6-11

6–26 (continued)

The auditor normally assesses the likelihood of material

misappropriation of assets as a part of understanding the entity’s

internal control and assessing control risk. Audit evidence should

Because the auditor’s responsibility is limited to material

misstatements, we believe that the auditor’s responsibility is

The independent auditor is not an insurer or guarantor. The

negligence on the auditor’s part.

6–27 a. Professional skepticism primarily consists of two components: a

questioning mind and a critical assessment of the audit evidence. A

questioning mindset means the auditor approaches the audit with a

to inconsistencies.

b. Because the vendor allowance agreements were unwritten, this

should have increased the auditor’s professional skepticism. In

c. Auditors may be inclined to accept client representations because

of a natural bias to want to trust the client. In addition, if these

d. The following are example of three probing questions related to the

vendor allowances:

Are there written agreements or other corroborating evidence

vendor allowances?

6-12

Copyright © 2017 Pearson Education, Inc.

6–28 1. When Chen Li saw that the recorded balance for the allowance

followed the client’s allowance policy and the fact that AHA’s policy

of recording an allowance for patient receivables equal to the

amount of receivables over 180 days old had historically

approximated subsequent write–offs, Chen Li likely had difficulty

considering an amount different from what was already recorded,

despite the effect of recent regulatory changes on patients’ ability to

pay. This is an example of the anchoring judgment trap.

2. Sherry Zipersky’s judgment was likely impacted by the complexity

extensive information and detailed schedules likely convinced her

of the availability judgment trap.

3. Jason Jackson’s judgment was likely impacted by the confirmation

judgment trap. The contracts and other documentation, including

on the emails that suggested potential concerns about side

agreements that might impact their recording as sales. In this case

disconfirming.

