24–11

24–22 (continued)

d. The search for unknown commitments is typically performed as part

of individual audit areas. Three examples of procedures Johnson

is likely to perform for the purpose of uncovering commitments are:

As part of the audit of purchase transactions, be alert for

24–23 a. A contingent liability is a potential future obligation to an outside

party for an unknown amount resulting from activities that have

b. Audit procedures to learn about these items would be as follows:

The following procedures apply to all three items:

Discuss the existence and nature of possible contingent

liabilities with management and obtain appropriate

written representations.

Stock dividend

Confirm details of stock transactions with registrar

and transfer agent.

Review records for unusual journal entries subsequent

to year–end.

24–12

24–23 (continued)

Guarantee of interest payments

Discuss, specifically, any related party transactions

of representation.

Review financial statements of affiliate, and where

1. The lawsuit should be described in a footnote to the balance

sheet. In view of the court decision, retained earnings may

current liability will be set up as soon as a final decision is

rendered or if an agreement as to damages is reached. If

2. The declaration of such a dividend does not create a

necessary, but an indication of the action taken, and that

and common stock in the balance sheet.

3. If payment by Newart is uncertain, the $137,500 interest

liability for the period June 2 through December 1, 2016,

could be reflected in the Marco Corporation’s accounting

records by the following entry:

Interest Payments for Newart Company $137,500

Accrued Interest Payable — Newart Bonds $137,500

24–13

24–23 (continued)

the amount of $2,200,000.

If the interest has been paid by the time the audit is

completed, or if for other reasons it seems certain that the

payment will be made by Newart on January 15, no entry

should be made by Marco. In this circumstance a footnote

24–24 a. In this situation, Little need only send requests for letters to those

attorneys who are involved with legal matters directly affecting

the financial statements. The letters should be sent reasonably

near to the completion of the field work, but the follow–up on

b. The auditor would be required to follow up on the first attorney’s

letter by sending a second request or by calling the attorney to solicit

a response. The second letter would not require any additional

24–25

16. Most auditors would probably require that the account be

written off as uncollectible at 6–30–16, but they are not required to

b. 3 ― Amount should have been determined to be uncollectible

before end of field work, but it was discovered after the issuance of

24–14

24–25 (continued)

c. 4 ― The amount appeared collectible as of the date of the audit

report.

d. 1 ― The uncollectible amount was determined before end of field

work.

e. 1 ― The settlement should be reflected in the 6–30–16 financial

statement as an adjustment of current period income and not a

prior period adjustment.

24–26 a. Auditing standards require the auditor to evaluate whether there

is substantial doubt about a client’s ability to continue as a going

concern for at least one year beyond the balance sheet date.

Auditors make this evaluation during the planning phase, but also

b. The auditor is required to consider whether the client is able to

c. For the audit of MakingNewFriends.com, the relevant information

includes the fact that MakingNewFriends.com has had difficulty

establishing a loyal client base and generating advertising revenues.

This suggests the company may continue to have difficulty

generating revenues over the next 12 months. The recurring

24–15

24–26 (continued)

revenue or other financing for the coming year, knowledge of

d. The auditor is required to evaluate the feasibility of management

achieving their plans. For example, the auditor may discuss with

the bank the likelihood of the company obtaining financing. The

24–27 a. A typical additional information report includes the financial statements

associated with a short–form report on the basic financial

statements plus additional information likely to be useful to

b. The purpose of additional information reports is to provide

c. It would be appropriate to include all of the items as additional

information except the following:

2. The adequacy of insurance coverage. The auditor is not

an insurance professional, and any comments about the

3. Adequacy of the allowance for uncollectible accounts.

Comments that an account balance is correctly stated are

5. Material weaknesses in internal control. These should be

identified and communicated to management as a part of

24–16

24–27 (continued)

d. The following would be added to the standard audit report:

Our audit was made for the purpose of forming an opinion on

the basic financial statements taken as a whole. The accompanying

information on pages x through y is presented for purposes of

24–28 a. AU–C 450 identifies three types of misstatements:

no doubt.

