When errors are found in a sample, auditors in practice generally make the assumption

A) that the population errors cannot be determined.

B) that the population errors are larger than the sample errors.

C) that the population errors are smaller than the sample errors.

D) that the actual sample errors are representative of the population errors.

The auditors test the client’s monthly bank reconciliation to verify whether the client’s

recorded bank balance is the same amount as the actual cash in the bank. Which of the

following would not explain a difference between the company’s cash balance and the

bank’s balance for the client?

A) deposits in transit

B) Checks are written by the client in the same month the checks clear the bank.

C) other reconciling items

D) outstanding checks

Which of the following statements about Generally Accepted Audit Standards are true?

I. They serve as broad guidelines to auditors for conducting an audit engagement.

II. They are sufficiently specific to provide any meaningful guide to practitioners.

III. They represent a framework upon which the AICPA can provide interpretations.

A) I and II

B) I and III

C) II and III

D) I, II and III

Most tests of accounts receivable are based on what schedule, file, or listing?

A) sales master file

B) aged accounts receivable trial balance

C) accounts receivable master file

D) accounts receivable general ledger account

Which of the following is not a standard contained in both the Attestation Standards

and Generally Accepted Auditing Standards?

A) The examination is to be performed by a person having adequate technical training.

B) An independence in mental attitude is to be maintained.

C) Sufficient evidence is to be obtained.

D) The practitioner must obtain a sufficient understanding of the client’s internal

control.

Auditors are ________ to document the known and likely misstatements in the financial

statements under audit.

A) permitted

B) required

C) not allowed

D) strongly encouraged

Statements on Internal Auditing Standards are issued by the

A) AICPA.

B) SEC.

C) Internal Auditing Standards Board.

D) Auditing Standards Boards.

If the auditor concludes that physical controls over inventory are so inadequate that the

inventory will be difficult to count, the auditor should ordinarily

A) withdraw from the engagement.

B) issue a qualified audit report.

C) conduct expanded observation tests of physical inventory.

D) hire a specialist to assist the auditor.

Which of the following would the auditor expect to find in the client’s management

representation letter?

A) management’s recommendations for internal control effectiveness improvements

B) management’s plans for improving product quality

C) management’s compliance with contractual arrangements that impact the financial

statements

D) management’s goals for improving earnings per share

If an auditor wishes to rely on the work of internal auditors (IA), the auditor must

obtain satisfactory evidence related to the IA’s competence, integrity, and objectivity.

If an auditor concludes that internal controls are likely to be effective, the preliminary

assessment of control risk can be reduced, leading to which of the following impacts on

the acceptable risk of incorrect acceptance?

A) The acceptable risk of incorrect acceptance will be reduced.

B) The acceptable risk of incorrect acceptance will be increased.

C) The acceptable risk of incorrect acceptance will be eliminated.

D) The acceptable risk of incorrect acceptance will not be impacted.

If the auditor finds extensive control test deviations and significant misstatements while

performing substantive tests of transactions and substantive analytical procedures,

A) the cost of the audit should decrease.

B) the auditor will conclude that internal controls are effective.

C) extensive tests of details of balances will need to be performed.

D) all of the above

Which of the following is not a correct statement regarding fraudulent hours?

A) Fraudulent hours occur when an employee reports more time than was actually

worked.

B) It is difficult for an auditor to discover fraudulent hours.

C) It is ordinarily easier for the client to prevent fraudulent hours by adequate internal

controls than for the auditor to detect it.

D) To detect fraudulent hours, the auditor should examine the cancelled checks written

to the employees.

Management implements internal controls to ensure that all required footnote

disclosures are accurate. Auditors tests those controls to provide evidence supporting

the ________ presentation.

A) completeness and valuation

B) completeness and accuracy

C) rights and obligations and existence

D) occurrence and accuracy

As a CPA, you have been engaged to perform an attestation engagement. You would

typically

A) express a conclusion about an assertion.

B) provide management consulting services.

C) prepare financial forecasts to secure in preparation for receiving debt funding.

D) compile financial statements for the client.

The risk the auditor is willing to take of accepting a balance as correct when the true

misstatement in the balance under audit is greater than the tolerable misstatement is

A) the upper bound.

B) the tolerable risk.

C) the acceptable risk of incorrect acceptance.

