3-11

3–24 (continued)

an audit is.

7. The audit was made in accordance with auditing standards

than generally accepted accounting standards.

8. The word material is excluded from the statement in

responsibility (free of material misstatement).

9. Additional paragraph(s) should be included that describe

10. The opinion paragraph states that accounting principles

material respects.”

12. The opinion paragraph includes the words “generally accepted

13. The opinion should be qualified rather than being unmodified.

Qualifications are caused by the:

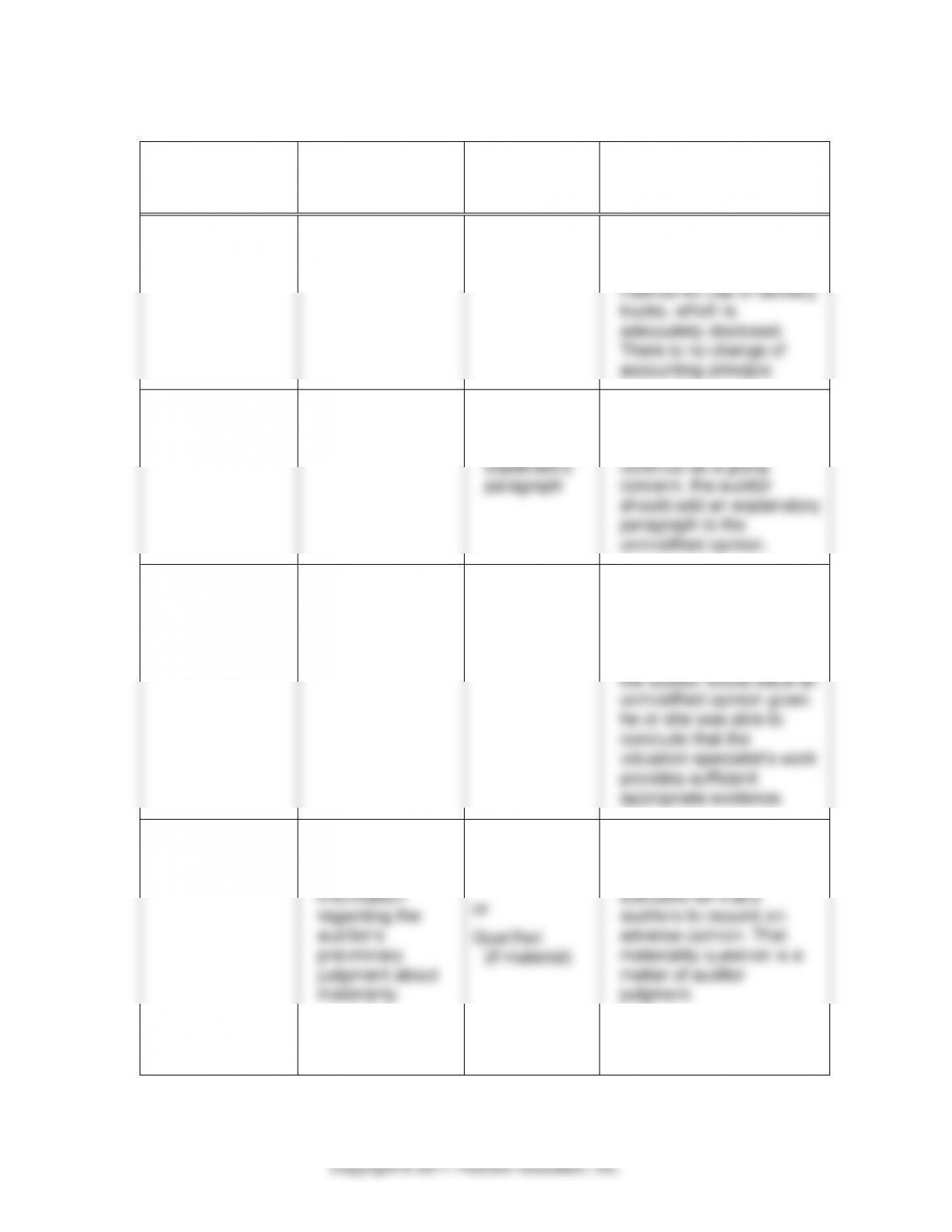

3–25

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF

REPORT

COMMENTS

1. None

Not applicable

Standard,

unmodified

The company has made

a business decision to

follow a different financing

method for use of delivery

trucks, which is

adequately disclosed.