2. Judgmental misstatements are differences arising from the

judgments of management concerning accounting estimates

inappropriate.

3. Projected misstatements are the auditor’s best estimate of

misstatements in populations, involving the projection of

misstatements identified in audit samples to the entire

Evidence that a misstatement is not an isolated occurrence

and other misstatements may exist include situations when the

b. AU–C 450 indicates the auditor should determine whether

the size and nature of the misstatements, both in relation

to particular classes of transactions, account balances, or

disclosures and the financial statements as a whole, and

24–17

24–28 (continued)

c. AU–C 450 requires the auditor to document the following:

the amount below which misstatements would be regarded

as clearly trivial;

all misstatements accumulated during the audit and

24–29 a.

POSSIBLE MISSTATEMENT ―

OVERSTATEMENT (UNDERSTATEMENT)

Item

Total

Amount

Current

Assets

Noncurrent

Assets

Current

Liabilities

Noncurrent

Liabilities

Income

Before Tax

1

$125,000

($125,000)

$125,000

2

85,000

(85,000)

60,000

(25,000)

3

44,000

(44,000)

(44,000)

4

52,000

52,000

52,000

5

43,000

0

6

Not known

0

0

(129,000)

112,000

(125,000)

0

108,000

net effect of adjustments to current assets and noncurrent assets

is less than materiality for total assets, the fact that a major

financial statement line item, such as current assets, is misstated

by more than materiality, indicates the adjustments would need to

assets and noncurrent liabilities.

24–18

24–30 a. Schwartz’s legal and professional responsibility in the issuance

b. Major considerations that will determine whether Schwartz is liable

in this situation are whether the client installed the system

according to Schwartz’s instructions or whether they deviated

from his instructions and whether they could have foreseen the

Case

24–31 a. See the “Summary of Possible Adjustments” on page 24–20 that

follows.

their records contain misstatements.

c. As indicated on the “Summary of Possible Adjustments” on page

24–20, you should attempt to have Aviary’s management record

required to determine the allowances for inventory obsolescence

and doubtful accounts and (2) it is not uncommon for auditors to

assist clients in adjusting these accounts. This may help minimize

management’s reluctance to admit making a mistake.

24–19

24–31 (continued)

the current year.

d. Your responsibility related to unadjusted misstatements that

management has determined are immaterial individually and in

the aggregate is to determine for yourself whether the combined

representation letter, along with management’s representation that

the uncorrected misstatements are immaterial.

e. Auditors of larger public companies must evaluate the noted

financial statements when issuing the audit report on internal

control. For example, if the possible adjustments identified by Aviary

Industries’ auditor are deemed to be material misstatements that

were not initially identified by the company’s internal controls, the

would include an adverse opinion if the auditor concludes that it

is a material weakness.

