Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

20-1

Chapter 20

Audit of the Payroll and

Personnel Cycle

Concept Checks

P. 666

1. Transactions for the payroll and personnel cycle are generally far more

represent amounts associated with the last pay period, while payroll related

2. The human resources department provides an independent source for the

hiring and firing of personnel and the verification of wage information,

including changes in wages and deductions. The primary role of the

P. 675

are:

1. Examine time card for indication of approval to ensure that payroll

performed by existing employees (occurrence).

2. Account for a sequence of payroll checks to ensure existing payroll

payments are recorded. The purpose of this test is to determine

payroll transactions are properly classified. (Classification)

5. Observe when recording takes place to ensure that payroll

transactions are recorded on a timely basis. (Timing)

20-2

Concept Check, P. 675 (continued)

2. An auditor should perform audit tests primarily designed to uncover fraud in

the payroll and personnel cycle when he or she has determined that internal

Review Questions

Cash Direct labor

Inventory Salary expense

Construction in progress Commission expense

overstated. Similarly, if the indirect labor cost of individual employees is charged

to specific jobs or processes, the valuation of inventory is affected if labor is

year and indicates his or her gross pay, income taxes withheld, and FICA

withheld for the year. In serving as a summary of the employee’s earnings

record, the W-2 form conveniently provides information necessary for the

employee to fill out his or her income tax returns.

compensation taxes.

20-3

Copyright © 2017 Pearson Education, Inc.

20-4 An imprest payroll account is a separate payroll bank account in which

a constant balance, either zero or small, is maintained. When a payroll is paid,

the exact amount of the net payroll is transferred by check or electronic funds

transfer from the general account to the imprest account. The purpose and

advantage of an imprest payroll account is that it limits the company’s exposure

to payroll fraud by limiting the amount that may be misappropriated.

20-5 Where the primary objective is to detect fraud, the auditor will examine

the following supporting documents and records:

1. Cancelled payroll checks for employee name, authorized signature,

recurring second endorsements.

2. Payroll journal or listing, tracing transactions to the personnel files

the payroll period.

3. Payroll journal or listing and individual payroll records, selecting

terminated employees to determine whether each terminated

subsequent payroll period.

signs for his or her check.

5. Time cards, testing them for reasonableness or observing whether

they are being punched by the proper employees.

20-6 The auditor should be concerned with whether the human resources

department is following the proper hiring and termination procedures. An

obvious reason for this would be to ensure that there are adequate safeguards

against hiring and retaining incompetent and untrustworthy people. The

ramifications of hiring such people can range from simple inefficiency and

waste to outright fraud or theft. More importantly, though, it is necessary for the

20-7 To trace a random sample of prenumbered time cards to the related

payroll payments in the payroll register and compare the hours worked to the

hours paid is to test if payroll payments have been recorded (completeness)

and if those employees who worked are being paid for their time actually

20-4

20-7 (continued)

(occurrence). This test, in effect, attempts to discover nonexistent employees or

20-8 The percentage of total audit time in the cycle devoted to performing

tests of controls and substantive tests of transactions is usually far greater in

the payroll and personnel cycle than for the sales and collection cycle because

year-end balances in payroll-related accounts are often immaterial. Also, there

consuming tasks.

20-9 Audit procedures that are primarily for the detection of fraud in the payroll

and personnel cycle include:

1. Examine cancelled payroll checks for employee name, authorized

employees were actually employed during the period.

3. Select several terminated employees from payroll records to

determine whether each former employee received his or her

termination pay in accordance with company policy and to determine

that the employee’s pay was discontinued on the date of termination.

result, which will necessitate extensive investigation.

20-10 The auditor can use audit software for tests of controls in the payroll

cycle by accounting for the numerical sequence of payroll checks or other

documents, testing for proper approval of time records if the client uses an

general ledger, or summarize payroll by job or by category.

20-5

Copyright © 2017 Pearson Education, Inc.

20-11 Types of authorizations in the payroll and personnel cycle are:

1. Deduction authorization, without which the wrong amount (or no

deduction) may be deducted from the employee’s paycheck.