4. Allison Garrett’s judgment about the inventory obsolescence

reserve was likely negatively impacted by the overconfidence

judgment trap. Allison’s experience in auditing clients in the

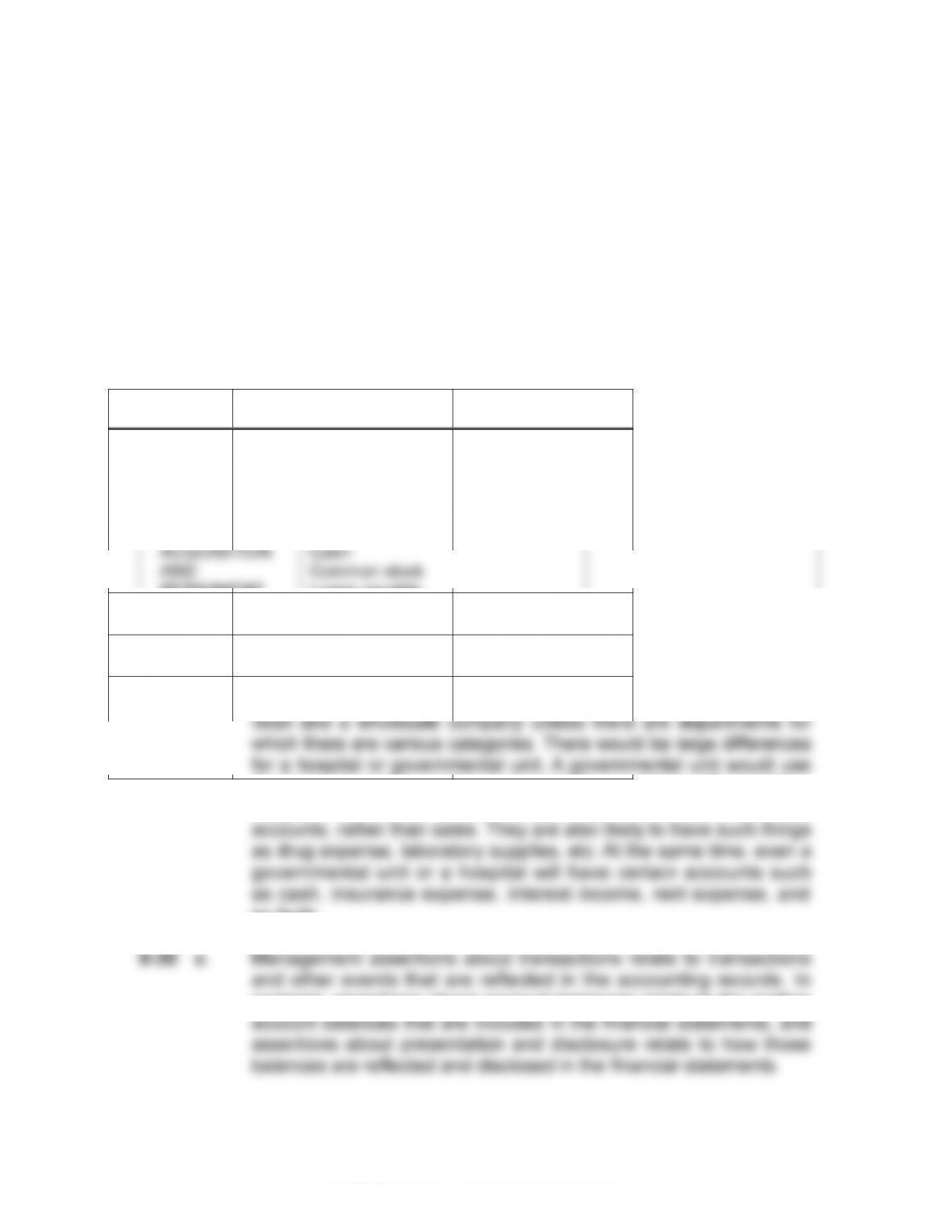

6–29 a.

CYCLE

BALANCE SHEET ACCOUNTS

INCOME STATEMENT

ACCOUNTS

SALES AND

COLLECTION

Accounts receivable

Allowance for doubtful accounts

Cash

Notes receivable—trade

Bad debt expense

Sales

6-13

6–29 (continued)

