The objective of the audit of financial statements by an independent auditor is to verify

that the financial statements are free of misstatements and accurately represent the

company’s financial position and results of operations.

Analytical procedures may be used to assess the year-end balances for financial

instruments.

The two most important qualities for an operational auditor to possess are independence

and competence.

Analytical procedures must be used in the planning and completion phases of the audit.

The auditing profession has established guidelines for setting inherent risk.

The confidence coefficients for ARIA are different from the confidence level.

Auditors primarily emphasize the understatement of liabilities in the audit of accounts

payable because they are concerned about potential legal liability.

Auditors of the financial statements of public companies must follow the guidelines in

the SSAEs.

A design deficiency exists if the person performing the control is not qualified.

Membership in the AICPA is restricted to CPAs who are currently practicing as

independent auditors.

In obtaining reasonable assurance that the financial statements are free of material

misstatement, the auditor does not need to take into account the applicable legal and

regulatory framework relevant to the client.

A canceled check written by the client, made payable to a local supplier and drawn on

the client’s bank account is one type of internal document.

Directed sample selection, block sample selection, and haphazard sample selection are

three types of probabilistic sample selection methods.

The Single Audit Act applies only to audits of state and local governments.

Notes payable are generally for a period of sixty days or less.

Statements on Auditing Standards (SASs) are issued by the Public Company

Accounting Oversight Board.

The nature, extent, and timing of substantive tests of payroll transactions vary

depending, in part, on assessed control risk.

Acceptable risk of overreliance is the risk that the auditor is willing to take in accepting

a control as effective when the true population exception rate is greater than the

estimated population exception rate.

Ethical frameworks help identify the ethical issues and will always lead to the

appropriate course of action.

If the misstatement bound exceeds tolerable misstatement, the population is considered

acceptable.

The accounts receivable balance-related audit objective net realizable value is not

affected by assessed control risk for sales or cash receipts.

The sampling unit is the physical unit that corresponds to the random numbers the

auditor generates.

Under the Form of Organization and Name rule, a CPA firm is prohibited from

practicing as a limited liability partnership.

A significant internal control deficiency is always considered a material weakness.

Auditors have a higher degree of responsibility for detecting illegal acts that have a

direct effect on the financial statements than illegal acts that do not have a direct effect

on the financial statements.

The auditor must do misstatement analysis to decide whether any modification of the

audit risk model is needed.

If an action is considered legal, it must also be considered ethical.

The auditor must use the same TER and ARO levels for all attributes of an audit test.

A pervasive exception is one that affects different parts of the financial statements.

One factor that determines the amount of additional evidence required for tests of

controls is the planned reduction in control risk.

Auditors should rely on original, rather than duplicate, copies of documents.

Tests of controls and tests of details of balances are the auditor’s most important means

of verifying account balances in the payroll and personnel cycle.

A CPA firm may practice public accounting only in a form of organization permitted by

federal law or regulation.

The realizable value audit objective is not applicable when auditing prepaid insurance

or insurance expense.

To test for recorded sales for which there were no actual shipments, the auditor vouches

from the

A) bill of lading to the sales journal.

B) sales journal to the shipping documents.

C) sales journal to the accounts receivable subsidiary ledger.

D) bill of lading to the supporting customer order and sales order.

A(n) ________ control is a control elsewhere in the system that offsets the absence of a

key control.

A) significant

B) alternate

C) design

D) compensating

The auditor gets highly reliable evidence about individual transactions by examining

A) vendors’ invoices.

B) vendors’ statements.

C) confirmations of accounts payable balances.

D) detailed inventory counting instructions.

The use of the Certified Public Accountant title is regulated by

A) the federal government.

B) state law through the licensing departments of each state.

C) the American Institute of Certified Public Accountants through the licensing

departments of the tax and auditing committees.

D) the Securities and Exchange Commission.

Which of the following is not one of the elements to prevent, deter, and detect fraud

according to the AICPA?

A) performing analytical procedures

B) culture of honesty and high ethics

C) management’s responsibility to evaluate risks of fraud

D) audit committee oversight

Under the Securities Exchange Act of 1934, most of the litigation against the auditor

has been generated because of the auditor’s involvement with the

A) 8-K form.

B) 10-K form.

C) 10-Q form.

