When customers purchase goods by credit card, the issuer of the credit card uses EFT to

transfer funds into the company’s bank account.

The three most important audit objectives for cash are accuracy, existence, and

classification.

Auditing standards require that records for audits of private companies be retained for a

minimum of seven years.

Confirmation is the most common test of details of balances for the accuracy of

accounts receivable.

Tests of details of balances typically involve the use of comparisons and relationships to

assess the overall reasonableness of account balances.

Overall assessment of acceptable audit risk is highly subjective.

Several states have statutes that permit privileged communication between the client

and auditor, allowing a CPA to refuse to testify in state and federal courts.

Net income before taxes is the normal base used to determine materiality for a

not-for-profit organization.

Audits are expected to provide a higher degree of assurance for the detection of

material frauds than is provided for an equally material error.

When auditing insurance expense, auditors normally rely on analytical procedures and

limited testing of the debits to ensure that they arose from credits to prepaid insurance.

Cost of goods sold is generally a residual of beginning inventory less acquisitions plus

ending inventory.

A credit memo is a document used internally that indicates authority to write-off an

account receivable as uncollectible.

Sarbanes-Oxley and the Securities and Exchange Commission restrict auditors from

providing many consulting services to their publicly traded audit clients.

Although systematic sample selection is easy to use, its primary disadvantage is that it

is not a probabilistic sampling method.

As misstatements become more pervasive, the likelihood of issuing a disclaimer rather

than a qualified opinion increases.

Auditors verify the accruals before they verify the current year property tax payments.

Inventory price tests include testing the client’s summarization of the inventory counts.

Auditing the acquisition and payment cycle often takes more time than any other cycle.

As control risk increases, the amount of substantive evidence the auditor plans to

accumulate should increase.

Sales transactions are the result of the following five functions in the sales and

collection cycle: processing customer orders, granting credit, shipping goods, billing

customers, and recording sales.

The presentation and disclosure-related audit objectives are identical to the

management assertions for presentation and disclosure.

Completeness is an important objective for derivative financial instruments.

A shareholders’ capital stock master file is a record of the issuance and repurchase of

capital stock over the life of the corporation.

Although the letter of representation is typed on the client’s letterhead and signed by the

client, it is common for the auditor to prepare the letter.

Auditing standard indicate that if the auditor identifies a significant risk at the assertion

level, the auditor is not required to perform substantive procedures.

If auditors determine that there is not a significant risk of material improper revenue

recognition, no documentation of this decision is required.

Required disclosures for payroll and personnel cycle transactions and balances are

extensive.

Incentives and opportunities are two conditions that are generally present when

financial statement fraud occurs.

The most important element of the audit risk model is control risk.

In a CPA firm, the audit partner coordinates the performance of audit procedures.

In using sampling distribution for attributes, which one of the following must be known

to evaluate the sample results?

A) estimated dollar value of the population

B) standard exception of the values in the population

C) actual exception rate of the attribute in the population

D) sample size

Misstatements must be compared with some measurement base before a decision can be

made about materiality. A commonly accepted measurement base includes

A) net income.

B) total assets.

C) working capital.

D) all of the above.

An advantage of using statistical sampling techniques is that such techniques

A) quantify sampling risk.

B) eliminate the need for judgmental decisions.

C) define the values of precision and reliability required to provide audit satisfaction.

D) have been established in the courts to be superior to judgmental sampling.

The auditor’s starting point for verifying disposals of property, plant, and equipment is

the

A) equipment account in the general ledger.

B) file of shipping documents.

C) client’s schedule of recorded disposals.

D) equipment subsidiary ledger.

The professional organization which is responsible for providing guidance for internal

auditors is the

A) Association of Private Auditors.

B) Institute of Internal Auditors.

C) American Bar Association.

D) Association of Internal Auditors.

A ________ indicates a reduction in the amount due from a customer because of

returned goods or an allowance.

A) bill of lading

B) sales invoice

C) credit memo

D) monthly statement

Which of the following services are allowed by the SEC whenever a CPA also audits

the company?

A) internal audit outsourcing

B) legal services unrelated to the audit

C) appraisal or valuation services

D) services related to assessing the effectiveness of internal control over financial

reporting

The introductory paragraph of the standard unmodified opinion audit report for a

nonpublic company performs which functions?

I. It states the CPA has performed an audit.

II. It lists the financial statements being audited.

III. It states the financial statements are the responsibility of the auditor.

A) I and II

B) I and III

C) II and III

D) I, II and III

Which of the following results in a larger sample size?