There is no change of

accounting principle.

2. Substantial

doubt about

going concern

Material

Unmodified ─

Emphasis–

of–matter

explanatory

paragraph

Because the auditor has

substantial doubt about

the client’s ability to

continue as a going

concern, the auditor

should add an explanatory

paragraph to the

unmodified opinion.

3. None

Material

Standard,

unmodified

While the auditor engaged

a business valuation

specialist to gather

evidence about the fair

value of the investment,

the auditor would issue an

unmodified opinion given

he or she was able to

conclude that the

valuation specialist’s work

provides sufficient

appropriate evidence.

4. Failure to

follow GAAP

Highly material or

material. We

need additional

information

regarding the

auditor’s

preliminary

judgment about

materiality

Adverse

(if highly

material)

or

Qualified

(if material)

The materiality of twenty

percent of net earnings

before taxes would be

sufficient for many

auditors to require an

adverse opinion. That

materiality question is a

matter of auditor

judgment.

3–25 (continued)

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF

REPORT

COMMENTS

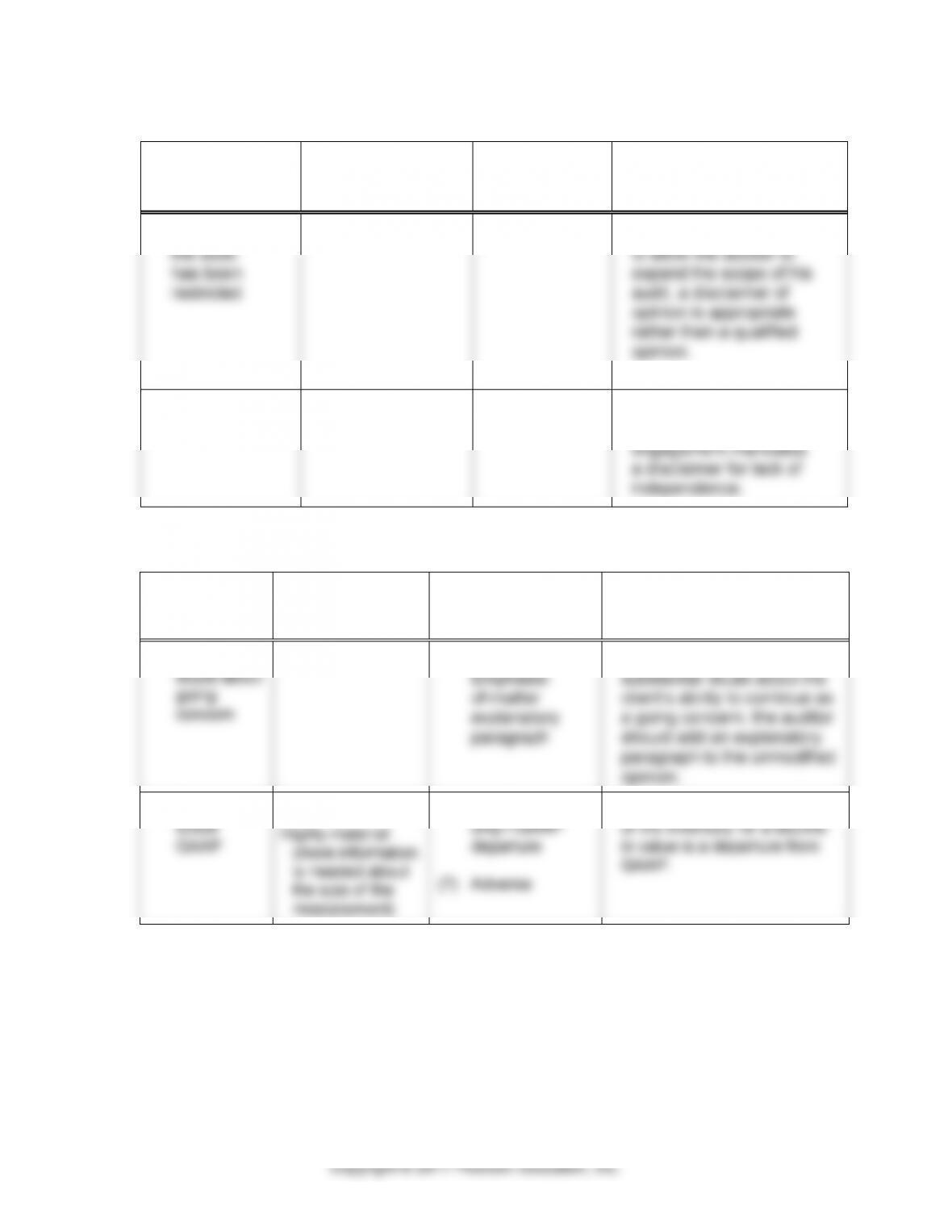

5. Scope of

the audit

has been

restricted

Highly material

Disclaimer

Because the client refuses

to allow the auditor to

expand the scope of his

audit, a disclaimer of

opinion is appropriate

rather than a qualified

opinion.

6. Lack of

independence

Not applicable

Disclaimer

Lack of independence by

audit personnel on the

engagement mandates

a disclaimer for lack of

independence.

3–26

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF REPORT

COMMENTS

1. Substantial

doubt about

going

concern

Material

(2) Unmodified ─

Emphasis–

of–matter

explanatory

paragraph

Because the auditor has

substantial doubt about the

client’s ability to continue as

a going concern, the auditor

should add an explanatory

paragraph to the unmodified

opinion.

2. Failure to

follow

GAAP

Material or

Highly material

(more information

is needed about

the size of the

misstatement)

(4) Qualified opinion

only—GAAP

departure

(7) Adverse

The failure to reduce the value

of the inventory for a decline

in value is a departure from

GAAP.

3-26 (continued)

