53

19) Smith and Jones, CPAs, audited the consolidated financial statements of Concord Inc. and all

but one of its subsidiaries for the year ended September 30, 2016 and are expressing an

unqualified opinion on the financials presented as a whole.

Smith, the engagement partner, instructed Mary, an assistant on the engagement, to draft the

auditor’s report on November 4, 2016, the date of fieldwork completion. In drafting the report

Mary considered the following:

• In preparing its financial statements, Concord changed its method of accounting for research

and development costs and properly expensed these amounts. Management described the change

in principle in Note 10 to the consolidated financial statements.

• Ball & Brown, CPAs, audited the financial statements of Biotherm, Inc., a consolidated

subsidiary of Concord for the year ended September 30, 2016. The subsidiary’s financial

statements reflect total assets of 22% and total revenues of 20% of the consolidated totals. Ball &

Brown expressed an unqualified opinion and furnished to Smith & Jones a copy of their auditor

report. Smith & Jones have decided not to assume responsibility for the work of Ball & Brown

insofar as it relates to the expression of an opinion on the consolidated financial statements taken

as a whole because of the materiality of Biotherm’s financial statements to the consolidated

whole. Ball & Brown’s report will not be presented together with that of Smith & Jones.

• Concord is the subject of a grand jury investigation into possible violations of federal

antitrust laws and possible related crimes. Related civil class actions are pending. Concord’s

management has adequately disclosed in Note 12 to their consolidated financial statements.

Because of the early stage of the investigation, the ultimate outcome of these matters cannot be

determined at this time. Therefore, no provision for any liability that may result has been

recorded.

• Concord experienced a net loss in 2016 and is currently in default under substantially all of

its debt agreements. Management’s plans in regard to these matters are adequately disclosed in

Note 14 to Concord’s consolidated financial statements. The financials do not include any

adjustments that might result from the outcome of this uncertainty. These matters rase substantial

doubt about Concord’s ability to continue as a going concern.

Ball reviewed Mary’s draft and indicated in his review notes that there were many deficiencies in

Mary’s Draft. The audit report that Mary drafted follows.

Independent Auditor’s Report

We have audited the consolidated financial statements of Concord, Inc., and subsidiaries as of

September 30, 2016, and the related consolidated statements of income, changes in stockholders

equity and cash flows for the year then ended. These financial statements are the responsibility of

the Company’s management. Our responsibility is to express an opinion on these financial

statements based on our audits. We did not audit the financial statements of Biotherm, Inc., a

wholly-owned subsidiary, which statements reflect total assets and revenues constituting 22%

and 20% respectively at September 30, 2016 of the consolidated totals. Those statements were

audited by Ball & Brown, CPAs, whose reports have been furnished to us, and our opinion,

insofar as it relates to the amounts included for Biotherm, Inc. is based solely on their report.

54

We conducted our audit in accordance with generally accepted auditing standards. Those

standards require that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement. An audit includes examining,

on a test basis, evidence supporting the amounts and disclosures in the financial statements. An

audit also includes assessing the accounting principles used, as well as assessing control risk. We

believe our audits provide a reasonable basis for our opinion.

In our opinion, based on our audit and the report of the other auditors, the consolidated financial

statements referred to above present fairly, in all material respects, the financial position of

Concord Inc., as of September 30, 2016 in conformity with generally accepted accounting

principles, except for the uncertainty, which is discussed in Note 12 to the consolidated

financials.

The accompanying consolidated financial statements have been prepared assuming that the

Company will continue in existence for a reasonable period of time. As discussed in Note 14 to

the consolidated financial statements, the Company suffered a net loss and is currently in default

under substantially all of its debt agreements. Management’s plans in regard to these matters are

also described in Note 14. The consolidated financial statements do not include any adjustments

that might result from the outcome of this uncertainty.

Smith & Jones, CPAs

November 4, 2016

Required:

The following items present some of the deficiencies in the drafted audit report noted by Smith.

For each deficiency, indicate whether:

S. Smith’s review note is correct

M. Mary’s draft is correct

B. Both Smith’s review note and Mary’s draft are incorrect

Smith’s Review Notes

1. An explanatory paragraph is required between the scope and opinion paragraphs for the

change in accounting principles referring the reader to Note 10.