D) the lower bound.

The auditor is concerned that a client is failing to bill customers for shipments. An audit

procedure that would gather relevant evidence would be to

A) select a sample of duplicate sales invoices and trace each to related shipping

documents.

B) trace a sample of shipping documents to related duplicate sales invoices.

C) trace a sample of Sales Journal entries to the Accounts Receivable subsidiary ledger.

D) compare the total of the Schedule of Accounts Receivable with the balance of the

Accounts Receivable account in the general ledger.

Prices in an active market for identical assets is a level ________ fair value estimate.

A) 1

B) 2

C) 3

D) 4

When dealing with fraudulent financial reporting risk for accounts payable,

A) companies will generally tend to overstate accounts payable.

B) it is difficult for the auditor to verify if all liabilities have been recorded if

prenumbered receiving reports are used.

C) companies have used fictitious reductions to accounts payable to overstate net

income.

D) accounts payable is rarely a significant risk area for fraudulent financial reporting.

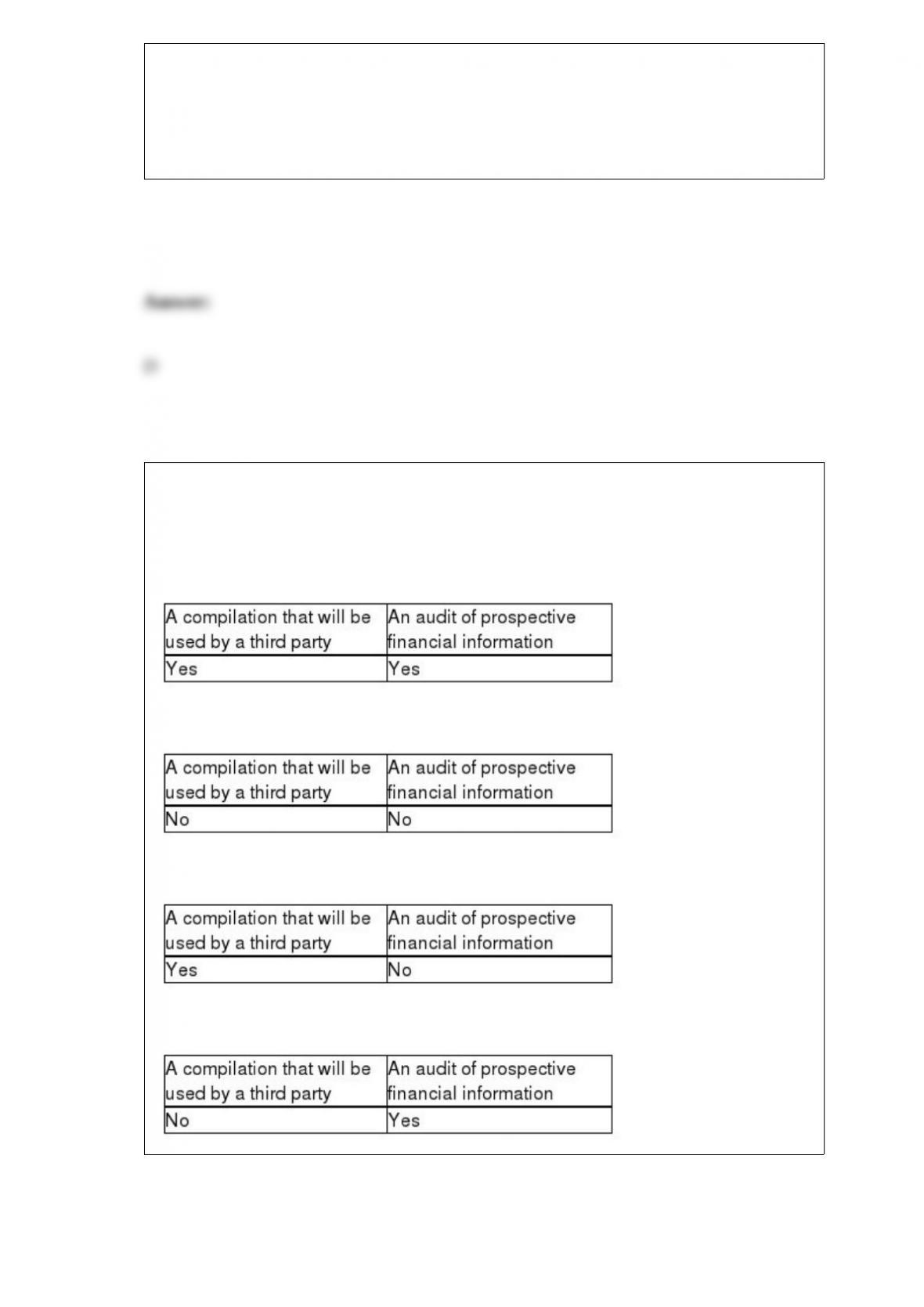

Which of the following statements is not correct?