D) S-1 form.

To what extent do auditors typically rely on internal controls of their public company

clients?

A) extensively

B) only very little

C) infrequently

D) never

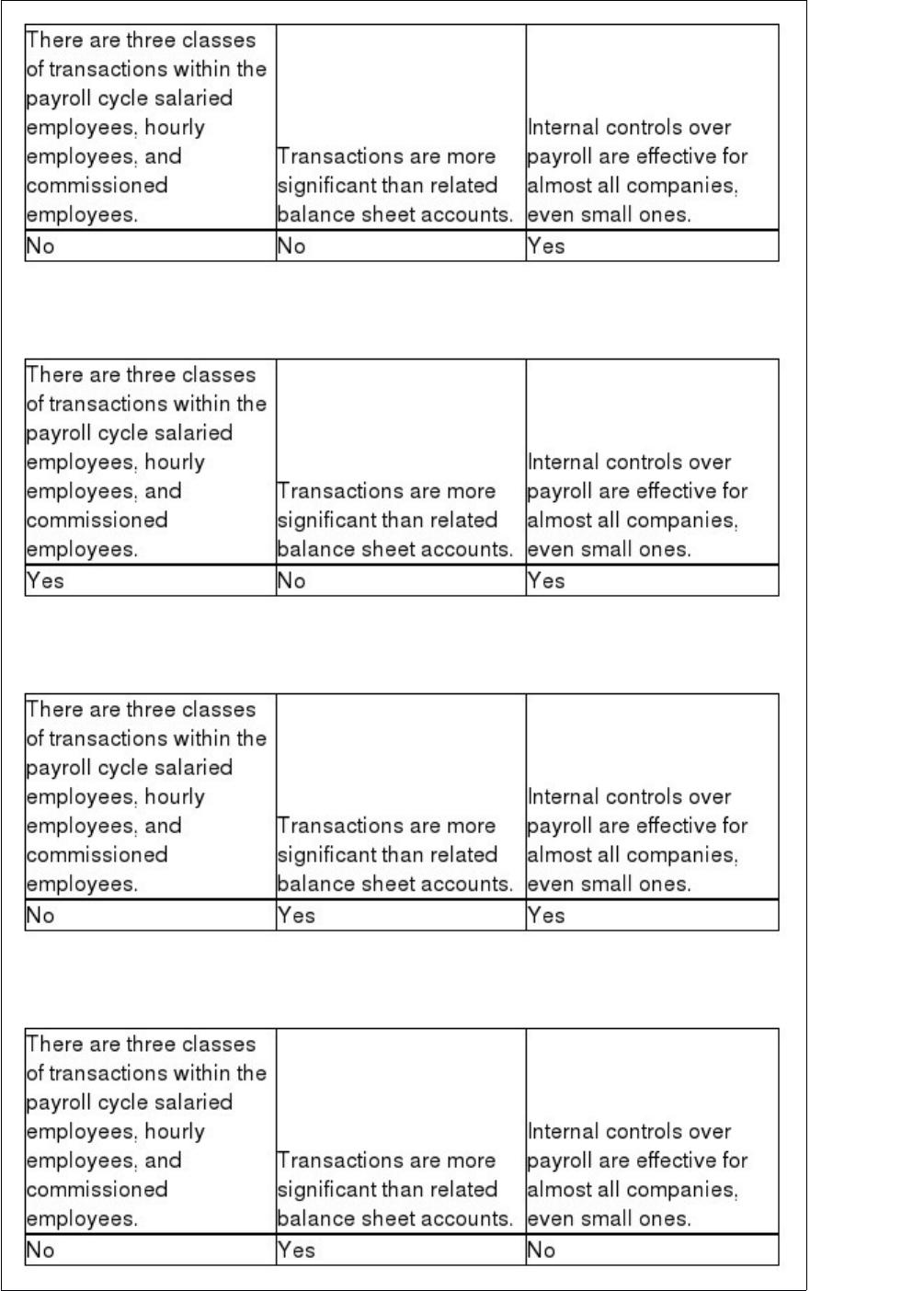

Which of the following statements about the payroll and personnel cycle is correct?

A)

B)

C)

D)

Which of the following would most likely not be included in the evidence mix for an

integrated audit of a public company’s financial statements and internal control over

financial reporting?

