Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

15-11

15-28 (continued)

billing date for timeliness of billing. (Timing)

3. Trace entries into perpetual inventory records to determine

e. The test performed in part c. cannot be used to test for occurrence

of sales because the auditor already knows that inventory was

shipped for these sales. To test for occurrence of sales, the sales

15-29 a. It would be appropriate to use attributes sampling for all audit

procedures except audit procedures 1 and 2. Procedure 1 involves

recalculation of just one month’s sales journal’s mathematical

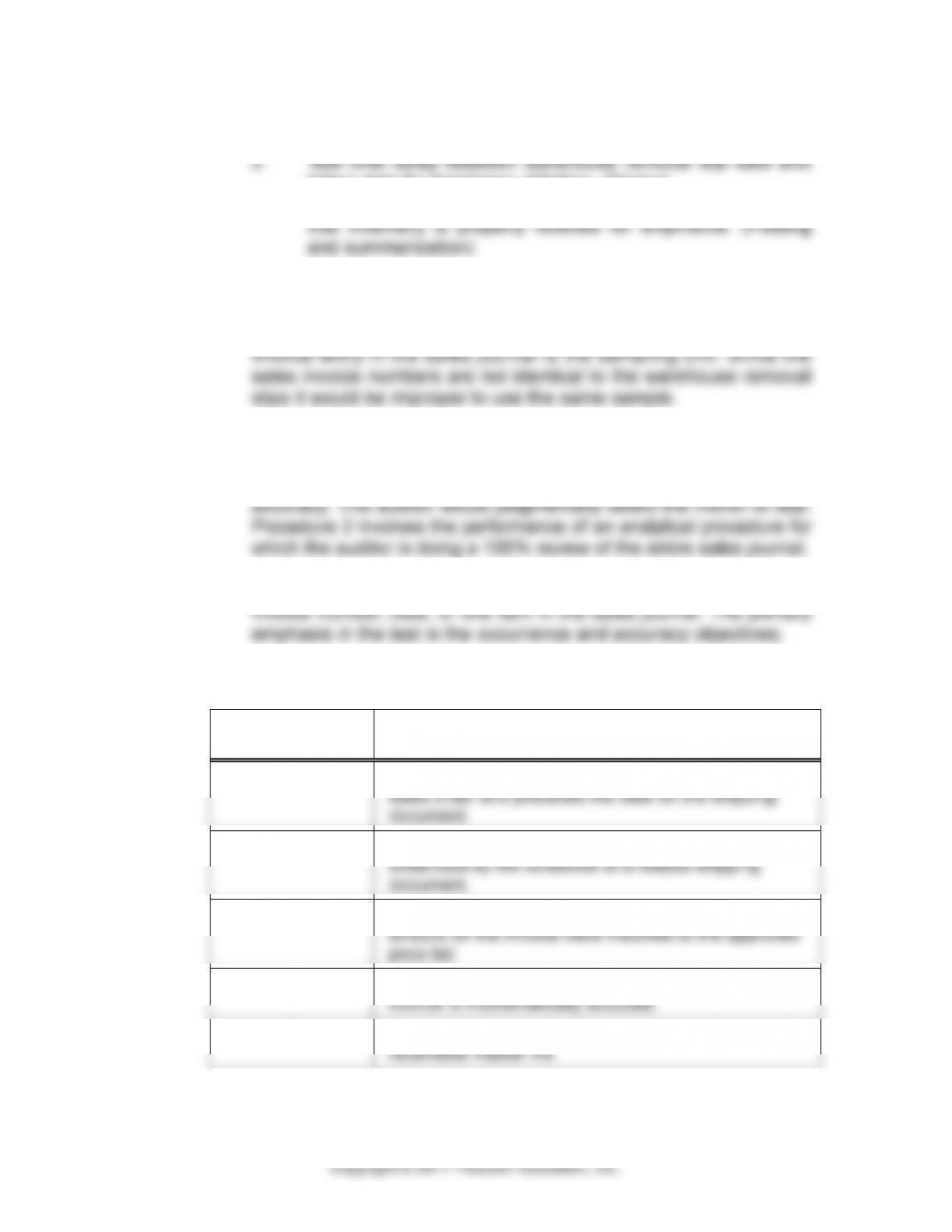

b. The appropriate sampling unit for audit procedures 3-7 is a sales

c. The attributes for testing are as follows:

AUDIT

PROCEDURE

ATTRIBUTE

3

The date that credit approval is documented on the

sales order and precedes the date on the shipping

document.