CYCLE

BALANCE SHEET ACCOUNTS

INCOME STATEMENT

ACCOUNTS

ACQUISITION

AND PAYMENT

Accounts payable

Accumulated depreciation—

furniture and equipment

Cash

Furniture and equipment

Income tax payable

Inventory

Prepaid insurance

Property tax payable

Advertising expense

Depreciation expense—

furniture and equipment

Income tax expense

Insurance expense

Property tax expense

Purchases

Rent expense

Telecommunications

expense

PAYROLL AND

PERSONNEL

Cash

Accrued sales salaries

Salaries, office and general

Sales salaries expense

INVENTORY AND

WAREHOUSING

Inventory

Purchases

CAPITAL

ACQUISITION

AND

REPAYMENT

Accrued interest expense

Cash

Common stock

Loans payable

Notes payable

Retained earnings

Interest expense

accounts, rather than sales. They are also likely to have such things

as drug expense, laboratory supplies, etc. At the same time, even a

6-14

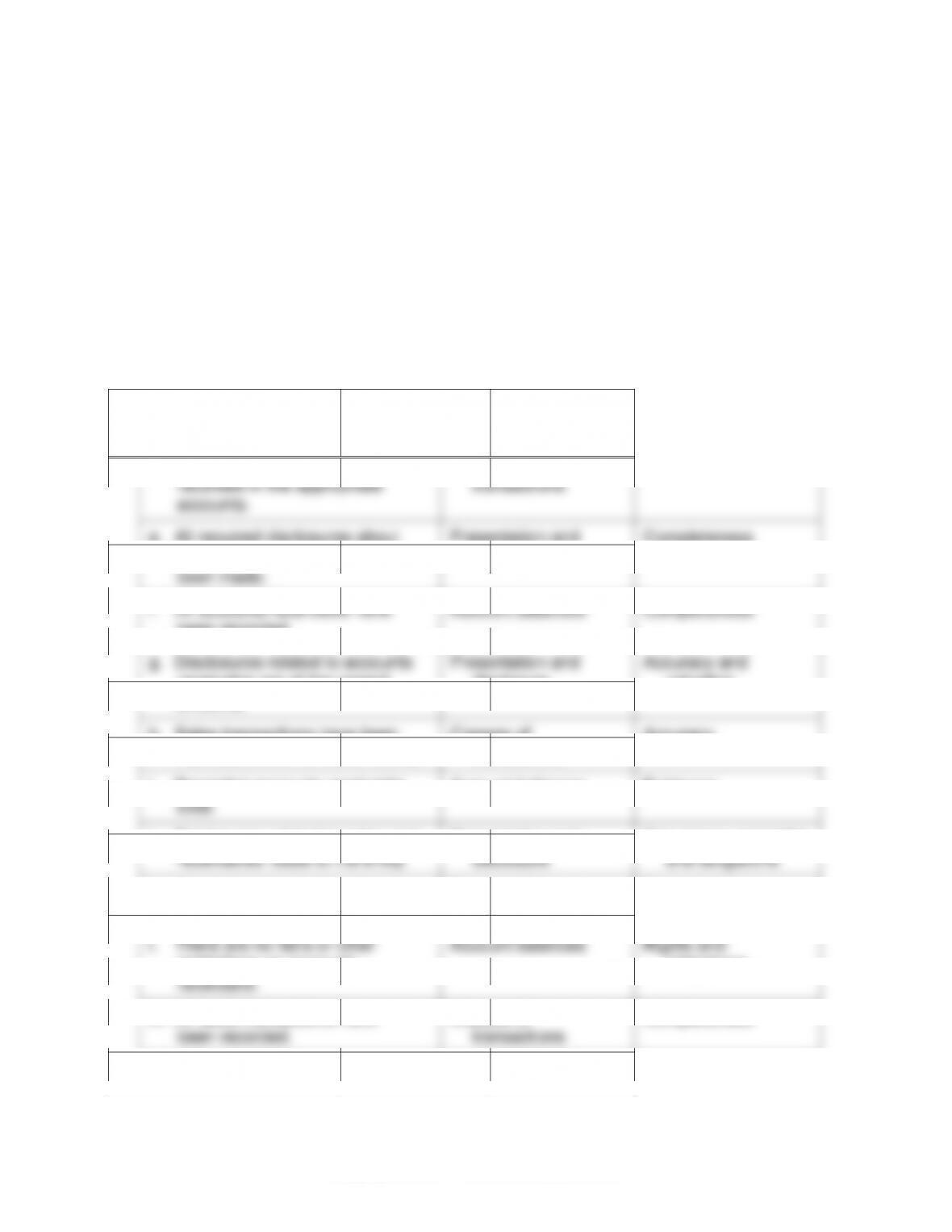

6–30 (continued)

MANAGEMENT ASSERTION

b.

CATEGORY OF

MANAGEMENT

ASSERTION

c.

NAME OF

ASSERTION

a. Receivables are appropriately

classified as to trade and other

receivables in the financial

statements and are clearly

described.

Presentation and

disclosure

Classification and

understandability

b. Sales transactions have been

recorded in the proper period.

Classes of

transactions

Cutoff

c. Accounts receivable are

recorded at the correct amounts.

Account balances

Valuation and

allocation

d. Sales transactions have been

recorded in the appropriate

accounts.

Classes of

transactions

Classification

e. All required disclosures about

sales and receivables have

been made.

Presentation and

disclosure

Completeness

f. All accounts receivable have

been recorded.

Account balances

Completeness

g. Disclosures related to accounts

receivable are at the correct

amounts.

Presentation and

disclosure

Accuracy and

valuation

h. Sales transactions have been

recorded at the correct amounts.

Classes of

transactions

Accuracy

i. Recorded accounts receivable

exist.

Account balances

Existence

j. Disclosures related to sales and

receivables relate to the entity.

Presentation and

disclosure

Occurrence and rights

and obligations

k. Recorded sales transactions

have occurred.

Classes of

transactions

Occurrence

l. There are no liens or other

restrictions on accounts

receivable.

Account balances

Rights and

obligations

m. All sales transactions have

been recorded.