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF REPORT

COMMENTS

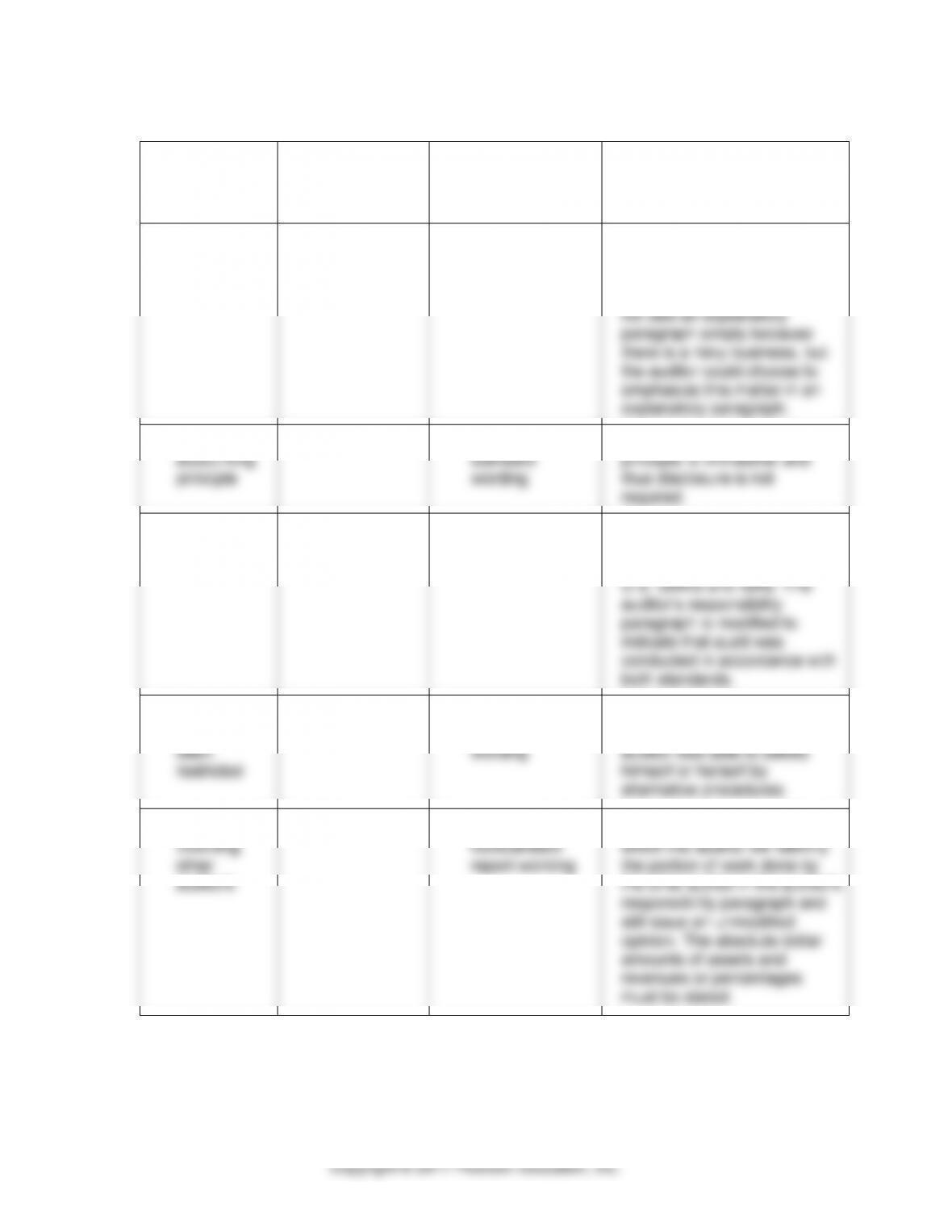

3. None

Not applicable

(1) Unmodified—

standard

wording

There is no indication

questioning the ability of the

business to continue

operations. The auditor does

not add an explanatory

paragraph simply because

there is a risky business, but

the auditor could choose to

emphasize this matter in an

explanatory paragraph.

4. Change in

accounting

principle

Immaterial

(1) Unmodified—

standard

wording

The change in accounting

principle is immaterial and

thus disclosure is not

required.

5. None

Not applicable

(3) Unmodified—

nonstandard

report wording

U.S. auditing standards now

allow an auditor to perform an

audit in accordance with both

U.S. GAAS and ISAs. The

auditor’s responsibility

paragraph is modified to

indicate that audit was

conducted in accordance with

both standards.

6. Scope of the

audit has

been

restricted

Material or Highly

material

(1) Unmodified—

standard

wording

The scope of the audit was

initially restricted, but the

auditor was able to satisfy

himself or herself by

alternative procedures.

7. Report

involving

other

auditors

Material

(3) Unmodified—

nonstandard

report wording

This is a shared audit report in

which the auditor will identify

the portion of work done by

the other auditor in the auditor’s

responsibility paragraph and

still issue an unmodified

opinion. The absolute dollar

amounts of assets and

revenues or percentages

must be stated.