2. The names of the other auditors do not need to be explicitly stated in the introductory

paragraph. Only that “other auditors” performed the audit and provided their report.

3. The opinion paragraph should extend the auditor’s opinion beyond financial position to

include the results of Concord’s operations and flows.

4. The reference to the uncertainty in the opinion paragraph is incomplete. It should describe the

nature of the uncertainty as pertaining to the grand jury investigation into possible violations of

federal antitrust laws.

55

5. The explanatory paragraph following the opinion paragraph does not include the terms

“substantial doubt” and “going concern”. These terms are required to be used in this paragraph.

6. The explanatory paragraph following the opinion paragraph includes an inappropriate

statement that “the consolidated financial statements do not include any adjustments that might

result from the outcome of this uncertainty.” This statement is misleading and should be omitted.

56

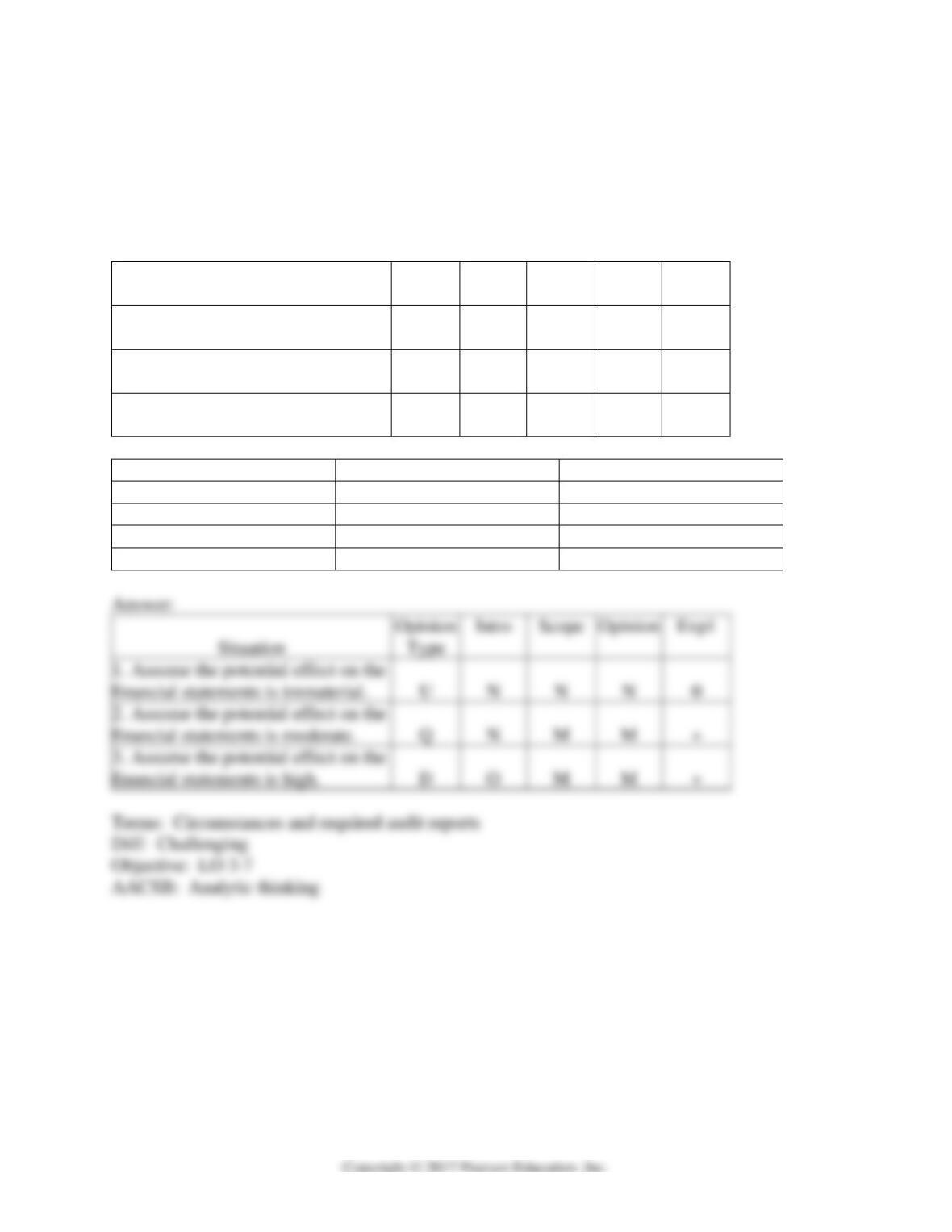

20) In auditing the long-term investments account, Arens, CPA, is unable to obtain audited

financial statements for an investee located in a foreign country. Levine concludes sufficient

appropriate audit evidence regarding this investment cannot be obtained.