Classes of

transactions

Completeness

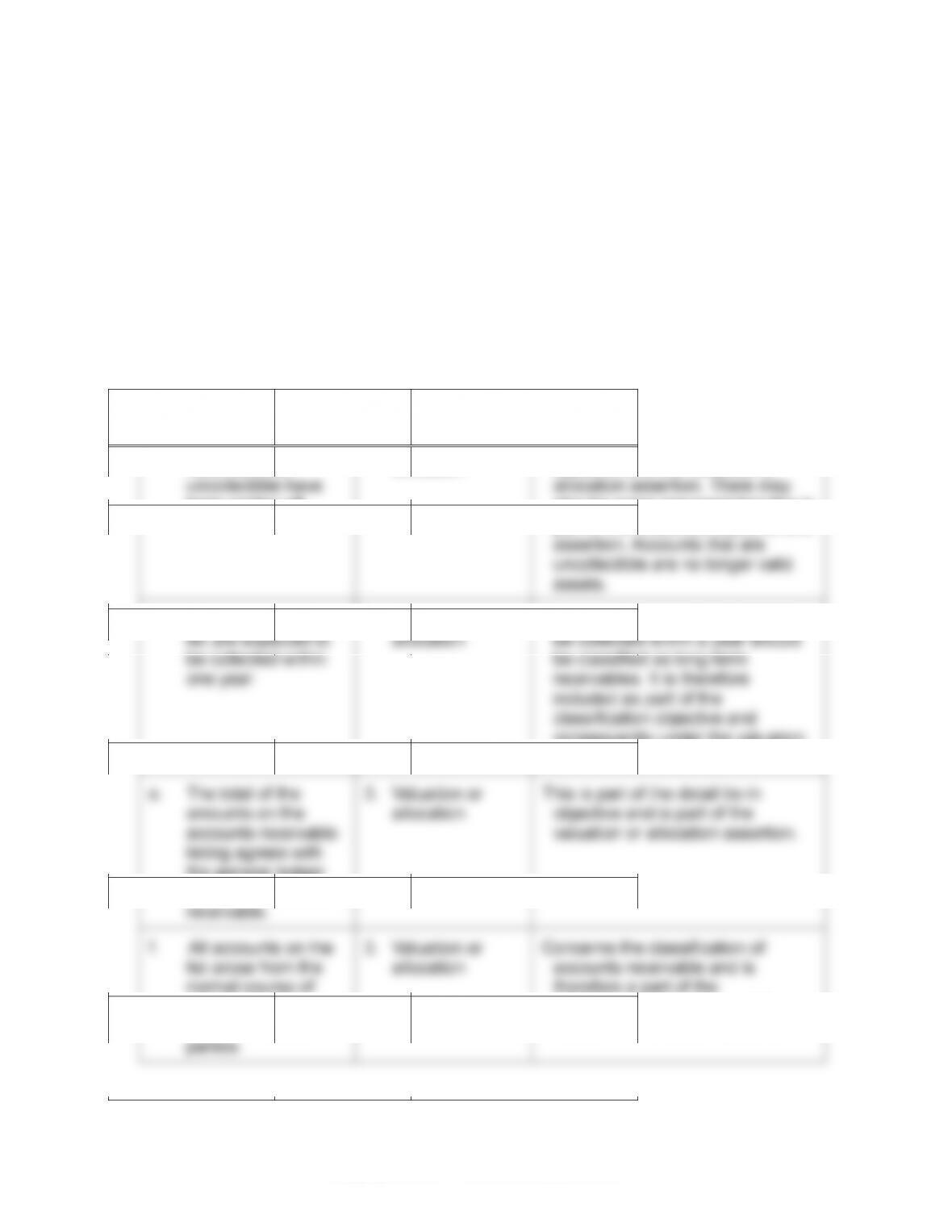

6–31

SPECIFIC BALANCE–

RELATED AUDIT

OBJECTIVE

MANAGEMENT

ASSERTION

COMMENTS

a. There are no

unrecorded

receivables.

2. Completeness

Unrecorded transactions or

amounts deal with the

completeness objective.

b. Uncollectible

accounts have been

provided for.

3. Valuation or

allocation

Providing for uncollectible accounts

concerns whether the allowance

for uncollectible accounts is

adequate. It is part of the

realizable value objective and the

valuation or allocation assertion.

c. Receivables that

have become

uncollectible have

been written off.

3. Valuation or

allocation

This is part of the realizable value

objective and the valuation or

allocation assertion. There may

also be some argument that this is

part of the existence objective and

assertion. Accounts that are

uncollectible are no longer valid

assets.

d. All accounts on the

list are expected to

be collected within

one year.

3. Valuation or

allocation

Accounts that are not expected to

be collected within a year should

be classified as long–term

receivables. It is therefore

included as part of the

classification objective and

consequently under the valuation

or allocation assertion.

e. The total of the

amounts on the

accounts receivable

listing agrees with

the general ledger

balance for accounts

receivable.

3. Valuation or

allocation

This is part of the detail tie–in

objective and is part of the

valuation or allocation assertion.

f. All accounts on the

list arose from the

normal course of

business and are not

due from related

parties.

3. Valuation or

allocation

Concerns the classification of

accounts receivable and is

therefore a part of the

classification objective and the

valuation or allocation assertion.

6-16

6-31 (continued)

SPECIFIC BALANCE–

RELATED AUDIT

OBJECTIVE

MANAGEMENT

ASSERTION

COMMENTS

g. Sales cutoff at year–

end is proper.

