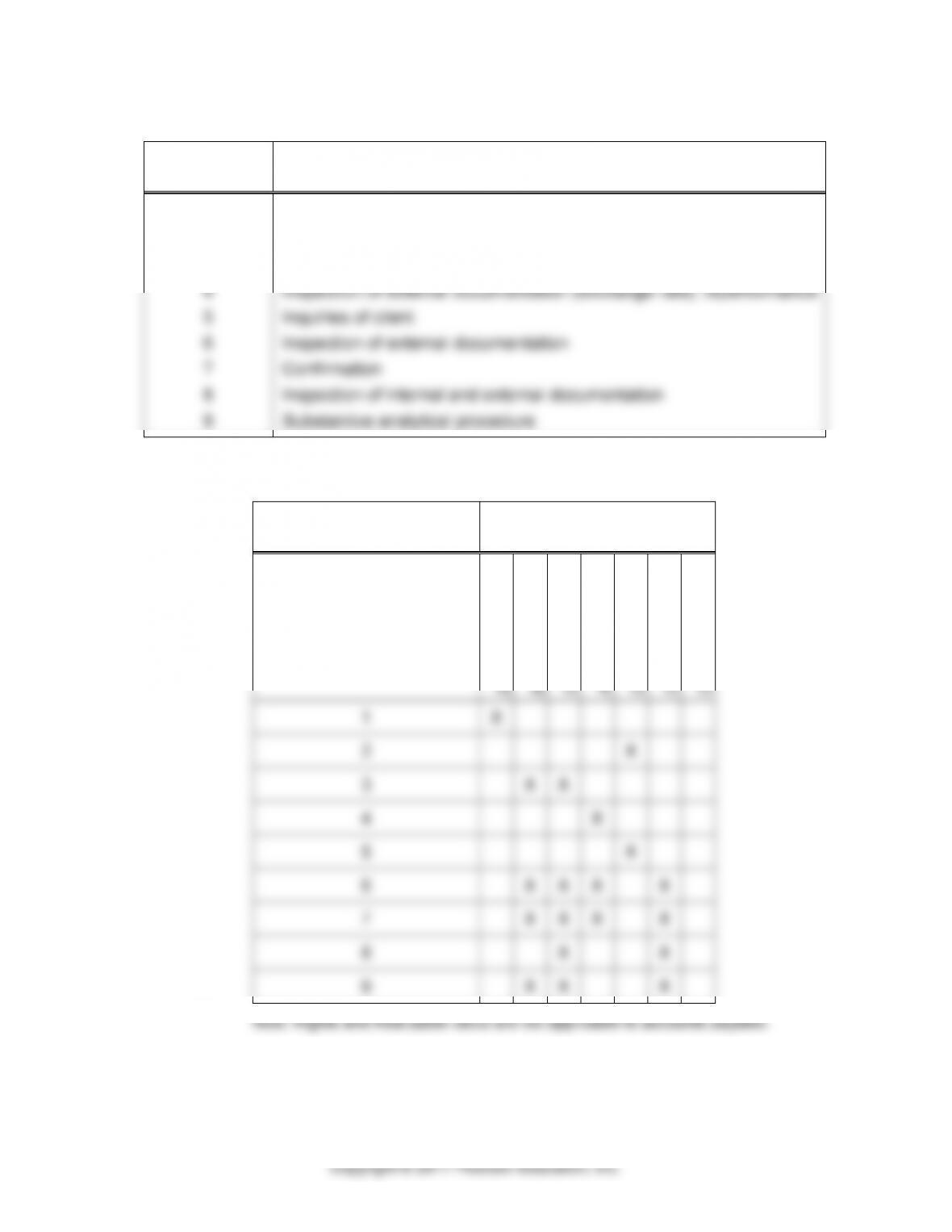

18–25 a. The type of audit evidence used for each procedure is as follows:

AUDIT

PROCEDURE

TYPE OF AUDIT EVIDENCE

1

2

3

4

5

6

7

8

9

Reperformance

Inspection of internal documentation; reperformance

Substantive analytical procedure

Inspection of external documentation (exchange rate); reperformance

Inquiries of client

Inspection of external documentation

Confirmation

Inspection of internal and external documentation

Substantive analytical procedure

b.

