If an auditor concludes there are contingent liabilities, then he or she must evaluate the

A)

B)

C)

D)

The auditor must gather sufficient and appropriate evidence during the course of the

audit. Sufficient evidence must

A) be well documented and cross-referenced in the audit documents.

B) be based on sources that are external to company.

C) provide evidence that prove or disprove an audit objective/assertion.

D) be persuasive enough to enable the auditor to issue an audit report.

Which of the following audit procedures would be least likely to lead the auditor to find

an unrecorded fixed asset disposal?

A) Examination of insurance policies

B) Review of repairs and maintenance expense

C) Review of property tax files

D) Scanning of invoices for fixed asset additions

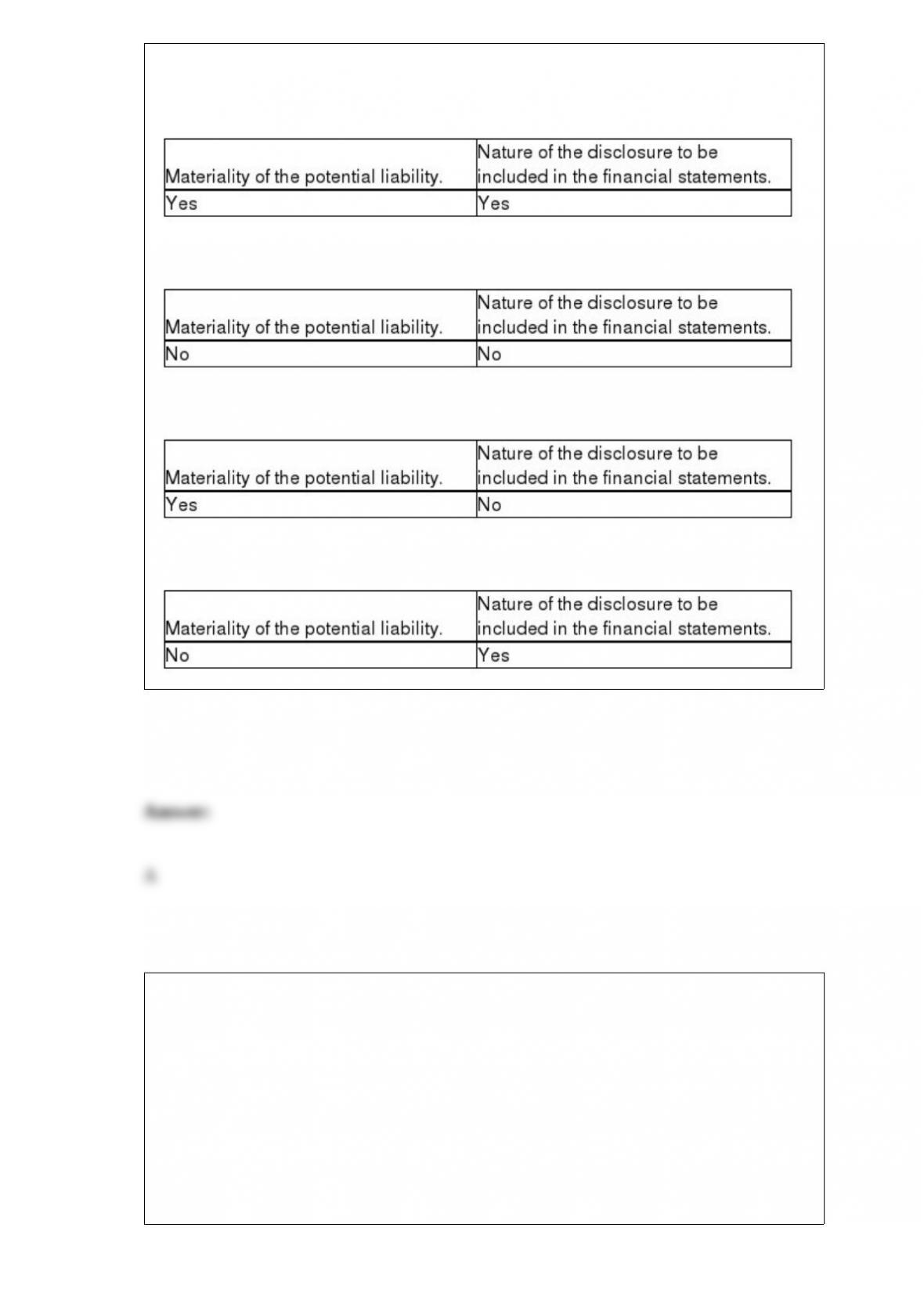

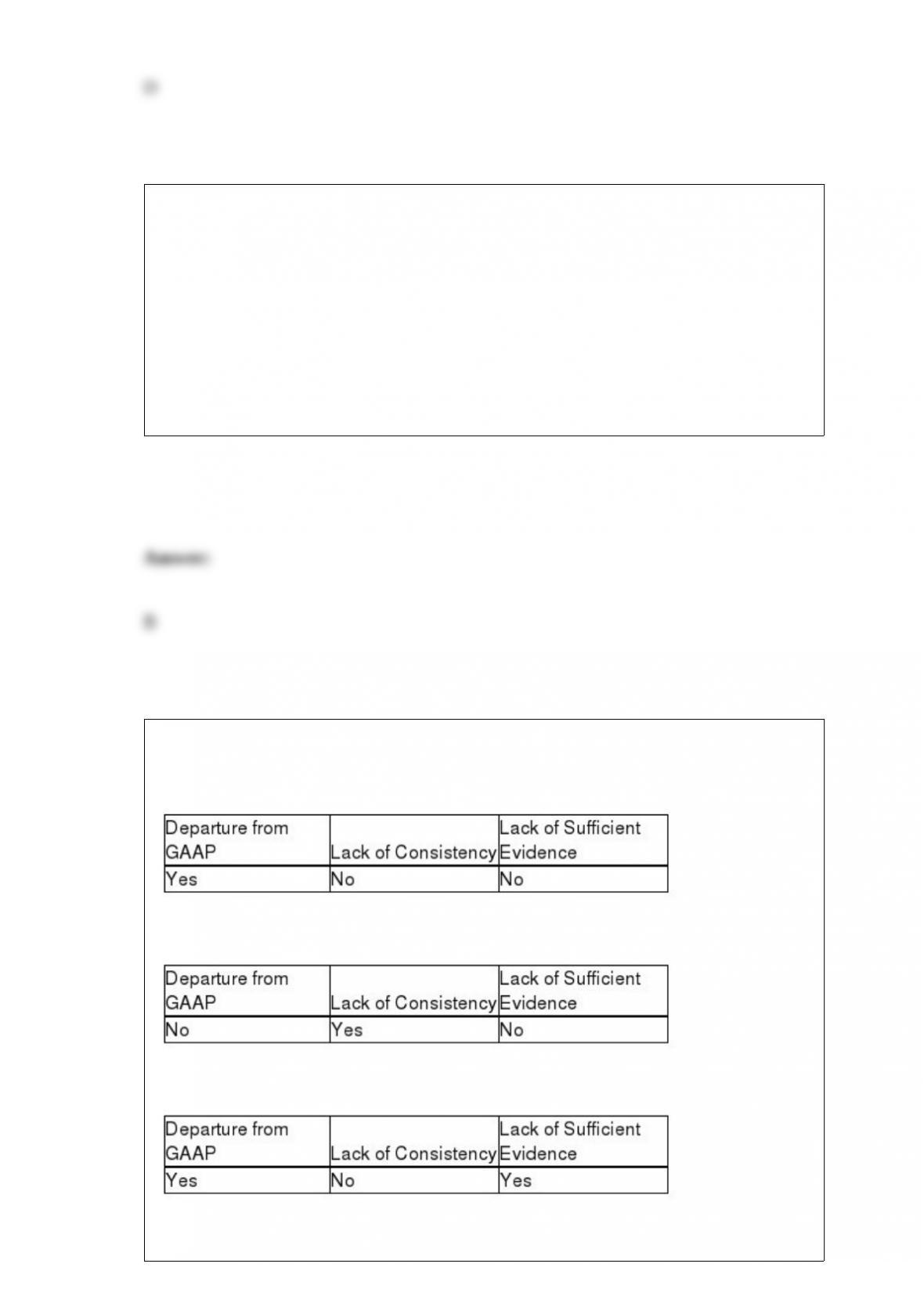

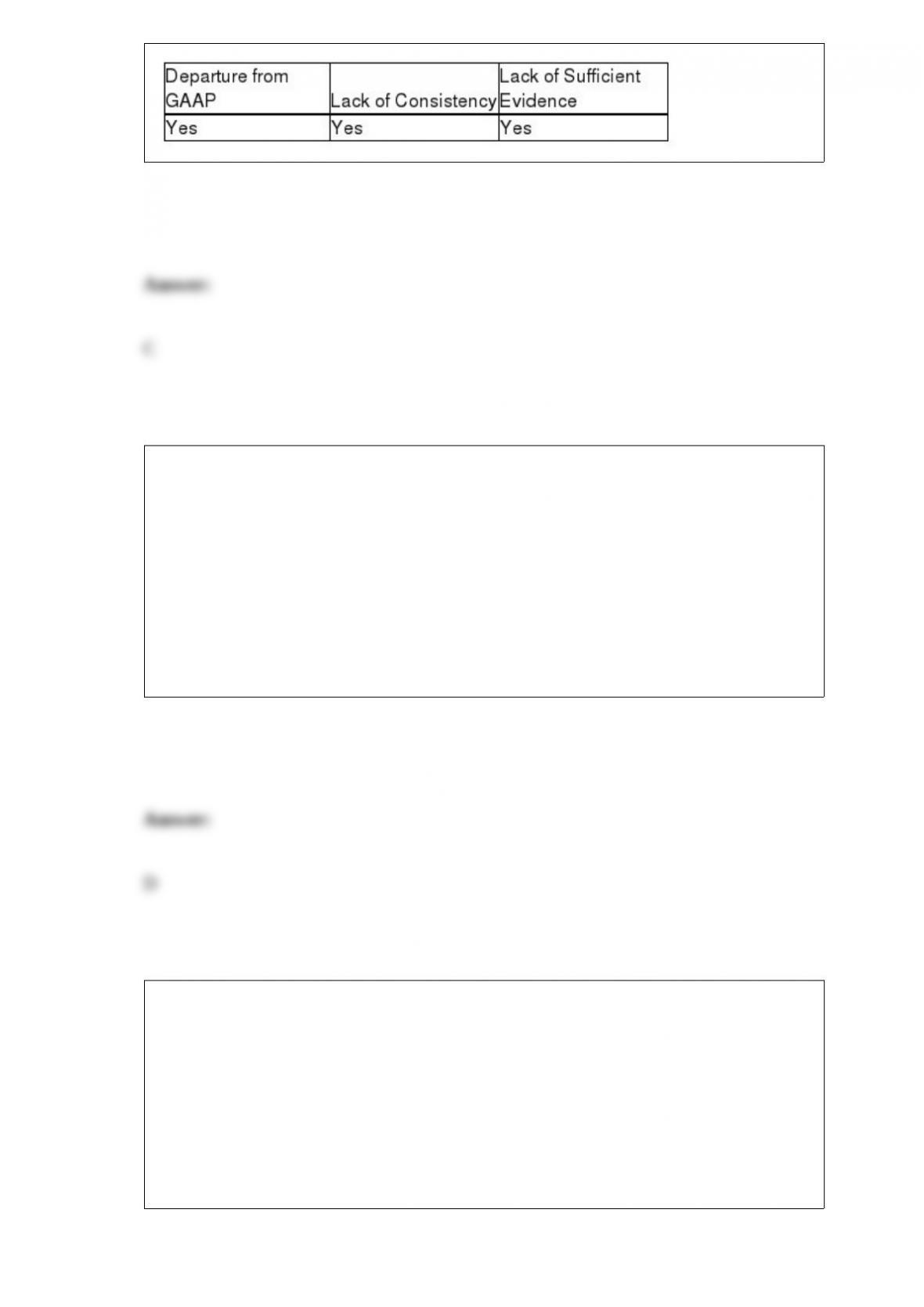

When dealing with materiality and scope limitation conditions,

A) a disclaimer of opinion must be issued.

B) it is easier to evaluate the materiality of potential misstatements resulting from a

scope limitation than for failure to follow GAAP.

C) scope limitations imposed by the client are always considered material.

D) a unqualified opinion may still be issued depending on the materiality of the scope

limitation.

The reliance the auditor places on substantive tests in relation to the reliance placed on

internal control varies in a relationship that is ordinarily

A) parallel.

B) inverse.

C) direct.

D) equal.

An auditor can express a qualified opinion due to a

A)

B)

C)

D)

Which of the following is a performance standard under the International Standards for

the Professional Practice of Internal Auditing?