A) sophisticated internal controls

B) extensive substantive analytical procedures

C) extensive tests of details of balances

D) low inherent risk

Which of the following is not a factor that relates to opportunities to commit fraudulent

financial reporting?

A) lack of controls related to the calculation and approval of accounting estimates

B) ineffective oversight of financial reporting by the board of directors

C) management’s set of ethical values

D) high turnover of accounting, internal audit, and information technology staff

Which type of audit procedure would normally be sufficient for purposes of auditing

prepaid expenses and deferred charges?

A) tests of controls

B) tests of transactions

C) tests of details of balances

D) substantive analytical procedures

Which of the following is true?

A) Tests of details of balances focus on the ending general ledger balances for both

balance sheet and income statement accounts.

B) Tests of details of balances focus on the transactions during the period for both

balance sheet and income statement accounts.

C) Tests of details of balances focus on the auditor’s understanding of internal controls.

D) Tests of details of balances focus on comparisons of recorded amounts to

expectations developed by the auditor.

An audit must be performed with an attitude of professional skepticism. Professional

skepticism consists of two primary components: a questioning mind and

A) the assumption that upper-level management is dishonest.

B) a critical assessment of the audit evidence.

C) the assumption that all employees are motivated by greed.

D) verification of all critical information by independent third parties.

Which of the following is not a similarity between external and internal auditors?

A) Both must be independent of the company.

B) Both must be competent.

C) Both follow a similar methodology in performing their audits.

D) Both consider risk and materiality deciding the extent of their tests and evaluating

results.

An effective code of conduct should contain the company’s policies regarding

A) conflicts of interests.

B) kickbacks.

C) gifts and entertainment.

D) all of the above.

The 2012 news of a massive alleged bribery scheme involving Wal-Mart has brought

charges against the company under the

A) Securities Act of 1933.

B) Securities Act of 1934.

C) Foreign Corrupt Practices Act of 1977.

D) Sarbanes-Oxley Act of 2002

Which of the following conditions would lead to a larger sample size?

A) larger tolerable misstatement

B) low inherent risk

C) high control risk

D) smaller account balance

The date of the management representation letter received from the client should

A) be the date of latest subsequent event disclosed in the notes to the financial

statements.

B) be dated no earlier than the date of the audit report.

C) have the same date as the date of the balance sheet.

D) have the same date as the date of the engagement letter.

Which of the following statements regarding prospective financial statements is most

correct?

A) CPAs are not attesting to the accuracy of the prospective financial statements.

B) CPAs are attesting to the accuracy of the prospective financial statements.

C) CPAs are performing a review on the company’s assumptions and hypotheticals that

underlie the prospective financial statements.

D) CPAs are performing a review on the achievability of the prospective financial

statements.

You are performing the audit of internal control for Clifton Company. Which of the

following would represent a material weakness in internal control?

A) The company’s audit committee has experienced unusual turnover of members.

B) The company’s CFO was indicted for embezzling from the company.

C) Bank reconciliations are done monthly.

D) The CEO retired after twenty years of service to the company.

A CPA sole practitioner purchased stock in a client corporation and placed it in a trust

as an educational fund for the CPA’s minor child. The trust securities were not material

to the CPA but were material to the child’s personal net worth. Would the independence

of the CPA be considered to be impaired with respect to the client?

A) Yes, because the stock is a direct financial interest.

B) Yes, because the stock is an indirect financial interest that is material to the CPA’s

child.

C) No, because the CPA does not have a direct financial interest in the client.

D) No, because the CPA does not have a material indirect financial interest in the client.

________ is a balance-related audit objective that is not applicable to liabilities.

A) Existence

B) Accuracy

C) Detail tie-in

D) Realizable value

Which of the following accounts is not part of the acquisition and payment cycle?

A) prepaid expenses

B) accounts payable

C) sales returns and allowances

D) property, plant, and equipment

Which of the following is not a typical audit procedure performed as part of the

out-of-period liability tests?

A) Examine underlying documentation for cash disbursements made during the last

month of the year.

B) Examine underlying documentation for bills not paid several weeks after the

year-end.

C) Trace receiving reports issued before year-end to related vendors’ invoices.

D) All of the above are correct.

