A major consideration in audit staffing is the need for continuity from year to year.

As the impact from noncompliance is further removed from affecting the financial

statements, the less likely the auditor is to become aware of or recognize

noncompliance when auditing the financial statements.

Subsequent events which require adjustment to the financial statements provide

additional information about significant conditions/events which did not exist at the

balance sheet date.

Presentation and disclosure objectives are important when auditing financial

instruments.

There is an indirect relationship between the interest and dividends accounts and debt

and equity.

Items that materially affect the comparability of the financial statements generally

require disclosure in the footnotes.

Substantive tests of balances performed before year-end provide significant assurance

and are normally only done when internal controls are ineffective.

Adverse interest is the threat that a member will not act with objectivity because their

interests are opposed to the client’s interests.

The only parties who can recover from auditors under the Securities Act of 1933 are

original purchasers of securities.

The prelisting of cash receipts should be prepared by the individual who has primary

responsibility for the recording of cash receipts.

The audit procedure “Test clerical accuracy by footing the journals and tracing postings

to general ledger and to accounts payable and inventory master files” is used to test the

posting and summarization objective for acquisitions.

A qualified opinion audit report is issued when all auditing conditions have been met,

no significant misstatements have been discovered, and it is the auditor’s opinion that

the financial statements are fairly stated in accordance with GAAP.

Rights and obligations is the only balance-related assertion without a similar

transaction-related assertion.

Parallel testing is used when old and new systems are operated simultaneously in all

locations.

There should generally be correspondence in the client’s file establishing the

uncollectibility of their account.

Generalized audit software is used to test automated controls.

Difference estimation frequently results in smaller sample sizes than any other variables

sampling method.

When an auditor is determining what information to include in the notes to the financial

statements relating to bonds payable, he is concerned with the transaction-related audit

objectives.

When auditing accounts payable, the auditor is more concerned about the possibility of

understatements than overstatements.

The performance of risk assessment procedures is designed to help the auditor obtain an

understanding of the entity.

The deduction authorization form authorizes the rate of pay and the deductions for

taxes, dues, etc.

For a private company audit, tests of controls are normally performed only on those

internal controls the auditor believes have not been operating effectively during the

period under audit.

When a successor auditor contacts a company’s previous auditor, the predecessor

auditor is required to respond fully and without limit to the request for information.

When auditing the general cash account, receipt of a standard bank confirmation is the

starting point for verifying the company’s general cash account balance.

When an auditor discovers a highly material GAAP violation in the financial statements

and the client refuses to correct it, the auditor should issue a disclaimer of opinion.

The company’s choices for determining the fixed asset’s useful life and residual value

impact the amount of depreciation recorded.

In the AICPA Code of Professional Conduct, the second principle of professional

conduct, entitled “The Public Interest,” applies only to members of the AICPA in public

practice and not to members who work as accountants in business, government, or

education.

The audit report date is the date the auditor completed audit procedures in the field.

The lower the dollar amount of the preliminary judgment, the more audit evidence is

required.

In a lockbox system, bank employees are responsible for opening cash receipts and

maintaining records of all payments made by customers at the lockbox address.

Because auditors are responsible for having appropriate competence and capabilities to

perform an audit, auditors are not normally permitted to consult with outside specialists

during an audit engagement.

Net assets are the most often used base for deciding materiality.

The audit procedure that provides the auditor with the most appropriate evidence when

performing test of details of balances for accounts receivable is

A) confirmations.

B) recalculation of the aged receivables and uncollectible accounts.

C) tracing credit memos for returned merchandise to receiving room reports.

D) tracing from shipping documents to journals to the accounts receivable ledger.

When a dividend is declared by the board of directors, the source for determining who

should receive dividend checks is the

A) shareholders’ capital stock master file.

B) stock certificate books.

C) common stock account in the general ledger.

D) corporate directory.

In which type of service does the CPA assemble the financial statements but provide no

assurance to third parties?

A) audit

B) compilation

C) review

D) bookkeeping

Internal controls that are likely to prevent the client from including as a business

expense those transactions that primarily benefit management or other employees rather

that the entity being audited satisfy the control objective that

A) acquisitions are correctly valued.

B) existing acquisitions are recorded.