A) proficiency and due professional care

B) independence and objectivity

C) requirement that the internal audit must be a CPA

D) engagement planning

When performing an operational audit, the internal audit team must first determine that

A) a financial audit has been performed by an independent auditor.

B) a financial audit has been performed by an internal auditor.

C) a review was performed by either an independent or an internal auditor.

D) specific criteria are developed to define effectiveness.

Which of the following is a component of general controls?

A) processing controls

B) output controls

C) back-up and contingency planning

D) input controls

Auditors are especially concerned with three aspects of internal control for the sales and

collection cycle. Which of the following is not one of their major concerns?

A) controls over cutoff

B) controls that prevent or detect embezzlements

C) controls over sales discounts

D) controls related to the allowance for uncollectible accounts

The scenarios below all involve a possible violation of the AICPA’s Code of

Professional Conduct.

1. Using the list below, indicate which of the Code of Conduct Rules applies to the

scenario.

a. Independence

b. Integrity and Objectivity

c. Contingent Fees

d. Acts Discreditable

e. Commissions and Referral Fees

f. Form of Organization and Name

2. State if the scenario is a violation of the Code.

Scenario:

1. Margaret Henry is a partner in the Tupelo office of Jenkins & Thorn, CPAs.

Margaret’s father is the controller at Markrich Sporting Supplies, Inc., a publicly held

company in Tupelo. Markrich is one of Jenkins & Thorn’s audit clients. Margaret is not

involved in the audit of Markrich.

2. Jason Alexander is an audit manager with Reese & Co., CPAs. Jason owns 100 share

of common stock in one of the firm’s audit clients, but he does not provide any audit or

non-audit services to the company.

3. The accounting firm of Fine & Herman, CPAs, provides bookkeeping and tax

services for Henderson Corporation, a privately held company. Mr. Herman also

performs the annual audit of Henderson Corporation.

4. Elaine Cooper, CPA, is the auditor of Paula’s Pizza. Toward the end of the audit,

Paula gave Elaine her estimate of receivable collectability and Elaine accepted it

without any testing.

5. Charley Ray, CPA, is a member of the engagement team that performs the audit of

Desiree Corporation. Charley’s five-year-old daughter, Becky, received ten shares of

Desiree common stock for her fifth birthday in a trust fund established by Becky’s

grandmother.

6. Freeman and Johnson formed a successful CPA practice ten years ago. In the current

year, they approached Adam Sawtooth, a surgeon and medical expert, and asked him to

assist them with their growing medical consulting practice. Sawtooth agreed, but only

after he was given an ownership interest in the firm. Sawtooth does intend to reduce his

private practice hours and spend 40% of his working hours devoted to the Freeman &

Johnson practice.

7. Sally Preen has a successful computer network consulting business. Sally has

recommended one of her clients to Sam Walton, CPA. To show gratitude for the

referral, Sam has agreed to pay Sally a token gift of $50. Sam has not disclosed the

payment arrangement to his ne clients.

8. The accounting firm of Smith & Black, CPAs, is negotiating a fee with a new audit

client where the client will pay $50,000 if the client obtains the line of credit needed for

working capital purposes. Otherwise, the fee will be $40,000.

9. Brad Barns, CPA, was traveling from Las Vegas to the Grand Canyon when he was

pulled over by a police officer for suspicion of driving under the influence. He was

convicted in court of driving under the influence of alcohol and received six months’

probation.

10. Manuel Lopez, CPA, is a senior in a small, local, CPA firm that audits Childress,

Inc., a closely held corporation. Manuel’s sister was recently appointed as the controller

for Childress, Inc.

Within the context of quality control, the primary purpose of continuing professional

education and training activities is to enable a CPA firm to provide its personnel with

A) technical training that assures proficiency as a valuation expert.

B) professional education that is required in order to perform with due professional

care.

C) knowledge required to fulfill assigned responsibilities.

D) knowledge required to perform a peer review.

The documents typically used to reconcile the balance on the accounts payable list with

the confirmation or vendor’s statements include all of the following except for

A) receiving reports.

B) vendor’s invoices.

C) sales invoices.

D) cancelled checks.

Which of the following is not a phase in the planning of both statistical and

nonstatistical sampling?

A) Plan the sample.

B) Determine the probability that fraud has occurred.

C) Select the sample and perform the tests.

D) Evaluate the results.