4

Entries in the sales journal have been shipped as

evidenced by the existence of a related shipping

document.

5

Evidence that prices used to calculate the sales

amount on the invoice were matched to the approved

price list.

6

The calculation of the sales amount on the sales

invoice is mathematically accurate.

7

Entry in the sales journal matches entry in accounts

receivable master file.

15-12

15-29 (continued)

d. The sample sizes for each attribute are as follows:

AUDIT

PROCEDURE

TEST OF

CONTROL OR

SUBSTANTIVE

TEST OF

TRANSACTIONS

SAMPLE SIZE

SAMPLE

SIZE

ARO

TER

EPER

3

T of C

5%

6%

1.0%

78

4

ST of T

5%

5%

0.5%

93

5

T of C

5%

6%

1.0%

78

6

ST of T

5%

5%

0.5%

93

7

ST of T

5%

5%

0.5%

93

point to remember is that the sample sizes chosen should reflect

the changes in the four factors (ARO, TER, EPER, and population

decisions:

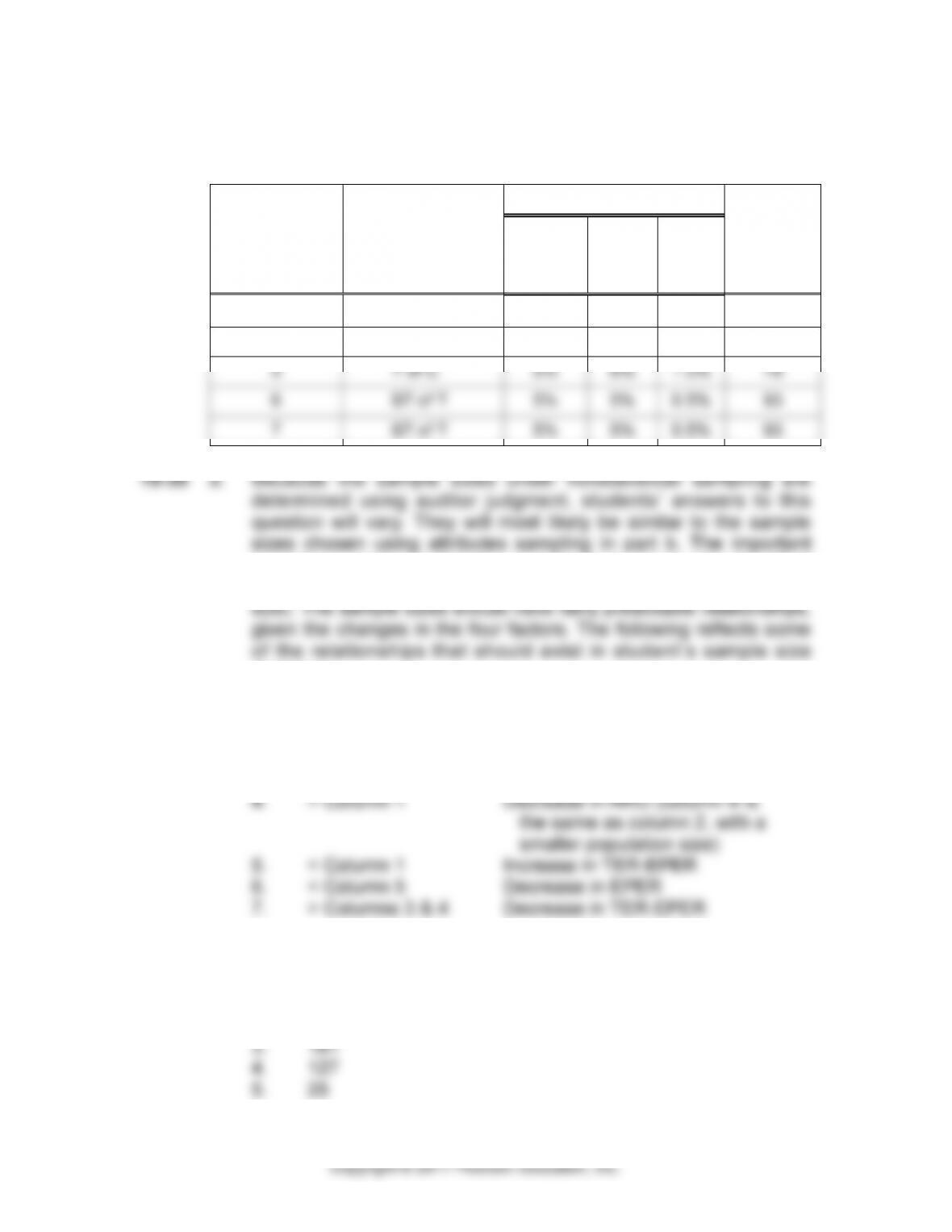

SAMPLE SIZE EXPLANATION

1. 90 Given

2. > Column 1 Decrease in ARO

3. > Column 2 Decrease in TER

b. Using the attributes sampling table in Table 15-8, the sample

sizes for columns 1-7 are:

1. 88

2. 127

15-30 (continued)

6. 18

7. 149

c.

CHANGE IN

FACTORS

EFFECT ON

SAMPLE SIZE

ILLUSTRATION IN

PART a. or b.

1. Increase in ARO.

Decrease

Compare columns 4 and 1

2. Increase in TER.

Decrease

Compare columns 3 and 2

(population sizes are not

consistent, but this has

little effect on sample

size)

3. Increase in EPER.

Increase

Compare columns 6 and 5

4. Increase in

population size.