3–27

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF REPORT

COMMENTS

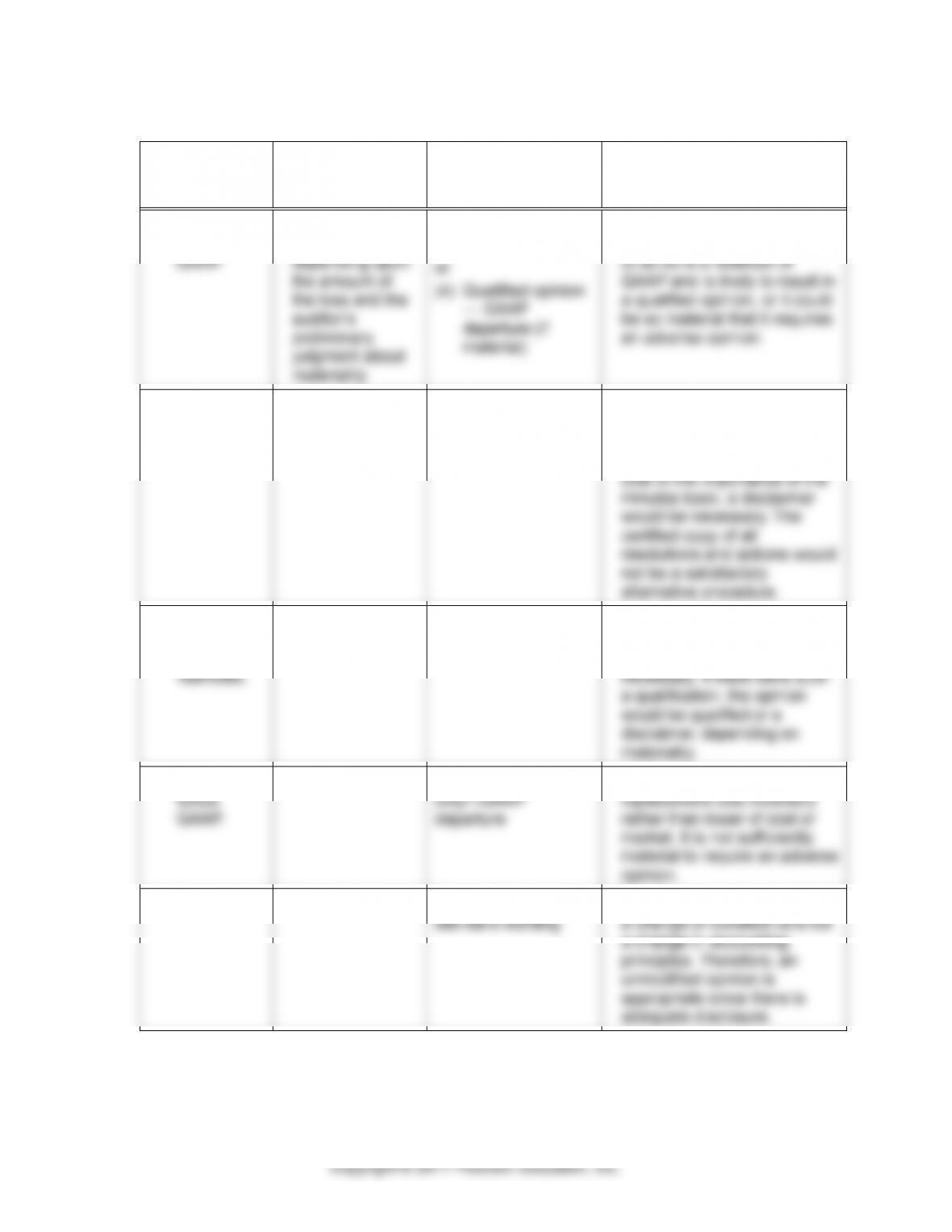

1. Failure to

follow

GAAP.

Highly material

or material,

depending upon

the amount of

the loss and the

auditor’s

preliminary

judgment about

materiality

(7) Adverse (if highly

material)

or

(4) Qualified opinion

— GAAP

departure (if

material)

Disclosure of this information is

required in a footnote. Failure

to do so is a violation of

GAAP and is likely to result in

a qualified opinion, or it could

be so material that it requires

an adverse opinion.

2. Scope of

the audit

has been

restricted.

Highly material

(6) Disclaimer

Failure of the client to allow the

auditor to inspect the minutes

book would be a material

client–imposed restriction.

Due to the importance of the

minutes book, a disclaimer

would be necessary. The

certified copy of all

resolutions and actions would

not be a satisfactory

alternative procedure.

3. Scope of

the audit

has been

restricted.