2. Rate authorizations, without which the employee may be getting

paid at the wrong rate.

3. Time card authorization, without which the employee may be getting

paid for the wrong quantity of hours worked.

4. Payroll check authorization, without which unauthorized funds may

be paid out.

6. Authorization to hire a new employee, without which nonexistent

or unqualified personnel may be added to the payroll.

following objectives:

1. Time card hours agree with payroll computations.

2. Overtime hours are approved.

3. Foreman approves all time cards.

5. Gross pay calculation is verified.

6. Exemptions taken agree with W-4.

7. Income tax, other deductions, and net pay calculations are verified.

8. Authorizations are available for voluntary withholdings and

miscellaneous deductions.

9. Paycheck endorsement is same as signature on W-4 form.

The frequency of control deviations or monetary errors must be estimated

prior to performing the tests. This estimate together with the acceptable risk of

overreliance (ARO) and the tolerable exception rate will enable the auditor to

20-13 In auditing payroll withholding and payroll tax expense, the emphasis

should normally be on evaluating the adequacy of the payroll tax return preparation

procedures rather than the payroll tax liability, because a major reason for

misstatements in the liability account is incorrect preparation of the returns in

20-6

20-14 Several analytical procedures for the payroll and personnel cycle and

misstatements that might be indicated by significant fluctuations are as follows:

SUBSTANTIVE ANALYTICAL

PROCEDURE

MISSTATEMENT TYPES

1. Comparison of payroll expense

accounts to amounts in prior years.

Cutoff misstatements or improper

amounts recorded in a period.

2. Direct labor divided by sales compared

to industry standards in prior years.

Cutoff misstatements or amounts

charged to improper payroll

accounts.

3. Commission expense divided by sales

compared to industry standards, prior

years, or sales agreements.

Failure to record commission on

sales, or recording the improper

commission amount.

4. Payroll tax expense divided by salaries

and wages compared to prior year

balances adjusted for changes in the

tax rate and not including officers’

salaries.

Failure to record payroll taxes or

recording of the improper amount.

5. Comparison of accrued payroll and

payroll tax accounts to prior years.

Failure to record payroll accruals or

recording improper amounts at the

end of a period.

6. The percentage of labor included in

work in process and finished goods

inventories compared to prior years.

Use of improper labor standards, or

classification misstatements.

7. Analysis of direct labor variances.

Use of improper labor standards, or

classification misstatements.

20-15 It is common to verify total officers’ compensation even when the tests

of controls and substantive tests of transactions results in payroll are excellent

because the salaries and bonuses of officers must be included in filings with the

SEC and IRS (e.g., the Form 10-K Report, proxy, and the federal income tax

Multiple Choice Questions From CPA Examinations

20-16 a. (2) b. (2) c. (3)

20-17 a. (4) b. (4) c. (4)

Multiple Choice Questions From Becker CPA Exam Review

20-18 a. (1) b. (3) c. (3)

Discussion Questions and Problems

20-19

a.

TRANSACTION-

RELATED AUDIT

OBJECTIVE

b.

TEST OF

CONTROL

c.

POTENTIAL

MISSTATEMENT

d.