No effect or slight

increase

Compare columns 4 and 2

e. The greatest effect on the sample size is the difference between

TER and EPER. For columns 3 and 7, the differences between the

TER and EPER were 3% and 2% respectively. Those two also had

Population size has the least effect on sample size. The

difference in population size in columns 2 and 4 was 99,000 items,

f. The sample size is referred to as the initial sample size because it

15-14

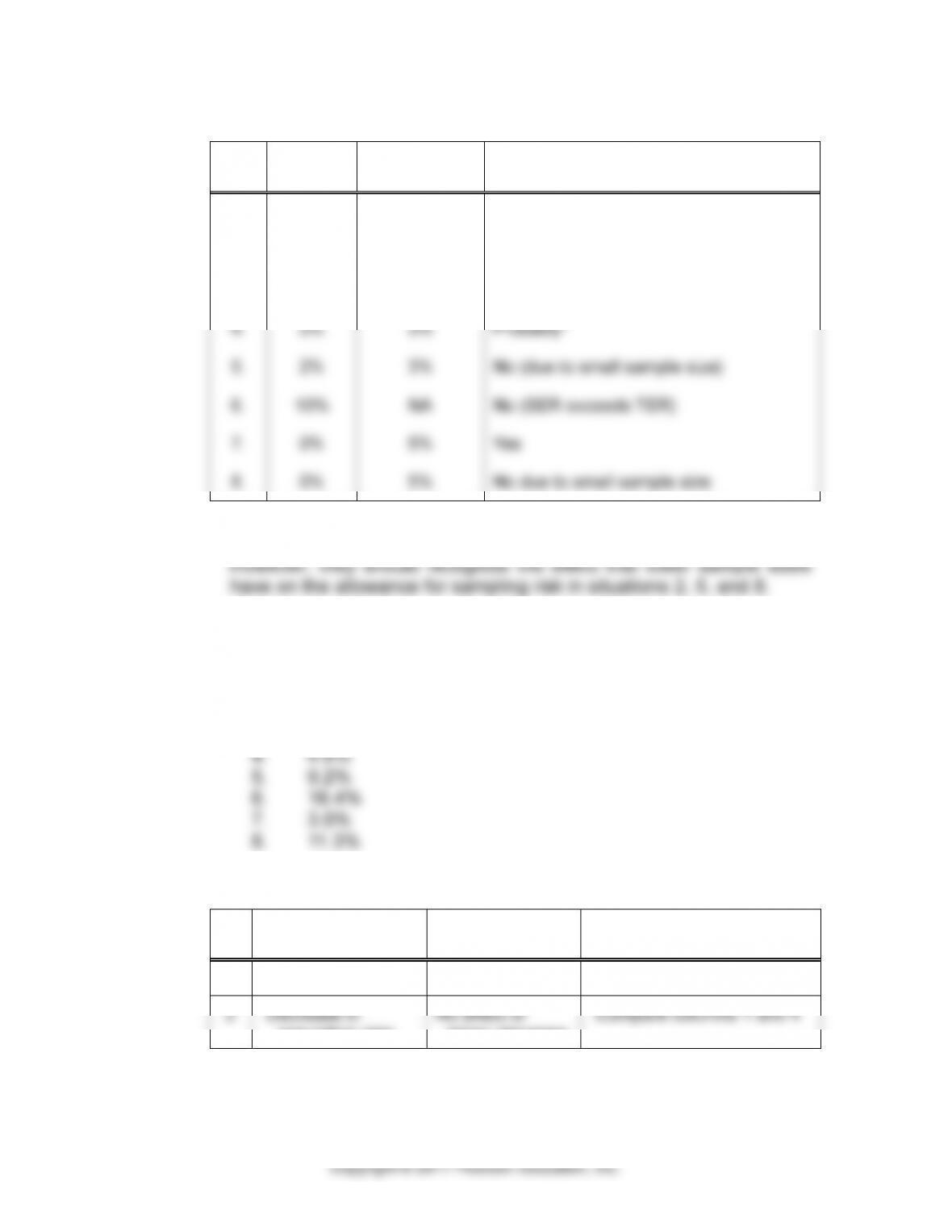

15-31 a.

SER

TER-SER

ALLOWANCE FOR SAMPLING

RISK SUFFICIENT?

1.

2%

3%

Probably*

2.

2%

3%

No (due to smaller sample size)*

3.

2%

3%

Yes

4.

2%

3%

Probably*

5.

2%

3%

No (due to small sample size)

6.

10%

NA

No (SER exceeds TER)

7.

0%

5%

Yes

8.

0%

5%

No due to small sample size

* Students’ answers as to whether the calculated allowance for

sampling risk is sufficient will vary, depending on their judgment.

b. Using the attributes sampling table in Table 15-9, the CUERs for

columns 1-8 are:

1. 4.6%

2. 6.2%

3. 4.0%

c.

CHANGE IN

FACTORS

EFFECT ON

CUER

ILLUSTRATIONS IN PART

a. or b.

1

Decrease in ARO

Increase

Compare columns 3 and 4

2

Decrease in

population size

No effect or

minor decrease

Compare columns 1 and 4

15-15

15-31 (continued)

CHANGE IN

FACTORS

EFFECT ON

CUER

ILLUSTRATIONS IN

PART a. or b.