Not applicable

(1) Unmodified

opinion—

standard wording

Because the auditor was able

to obtain alternative evidence,

no scope qualification is

necessary. If there were such

a qualification, the opinion

would be qualified or a

disclaimer, depending on

materiality.

4. Failure to

follow

GAAP.

Material

(4) Qualified opinion

only—GAAP

departure

Retail Auto Parts has used

replacement cost inventory

rather than lower of cost or

market. It is not sufficiently

material to require an adverse

opinion.

5. None

Not applicable

Unmodified opinion—

standard wording

The change of estimated life is

a change of condition and not

a change in accounting

principles. Therefore, an

unmodified opinion is

appropriate since there is

adequate disclosure.

3–27 (continued)

(a)

CONDITION

(b)

MATERIALITY

LEVEL

(c)

TYPE OF REPORT

COMMENTS

6. Failure to

follow

GAAP.

Immaterial

(1) Unmodified

opinion—

standard wording

The amount is immaterial.

7. Scope of

the audit

has been

restricted.

Highly material

or material,

depending upon

the auditor’s

preliminary

judgment about

materiality.

(6) Disclaimer (if

highly material)

or

(5) Qualified

opinion—scope

limitation (if

material)

Because the auditor was

unable to become satisfied

about beginning inventories,

it is necessary to issue either

a qualified or disclaimer of

opinion on the income

statement and statement of

cash flows as well as the

beginning balance sheet. The

use of a qualified or disclaimer

would depend upon

materiality. An unmodified

opinion could be issued for the

current period balance sheet.

b. Auditing financial statements is a complex process that requires the

knowledge, experience, and judgment of professional auditors. Most

investors are not familiar with the details of the audit process and they

may not be able to appropriately evaluate many of the issues disclosed

management rather than the auditor.

c. The challenge for auditors when making disclosure of critical audit

matters will be determining which items should be communicated and

the nature and extent of that communication. Because most audits

3-17

3–29 a. There are a number of differences between the ISA 700 auditor’s

report and the unmodified opinion audit report for nonpublic entities

shown in Figure 3–1:

1 is in the report title.

3. The unmodified opinion audit report for nonpublic entities includes a

description of what the audit entails, including the auditor’s

consideration of internal control over financial reporting, accounting

4. While both reports acknowledge that the auditor obtains reasonable

5. While the wording differs between the two reports, both the ISA

basis for the opinion issued.

b. There are a number of differences between the ISA 700 auditor’s

report and the standard unmodified opinion audit report for public

companies shown in Figure 3–3.

same disclosure.

3. The unmodified opinion audit report for public companies includes a

brief description of what the audit entails, including the examination

4. While both reports acknowledge that the auditor obtains reasonable

assurance, the ISA reports provides additional information about

3-18

3–29 (continued)

auditor’s conclusion that the audit evidence obtained provides a

basis for the opinion issued

c. The ISA report’s discussion about the importance of auditor

independence provides more explicit emphasis on the independence

key aspects of the audit process and what the auditor has and has not

done.

3–30 a. The following information was obtained from the Form 10–K filing for

Google Inc., for the year ended December 31, 2015:

1. Ernst & Young, LLP is the auditor.

unmodified opinion audit report.

4. According to the auditor’s report on internal controls over financial

reporting, the auditor’s opinion is that Google maintained, in all

5. Both audit reports are dated February XX, 2016.

appropriate guidance in the reorganized standards.

1. Guidance for auditor reporting when there is a material change in

accounting principle is found in paragraphs .17A through .17E of

2. Guidance for considering an entity’s ability to continue as a going

concern is found in AS 2415, Consideration of an Entity’s Ability to

3-19

3–30 (continued)

Paragraphs .12 through .16 of AS 2415 provide guidance about

Documents Containing Audited Financial Statements. Paragraph

.04 of AS 2710 notes that the auditor has no obligation to perform

any audit procedures to corroborate the financial information

contained in the document; however, he or she should read the

other information and consider whether such information is

audited financial statements.