SUBSTANTIVE

AUDIT

PROCEDURE

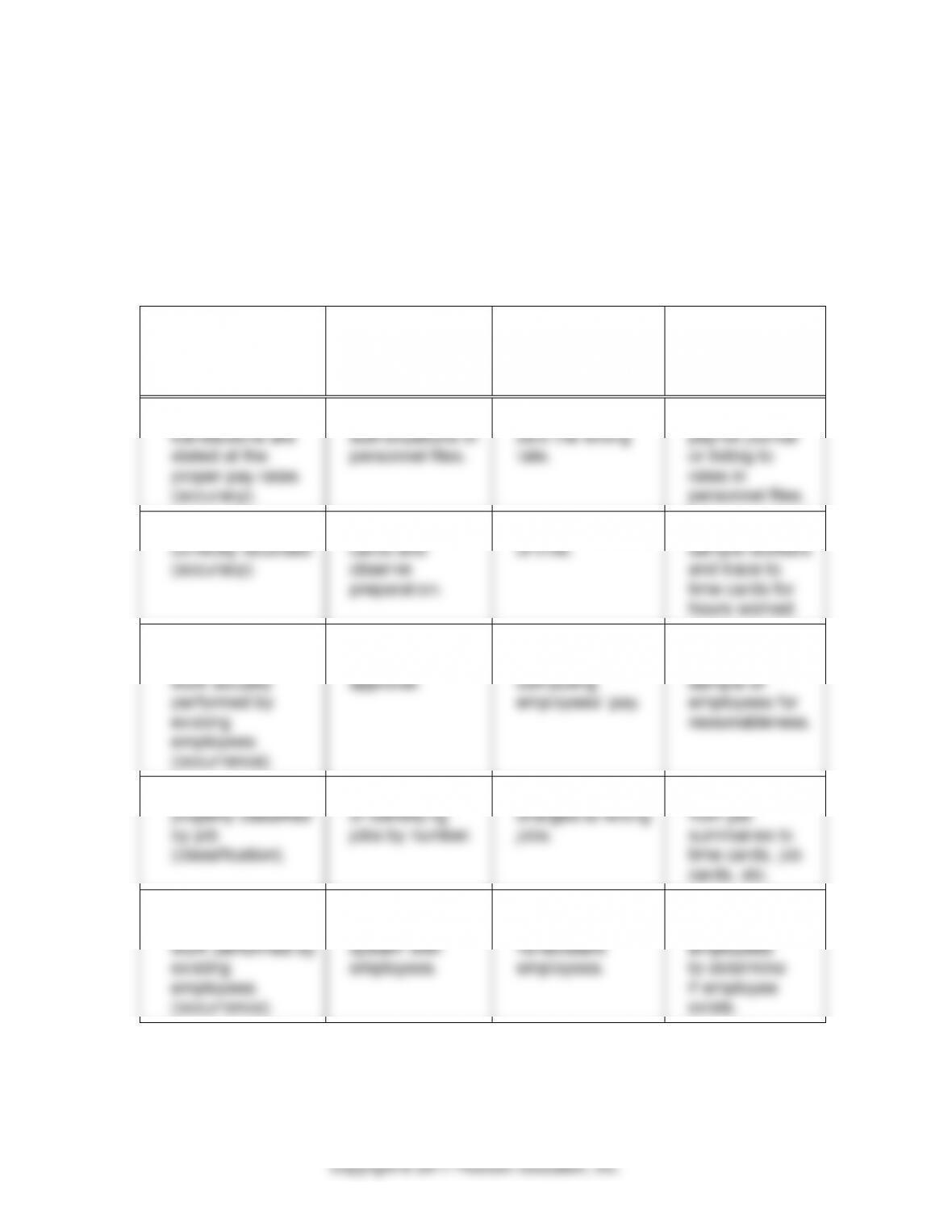

1. Recorded payroll

transactions are

stated at the

proper pay rates

(accuracy).

Examine

authorizations in

personnel files.

Employees are

paid the wrong

rate.

Compare rates in

payroll journal

or listing to

rates in

personnel files.

2. Hours worked are

correctly recorded

(accuracy).

Examine time

cards and

observe

preparation.

Incorrect recording

of time.

Randomly

sample workers

and trace to

time cards for

hours worked.

3. Recorded payroll

payments are for

work actually

performed by

existing

employees

(occurrence).

Examine time

cards for

approval.

Incorrect times are

used in

computing

employees’ pay.

Analyze payroll

records of a

sample of

employees for

reasonableness.

4. Time records are

properly classified

by job

(classification).

Examine system

of identifying

jobs by number.

Direct labor is

charged to wrong

jobs.

Trace entries

from job

summaries to

time cards, job

cards, etc.

5. Recorded payroll

checks are for

work performed by

existing

employees

(occurrence).

Observe and

discuss payroll

system with

employees.

Payroll payments

are made to

nonexistent

employees.

Trace payroll

payments to

employees

to determine

if employee

exists.

20-8

20-19 (continued)

a.

TRANSACTION-

RELATED AUDIT

OBJECTIVE

b.

TEST OF

CONTROL

c.