3

Decrease in

sample size

Increase

Compare columns 4 and 5

(both sample exception

rates are 2%)

4

Decrease in the

number of

exceptions in the

sample

Decrease

Compare columns 6 and 7

even though the population in column 1 was 10 times larger.

e. The CUER represents the results of the actual sample whereas

the TER represents what the auditor will allow. They must be

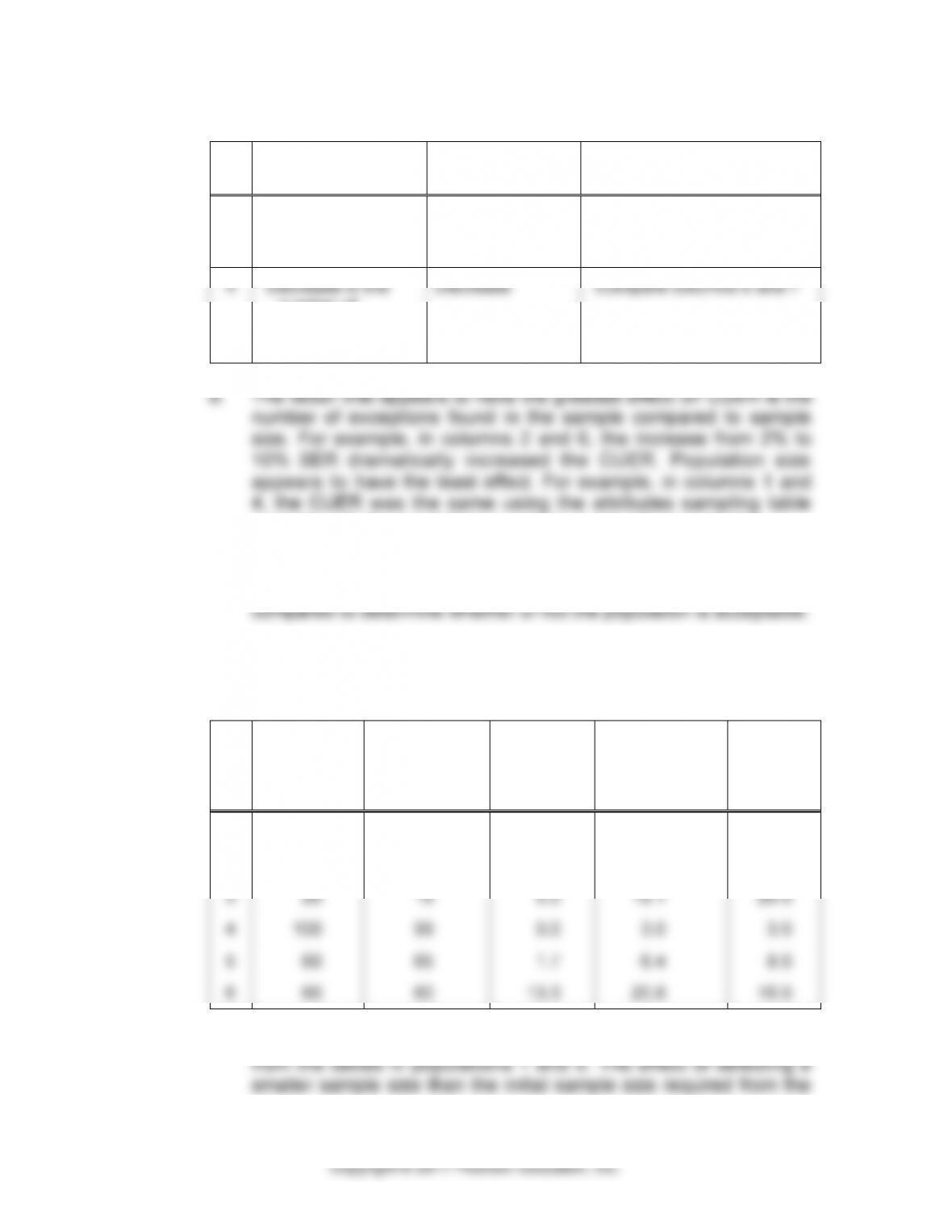

15-32 a. The sample sizes and CUERs are shown in the following table:

and

b.