For each of the following situations below, identify the appropriate opinion type and report

modification by selecting a choice from the appropriate tables below.

Situation

Opinion

Type

Intro

Scope

Opinion

Exp1

1. Assume the potential effect on the

financial statements is immaterial.

2. Assume the potential effect on the

financial statements is moderate.

3. Assume the potential effect on the

financial statements is high.

Opinion Type

Standard Paragraph Choice

Explanatory Paragraph

U Unmodified

O Omit

0 None required

Q Qualified

N No change

+ Insert before opinion

A Adverse

M Modify

– Insert after opinion

D Disclaimer

Situation

Type

1. Assume the potential effect on the

financial statements is immaterial.

N

N

2. Assume the potential effect on the

financial statements is moderate.

N

M

3. Assume the potential effect on the

financial statements is high.

O

M

57

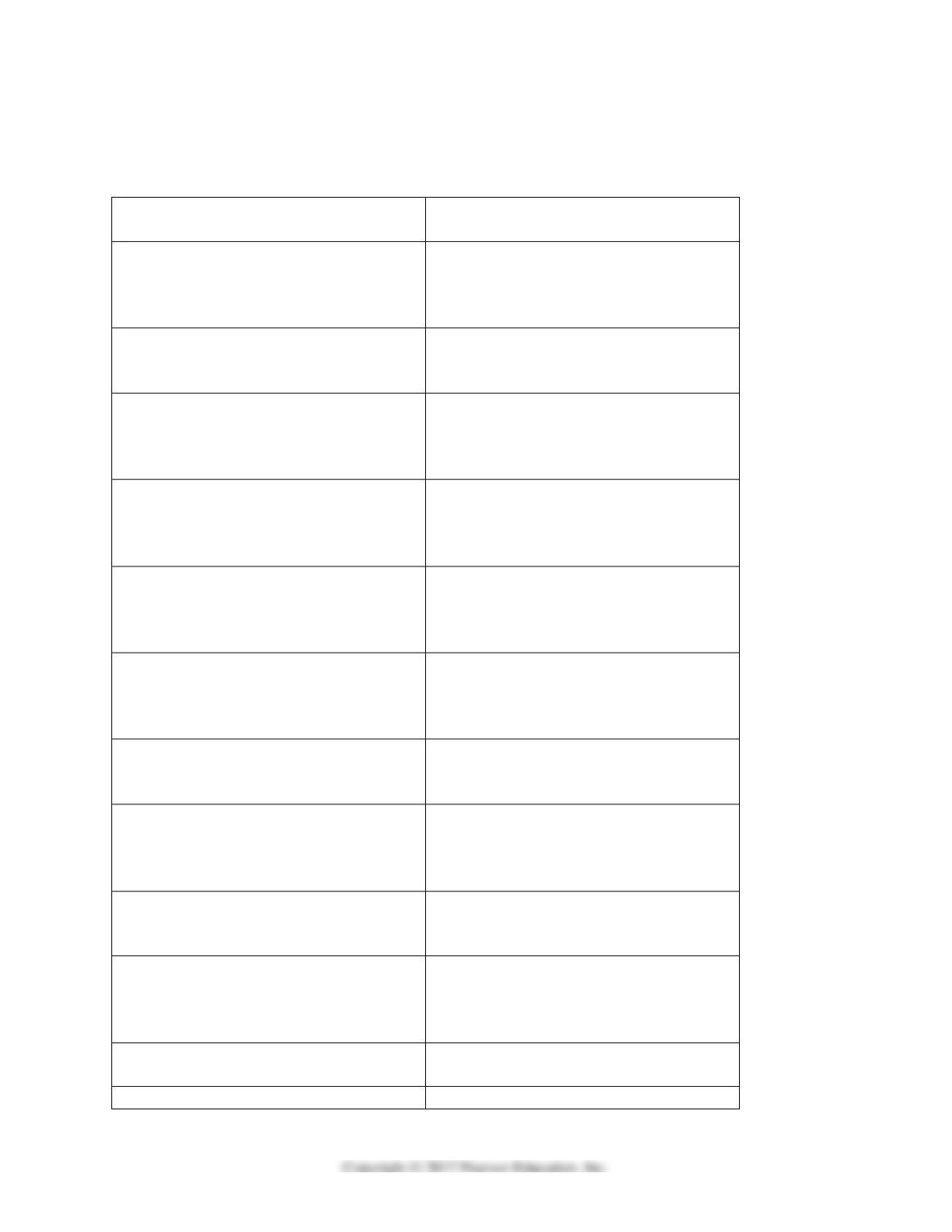

21) Audit situations 1 through 10 present various independent factual situations an auditor might

encounter in conducting an audit. List A represents the types of opinions the auditor ordinarily

would issue, and List B represents the report modifications (if any) that would be necessary. For

each situation, select one response from List A and one from List B. Select, as the best answer

for each item, the action the auditor normally would take. Items from either list may be selected

once, more than once, or not at all.

Assume the following:

• The auditor is independent

• The auditor previously expressed an unmodified opinion on the prior-year financial

statements unless otherwise noted

• Only single-year (not comparative) statements are presented for the current year (unless

otherwise stated)

• The conditions for an unmodified opinion exist unless contradicted in the factual scenario

• The conditions stated in the factual scenario are material

• No report modifications are to be made except in response to the factual scenario

Factual Scenario

1. The financial statements present fairly, in all material respects, the financial position, results of

operations, and cash flows in conformity with GAAP.

2. In auditing the Long-Term Investments account, an auditor is unable to obtain audited

financial statements for an investee located in a foreign country. The auditor concludes that

sufficient competent evidential matter regarding this investment cannot be obtained but it is not

pervasive to the financials as a whole.

3. Due to recurring operating losses and working capital deficiencies the auditor has substantial

doubt about an entity’s ability to continue as a going concern for a reasonable period of time.