Which of the following further audit procedures are used to determine whether all six

transaction-related audit objectives have been achieved for each class of transactions?

A) tests of controls

B) risk assessment procedures

C) substantive tests of transactions

D) preliminary analytical procedures

In performing a review of a client’s cash disbursements, an auditor uses systematic

sample selection with a random start. The primary disadvantage of this technique is

population items

A) may occur twice in the sample.

B) must be reordered in a systematic pattern before the sample can be drawn.

C) may occur in a systematic pattern, thus negating the randomness of the sample.

D) must be replaced in the population after sampling to permit valid statistical

inference.

When an acquisition is on an FOB origin basis, the inventory and related accounts

payable must be recorded in the current period if the goods were

A) received prior to the balance sheet date.

B) shipped on or before the balance sheet date.

C) both shipped and received prior to the balance sheet date.

D) paid for in advance.

When an auditor believes that an illegal act may have occurred, the auditor should first

A) obtain an understanding of the nature and circumstances of the act.

B) consult with legal counsel or others knowledgeable about the illegal act.

C) discuss the matter with the audit committee.

D) withdraw from the engagement.

Auditors may decide to replace tests of details with analytical procedures when possible

because the

A) analytical procedures are more reliable.

B) analytical procedures are considerably less expensive.

C) analytical procedures are more persuasive.

D) tests of details are more difficult to interpret.

Which of the following is not one of the five classes of transactions included in the

sales and collection cycle?

A) sales returns and allowances

B) write-off of uncollectible accounts

C) bad debt expense

D) interest income

Which of the following is not an objective of the auditor’s examination of notes

payable?

A) to determine whether internal controls are adequate

B) to determine whether client’s financing arrangements are effective and efficient

C) to determine whether transactions regarding the principal and interest of notes are

properly authorized

D) to determine whether the liability for notes and related interest expense and accrued

liabilities are properly stated

________ are used as evidence to provide assurance about an account balance.

A) Substantive analytical procedures

B) Tests of transactions

C) Audit risks

D) Tests of details of balances

At what point do most companies recognize liabilities in the acquisition and payment

cycle when the goods are shipped FOB destination?

A) when the purchase order is issued

B) when the vendor acknowledges receipt of the order

C) when the goods or services are received

D) when the vendor invoice is received

The primary emphasis by auditors is on controls over

A) classes of transactions.

B) account balances.

C) both A and B, because they are equally important.

D) both A and B, because they vary from client to client.

What typically ends the acquisitions and payment cycle?

A) issuance of a purchase requisition or request for purchase of goods/services

B) issuance of a payment on accounts payable

C) approval of a new vendor

D) purchase requisition

Factors that determine the auditor’s willingness to accept a document as reliable

evidence include

A) whether it is internal or external.

B) whether it was created and processed under conditions of effective internal control.

C) whether it is an original document or a photocopy.

D) all of the above.

Which of the following is the risk that audit tests will not uncover existing exceptions

in a sample?

A) sampling risk

B) nonsampling risk

C) audit risk

D) detection risk

The statistical methods used to evaluate monetary unit samples

A) neither exclude nor include units twice.

B) may permit the inclusion of a unit in the sample more than once.

C) do not permit a unit to be included in the sample more than once.

D) ignore the possibility that a unit may be included in a sample more than once.

Analytical procedures can be very effective in detecting inventory fraud. Which of the

following analytical procedures would not be useful in detecting fraud?

A) gross margin percentage

B) inventory turnover

C) cost of sales percentage

D) accounts receivable turnover

A written purchase order is a contractual document that is

A) an offer to buy goods or services.

B) not enforceable if it is not in writing.

C) prepared by the receiving department.

D) an acceptance of a vendor’s catalog offer to sell.

McKesson & Robbins Company is a well-known audit case involving auditor

responsibility. What occurred at the McKesson & Robbins Company to change the way

in which auditors audit inventory?

A) The company recorded nonexistent inventory.

B) The auditor did not perform any audit tests of the inventory.

C) The auditor and company colluded to overstate inventory balances.

D) The company counted inventory three months prior to year-end.

Under common law, a foreseen user would be treated the same as

A)

B)

C)

D)

In order to strengthen controls over cost accounting information, a company should

consider implementing

A) perpetual inventory master files.

B) a job order cost accounting system.

C) an accounting system that keeps separate the records of the accounting department

from the records of the production department.

D) an economic quantity order system.