A) Forecasts can be provided for general use.

B) Forecasts can be provided for limited use.

C) Projections can be provided for general use.

D) Projections can be provided for limited use.

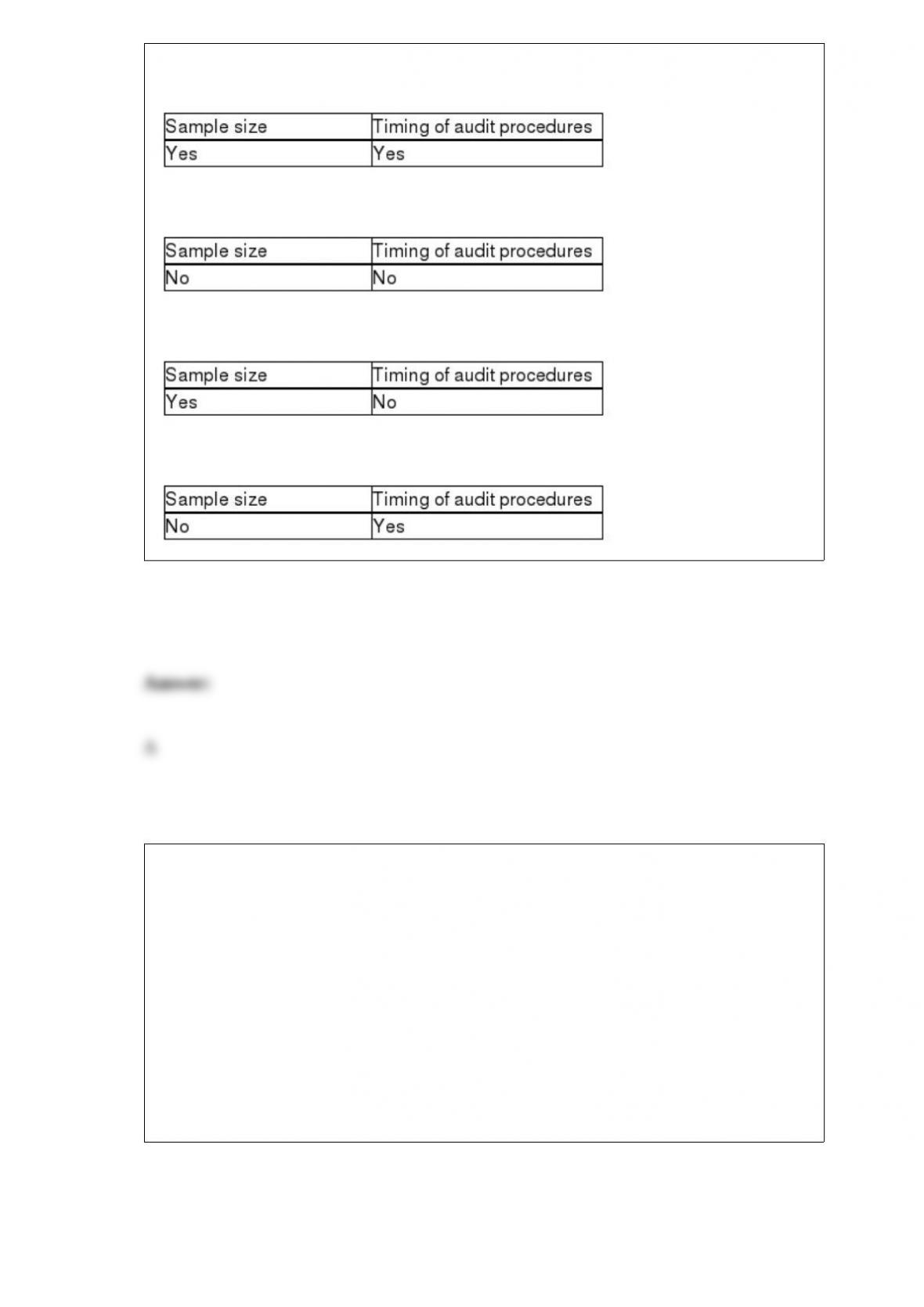

Auditors must make decisions regarding what evidence to gather and how much to

accumulate. Which of the following is a decision that must be made by auditors related

to evidence?

