Current professional auditing standards require the performance of analytical

procedures during the planning and completion phases of the audit.

Depreciation amounts are determined by exchange transactions with outside parties.

International Standards on Auditing are issued by the International Auditing and

Assurance Standards Board (IAASB).

When performing a review service and the accountant becomes aware that fraud may

have occurred, the accountant must withdraw from the engagement.

Gross negligence is the existence of extreme or unusual negligence with the intent to

deceive.

Level 1 estimates require more management judgment than level 2 or level 3 estimates.

The job time ticket indicates the starting and stopping times of work during the pay

period.

A proof of cash helps the auditor determine whether all recorded cash receipts were

deposited in the bank and whether all recorded cash disbursements were paid by the

bank.

Auditors of public company financial statements must issue separate reports on internal

control over financial reporting.

General transaction-related audit objectives vary from audit to audit, depending on the

nature and characteristics of the client’s business and industry.

There is a direct relationship between acceptable audit risk and planned detection risk.

In applying the audit risk model, auditors are concerned about overstatements, not

understatements.

Completeness and existence are the auditor’s primary objectives in auditing

manufacturing equipment.

There is significant potential for misstatements and misclassification of financial

instruments.

Auditing standards require the engagement partner to be included in discussions about

the susceptibility of the client’s financial statements to material misstatements.

The risk of material misstatement exists only at the overall financial statement level.

To issue an unqualified opinion on internal control over financial reporting, there must

be no identified material weaknesses and no restrictions on the scope of the audit.

The prohibition on direct financial interests applies to covered members in a position to

influence an engagement.

The results of the tests of controls determine whether assessed control risk for sales and

cash receipts needs to be revised.

The transaction-related audit objective of timing is related to the assertion of cutoff.

Analytical procedures are the most expensive type of audit test to perform because of

the expertise and training required to properly use them.

Because attributes sampling is a statistical sampling approach, it allows the auditor to

quantify the allowance for sampling risk and the upper exception rate.

The objective of the test data approach is to determine whether the client’s computer

programs can correctly process valid and invalid transactions.

The two major balance-related audit objectives in testing payroll liabilities are accuracy

and cutoff.

A statement near the bottom of the standard bank confirmation form requires the bank

to inform auditors of open lines of credit and compensating balance requirements.

Individuals engaged in conducting a fraud will generally not misrepresent information

to the auditor.

Tests for kiting are performed using only a schedule of intrabank transfers.

When sending confirmations during most audits of accounts receivable, the emphasis is

often on confirming larger and older accounts.

It is a violation of the rules of conduct if someone does something on behalf of a

member that is a violation if the member does it.

The auditor assesses control risk for each related audit objective and supports control

risk assessments with tests of controls.

Output controls focus on preventing errors during processing.

All evidence must have the same level of persuasiveness.

Negative confirmations are less expensive, and less reliable, than positive

confirmations.

Tests of controls provide an indication of the likelihood of misstatements in both the

income statement and the balance sheet, simultaneously.

Firewalls can protect company data and software programs.

Before accepting a new client, most CPA firms investigate the company to determine its

acceptability. However, AICPA confidentiality requirements prohibit CPA firms from

contacting certain parties”namely the company’s attorneys and bankers”during this

investigation.

If an auditor does a test in the wrong direction, sampling risk will increase.

Under the International Standards for the Professional Practice of Internal Auditing, the

performance standards deal with the education requirements of the internal auditor.

The cutoff objective, “transactions near the balance sheet date are recorded in the

proper period,” is a balance-related audit objective.

“Cookie jar reserves” are often created by companies whenever their earnings are low

to create reserves for future periods when earnings need to be “boosted” upward.

Both sampling and nonsampling risks are associated with

A)

B)

C)

D)

One of the characteristics of professional skepticism is ________, which is the

conviction to decide for oneself, rather than accepting the claims of others.

A) interpersonal understanding

B) autonomy

C) suspension of judgment

D) self-esteem

When an auditor observes that personnel who are responsible for physically counting

inventory are not following the inventory instructions, the auditor should

A) contact a client’s supervisor to correct the problem.

B) modify the client’s physical inventory instructions.

C) not discuss the problem with client’s supervisor in order to maintain independence.

D) assign audit staff to the inventory count.

When analyzing a client’s performance measurement system,

A) ratio analysis and benchmarking against key competitors are utilized.

B) only income statement numbers are used.

C) inherent risk of financial statement misstatements may be decreased if the

performance measurement system encourages aggressive accounting.

D) the auditor is likely to decrease the extent of testing if the client has set unreasonable

objectives.