A) Decrease the estimated population exception rate and decrease the tolerable

exception rate.

B) Increase the estimated population exception rate and decrease the tolerable exception

rate.

C) Decrease the estimated population exception rate and increase the tolerable

exception rate.

D) Increase the estimated population exception rate and increase the tolerable exception

rate.

Which of the following forms of evidence would be least persuasive in forming the

auditor’s opinion about marketable securities and other investments held by the

company?

A) responses to auditor’s questions by the president and controller regarding the

investments account

B) correspondence with a stockbroker regarding the quantity of client’s investments

held in street name by the broker

C) minutes of the board of directors authorizing the purchase of stock as an investment

D) the auditor’s count of marketable securities

Audit procedures related to contingent liabilities are initially focused on

A) accuracy.

B) completeness.

C) existence.

D) occurrence.

Which of the following represents a correct statement regarding internal control testing?

A) When auditors plan to use evidence about the operating effectiveness of internal

control contained in prior audits, auditing standards require tests of the controls’

effectiveness at least every other year.

B) The greater the risk, the less audit evidence the auditor should obtain that controls

are operating effectively.

C) The auditor uses control risk assessment and results of tests of controls to determine

planned detection risk and the related substantive tests for the financial statement audit.

D) Testing of internal controls can only be performed by the auditor at the end of the

fiscal year.

Which of the following resulted in a federal law passed in 1995 that significantly

reduced potential damages in securities-related litigation?

A) Private Securities Litigation Reform Act

B) Public Securities Damages and Settlements Act

C) Racketeer Influenced and Corrupt Organization Act

D) U.S. Securities Claims Reform Act

As a test of control, the auditor examines sales invoices for supporting documents. The

relevant transaction-related audit objective is

A) accuracy.

B) occurrence.

C) classification.

D) timing.

You are auditing the company’s purchasing process for goods and services. You are

primarily concerned with the company not recording all purchase transactions. Which

audit procedure below would be the most effective audit procedure in this case?

A) vouching from the accounts payable account to the vendor invoices

B) tracing vendor invoices to recorded amounts in the accounts payable account

C) confirmation accounts payable recorded amounts

D) reconciling the accounts payable subsidiary ledger to the accounts payable account

Which of the following is not a general control?

A) separation of IT duties

B) systems development

C) processing controls

D) hardware controls

The legal term for when an auditor issues an audit opinion, knowing that an adequate

audit was not performed, is a

A) breach of contract.

B) tort action for negligence.

C) constructive fraud.

D) fraud.

After the auditor has completed all audit procedures, it is necessary to combine the

information obtained to reach an overall conclusion as to whether the financial

statements are fairly presented. This is a highly subjective process that relies heavily on

A) generally accepted auditing standards.

B) the AICPA’s Code of Professional Conduct.

C) generally accepted accounting principles.

D) the auditor’s professional judgment.

Three common types of attestation services are

A) audits of historical financial statements, reviews of historical financial statements,

and audits of internal control over financial reporting.

B) audits of historical financial information, verifications of historical financial

information, and attestations regarding internal controls.

C) reviews of historical financial information, verifications of future financial

information, and attestations regarding internal controls.

D) audits of historical financial information, reviews of controls related to investments,

and verifications of historical financial information.

Management is responsible for

A)

B)

C)

D)

Auditors of accelerated filer public companies

A) are responsible for reviewing subsequent events for a period of up to six months

after the balance sheet date.

B) must always dual-date their audit reports.

C) must inquire about and consider any information about subsequent events that

materially affects the effectiveness of internal control over financial reporting.

D) must perform all of the above procedures.

Cost accounting controls are those related to the physical inventory and the consequent

costs from the point at which

A) materials are ordered for purchase until the finished product is sold.

B) the customer’s order is received until the finished product is shipped.

C) raw materials are requisitioned until the finished product is sent to storage.

D) raw materials are requisitioned until the finished product is completely

manufactured.

The auditor is responsible for communicating significant internal control deficiencies to

the audit committee, or those charged with governance. This communication

A) may be oral or written.

B) must be oral.

C) must be written.

D) must be oral via direct communication.

Professional standards prohibit which one of the following types of engagements for

prospective financial statements from being undertaken?

A) a compilation

B) a review

C) an examination

D) an agreed-upon procedures engagement

The International Standards for the Professional Practice of Internal Auditing include

which two categories of standards?

