The computer file used for recording payroll transactions for each employee and

maintaining total wages paid for the year to date is the

A) payroll transaction file.

B) payroll master file.

C) payroll bank account reconciliation.

D) payroll tax returns.

The auditor generally decides whether the inventory count can be taken before year-end

primarily on the basis of

A) audit efficiency.

B) accuracy of the perpetual inventory master files.

C) client convenience.

D) audit staff availability.

A restriction on the scope of the auditor’s examination requires

A) a qualifying paragraph to be included in the introduction.

B) a qualifying paragraph preceding the opinion paragraph.

C) a disclaimer opinion.

D) a basis for a qualified opinion paragraph.

Which of the following is an accurate statement regarding nonexistent employees?

A) In order to prevent this type of fraud, the foreman should distribute the paychecks

and approve the time cards.

B) Records for all terminated employees should be destroyed to prevent this type of

fraud.

C) The person committing this type of fraud is generally the CEO or CFO of the

company.

D) This type of fraud often results from the continuance of an employee on the payroll

after the employee has been terminated.

The most reliable evidence from confirmations is obtained when they are sent

A) as close to the balance sheet date as possible.

B) at various times throughout the year to different segments of the sample, so that the

entire sample is representative of account balances scattered throughout the year.

C) several months before the year-end, so the auditor will have adequate time to

perform alternate procedures if they are required.

D) at various times throughout the year to the same group in the sample, so that the

sample will not have a time bias.

Which of the following best expresses the understanding of the terms of the

engagement that exist between the client and the CPA firm?

A) Management asserts there are no errors, material or immaterial, in the general

ledger.

B) Auditors assert that the primary audit goal is audit efficiency.

C) Auditors assert that their primary responsibility is to plan and perform the audit in

order to provide reasonable assurance as to the detection of material misstatement due

to error or fraud.

D) Management asserts that they will provide the auditor with a risk assessment as to

material misstatements due to errors or fraud in the company’s financial statements.

Which of the following is incorrect concerning scope limitations?

A) If client imposed, the auditor should be concerned about the client trying to prevent

discovery of a material misstatement.

B) An unqualified opinion can result if auditors can perform alternative procedures and

are satisfied that the information is fairly stated.

C) The most common circumstance imposed scope restriction is due to the client

changing their auditors.

D) The most common circumstance imposed scope limitation is when the auditor is

appointed after the balance sheet date.

Improperly classifying a fixed asset by recording the amount in the repairs and

maintenance expense account will have an effect on which of the following financial

statements until the asset would normally have been depreciated?

A) the balance sheet

B) the income statement

C) the cash flow statement

D) both the income statement and the balance sheet

The standard bank confirmation form has been agreed upon by the

A) SEC and FASB.

B) AICPA and the SEC.

C) SEC and the American Bankers’ Association.

D) AICPA and the American Bankers’ Association.