POTENTIAL

MISSTATEMENT

d.

SUBSTANTIVE

AUDIT

PROCEDURE

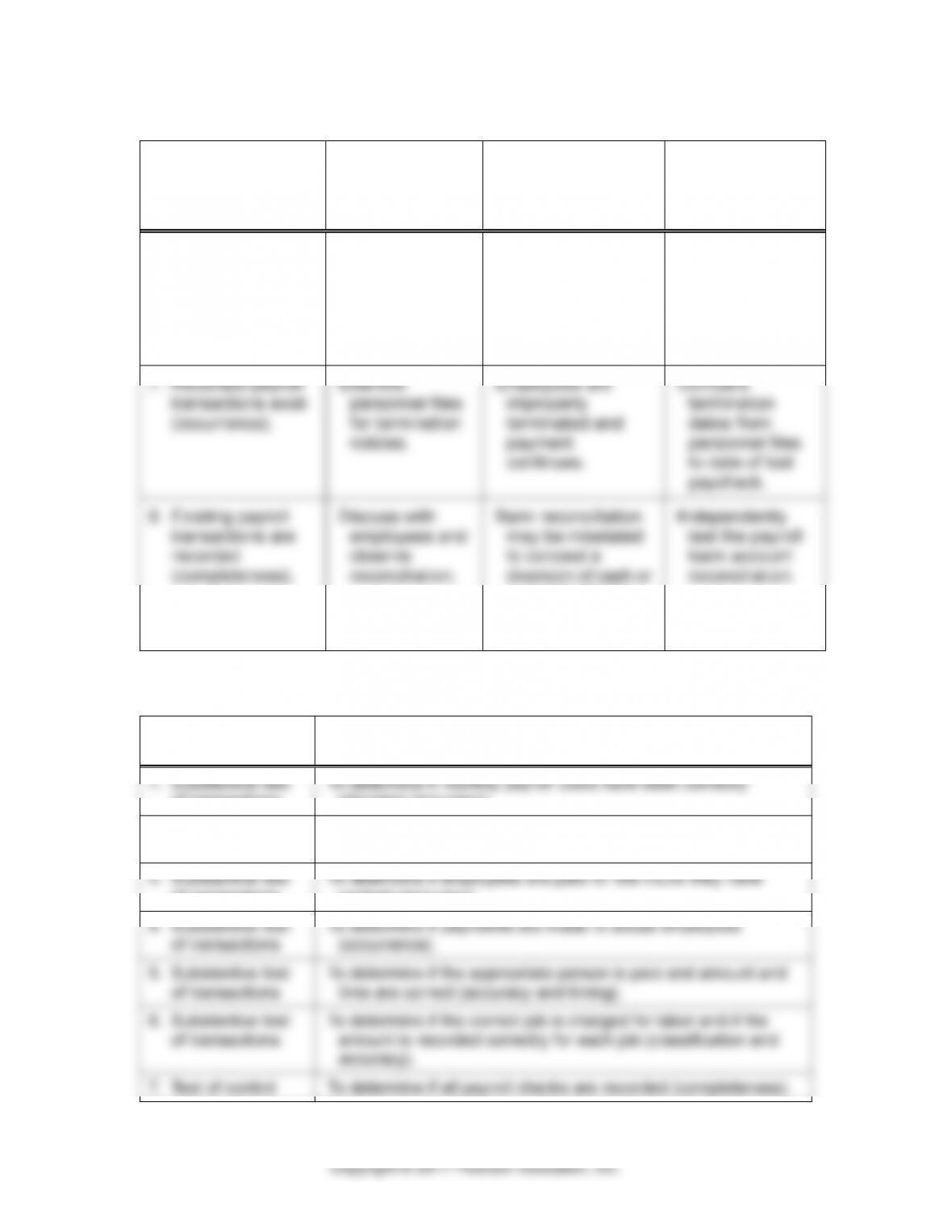

6. Payments are

made to actual

employees

(occurrence).

Observe

payments and

discuss with

employees.

Payments are made

to wrong

employees.

Examine

cancelled

checks for

endorsement,

and compare to

personnel file.