AUDIT PROCEDURE

BALANCE–RELATED

AUDIT OBJECTIVE

Detail tie–in

Existence

Completeness

Accuracy

Classification

Cutoff

Obligations

1

X

2

X

3

X

X

4

X

5

X

6

X

X

X

X

7

X

X

X

X

8

X

X

9

X

X

X

18-23

18–25 (continued)

be gathered using other audit procedures.

In this case, the evidence used in procedure 5 is from inquiries

of the client, which is generally a weak form of evidence. Thus, the

Procedure 2 uses internal documentation as its primary

internal documents.

18–26

a. Vouchers 2528 and 2531 were incorrectly included in the June

2016 acquisitions journal. The associated goods were received

after June 30, 2016.

As for July 2016, voucher numbers 2527 and 2530 were

before the end of June 2016.

Let’s assume the corrections were made in two journal entries as

follows:

Accounts payable $11,687.99

Inventory $11,687.99

Inventory $ 6,935.73

Accounts payable $ 6,935.73

vendor invoices or vendor statements to determine if the items

reflected as being received by the client just prior to year end are

18-24

18–26 (continued)

that receipts of goods after year end are not reflected in the

acquisitions journal (and thus the accounts payable balance) as of

year end.

order as goods are received.

Require receiving reports to be routed to accounts payable

daily for immediate voucher preparation.

Accounts payable clerks account for the numerical sequence

of receiving reports and prepare voucher packages in

reports received.

An independent person matches the purchase order,

18–27 a. The fact that the client made a journal entry to record vendors’

invoices which were received late should simplify the CPA’s test

for unrecorded liabilities and reduce the possibility of a need for a

entry. In this audit, the CPA should test entries in the 2017

voucher register to ascertain that all items that were applicable to

2016 have been included in the journal entry recorded by the

client.

18-25

18–27 (continued)

both technically competent and reasonably independent. Once

her work to a less extensive test in this audit area if the results of

the internal auditor’s tests were satisfactory.

c. No. Response to inquiry alone generally does not constitute

responsibility for making his or her own tests.

d. Work done by an auditor for a federal agency will normally have

no effect on the scope of the CPA’s audit, since the concern of

reduce certain work in an area. However, government auditors

are usually interested primarily in substantiating as valid and

allowable those costs which a company has allocated against

specific government contracts or sales to the government, and

statements in other ways.)

e. In addition to the 2017 acquisitions journal, the CPA should

consider the following sources for possible unrecorded liabilities:

1. If a separate cash disbursements journal exists, examine

underlying documentation for disbursements recorded during

the first part of 2017. Determine if any of the disbursements

relate to acquisitions that should have been recorded in

2016.

18–27 (continued)

acquisitions journal.