ACTUAL

SAMPLE

SIZE

INITIAL

SAMPLE

SIZE FROM

TABLE 15-8

SER

CUER FROM

TABLE 15-9

TER

1

100

127

2.0%

6.2%

6.0%

2

100

93

4.0

9.0

5.0

3

20

18

5.0

18.1

20.0

4

100

99

0.0

3.0

3.0

5

60

65

1.7

6.4

8.0

6

60

60

13.3

20.8

15.0

a. The auditor selected a sample size smaller than that determined

15-16

15-32 (continued)

table is the increased likelihood of having the CUER exceed the

TER. If a larger sample size is selected, the result may be a sample

b. The SER and CUER are shown in columns 4 and 5 in the

c. The population results are unacceptable for populations 1, 2, and

6. In each of those cases, the CUER exceeds TER.

The auditor’s options are to change TER or ARO, increase

sample size, or perform other substantive tests to determine

whether there are actually material misstatements in the population.

d. Analysis of exceptions is necessary even when the population is

acceptable because the auditor wants to determine the nature and

e.

TERM

NATURE OF TERM

1. Estimated population exception

rate

Nonstatistical estimate made

by auditor

2. Tolerable exception rate

Audit decision

3. Acceptable risk of overreliance

Audit decision

4. Actual sample size

Audit decision (determined by

other audit decisions)

5. Actual number of exceptions

in the sample

Sample result

6. Sample exception rate

Sample result

7. Computed upper exception

rate

Statistical conclusion about

the population

15-17

Copyright © 2017 Pearson Education, Inc.

15-33 a. Based on the given ARO of 5% (confidence level of 95%), a

CUER of 7.92% indicates the auditor can conclude that the

exception rate in the population is no greater than 7.92% with a

5% risk of the exception rate exceeding 7.92%. Stated differently,

the auditor is 95% confident that the population exception rate

does not exceed 7.92%.

b. Given that Annie established a tolerable exception rate (TER) of

if she believes that the sample tested was not

representative of the population and that exceptions are

not expected in the expanded sample.

3. Revise assessed control risk upward. This is likely to

increase substantive procedures. Revising assessed

additional substantive procedures are possible.

4. Disclose the information to management. This action

covered by the temporary employee. In expanding the sample, she

could test additional transactions occurring outside the time period,

and assuming zero exceptions are identified in the expanded

sample and the CUER is less than TER, she could conclude

each.