C) acquisitions are correctly classified.

D) recorded acquisitions are for goods and services received.

The internal control framework used by most U.S. companies is the ________

framework.

A) FASB

B) PCAOB

C) COSO

D) SEC

External users of the financial statements

A) value the auditor’s report because of the auditor’s independence from the client.

B) look to the auditor’s report as an indication of the statements’ reliability.

C) use the audited information on the assumption that it is reasonably complete,

accurate, and unbiased.

D) all of the above.

Which one of the following is more difficult to evaluate objectively?

A) presentation of financial statements in accordance with generally accepted

accounting principles

B) compliance with government regulations

C) efficiency and effectiveness of operations

D) All three of the above are equally difficult.

The two most important balance-related audit objectives for notes payable are

A) completeness and detail tie-in.

B) completeness and valuation.

C) accuracy and valuation.

D) accuracy and completeness.

A document used by organizations to establish a formal means of recording and

controlling acquisitions which usually contains a package of documents about the

acquisition is the

A) voucher.

B) purchase order.

C) receiving report.

D) purchase requisition.

A CPA performs bookkeeping services for a client and then performs an audit of those

financial statements. This is an example of a ________ threat.

A) familiarity

B) self-interest

C) self-review

D) management participation

A high, but not absolute, level of assurance is called

A) probable assurance.

B) reasonable assurance.

C) limited assurance.

D) incomplete assurance.

What type of SOC report is intended to meet the needs of entities that use service

organizations and their auditors, who are responsible for understanding internal controls

over financial reporting at service organizations?

A) SOC 1 report

B) SOC 2 report

C) SOC 3 report

D) none of the above

A positive confirmation is more reliable evidence than a negative confirmation because

A) fewer confirmations can be sent out.

B) the auditor has a document which can be used in court.

C) the debtor’s lack of response indicates agreement with the stated balance.

D) follow-up procedures are performed if a response is not received from the debtor.

Freedom from ________ means the absence of relationships that might interfere with

objectivity or integrity.

A) independence

B) acts discreditable

C) impartiality

D) conflicts of interest

There is inherent risk of payroll fraud because most transactions involve

A) expense accounts.

B) accrued liabilities.

C) estimates.

D) cash.

In which of the following circumstances would an auditor most likely express an

adverse opinion?

A) The CEO refuses to let the auditor have access to the board of director meeting

minutes.

B) The financial statements are not in conformity with the FASB statement on loss

contingencies.

C) Information comes to the auditor’s attention that raises substantial doubt about the

ability for the client to continue as a going concern.

D) Tests of controls show that the internal control structure is so poor that the auditor

has to assess control risk at the maximum.

When the auditor identifies risk at the assertion level,

A) the auditor may need to obtain audit evidence that is more reliable and relevant.

B) the auditor may choose to conduct substantive testing during interim periods rather

than at the end of the period.

C) the auditor may decrease the sample size.

D) both a and b

Because of the importance of tests of controls and substantive tests of transactions for

acquisitions and cash disbursements, it is common in this audit area to use

A) block sampling.

B) variables sampling.

C) attributes sampling.

D) probability proportional to size sampling.

How might the auditor determine whether a client has limited rights to accounts

receivable?

A)

B)

C)

D)