3. Valuation or

allocation

Cutoff is a part of the cutoff

objective and therefore part of the

valuation or allocation assertion.

h. Receivables have

not been sold or

discounted.

4. Rights and

obligations

Receivables not being sold or

discounted concerns the rights

and obligations objective and

assertion.

transaction cycle and account. General transaction–related audit

objectives are essentially the same as management assertions, but

they are expanded somewhat to help the auditor decide which audit

evidence is necessary to satisfy the management assertions.

Accuracy and posting and summarization are a subset of the

accuracy assertion. Specific transaction–related audit objectives are

b. and c.

The easiest way to do this problem is to first identify the general

and transaction–related audit objectives for each specific

6-17

6–32 (continued)

SPECIFIC TRANSACTION–

RELATED AUDIT OBJECTIVE

b.

MANAGEMENT

ASSERTION

c.

GENERAL

TRANSACTION–

RELATED AUDIT

OBJECTIVE

a. Existing cash disbursement

transactions are recorded.

2. Completeness

7. Completeness

b. Recorded cash disbursement

transactions are for the amount of

goods or services received and

are correctly recorded.

3. Accuracy

8. Accuracy

c. Cash disbursement transactions

are properly included in the

accounts payable master file and

are correctly summarized.

3. Accuracy

9. Posting and

summarization

d. Recorded cash disbursements

are for goods and services

actually received.

1. Occurrence

6. Occurrence

e. Cash disbursement transactions

are properly classified.

4. Classification

10. Classification

f. Cash disbursement transactions

are recorded on the correct dates.