A third-party beneficiary is one which

A) has failed to establish legal standing before the court.

B) does not have privity of contract and is unknown to the contracting parties.

C) does not have privity of contract, but is known to the contracting parties and

intended to benefit under the contract.

D) may establish legal standing before the court after a contract has been consummated.

Which of the following statements is false?

A) Either an overstatement of an asset account or an understatement of a liability

account would have the same effect on the income statement.

B) A misclassification in the balance sheet will have no effect on operating income.

C) Either an overstatement of an asset account or an overstatement of a liability account

would have the same effect on the income statement.

D) Either an understatement of an asset account or an overstatement of a liability

account would have the same effect on the income statement.

When assets are being verified, auditors focus much of their attention on making sure

that the accounts are not overstated. Alternatively, auditors focus their efforts on

understatement when auditing liabilities. What is the primary reason for this difference

in focus?

A) auditors’ legal liability

B) GAAP

C) GAAS requirements

D) all of the above

Which of the following best explains the relationship between general controls and

application controls?

A) Application controls are effective even if general controls are extremely weak.

B) Application controls are likely to be effective only when general controls are

effective.

C) General controls have no impact on application controls.

D) None of the above

Which of the following is an accurate statement about professional skepticism?

A) Professional skepticism involves a critical assessment of the evidence.

B) Professional skepticism is easy to implement in practice.

C) It is easy for auditors to understand that their clients may try to deceive them

throughout the audit process.

D) Professional skepticism is only necessary for the audits of public companies.

Which of the following statements is not correct?

A) There are many ways an auditor can accumulate evidence to meet overall audit

objectives.

B) Sufficient appropriate evidence must be accumulated to meet the auditor’s

professional responsibility.

C) It is appropriate to minimize the cost of accumulating evidence.

D) Gathering evidence and minimizing costs are equally important considerations that

affect the approach the auditor selects.

When the auditor becomes aware of or suspects noncompliance with laws and

regulations

A) the auditor should evaluate the effects of the noncompliance on other aspects of the

audit.

B) the auditor should discuss the matter with management at a level above those

suspected of the noncompliance.

C) the auditor should obtain additional information to evaluate the possible effects on

the financial statements.

D) all of the above

Calculating the sample size using monetary unit sampling depends on which of the

following factors?

A)

B)

C)

D)

If the results of tests of controls support the design and operations of controls as

expected, the auditor uses ________ control risk as the preliminary assessment.

A) a lower

B) the same

C) a higher

D) either a lower or higher

The principles underlying an audit

A) contain the procedures that must be followed during an audit.

B) carry the same authority as AICPA auditing standards.

C) only apply to the audits of public companies

D) provide structure for the clarified Codification.

Which of the following is most correct with regard to the comparison of the financial

auditing standards of the Yellow Book with the principles of the AICPA auditing

standards?

A) the same as

B) quite different from

C) incompatible with

D) consistent with

Except for two key differences, the transaction-related audit objectives are essentially

the same for the processing of credit memos as they are for sales. Which of the

following are the two key differences?

A) risk and emphasis on the completeness objective

B) materiality and emphasis on the accuracy objective

C) risk and emphasis on the classification objective

D) materiality and emphasis on the occurrence objective

The audit objective to determine that notes payable in the schedule actually exist is

verified by the test of details of balances procedure to

A) foot the notes payable list.

B) confirm notes payable.

C) recalculate interest expense.

D) examine the balance sheet for proper disclosure of noncurrent portions.