7. Recorded payroll

transactions exist

(occurrence).

Examine

personnel files

for termination

notices.

Employees are

improperly

terminated and

payment

continues.

Compare

termination

dates from

personnel files

to date of last

paycheck.

8. Existing payroll

transactions are

recorded

(completeness).

Discuss with

employees and

observe

reconciliation.

Bank reconciliation

may be misstated

to conceal a

diversion of cash or

a misclassification

of payroll

transactions.

Independently

test the payroll

bank account

reconciliation.

20-20

a.

TYPE OF TEST

b.

TRANSACTION-RELATED AUDIT OBJECTIVE(S)

1. Substantive test

of transactions

To determine if monthly payroll costs have been correctly

allocated (accuracy).

2. Test of control

To determine if recorded payroll transactions are for work

actually performed by existing employees (occurrence).

3. Substantive test

of transactions

To determine if employees are paid for the hours they have

worked (accuracy).

4. Substantive test

of transactions

To determine if payments are made to actual employees

(occurrence).

5. Substantive test

of transactions

To determine if the appropriate person is paid and amount and

time are correct (accuracy and timing).

6. Substantive test

of transactions

To determine if the correct job is charged for labor and if the

amount is recorded correctly for each job (classification and

accuracy).

7. Test of control

To determine if all payroll checks are recorded (completeness).

20-9

20-21

a.

RECOMMENDED CONTROL

b.

SUBSTANTIVE AUDIT PROCEDURE

1. Approval of time cards by foreman and

observation of use of time clock by the

foreman.

Observe employees punching in—only

one card per employee—to see whether

any employee punches two cards

(normally not an effective or practical

audit procedure).

2. Paychecks distributed by someone

other than the foreman.

Perform payroll payoff, requiring identification

from all employees prior to payment.

3. Pay employees only for time charged

to jobs. Reconcile payroll expense to

amounts charged to jobs.

Compare total hours worked from payroll

journal or listing to total hours worked as

recorded on job cost tickets.

4. Internal verification of classification.

Trace labor distribution to supporting job

input forms.

5. Payroll checks not returned to payroll

clerk after signing.

Perform payoff as described in 2 above.

6. Internal verification of calculations and

amounts.

Recompute federal withholding taxes and

trace to employee earnings record.

7. Payroll checks are prenumbered and

accounted for. Use an imprest bank

account where the amount to be

deposited is taken from the payroll

journal or listing.

Reconcile the disbursements in the payroll

journal or listing to the disbursements on

the payroll bank statement.

20-10

20-22

a.

TYPE OF TEST

b.

TRANSACTION-RELATED

AUDIT OBJECTIVE(S)

c.

BALANCE-

RELATED AUDIT

OBJECTIVE(S)

1.

(4) TDB

N/A

Detail tie-in

2.

(4) TDB

N/A

Completeness

3.

(3) Substantive

analytical procedure

N/A

N/A

4.

(1) Test of control;

(2) STOT

Occurrence and accuracy

N/A

5.

(1) Test of control

Accuracy

N/A

6.

(1) Test of control

Accuracy

N/A

7.

(1) Test of control

Completeness

N/A

8.

(4) TDB

N/A

Accuracy

9.

(3) Substantive

analytical procedure

N/A

N/A

10.

(2) STOT

Occurrence, timing, and accuracy

N/A

PROCEDURE

PERFORMED

a.

ADDITIONAL PROCEDURES

b.

AUDIT OBJECTIVE

1.

Consider changes in client circumstances

that might suggest fluctuations in accrual

balances, such as increase in number of

employees.

Completeness

2.

Examine payroll tax form filed in subsequent

period to verify amount of payroll tax accrual.

Accuracy,

completeness

3.

Compare the bonus formula with prior years.

For a sample of salespersons, recompute

the accrued bonus based on the formula as

stated in the contract.

Trace amount of accrual to cash

disbursements in subsequent period.

Completeness

Accuracy

Accuracy,

completeness

4.

Review company policy for computing and

recording vacation pay accrual.

For a sample of employees, recompute

accrued vacation pay based on company

policy.

Accuracy

Accuracy