3. Status of tax returns for prior years still open.

4. Discussions with employees.

5. Representations from management.

6. Comparison of account balances with preceding year.

18–28

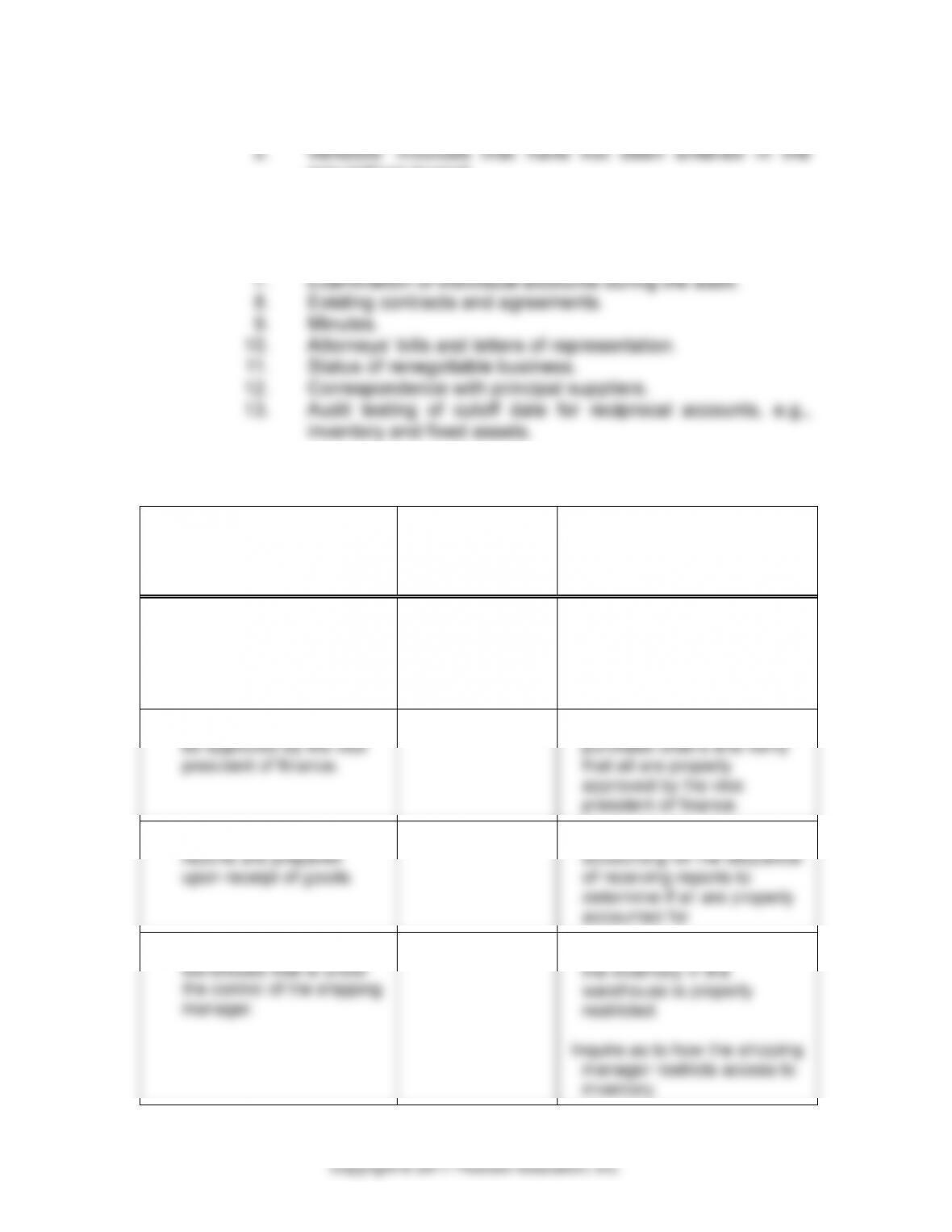

a.

BERGERON

INTERNAL CONTROLS

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

c.

TEST OF CONTROLS

1. Prenumbered purchase

orders are used and

accounted for.

Occurrence,

Completeness

Review Bergeron’s

accounting for the sequence

of purchase orders to

determine if all are properly

accounted for.

2. All purchase orders must

be approved by the vice

president of finance.

Occurrence

Examine a sample of

purchase orders and verify

that all are properly

approved by the vice

president of finance.

3. Prenumbered receiving

reports are prepared

upon receipt of goods.

Completeness

Review Bergeron’s

accounting for the sequence

of receiving reports to

determine if all are properly

accounted for.

4. Goods are stored in a

warehouse that is under

the control of the shipping

manager.

Completeness

Observe whether access to

the inventory in the

warehouse is properly

restricted.

Inquire as to how the shipping

manager restricts access to

inventory.