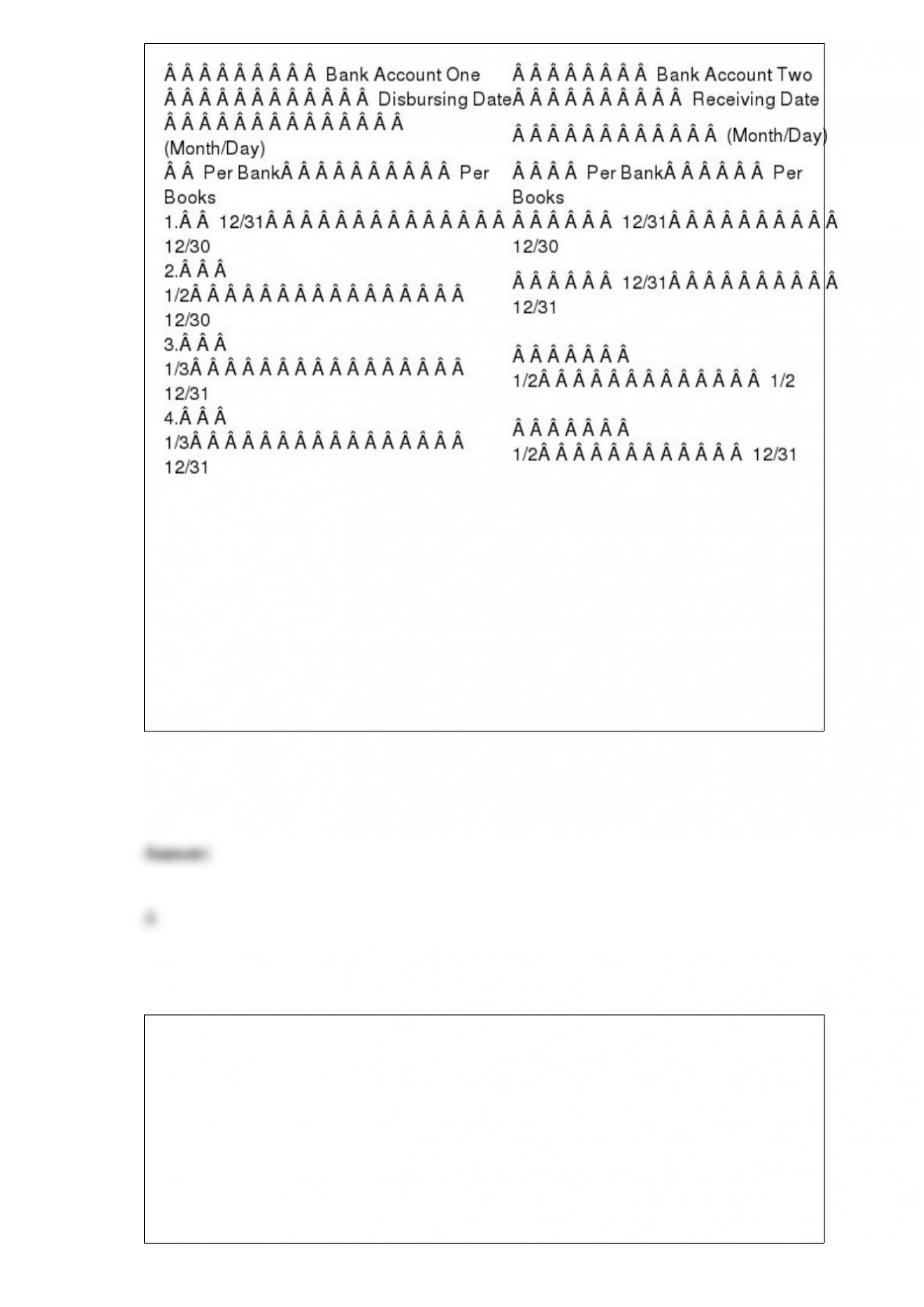

The following information applies to the questions below:

Listed below are four interbank cash transfers, indicated by the numbers 1, 2, 3, and 4,

of a client for late December 2015 and early January 2016:

Based on the schedule of interbank transfers above, which of the cash transfers would

not appear as an outstanding check on the December 31, 2015 bank reconciliation?

A) 1

B) 2

C) 3

D) 4

A deficiency uncovered in the audit of internal control is explained by which of the

following in relation to a financial statement misstatement?

A) the amount of the misstatement

B) the likelihood of the misstatement

C) the amount, likelihood, and classification of the misstatement

D) the amount and the classification of the misstatement

________ is the auditor’s examination of the client’s documents and records to

substantiate that the information is included in the financial statements.

A) Inspection

B) Recalculation

C) Observation

D) Verification

Place the following steps in their proper order:

1. Analyze exceptions.

2. Select the sample.

3. Define attributes and exception conditions.

4. State the objectives of the audit test.

5. Specify the tolerable exception rate.

A) 1, 3, 2, 4, 5.

B) 4, 3, 1, 2, 5.

C) 4, 3, 5, 2, 1.

D) 1, 2, 3, 4, 5.

The auditor designs and performs a combination of tests of controls and substantive

procedures to obtain reasonable assurance that the financial statements are fairly stated

when control risk

A) is assessed above the maximum.

B) is assessed below the maximum.

C) cannot be assessed.

D) none of the above

Which of the following best describes one of the primary objectives of audit

documentation?

A) defend against claims of a deficient audit

B) provide a basis for reviewing the work of subordinates

C) provide reasonable assurance that the audit was conducted in accordance with

auditing standards

D) provide additional support of recorded amounts to the client

Which of the following is not one of the types of engagements and related forms of

conclusions that are defined by the attestation standards?