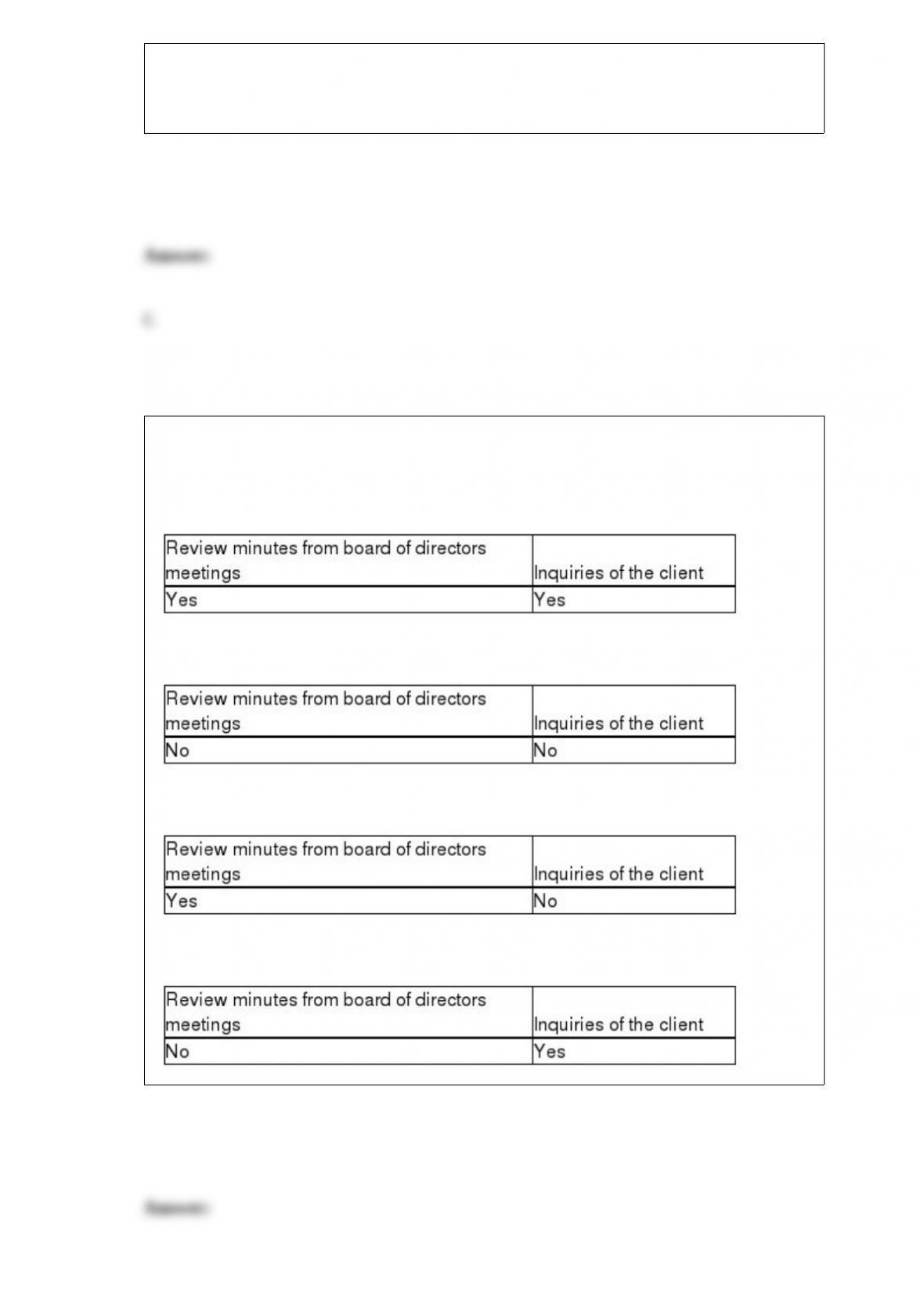

An auditor should examine minutes of the board of directors’ meetings

A) through the date of the financial statements.

B) through the date of the audit report.

C) only at the beginning of the audit.

D) on a test basis.

Appropriateness of evidence is a measure of the

A) quantity of evidence.

B) quality of evidence.

C) sufficiency of evidence.

D) meaning of evidence.

Subsequent events affecting the realization of assets ordinarily will require an

adjustment of the financial statements under examination because such events typically

represent

A) the culmination of conditions that existed at the balance sheet date.

B) additional new information related to events that were in existence on the balance

sheet date.

C) final estimates of losses relating to casualties occurring in the subsequent events

period.

D) preliminary estimate of losses relating to new events that occurred subsequent to the

balance sheet date.

All of the following are owners’ equity accounts except for

A) common stock.

B) paid-in-capital in excess of par.

C) sales.

D) retained earnings.

The most important balance-related audit objectives in the audit of cash include all

except which of the following?

A) existence

B) accuracy

C) completeness

D) occurrence

Statements on Standards for Attestation Engagements are established by the

A) Securities and Exchange Commission.

B) Public Company Accounting Oversight Board.

C) Auditing Standards Board of the AICPA.

D) Accounting and Review Services Committee.

