Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

15-20

15-34 (continued)

INVOICE

NUMBER

EXCEPTION ANALYSIS

6810

Confirm the account balances to the customers; examine the

reduction in the perpetual inventory records.

7625

Trace the amount to the sales journal and accounts receivable

master file; examine the shipping document and recompute

the sale amount.

8431

Determine who recorded the invoice and check several others

prepared by him or her to determine if the problem consistently

occurs.

8528

Examine the accounts receivable master file for subsequent

cash receipt; examine sales invoices for other invoices to the

same customer to determine if customer orders were attached.

8566

Check the price on other invoices to the same customer. Check

the price on other invoices that have the same product.

8780

See 7625

9169

Check credit history of customer and evaluate collectibility of the

customer’s account.

9974

Recheck actual price, extensions, and postings; determine who

the clerk was and check several other invoices for proper

indication of performance.

15-35 a.

ATTRIBUTE

MISSING ELEMENT

1

CUER is 9.2%

2

Initial sample size is 77

3

Tolerable exception rate is 7%

4

The actual number of exceptions in the sample was 1

5

ARO is 5%

6

Sample size is 70

c. Attribute 1 has a lower ARO, which normally would lead to a large

sample size. TER-EPER is 6% for both attribute 1 and attribute 3.

15-21

15-35 (continued)

for attribute 1.

d. The CUER is smaller for attribute 2 relative to attribute 5 because

Case

15-36 a. Audit sampling could be conveniently used for procedures 3 and 4

b. The most appropriate sampling unit for conducting most of the

audit sampling tests is the shipping document because most of

the tests are related to procedure 4. Following the instructions of

the audit program, however, the auditor would use sales journal

c. Note: The sampling data sheet that follows assumes an attributes

sampling approach. The only difference between the sampling

data sheet for attributes sampling and for nonstatistical sampling

sampling.