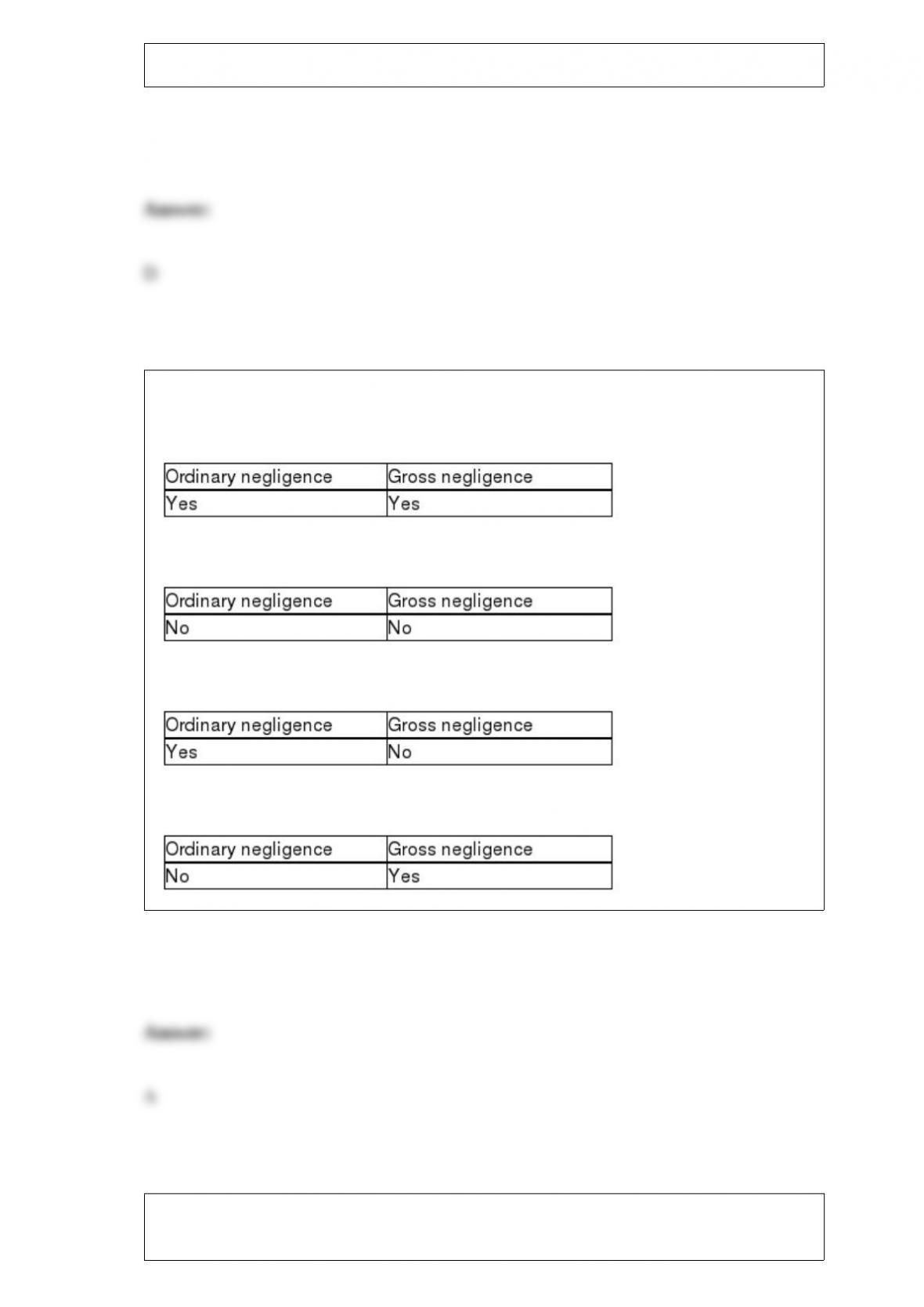

Auditors may be liable to their clients if they are found guilty of

A)

B)

C)

D)

Which of the following may represent the biggest challenge smaller public companies

and nonpublic companies face in implementing effective internal control?

A) a lack of competent, trustworthy personnel

B) no clear lines of authority

C) no adequate separation of duties

D) a lack of adequate documents and records

While the Foreign Corrupt Practices Act of 1977 remains in effect, its internal control

provisions have been largely superseded by which of the following?

A) Sarbanes-Oxley Act of 2002

B) Racketeer Influenced and Corrupt Organization Act

C) Federal False Statements Statute

D) Federal Mail Fraud Statute

The auditing standards of the Yellow Book are consistent with the ten generally

accepted auditing standards of the AICPA. There are, however, important

additions/modifications in the Yellow Book. For example, the Yellow Book recognizes

that materiality and risk are lower due to the nature of the government enterprise.

Discuss the other additions/modifications.

The use of unobservable inputs such as a pricing model or discounted cash flow is an

example of a level ________ estimate.