However, the financial statement disclosures are adequate.

4. The principal auditor decides to refer to the work of another auditor, who audited a wholly

owned subsidiary of the entity and issued an unqualified opinion.

5. An entity issues financial statements that present financial position and results of operations

but omits the related statement of cash flows. Management discloses in the notes to the financial

statements that it does not believe the statement of cash flows to be useful.

6. An entity changes its depreciation method for production equipment from straight-line to units

of production based on hours of utilization. The auditor concurs with the change, although it has

a material effect on the comparability of the entity’s financial statements.

7. An entity is a defendant in a lawsuit alleging infringement of certain patent rights. However,

management cannot reasonably estimate the ultimate outcome of the litigation. The auditor

believes that there is a reasonable possibility of a significant material loss, but the lawsuit is

adequately disclosed in the notes to the financial statements.

8. An entity discloses certain lease obligations in the notes to the financial statements. The

auditor believes that the failure to capitalize these leases is a departure from GAAP.

9. The entity wishes to show comparative financial statements and include the prior year.

However, the prior year financial statements contained a qualification due to an inappropriate

method of GAAP. Accordingly, management corrected the prior year GAAP deficiency and

included the updated numbers in the comparative financials for the current year.

58

10. The entity wishes to show comparative financial statements and include the prior year.

However, the prior year financial statements were audited by another auditor who refuses to

reissue his opinion.

List A

Opinion Choices

List B

Report Modification Choices

A Qualified

H Describe the circumstances in an

explanatory paragraph preceding the

opinion paragraph w/o modifying the

three standard paragraphs.

B Unmodified

I Describe the circumstances in the

opinion paragraph w/o adding an

explanatory paragraph.

C Adverse

J Describe the circumstances in an

explanatory paragraph preceding the

opinion paragraph and modify the

opinion paragraph.

D Disclaimer

K Describe the circumstances in an

explanatory paragraph following the

opinion paragraph and modify the

opinion paragraph.

E Either Qualified or Adverse

L Describe the circumstances in an

explanatory paragraph preceding the

opinion paragraph and modify the scope

& opinion paragraph.