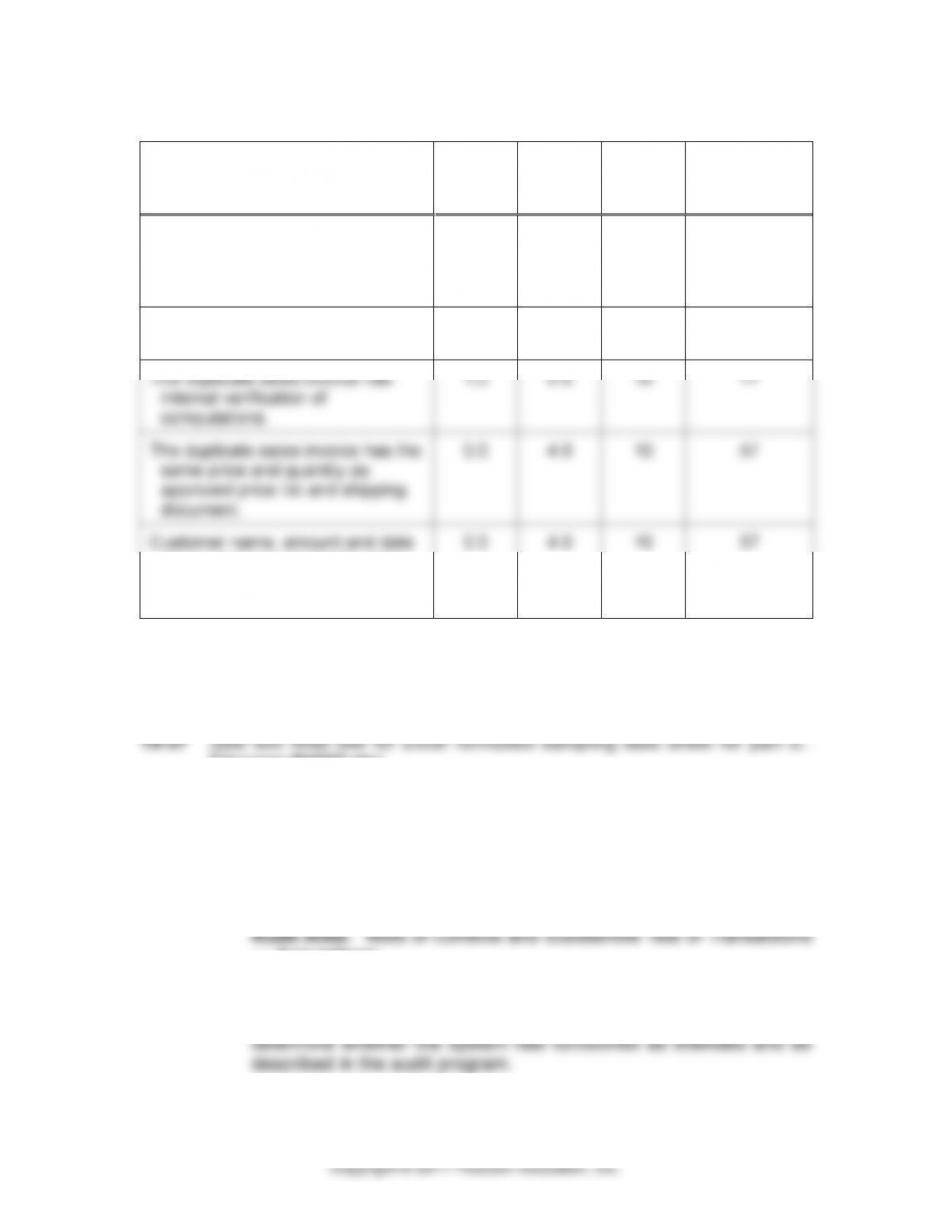

DESCRIPTION

OF ATTRIBUTES

EPER

TER

ARO

INITIAL

SAMPLE

SIZE*

A duplicate sales invoice exists for

the shipping document selected.

1.0

5.0

10

77

Shipping document agrees with

related duplicate sales invoice.

0.0

4.0

10

57

15-22

15-36 (continued)

DESCRIPTION

OF ATTRIBUTES

EPER

TER

ARO

INITIAL

SAMPLE

SIZE*

The duplicate sales invoice has

attached a copy of the shipping

document, shipping order, and

customer order.

1.0

5.0

10

77

The shipping order has proper

credit approval.

1.0

5.0

10

77

The duplicate sales invoice has

internal verification of

computations.

1.0

5.0

10

77

The duplicate sales invoice has the

same price and quantity as

approved price list and shipping

document.

0.0

4.0

10

57

Customer name, amount and date

agrees between duplicate sales

invoice and sales journal and

subsidiary ledger.

0.0

4.0

10

57

* assumes the shipping document is the sampling unit.

■ Integrated Case Application

Filename P1537.xls)

a.

and

d. PINNACLE MANUFACTURING―PART VI

Client: Pinnacle Manufacturing

― Acquisitions.

Define the Objective(s): Examine vendors’ invoices, receiving

reports, purchase orders, and other related documents to

15-37 (continued)

Vouchers from 1/1/2016 to 10/31/2016. First voucher number –

6734. Last voucher number – 33722.

Define the sampling unit, organization of population items,

and random selection procedures: Voucher number, recorded

electronic spreadsheet.