A) reviews

B) compilations

C) examinations

D) agreed-upon procedures

A document indicating a reduction in the amount owed to a vendor because of returned

goods is

A) a debit memo.

B) a credit memo.

C) a receiving report.

D) a contractual adjustment form.

Changing circumstances may require a change in the useful life of an asset. When this

occurs, it involves a change in

A) accounting estimate rather than a change in accounting principle.

B) accounting principle rather than a change in accounting estimate.

C) both accounting principle and accounting estimate.

D) neither accounting principle nor accounting estimate.

Failure to capitalize a fixed asset at the correct amount would impact which financial

statements?

A) the balance sheet only

B) the income statement only

C) the cash flow statement only

D) both the income statement and the balance sheet

Most auditors believe that financial statements are “presented fairly” when the

statements are in accordance with GAAP, and that it is also necessary to

A) determine that they are not in violation of FASB statements.

B) examine the substance of transactions and balances for possible misinformation.

C) review the statements using the accounting principles promulgated by the SEC.

D) assure investors that net income reported this year will be exceeded in the future.

When a client uses perpetual inventory records, the tests of details of balances for

inventory can be significantly reduced if the auditor believes the records are accurate.

The controls over the acquisitions included in the records are normally tested as a part

of the

A) tests of controls for acquisitions.

B) tests of controls and substantive tests of transactions for acquisitions.

C) tests of details of balances for acquisitions.

D) analytical procedures and tests of controls for acquisitions.

Which of the following departments is most likely responsible for pay rate changes and

changes in deductible amounts for employees?

A) general accounting department

B) human resources department

C) treasurer

D) controller

The Sarbanes-Oxley Act requires which employees of an accounting firm to rotate off

the engagement every five years?

A)

B)

C)

D)

Which of the following is not a business function within the “Sales” class of

transactions?

A) processing customer orders

B) granting credit

C) processing and recording sales returns and allowances

D) shipping goods

Which of the following attestation engagements result in a conclusion that represents

positive assurance?

A) review

B) compilation

C) examination

D) agreed upon procedure engagement

Which of the following best describes the purpose of control activities?

A) the actions, policies and procedures that reflect the overall attitudes of management

B) the identification and analysis of risks relevant to the preparation of financial

statements

C) the policies and procedures that help ensure that necessary actions are taken to

address risks to the achievement of the entity’s objectives

D) activities that deal with the ongoing assessment of the quality of internal control by

management

An audit of historical financial statements most commonly includes the

A) balance sheet, statement of retained earnings, and the statement of cash flows.

B) income statement, the statement of cash flows, and the statement of net working

capital.

C) statement of cash flows, balance sheet, and the statement of retained earnings.

D) balance sheet, income statement, statement of cash flows, and the statement of

changes in stockholders’ equity.

List and briefly describe the three conditions for fraud.

The AICPA Code of Conduct includes a conceptual framework approach for the

member to evaluate threats to compliance with the Code. List the three steps necessary

to evaluate the threats.

Identify the three categories of application controls, and give one example of each.

Explain why the audit of work in process and finished goods inventory is generally

more complex than the audit of purchased inventory.

Why are substantive analytical procedures essential for notes payable?

Define ordinary negligence, gross negligence, and constructive fraud.

What events initiate and terminate the payroll and personnel cycle?

List and briefly describe examples of risk factors for each condition of fraud for

fraudulent financial reporting.

Discuss the six Statements on Standards for Accounting and Review Services (SSARS)

requirements that must be met when an accountant is performing a compilation of

financial statements.

What are the six Ethical Principles stated in the Code of Professional Conduct? Briefly

discuss each principle. Are these principles enforceable?

List each of the five types of audit tests.

Explain what is meant by information risk, and list the four causes of this risk.

What are the three most important controls over cash disbursements?

Senior management is responsible for promoting a culture of honesty and ethics.

Describe what that implies for the organization.

The basis for preparing financial statements for companies is the general ledger. As

soon as possible the auditor obtains the general ledger accounts of the client and

prepares a working trial balance. Discuss the audit documentation in the current file that

relates to the working trial balance. Include a description of lead and support schedules

in your answer.

Evidence is paramount to audit and attestation engagements. List the four basic types of

audit evidence.

Smith and Jones, CPAs, audited the consolidated financial statements of Concord Inc.

and all but one of its subsidiaries for the year ended September 30, 2016 and are

expressing an unqualified opinion on the financials presented as a whole.

Smith, the engagement partner, instructed Mary, an assistant on the engagement, to

draft the auditor’s report on November 4, 2016, the date of fieldwork completion. In

drafting the report Mary considered the following:

– In preparing its financial statements, Concord changed its method of accounting for

research and development costs and properly expensed these amounts. Management

described the change in principle in Note 10 to the consolidated financial statements.