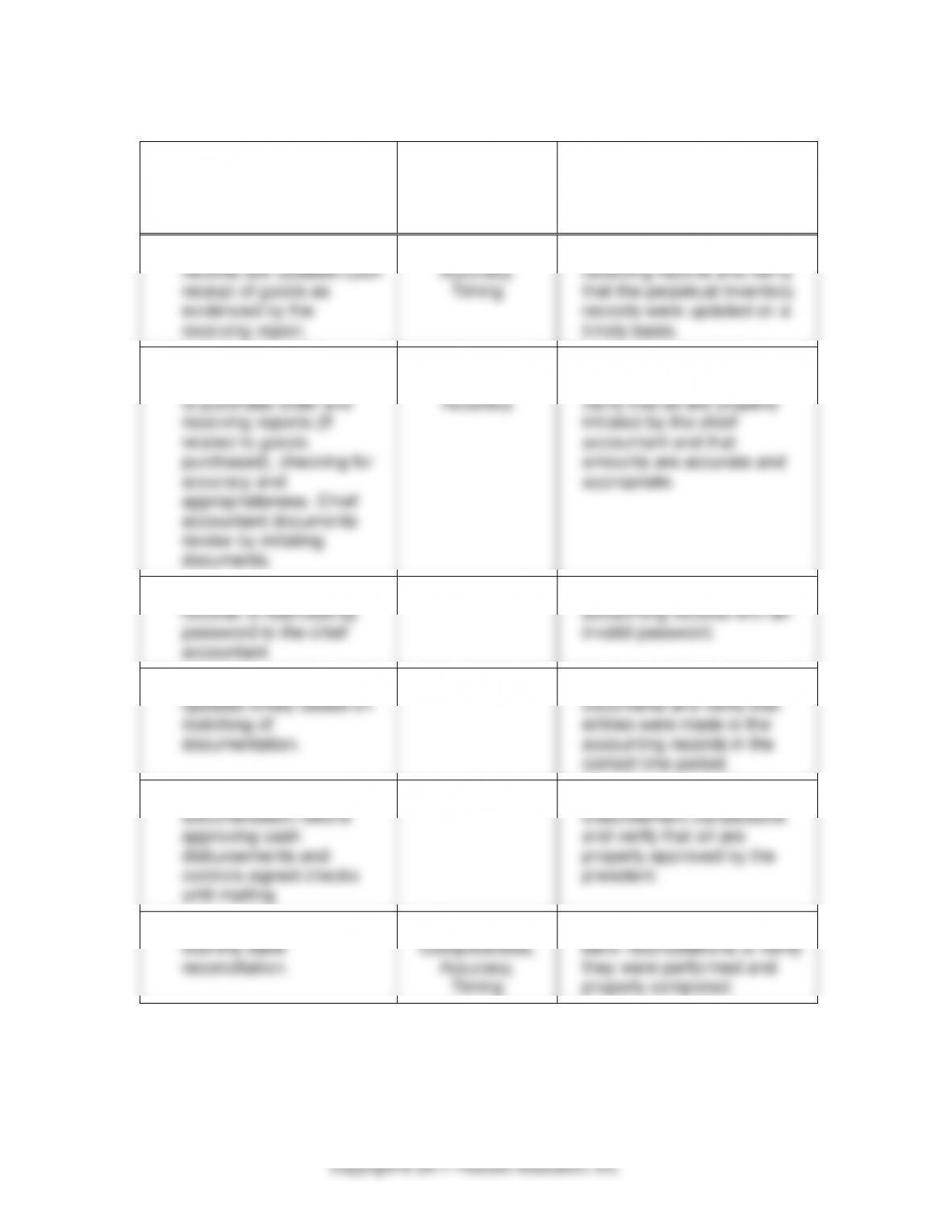

18-28 (continued)

a.

BERGERON

INTERNAL CONTROLS

b.

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

c.

TEST OF CONTROLS

5. Perpetual inventory

records are updated upon

receipt of goods as

evidenced by the

receiving report.

Completeness,

Accuracy,

Timing

Examine a sample of

receiving reports and verify

that the perpetual inventory

records were updated on a

timely basis.

6. Chief accountant

matches vendor invoices

to purchase order and

receiving reports (If

related to goods

purchased), checking for

accuracy and

appropriateness. Chief

accountant documents

review by initialing

documents.

Occurrence,

Completeness,

Accuracy

Examine a sample of

matched documents and

verify that all are properly

initialed by the chief

accountant and that

amounts are accurate and

appropriate.

7. Access to accounting

records is restricted by

password to the chief

accountant.

Occurrence

Attempt to access the

accounting records with an

invalid password.

8. Accounting records are

updated timely based on

matching of

documentation.

Timing

Examine a sample of matched

documents and verify that

entries were made in the

accounting records in the

correct time period.

9. President reviews all

documentation before

approving cash

disbursements and

controls signed checks

until mailing.

Occurrence

Examine a sample of cash

disbursement transactions

and verify that all are

properly approved by the

president.

10. Controller performs a

monthly bank

reconciliation.

Occurrence,

Completeness,

Accuracy,

Timing

Examine a sample of monthly

bank reconciliations to verify

they were performed and

properly completed.