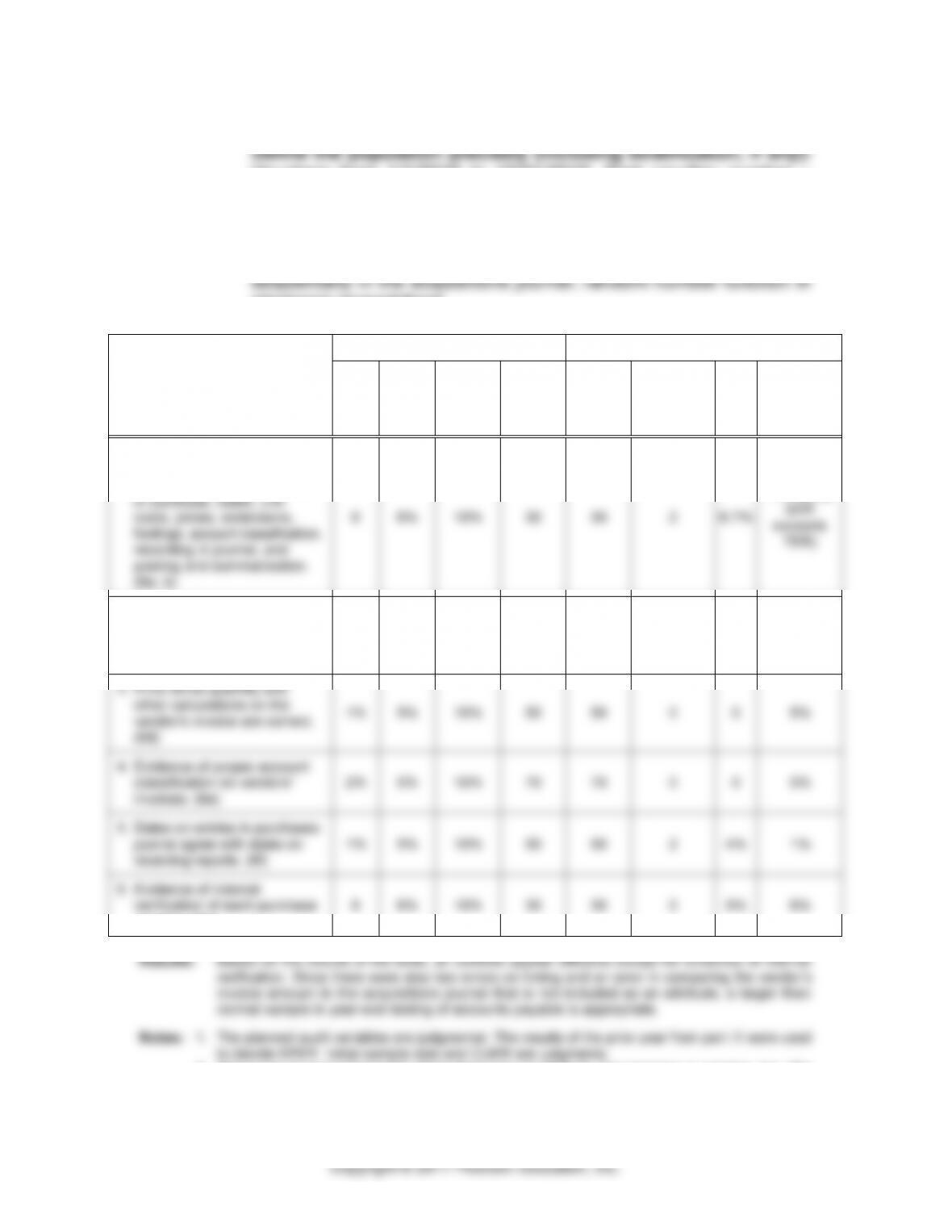

Description of Attributes

Planned Audit

Actual Results

EPER

TER

ARO

Initial

Sample

Size

Sample

Size

Number

of

Exceptions

SER

Calculated

Sampling

Error

(TER-SER)

1. Evidence of internal

verification of voucher

package including propriety

of purchase, dates, unit

costs, prices, extensions,

footings, account classification,

recording in journal, and

posting and summarization.

(6a, b)

0

6%

10%

30

30

2

6.7%

-.7% (note

SER

exceeds

TER)

2. Prices on vendors’ invoices

conform to approved price

limits established by

management. (6c)

0

5%

10%

40

40

0

0

5%

3. Price times quantity and

other calculations on the

vendor’s invoice are correct.

(6d)

1%

5%

10%

50

50

0

0

5%

4. Evidence of proper account

classification on vendors’

invoices. (6e)

2%

5%

10%

70

70

0

0

5%

5. Dates on entries in purchases

journal agree with dates on

receiving reports. (6f)

1%

5%

10%

50

50

2

4%

1%

6. Evidence of internal

verification of each purchase

voucher. (6g)

0

6%

10%

30

30

0

0%

6%

2. There was an error discovered where there was no attribute. This happens in practice, too. The

auditor should not ignore the exception even though it is an unplanned discovery.

15-37 (continued)

b. Client: Pinnacle Manufacturing

― Cash Disbursements

Define the Objective(s): Examine cancelled checks and other

– 12376. Last check number – 37318.