– Ball & Brown, CPAs, audited the financial statements of Biotherm, Inc., a

consolidated subsidiary of Concord for the year ended September 30, 2016. The

subsidiary’s financial statements reflect total assets of 22% and total revenues of 20% of

the consolidated totals. Ball & Brown expressed an unqualified opinion and furnished

to Smith & Jones a copy of their auditor report. Smith & Jones have decided not to

assume responsibility for the work of Ball & Brown insofar as it relates to the

expression of an opinion on the consolidated financial statements taken as a whole

because of the materiality of Biotherm’s financial statements to the consolidated whole.

Ball & Brown’s report will not be presented together with that of Smith & Jones.

– Concord is the subject of a grand jury investigation into possible violations of federal

antitrust laws and possible related crimes. Related civil class actions are pending.

Concord’s management has adequately disclosed in Note 12 to their consolidated

financial statements. Because of the early stage of the investigation, the ultimate

outcome of these matters cannot be determined at this time. Therefore, no provision for

any liability that may result has been recorded.

– Concord experienced a net loss in 2016 and is currently in default under substantially

all of its debt agreements. Management’s plans in regard to these matters are adequately

disclosed in Note 14 to Concord’s consolidated financial statements. The financials do

not include any adjustments that might result from the outcome of this uncertainty.

These matters rase substantial doubt about Concord’s ability to continue as a going

concern.

Ball reviewed Mary’s draft and indicated in his review notes that there were many

deficiencies in Mary’s Draft. The audit report that Mary drafted follows.

Independent Auditor’s Report

We have audited the consolidated financial statements of Concord, Inc., and

subsidiaries as of September 30, 2016, and the related consolidated statements of

income, changes in stockholders equity and cash flows for the year then ended. These

financial statements are the responsibility of the Company’s management. Our

responsibility is to express an opinion on these financial statements based on our audits.

We did not audit the financial statements of Biotherm, Inc., a wholly-owned subsidiary,

which statements reflect total assets and revenues constituting 22% and 20%

respectively at September 30, 2016 of the consolidated totals. Those statements were

audited by Ball & Brown, CPAs, whose reports have been furnished to us, and our

opinion, insofar as it relates to the amounts included for Biotherm, Inc. is based solely

on their report.

We conducted our audit in accordance with generally accepted auditing standards.

Those standards require that we plan and perform the audit to obtain reasonable

assurance about whether the financial statements are free of material misstatement. An

audit includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also includes assessing the accounting

principles used, as well as assessing control risk. We believe our audits provide a

reasonable basis for our opinion.

In our opinion, based on our audit and the report of the other auditors, the consolidated

financial statements referred to above present fairly, in all material respects, the

financial position of Concord Inc., as of September 30, 2016 in conformity with

generally accepted accounting principles, except for the uncertainty, which is discussed

in Note 12 to the consolidated financials.

The accompanying consolidated financial statements have been prepared assuming that

the Company will continue in existence for a reasonable period of time. As discussed in

Note 14 to the consolidated financial statements, the Company suffered a net loss and is

currently in default under substantially all of its debt agreements. Management’s plans

in regard to these matters are also described in Note 14. The consolidated financial

statements do not include any adjustments that might result from the outcome of this

uncertainty.

Smith & Jones, CPAs

November 4, 2016

Required:

The following items present some of the deficiencies in the drafted audit report noted

by Smith. For each deficiency, indicate whether:

S. Smith’s review note is correct

M. Mary’s draft is correct

B. Both Smith’s review note and Mary’s draft are incorrect

Smith’s Review Notes

1. An explanatory paragraph is required between the scope and opinion paragraphs for

the change in accounting principles referring the reader to Note 10.

2. The names of the other auditors do not need to be explicitly stated in the introductory

paragraph. Only that “other auditors” performed the audit and provided their report.

3. The opinion paragraph should extend the auditor’s opinion beyond financial position

to include the results of Concord’s operations and flows.

4. The reference to the uncertainty in the opinion paragraph is incomplete. It should

describe the nature of the uncertainty as pertaining to the grand jury investigation into

possible violations of federal antitrust laws.

5. The explanatory paragraph following the opinion paragraph does not include the

terms ‘substantial doubt” and “going concern”. These terms are required to be used in

this paragraph.

6. The explanatory paragraph following the opinion paragraph includes an inappropriate

statement that “the consolidated financial statements do not include any adjustments

that might result from the outcome of this uncertainty.” This statement is misleading

and should be omitted.