Auditors respond to risk primarily by

I. changing the extent of testing.

II. changing the types of audit procedures.

A) I only

B) II only

C) I and II

D) neither I nor II

Most auditors assess the risk of material misstatement as high for related parties and

related-party transactions because

A) of the unique classification of related-party transactions required on the balance

sheet.

B) of the lack of independence between the parties.

C) of the unique classification of related-party transactions required on the income

statement.

D) it is required by generally accepted accounting principles.

When examining payroll transactions, an auditor is primarily concerned with the

possibility of

A) incorrect summaries of employee time records.

B) overpayments and unauthorized payments.

C) under withholding of amounts required to be withheld.

D) posting of gross payroll amounts to incorrect salary expense accounts.

An auditor is using audit sampling to test transactions in the acquisition and payment

cycle. She would normally set the tolerable exception rate at what level?

A) Low

B) Medium

C) High

D) Indeterminate

Which of the following tests determines that every field in a record has been

completed?

A) validation

B) sequence

C) completeness

D) programming

Auditors have found that generally the most efficient and effective way to conduct

audits is to

A) obtain complete assurance about the correctness of each class of transactions

affecting the account.

B) obtain some combination of assurance for each class of transactions and for the

ending balance in the related accounts.

C) obtain assurance about the ending balance of the account only.

D) verify each entry that was made into an account.

To make a final evaluation as to whether sufficient appropriate evidence has been

accumulated, the auditor will do all of the following except

A) review the audit documentation for the entire audit to determine whether all material

classes of transactions have been adequately tested.

B) make sure that all parts of the audit program have been accurately completed and

documented.

C) obtain the management representation letter.

D) decide whether the audit program is adequate.

Which of the following expenses is not typically evaluated as part of the audit of the

acquisition and payment cycle?

A) depreciation expense

B) insurance expense

C) estimated liability for warranties

D) property tax expense

Which of the following is not one of the reasons that auditors provide only reasonable

assurance on the financial statements?

A) The auditor commonly examines a sample, rather than the entire population of

transactions.

B) Accounting presentations contain complex estimates which involve uncertainty.

C) Fraudulently prepared financial statements are often difficult to detect.

D) Auditors believe that reasonable assurance is sufficient in the vast majority of cases.

When auditing accrued property taxes,

A) the auditors will generally only verify the larger payments since there are usually

many property tax payments.

B) property taxes should only be charged to one expense account.

C) the auditor begins by obtaining a schedule of property tax payments from the client.

D) the auditor must generally spend a considerable amount of time in this area.

What are three similarities between internal and external auditors?

Explain what lapping means, and discuss the internal control deficiency that allows it to

occur. Also discuss the procedures the auditor can perform to detect lapping.

The design of tests of details of balances for inventory is affected by audit results from

multiple cycles. Identify the cycles, other than the inventory and warehousing cycle that

affect the audit of inventory.

Discuss the two circumstances under which auditors would extend their procedures

considerably in the audit of payroll.

Discuss three major differences between operational and financial auditing.

The internal control framework developed by COSO includes five so-called

“components” of internal control. Discuss each of these five components.

With what types of contingencies might an auditor be concerned?

Discuss three important differences between the payroll and personnel cycle and other

cycles in a typical audit.

Explain why it is necessary to allocate the preliminary judgment about materiality to

individual accounts (segments) in the financial statements. Also explain why allocating

to balance sheet accounts is more common than allocating to income statement

accounts.

Two types of attestation services provided by CPA firms are audits and reviews. Discuss

the similarities and differences between these two types of attestation services. Which

type provides the least assurance?

Discuss the essential activities involved in the initial planning of an audit.

Certain principles dictate the proper design and use of documents and records. Briefly

describe several of these principles.

List the three main types of revenue manipulations employed to commit fraudulent

financial reporting and give an example for each type.

Explain why auditors should compare current year expense totals with prior year

expense totals as an analytical procedure for accounts payable.

Discuss the auditor’s responsibilities for inventory maintained in public warehouses or

with other outside custodians.

List the five steps in applying materiality in an audit.

Discuss the differences in the auditor’s responsibilities for discovering (1) material

errors, (2) material fraud (3) illegal acts having a direct effect on the financial

statements, and (4) illegal acts that do not have a direct effect on the financial

statements.