F Either Disclaimer or Adverse

M Describe the circumstances in an

explanatory paragraph following the

opinion paragraph and modify the scope

& opinion paragraph.

G Either Qualified or Disclaimer

N Describe the circumstances in the

scope paragraph w/o adding an

explanatory paragraph.

O Describe the circumstances in an

explanatory paragraph following the

opinion paragraph w/o modifying the

three standard paragraphs.

P Describe the circumstances in the

introductory paragraph w/o adding an

explanatory paragraph.

.

Q Describe the circumstances in the

introductory paragraph w/o adding an

explanatory paragraph, and modify the

scope & opinion paragraphs.

R Issue the standard auditor’s report w/o

modification.

S None of the above.

59

22) Financial statement users are typically more concerned with an unmodified report with

explanatory paragraphs than they are with a disclaimer of opinion.

23) A lack of independence will override any other scope limitations and requires a disclaimer of

opinion.

24) When a qualified opinion is issued, an explanatory paragraph is added immediately after the

opinion paragraph to explain the nature of the qualification that affects the opinion.

60

25) In the case of a disclaimer due to lack of independence, the entire scope paragraph is

excluded from the report.

3.8 Learning Objective 3-8

1) When accounting principles are not consistently applied, and the materiality level is

immaterial, the auditor will issue a(n)

A) standard unmodified opinion.

B) unmodified opinion with an explanatory paragraph.

C) adverse opinion.

D) disclaimer opinion.

2) The first step to be followed when deciding the appropriate audit report in a given set of

circumstances is to

A) decide the appropriate type of report for the condition.

B) write the report.

C) determine whether any conditions exists requiring a departure from a standard unmodified

opinion audit report.

D) decide the materiality for each condition.

3) In most audits, the auditor issues a(n)

A) modified opinion audit report.

B) standard unmodified opinion audit report.

C) scope limited audit report.

D) adverse audit report.

61

4) More than one modification should be included in the audit report when

A) the auditor is not independent and the auditor knows that the company has not followed

generally accepted accounting principles.

B) there is substantial doubt about the going concern of the company and information about the

causes of the uncertainties is not adequately disclosed in the footnotes.

C) there is a scope limitation and there is substantial doubt about the company’s ability to

continue as a going concern.

D) all of the above

5) When there is a justified departure from GAAP which is considered material, the auditor

should issue a(n)

A) standard unmodified opinion.

B) disclaimer of opinion.

C) unmodified opinion with an explanatory paragraph.

D) adverse opinion.

6) If there is a deviation in the statements’ preparation in accordance with GAAP and another

accounting principle was applied on a basis that was not consistent with that of the preceding

year,

A) the auditor must choose which modification to include in the audit report.

B) only the most material modification can be disclosed.

C) more than one modification should be included in the report.

D) none of the above.

62

7) After the auditor determines whether any conditions exist which require a departure from a

standard unmodified opinion audit report, the next step in the decision process is to

A) write the report.

B) decide the materiality for each condition.

C) decide the appropriate type of report for the condition.

D) discuss the report with management.

8) For departures from GAAP or scope restrictions, the auditor must decide if the potential effect

on the financial statements is

A) immaterial.

B) material.

C) highly material.

D) any of the above.

9) If the scope restriction imposed by the client is so material that the overall fairness of the

financial statements is in question, the auditor should issue a(n)

A) standard unmodified opinion.

B) disclaimer of opinion.

C) adverse opinion.

D) unmodified opinion with revised wording in the scope paragraph.

10) The final step in the auditor’s decision process for audit reports is to write the audit report.

63

11) Auditors usually make the materiality judgment by referring to a standard checklist.

3.9 Learning Objective 3-9

1) Which of the following is correct regarding IFRS?

A) Companies that are required to file their financial statements with the SEC must follow IFRS

starting in 2015.

B) Recent developments suggest that the SEC may be slowing down its efforts towards adopting

IFRS any time soon.

C) When an auditor is engaged to report on financial statements prepared in accordance with

IFRS, they must issue a qualified opinion.

D) The introductory paragraph of the audit report is modified to indicate that the audit was

conducted in accordance with International Standards on Auditing.

2) Auditing standards in the United States allow an auditor to perform an audit of a nonpublic

U.S. entity in accordance with both generally accepted auditing standards in the U.S. and the

ISAs.