A)

B)

C)

D)

A major purpose of federal securities regulations is to

A) provide sufficient reliable information to the investing public who purchase

securities in the marketplace.

B) establish the qualifications for accountants who are members of the profession.

C) eliminate incompetent attorneys and accountants who participate in the registration

of securities to be offered to the public.

D) provide a set of uniform standards and tests for accountants, attorneys, and others

who practice before the Securities and Exchange Commission.

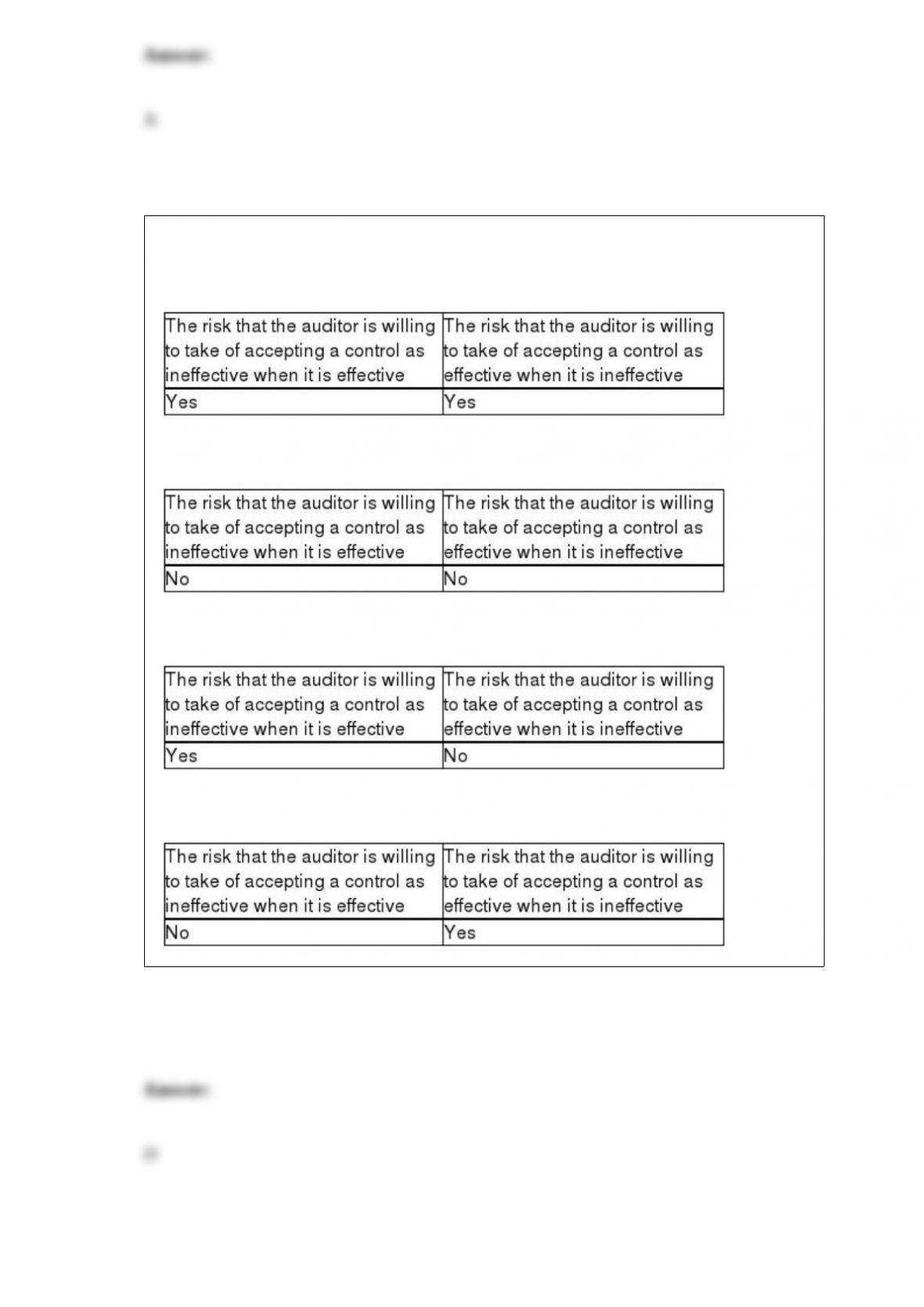

A danger in setting the acceptable risk of overreliance too low is

A)

B)

C)

D)

The predecessor auditor is required to respond to the request of the successor auditor

for information, but the response can be limited to stating that no information will be

provided when

A) the predecessor auditor has poor relations with the successor auditor.

B) the client is dissatisfied with the predecessor’s work.

C) there are actual or potential legal problems between the client and the predecessor.

D) the predecessor believes that the client lacks integrity.

A document review of which of the following is most likely to yield evidence of any

unrecorded liabilities?

A) debit memos

B) vendor memos

C) unpaid accounts payable

D) sales invoices out of sequence

It is generally possible for small companies to have all of the following except for

A) adequate documents and records.

B) physical controls over assets.

C) competent, trustworthy personnel.

D) internal auditors.

A member in public practice shall neither receive from, nor pay to, a client a

commission when the member or member’s firm also performs certain services for that

client. Are commissions allowed if the CPA performs

A)

B)

C)

D)

Which of the following is not a problem with monetary unit selection?

A) population items with a zero recorded balance

B) population items that should have a zero balance but do not

C) accounts with negative balances

D) accounts with small recorded balances that are significantly understated

Subsequent to the close of Spacely Sprockets fiscal year ending October 31, 2016, a

major debtor has declared bankruptcy due to a series of events. The receivable is

significantly material in relation to the financial statements, and recovery is doubtful.

The debtor had confirmed the full amount due to Spacely Sprocket at the balance sheet

date. Because the account was confirmed at the balance sheet date, Spacely refuses to

disclose any information in relation to this subsequent event. The CPA believes that all