A) 1

B) 2

C) 3

D) 1 and 3

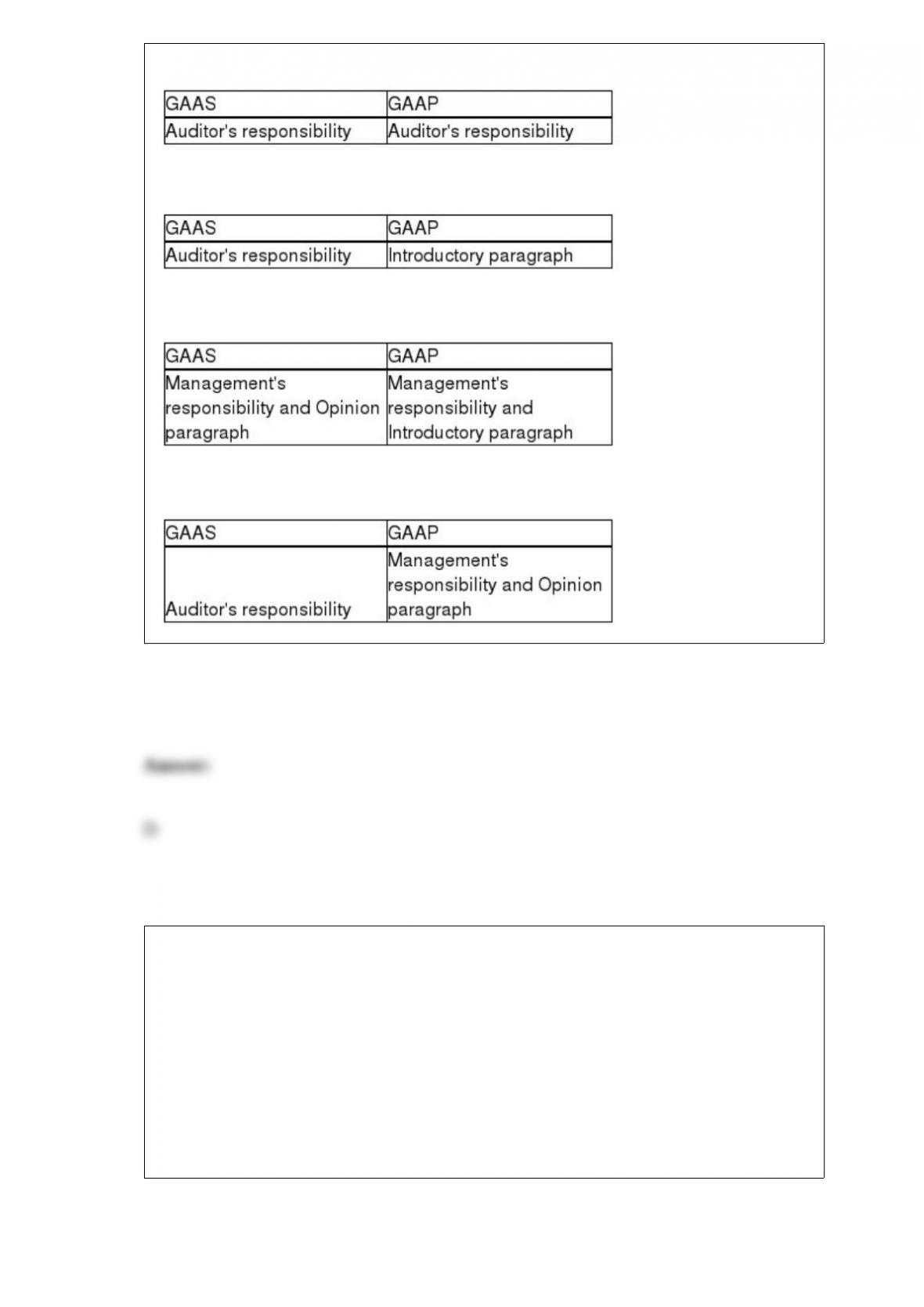

The standard audit report for nonpublic entities refers to GAAS and GAAP in which

sections?

A)

B)

C)

D)

Which of the following explanations might satisfy an auditor who discovers significant

debits to an accumulated depreciation account?

A) Extraordinary repairs have lengthened the life of an asset.

B) Prior years’ depreciation charges were erroneously understated.

C) A reserve for possible loss on retirement has been recorded.

D) An asset has been recorded at its fair value.

The auditor is testing for unrecorded retirements/disposals of equipment. Which of the

following audit procedures would the auditor most likely use?