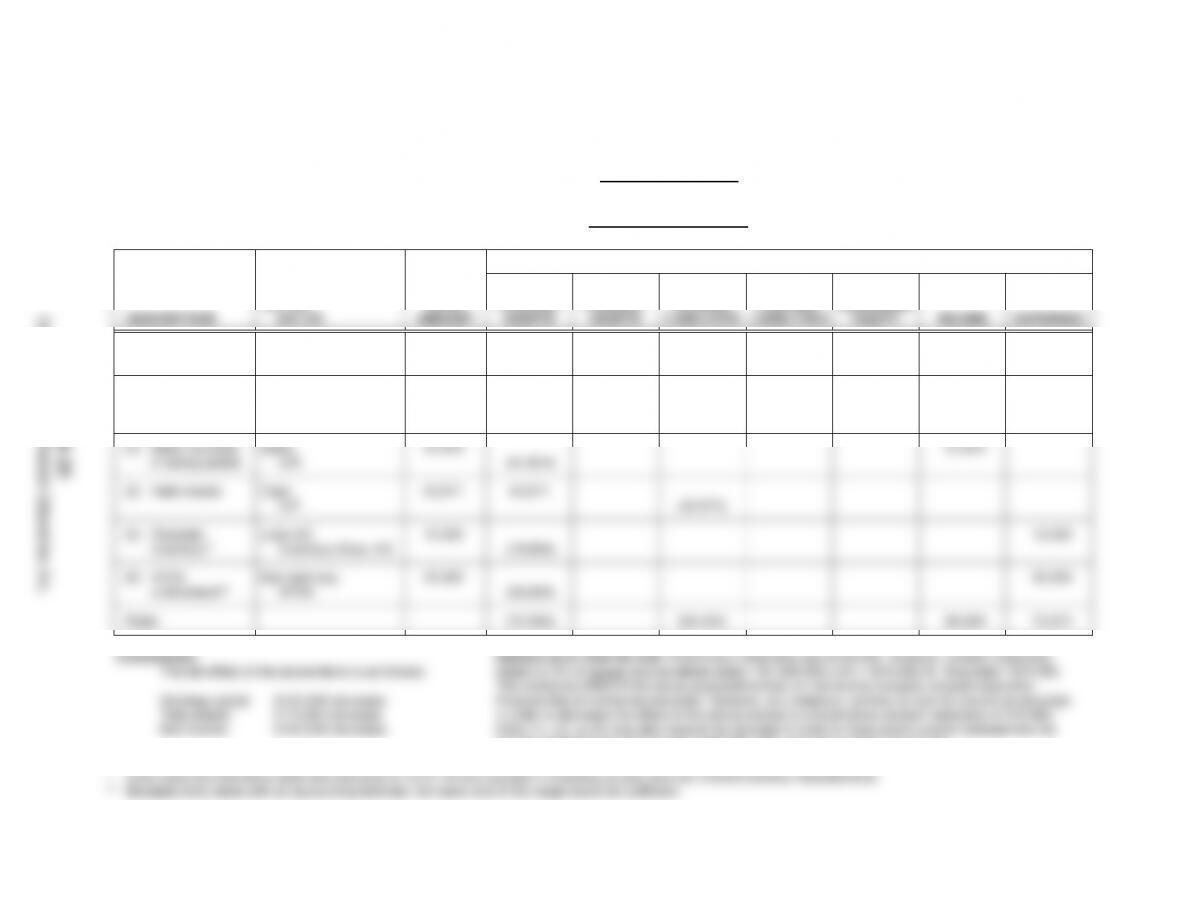

24–31 (continued)

a.

Client Name Aviary Industries

SUMMARY OF POSSIBLE ADJUSTMENTS

Year–ended December 31, 2016

A/C DR.

TOTAL

POSSIBLE ADJUSTMENTS – DR (CR)

CURRENT

NON–

CURRENT

CURRENT

NON–

CURRENT

BEGINNING

(1) Unrecorded

credit memos*

Sales R&A

A/R

26,451

(26,451)

26,451

(2) Unrecorded

inventory

purchases

Purchases

A/P

25,673

(25,673)

25,673

(3) Sales recorded

in wrong period

Sales

A/R

41,814

(41,814)

41,814

(4) Held checks

Cash

A/P

43,671

43,671

(43,671)

(5) Obsolete

inventory**

Loss A/C

Inventory Allow. A/C

15,000

(15,000)

15,000

(6) AFDA

understated**

Bad debt exp.

AFDA

35,000

(35,000)

35,000

Totals

(74,594)

(69,344)

68,265

75,673

Conclusions:

The net effect of the above items is as follows:

Working capital $143,938 decrease

Total assets: $ 74,594 decrease

Net income: $143,938 decrease

Opinion as to need for AJE: Preliminary materiality was $100,000. However, revised materiality

based on 5% of actual income before taxes = $1,508,929 x 5% = $75,446.45. Rounded = $75,000.

The combined effect of the above proposed entries on net income exceeds revised materiality.

Propose that all entries be recorded. However, at a minimum, entries (3) and (6) should be recorded

in order to decrease the effect of the above entries to a level below revised materiality of $75,000.

Entry (1), (2), or (5) may also have to be recorded in order to have some cushion between the net

income misstatement and revised materiality after recording entries (3) and (6).

24–20

Copyright © 2017 Pearson Education, Inc.