5. Cutoff

11. Timing

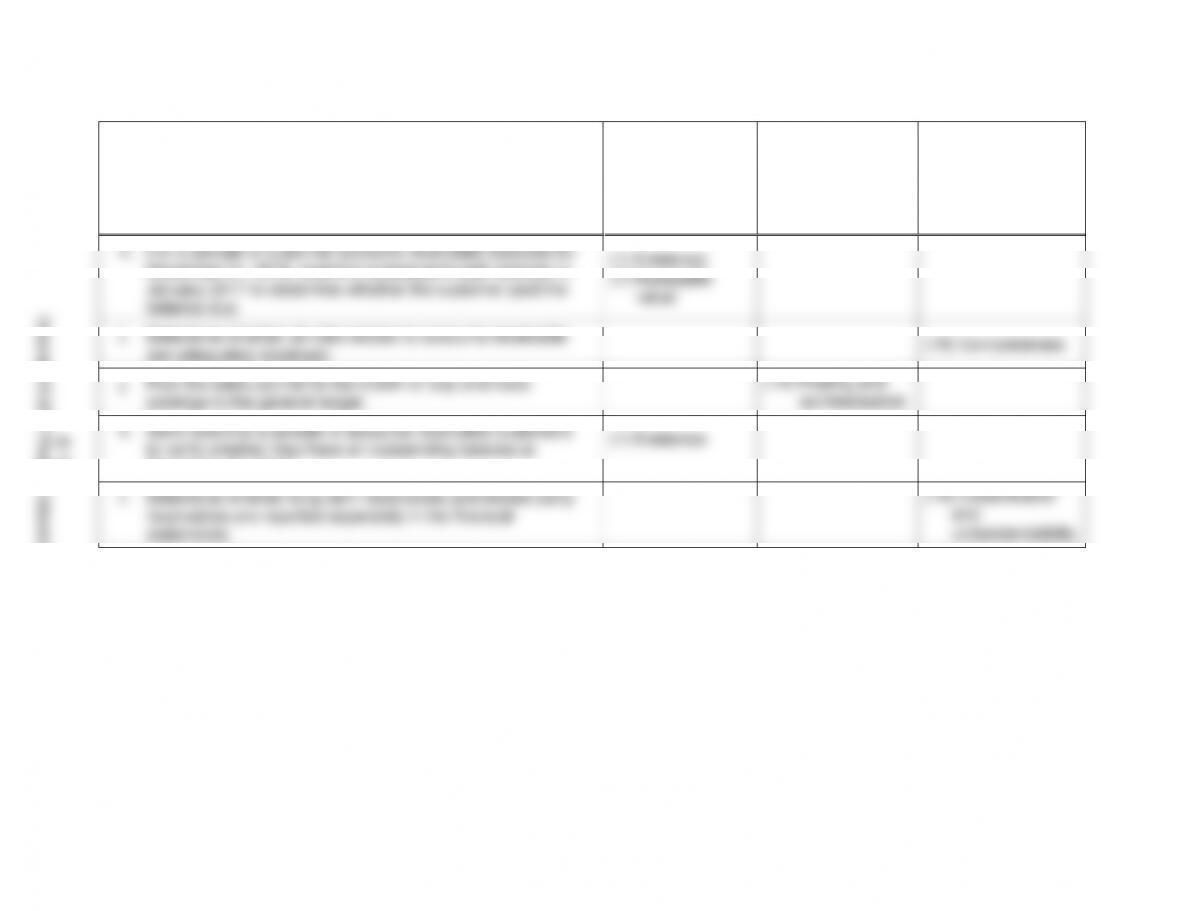

6–33

AUDIT PROCEDURE

BALANCE–

RELATED

AUDIT

OBJECTIVE

TRANSACTION

RELATED

AUDIT

OBJECTIVE

PRESENTATION

AND

DISCLOSURE

AUDIT

OBJECTIVE

a. Examine a sample of duplicate sales invoices to determine

whether each one has a shipping document attached.

(9) Occurrence

balance and agree the amount to the general ledger.

(6) Detail Tie–In

c. For a sample of sales transactions selected from the sales

journal, verify that the amount of the transaction has been

recorded in the correct customer account in the accounts

receivable subledger.

(14) Posting and

summarization

d. Inquire of the client whether any accounts receivable

balances have been pledged as collateral on long–term

debt and determine whether all required information is

included in the footnote description for long–term debt.

(15) Occurrence

and rights

e. For a sample of shipping documents selected from shipping

records, trace each shipping document to a transaction

recorded in the sales journal.

(10) Completeness

f. Discuss with credit department personnel the likelihood of

collection of all accounts as of December 31, 2016, with a

balance greater than $100,000 and greater than 90 days

old as of year–end.

(7) Realizable

value

g. Examine sales invoices for the last five sales transactions

recorded in the sales journal in 2016 and examine shipping

documents to determine they are recorded in the correct

period.

(5) Cutoff

6-18

Copyright © 2017 Pearson Education, Inc.

6–33 (continued)

AUDIT PROCEDURE

BALANCE–

RELATED

AUDIT

OBJECTIVE

TRANSACTION

RELATED

AUDIT

OBJECTIVE

PRESENTATION

AND

DISCLOSURE

AUDIT

OBJECTIVE

h. For a sample of customer accounts receivable balances for

December 31, 2016, examine subsequent cash receipts in

January 2017 to determine whether the customer paid the

balance due.

(1) Existence

(7) Realizable

value

i. Determine whether all risks related to accounts receivable

are adequately disclosed.

(16) Completeness

j. Foot the sales journal for the month of July and trace

postings to the general ledger.

(14) Posting and

summarization

k. Send letters to a sample of accounts receivable customers

to verify whether they have an outstanding balance at

December 31, 2016.

(1) Existence

l. Determine whether long–term receivables and related party

receivables are reported separately in the financial

statements.

(18) Classification

and

understandability

6-19

Copyright © 2017 Pearson Education, Inc.

6-20

6–34

AUDIT ACTIVITIES

AUDIT PHASE

a. Examine invoices supporting fixed asset

additions.

3. Perform substantive analytical

procedures and tests of details of

balances (Phase III)

b. Review industry databases to assess

the risk of material misstatements in the

financial statements.

1. Plan and design an audit

approach based on risk

assessment procedures (Phase I)

c. Summarize misstatements identified

during testing to assess whether the

overall financial statements are fairly

stated.

4. Complete the audit and issue an

audit report (Phase IV)

d. Test computerized controls over credit

approval for sales transactions.

2. Perform tests of controls

and substantive tests of

transactions (Phase II)

e. Send letters to customers confirming

outstanding accounts receivable balances.

3. Perform substantive analytical

procedures and tests of details of

balances (Phase III)

f. Perform analytical procedures comparing

the client with similar companies in the

industry to gain an understanding of the

client’s business and strategies.

1. Plan and design an audit

approach based on risk

assessment procedures (Phase I)

g. Compare information on purchase

invoices recorded in the acquisitions

journal with information on receiving

reports.

2. Perform tests of controls and

substantive tests of transactions

(Phase II)