Define the sampling unit, organization of population items,

and random selection procedures: Check number, recorded

Description

of Attributes

Planned Audit

Actual Results

EPER

TER

ARO

Initial

Sample

Size

Sample

Size

Number

of

Exceptions

SER

Calculated

Sampling

Error

(TER-SER)

1. Payee, name,

amount, and date

on cancelled

check agrees with

related purchases

journal and cash

disbursements

entry. (9a)

0

5%

10%

40

2. Evidence of

signature, proper

endorsement and

cancellation of

each check. (9b)

0

5%

10%

40

3. Date on cancelled

check agrees with

bank cancellation

date. (9c)

2

5%

10%

70

4. Cash discounts

are correct. (9d)

0

5%

10%

40

15-25

15-37 (continued)

c. Population = voucher numbers 6734 to 33722

Sample size = 50

Random Selection:

=RANDBETWEEN(6734, 33722)

The command for selecting the random number can be entered

directly onto the spreadsheet, or can be selected from the function

menu (math & trig) functions under the “insert” menu. It may

solution.

15-38 ACL Problem

the bottom of the screen.

b. The sample size is 39 and the sampling interval is 104 (rounded

down from 104.66).

the sample size decreases to 29.

(Note: answers to part b. and c. are similar to answers obtained

15-26

15-38 (continued)

Invoice Number

Sales Order Number

Customer

Number

Invoice Date

Invoice

Amount

173640036997

000008176082

0252432

2/10/2014

29144.36

173640037166

000008176251

0258424

3/9/2014

11167.69

173640037196

000008176281

0261014

3/12/2014

3723.44

173640037226

000008176311

0260835

3/22/2014

21582.56

173640037472

000008176558

0263402

4/15/2014

5009.58

173640037506

000008176592

0255268

4/16/2014

11707.48

173640037545

000008176631

0255998

4/28/2014

19450.53

173640037782

000008176869

0257490

5/11/2014

23638.49

173640037800

000008176887

0257884

5/11/2014

4639.11

173640037808

000008176895

0235520

5/17/2014

1595.31

173640037891

000008176978

0260600

5/20/2014

945.32

173640037931

000008177018

0245068

5/21/2014

27755.91

173640037940

000008177027

0262176

5/26/2014

19244.99

173640038114

000008177201

0257847

6/1/2014

7401.07

173640038204

000008177291

0240643

6/16/2014

15132.12

173640038292

000008177379

0249233

6/16/2014

15728.09

173640038449

000008177536

0244063

6/29/2014

22261.59

173640038458

000008177545

0241913

6/24/2014

6188.54

173640038611

000008177698

0239939

6/29/2014

4170.89

173640038717

000008177804

0256692

7/13/2014

15043.24

173640038905

000008177992

0240304

7/8/2014

9413.12

173640039091

000008178178

0250396

7/22/2014

3210.42

173640039277

000008178364

0239614

7/30/2014

2745.13

173640039343

000008178430

0244488

8/10/2014

20998.44

173640039430

000008178517

0234834

8/20/2014

15128.39

173640039457

000008178544

0251543

8/20/2014

3238.49

173640039487

000008178574

0252534

8/10/2014

768.13

173640039502

000008178589

0244430

8/16/2014

7268.08

173640039589

000008178677

0253965

8/27/2014

1276.47

173640039617

000008178705

0260685

8/27/2014

17376.00

173640039969

000008179057

0244080

9/23/2014

2010.65

173640040032

000008179121

0242752

9/20/2014

13466.11

173640040150

000008179239

0260166

9/30/2014

15636.04

173640040214

000008179303

0248413

9/30/2014

1137.00

173640040565

000008179655

0256038

10/21/2014

1538.06

173640040583

000008179673

0247128

10/29/2014

16293.16

173640040585

000008179675

0263951

10/29/2014

19807.72

173640040697

000008179787

0237042

11/16/2014

2967.13

173640040739

000008179829

0250143

11/25/2014

5182.95

15-27

15-38 (continued)

e. The largest invoice amount included in the sample above is

$29,144.36 (invoice number 173640036997). Since record

sampling was used, the invoice amount is not considered.

limit of 6%