________ inquiry is used to obtain information about facts and details that the auditor

does not have, usually about past or current events or processes.

A) Assessment

B) Declarative

C) Interrogative

D) Informational

When defining the population,

A) it may be necessary to define separate populations for different audit procedures.

B) the auditor may generalize only about the population that has been sampled.

C) auditors can define the population to include any items they want.

D) all of the above

A major consideration in verifying the ending balance in fixed assets is the possibility

of existing legal encumbrances. Tests to identify possible legal encumbrances would

satisfy the audit objective of

A) existence.

B) presentation and disclosure.

C) detail tie-in.

D) classification.

You are auditing Rodgers and Company. You are aware of a potential loss due to

noncompliance with environmental regulations. Management has assessed that there is

a 40% chance that a $10M payment could result from the non-compliance. The

appropriate financial statement treatment is to

A) accrue a $4 million liability.

B) disclose a liability and provide a range of outcomes.

C) since there is less than a 50% chance of occurrence, ignore.

D) since there is greater that a remote chance of occurrence, accrue the $10 million.

If an auditor judgmentally selects a sample of one hundred items from a population and

finds two exceptions, the auditor

A) can conclude that the sample exception rate is 2%.

B) can conclude that the population exception rate is 2%.

C) can calculate the highest exception rate expected in the population.

D) cannot make any conclusions about either the sample or the population.

If the board of accountancy in the state in which a CPA firm is licensed has rules that

are different than the AICPA’s rules, the CPA firm must follow

A) whichever rules are less restrictive.

B) whichever rules are more restrictive.

C) the rules of the AICPA.

D) the rules of the state’s board of accountancy.

Direct, written communication with the client’s customers to identify whether a

receivable exists is an example of a(n)

A) substantive test of transactions.

B) test of controls.

C) analytical procedure.

D) test of details of balances.

Which of the following audit procedures would normally be included in the audit plan

when auditing the allowance for doubtful accounts?

A) Send positive confirmations.

B) Inquire of the client’s credit manager.

C) Send negative confirmations.

D) Examine sales invoices.

________ risk reflects the possibility that the information upon which the business

decision was made was inaccurate.

A) Client acceptance

B) Information

C) Business

D) Control

An example of an external document that provides reliable information for the auditor

is: a(n)

A) employees’ time report.

B) bank statement.

C) purchase order for company purchases.

D) carbon copies of a check.

Briefly describe the circumstances in which it is acceptable to use negative

confirmation requests.

Risk assessment procedures are performed to identify and assess the risk of material

misstatement. List three risk assessment procedures.

Management’s identification and analysis of risk is an ongoing process and is a critical

component of effective internal control. An important first step is for management to

identify factors that may increase risk. Identify at least five factors, observable by

management, which may lead to increased risk in a typical business organization.

List the three reasons why an experienced member of the audit firm must thoroughly

review audit documentation at the completion of the audit.

Briefly describe each of the five Trust Services principles.

Discuss the purpose of the Securities and Exchange Commission and its influence on

setting generally accepted accounting principles.

List the two ways auditors can control sampling risk.

An important balance-related audit objective is realizable value. Describe the purpose

of this audit objective, what it is concerned with, and give an example.

Define fraud and distinguish between the two main categories of fraud.

What key separation of duties should the auditor expect to find within the payroll and

personnel cycle?

Auditor’s allocate the preliminary judgment about materiality to financial statement

segments rather than by financial statements as a whole. What is the term for the

auditor’s allocation of preliminary misstatement to account balances? What are three

difficulties auditors face when allocating materiality to balance sheet accounts?

There are several key internal controls over the payment of payroll function that should

be present. For example, the payroll should be distributed by someone who is not

involved in the other payroll functions. Discuss other key internal controls over the

payment of payroll function as it relates to the physical control over assets and records.

What are the auditor’s primary concerns in verifying the transfer of inventory from one

location to another?

Discuss the procedures involved in, and the purpose of a surprise payroll payoff.

Discuss four of the matters that should be specified in an engagement letter.

The most common fraud in the acquisition and payment cycle is for the perpetrator to

issue payments to fictitious vendors and deposit the cash in fictitious accounts. What

procedures could the company take to prevent this type of fraud?