15-18

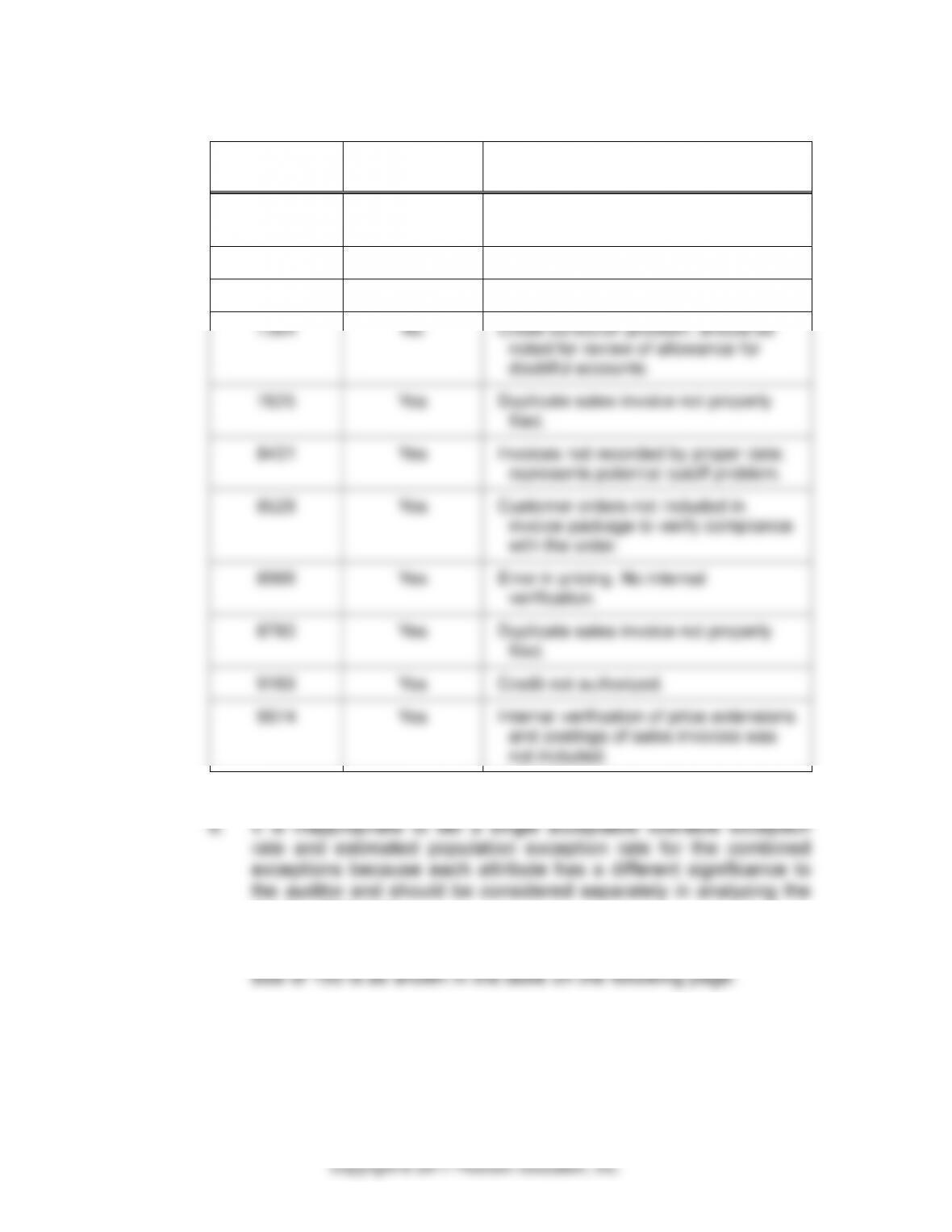

15-34 a. The following shows which are exceptions and why:

INVOICE

NUMBER

EXCEPTION?

TYPE OF EXCEPTION

5028

No

Error was detected and corrected by

client.

6791

No

Sales invoice was voided.

6810

Yes

Proof of shipment not presented.

7364

No

Credit collection problem; should be

noted for review of allowance for

doubtful accounts.

7625

Yes

Duplicate sales invoice not properly

filed.

8431

Yes

Invoices not recorded by proper date;

represents potential cutoff problem.

8528

Yes

Customer orders not included in

invoice package to verify compliance

with the order.

8566

Yes

Error in pricing. No internal

verification.

8780

Yes

Duplicate sales invoice not properly

filed.

9169

Yes

Credit not authorized.

9974

Yes

Internal verification of price extensions

and postings of sales invoices was

not included.

results of the test.