A) attribute and performance

B) competency and professional skepticism

C) performance and integrity

D) ethics and rules of conduct

Which of the following is not one of the classes of transactions in the acquisition and

payment cycle?

A) acquisition of common stock

B) acquisition of goods and services

C) cash disbursements

D) purchase returns and allowances and purchase discounts

When deciding the acceptability of the population,

A) the methodology for deciding the acceptability of the population for attributes differs

from determining the acceptability for nonstatistical sampling.

B) before the population can be considered acceptable, the CUER determined on the

basis of the actual sample results must be less than or equal to TER when both are

based on the same ARO.

C) when the CUER is greater than the TER, the auditor must increase the sample size.

D) the CUER is compared with the TER in total, not for each attribute.

When the auditor considers whether he understands the form and substance of the

transaction or event, and whether the relevant authoritative literature has been applied

consistently by the client, he is performing which step in the professional judgment

process?

A) identifying and defining the issue

B) performing the analysis and identifying potential alternatives

C) making the decision

D) gathering the facts

Which of the following statements regarding the capital acquisition and repayment

cycle is most correct?

A) A relatively few transactions affect the cycle, and most are smaller amounts.

B) A large numbers of transactions affect the cycle, and most are smaller amounts.

C) A relatively few transactions affect the cycle, and most are highly material.

D) A large number of transaction affect the cycle, and most are highly material.

The detail tie-in is part of the ________ assertion for account balances.

A) classification

B) valuation and allocation

C) rights and obligations

D) completeness

Which of the following is not a type of statistical method that provides results in dollar

terms?

A) variables sampling

B) attributes sampling

C) monetary unit sampling

D) sampling with probability proportional to size

Most frauds are detected by

A) a confession by the fraudster.

B) IT controls.

C) law enforcement.

D) a tip.

Discuss the differences between errors, frauds, and illegal acts. Give an example of

each.

In accumulating final evidence upon which to base an audit opinion, the auditor should

perform four activities. List the activities below.

There are three primary reasons for obtaining a thorough understanding of the client’s

industry and external environment. What are these reasons?

Describe each of the three broad objectives management typically has for internal

control. With which of these objectives is the auditor primarily concerned?

Discuss the major activities and procedures performed by the auditor in the plan and

design of the audit approach.

The following is a portion of an adverse audit report issued for a public company.

(Note: A separate report was issued on the effectiveness of internal control over

financial reporting.)

Independent Auditor’s Report

To the shareholders of Wallace Corporation

We have audited the accompanying balance sheet of Wallace Corporation as of

December 31, 2016, and the related statements of income, retained earnings, and cash

flows for the year then ended. These financial statements are the responsibility of the

company’s management. Our responsibility is to express an opinion on these financial

statements based on our audit.

We conducted our audit in accordance with the standards of the Public Company

Accounting Oversight Board (United States). Those standards require that we plan and

perform the audit to obtain reasonable assurance about whether the financial statements

are free of material misstatement. An audit includes examining, on a test basis, evidence

supporting the amounts and disclosures in the financial statements. An audit also

includes assessing the accounting principles used and significant estimates made by

management, as well as evaluating the overall financial statement presentation. We

believe that our audit provides a reasonable basis for our opinion.

The company has excluded from property and debt in the accompanying balance sheet

certain lease obligations that, in our opinion, should be capitalized in order to conform

with generally accepted accounting principles. If these lease obligations were

capitalized, property would be increased by $14,500,000, long-term debt by

$13,200,000, and retained earnings by $1,300,000 as of December 31, 2016, and net

income and earnings per share would be increased by $1,300,000 and $2.25,

respectively, for the year then ended.

Required:

Complete the above adverse audit report by preparing the opinion paragraph. Do not

date or sign the report.

Discuss the factors an auditor should consider before accepting a company as an audit

client.