other accounts were stated fairly at the balance sheet date. In addition, Spacely changed

their method of inventory valuation from FIFO to LIFO. This change was disclosed in

Note X to the financial statements. Accordingly, what type of opinion should be

expressed?

A) unqualified with an explanatory paragraph

B) qualified due to a GAAP departure

C) qualified due to a scope limitation

D) a combination of B and C

Due to a shortage of personnel, the client asks a member firm to assist with the

authorization of accounting transactions. This is an example of which type of threat to

compliance with the rules under the AICPA Code of Professional Conduct?

A) management participation

B) self-interest

C) self-review

D) undue influence

When the auditor is attempting to determine the extent to which external users rely on a

client’s financial statements, they may consider several factors except for

A) client size.

B) concentration of ownership.

C) nature and amounts of liabilities.

D) assessment of detection risk.

A useful starting point for becoming familiar with the client’s inventory is for the

auditor to

A) read the AICPA’s Industry Audit Guide.

B) review accounting theory covering special inventory problems.

C) read the client’s accounting manual.

D) tour the client’s facility.

When considering the risk of misstatement due to fraud,

A) the risk of not detecting a material misstatement due to fraud is lower than the risk

of not detecting a misstatement due to error.

B) the risk is only made at the financial statement level.

C) auditing standards require the auditor to presume that risk of fraud exist in expense

transactions.

D) auditing standards outline procedures the auditor should perform to obtain

information from management about their consideration of fraud.

Which of the following is a correct statement regarding analytical procedures?

A) A major strength in using industry ratios for auditing is the difference between the

nature of the client’s financial information and that of the firms making up the industry

totals.

B) Common-size financial statements display all items as a percentage change from a

base year.

C) In identifying areas of specific risk, the auditor is likely to focus on the liquidity

activity ratios.

D) In order to look for a misstatement in the allowance for bad debts, the auditor should

divide gross sales by sales returns and allowances.

The process which requires the calculation of an interval and then selects the items

based on the size of the interval is

A) statistical sampling.

B) random sample selection.

C) systematic sample selection.

D) computerized sample selection.