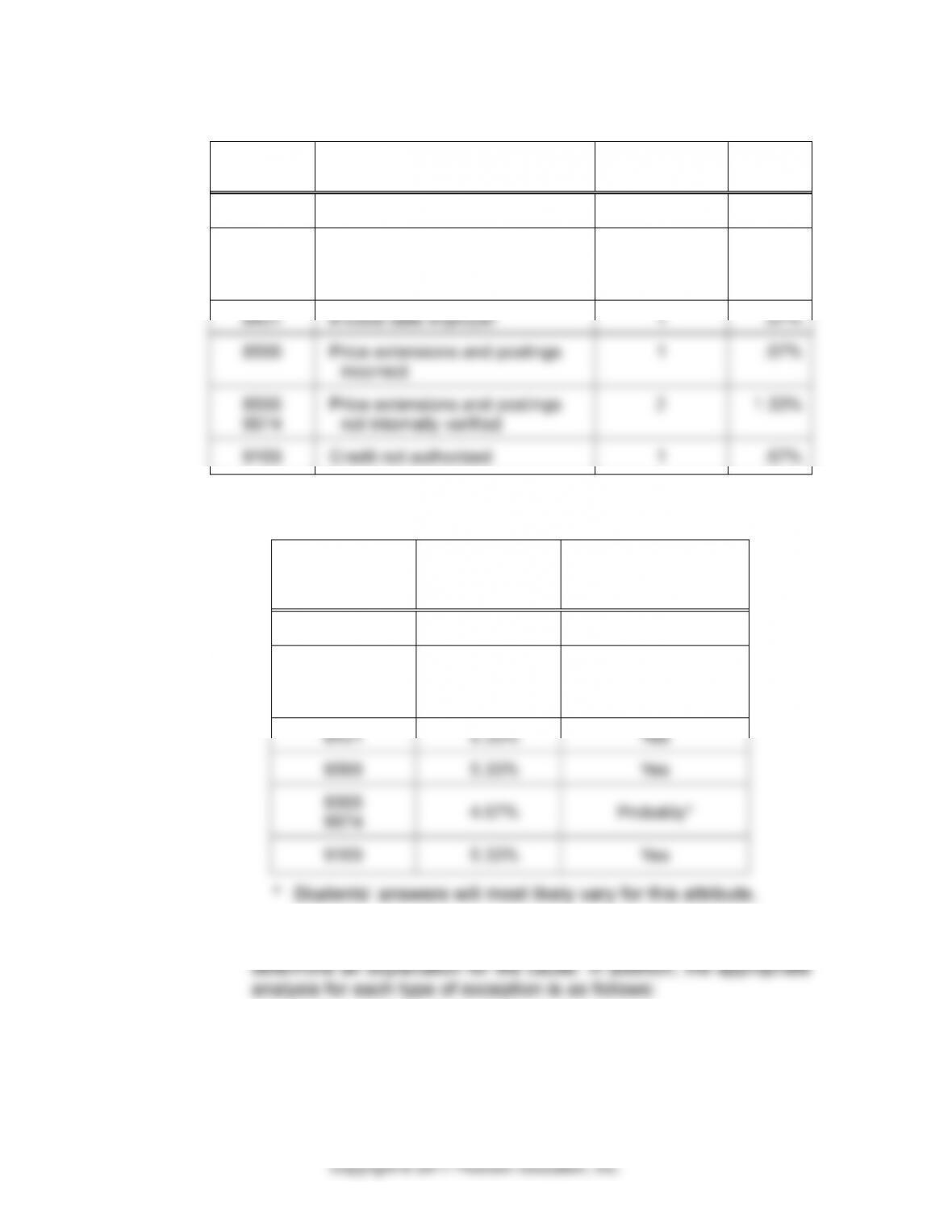

c. The SER assuming a 5% ARO for each attribute and a sample

15-19

15-34 (continued)

INVOICE

NUMBER

DESCRIPTION OF ATTRIBUTE

NUMBER OF

EXCEPTIONS

SER

6810

Shipping document not located

1

.67%

7625

8528

8780

Duplicate sales invoice/

customer order not located

3

2.00%

8431

Invoice date improper

1

.67%

8566

Price extensions and postings

incorrect

1

.67%

8566

9974

Price extensions and postings

not internally verified

2

1.33%

9169

Credit not authorized

1

.67%

d.

INVOICE

NUMBER

TER-SER

ALLOWANCE FOR

SAMPLING RISK

SUFFICIENT?

6810

5.33%

Yes

7625

8780

8528

4.0%

Probably*

8431

5.33%

Yes

8566

5.33%

Yes

8566

9974

4.67%

Probably*

9169

5.33%

Yes

* Students’ answers will most likely vary for this attribute.

e. For each exception, the auditor should check with the controller to