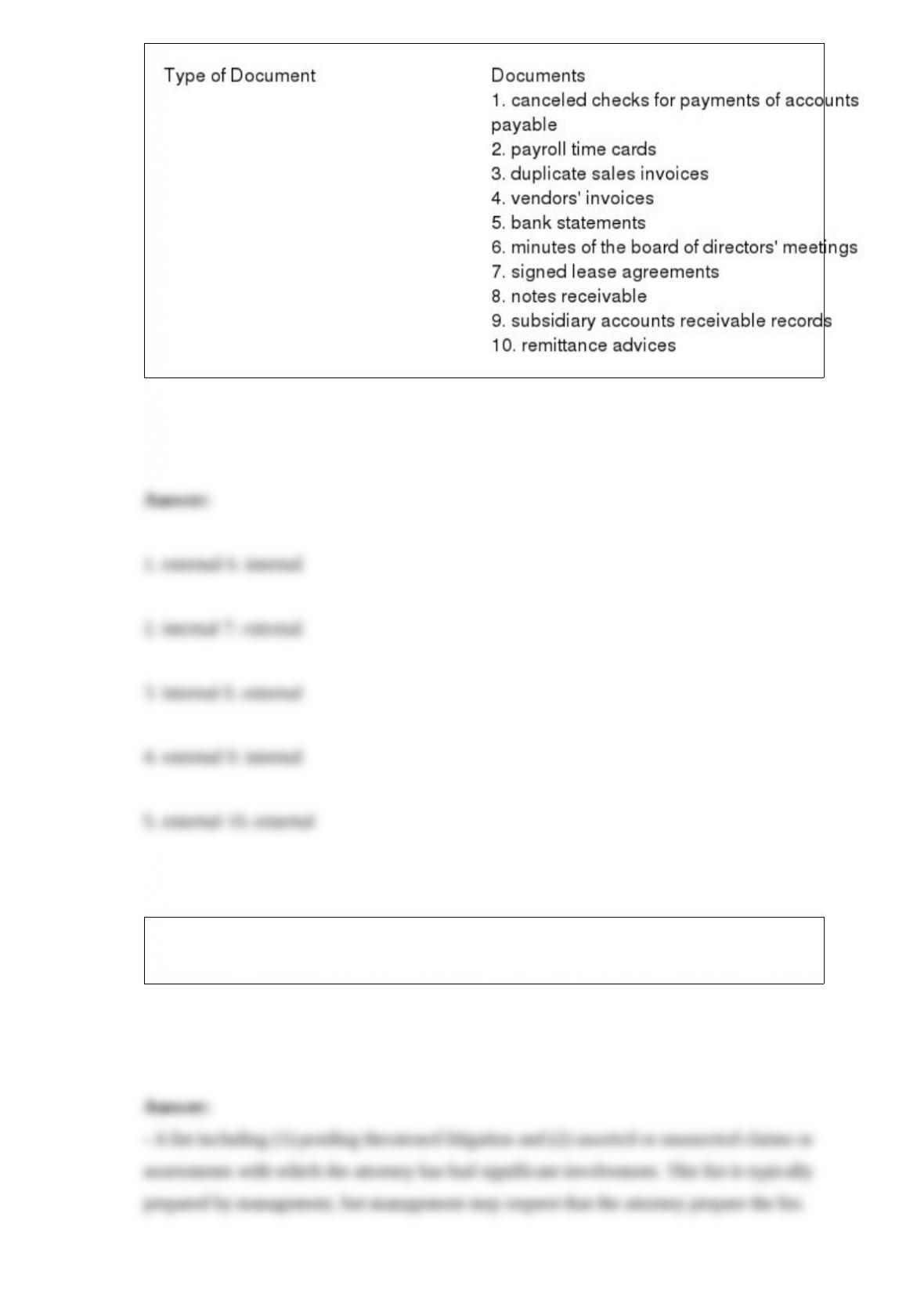

Below are 10 documents typically examined during an audit. Classify each document as

either internal or external.

State three items that should be included in a standard inquiry to the client’s attorney

letter.

What documents do auditors routinely obtain to aid in their understanding of a client’s

governance system? Briefly discuss each of these documents.

Discuss what is meant by the term “control environment” and identify four control

environment subcomponents that the auditor should consider.

Discuss several reasons why an auditor may not wish to continue a relationship with an

existing audit client.

Performance is one of the principles underlying an audit. List three performance

responsibilities.

Explain the audit objective allocation and why it is important to have accurate

allocation within the financial statements, particularly for property, plant, and

equipment.

When using nonstatistical sampling, the auditor must subjectively consider whether the

true population misstatement exceeds a tolerable amount. This is done by considering

five factors. One factor is the difference between the point estimate and tolerable

misstatement. State the other four factors the auditor must consider.

Define control for general controls and application controls. Also list the categories of

controls included under general controls and application controls.

Define the term “related party” and discuss why an auditor should identify the client’s

related parties early in the audit.

Discuss each of the following primary documents and records used in the personnel and

employmentfunction in the payroll and personnel cycle: human resource records,

deduction authorization form, and the rate authorization form.

Discuss the advantages and disadvantages of monetary unit sampling over other

sampling methods.