A) Select items from the fixed asset master file and then physically locate them.

B) Examine the repairs and maintenance amount for large debits.

C) Compare current year’s depreciation expense with the previous year’s depreciation

expense.

D) Trace acquisition documents to the fixed asset master file.

Which of the following is most reliable for verifying the correct balance of accounts

payable?

A) vendors’ invoices

B) vendors’ statements

C) confirmations

D) bills of lading

When do most companies record sales returns and allowances?

A) during the month in which the sale occurs

B) during the accounting period in which the return occurs

C) whenever the customer contacts the company regarding the credit

D) during the month after the sale occurs

You are reviewing sales to discover cutoff problems. If the client’s policy is to record

sales when title to the merchandise passes to the buyer, then the books and records

would contain errors if the December 31 entries were for sales recorded

A) before the merchandise was shipped.

B) at the time the merchandise was shipped.

C) several days subsequent to shipment.

D) at a time after the point at which title passed.

A CPA who has been engaged to audit financial statements that were prepared on a cash

basis

A) must ascertain that there is proper disclosure of the fact that the cash basis has been

used.

B) may not be associated with such statements which are not in accordance with

generally accepted accounting principles.

C) must render a qualified report explaining the departure from generally accepted

accounting principles in the opinion paragraph.

D) must restate the financial statements on an accrual basis and then render the standard

(short-form) report.

When should auditors not perform alternative procedures in testing the accounts

receivable balance?

A) when customers do not return positive confirmation requests

B) when customers do not return negative confirmation requests

C) when confirmations are deemed to be ineffective as an audit procedure

D) when confirmations are too costly to use

Which of the following is ordinarily designed to detect material dollar errors on the

financial statements?

A) tests of controls

B) analytical review procedures

C) computer controls

D) tests of details of balances

A weak internal control system allows a department supervisor to “clock in” for a

fictitious employee and then approve the employee’s time card at the end of the pay

period. This fraud would be detected if other controls were in place, such as having an

independent party

A) distribute paychecks.

B) recompute hours worked from time cards.

C) foot the payroll journal and trace postings to the general ledger and the payroll

master file.

D) compare the date of the recorded check in the payroll journal with the date on the

canceled checks and time cards.

When the client fails to include information that is necessary for the fair presentation of

financial statements in the body of the statements or in the footnotes,

A) it is the auditor’s responsibility to present the information in the audit report.

B) the auditor should issue a qualified or an adverse opinion.

C) the qualification is put in an added paragraph preceding the opinion.

D) all of the above

When the auditor compares the cancelled check or direct deposit with the payroll

journal for amount, they are concerned with the transaction-related audit objective of

A) occurrence.

B) accuracy.

C) classification.

D) timing.

Analytical procedures

A) are only done during the planning of the audit and when performing detailed tests.

B) performed during the detailed testing phase are done before tests of details of

balances.

C) performed during the detailed testing phase are done before the balance sheet date.

D) are performed only on accounts receivable, not on the entire sales and collection

cycle.

Which of the following is not explicitly stated in the standard unmodified opinion audit

report?

A) The financial statements are the responsibility of management.

B) The audit was conducted in accordance with generally accepted accounting

principles.

C) The auditors believe that the audit evidence provides a reasonable basis for their

opinion.

D) An audit includes assessing the accounting estimates used.

In the fraud triangle, fraudulent financial reporting and misappropriation of assets

A) share little in common.

B) share most of the same risk factors.

C) share the same three conditions of the fraud triangle.

D) share most of the same conditions. of the fraud triangle.

Which of the following is true regarding the auditor’s opinion on the effectiveness of

internal control?

A) The auditor is attesting to the effectiveness of internal controls as of the end of the

fiscal year.

B) If the client remedies a material weakness before the end of the fiscal year, the

auditor must still issue a qualified opinion or a disclaimer of opinion.

C) A scope limitation requires the auditor to issues an adverse opinion.

D) Section 404 requires that the auditor design the audit to detect all deficiencies in

internal control.

The laws that have been developed through court decisions are called

A) common laws.

B) criminal laws.

C) statutory laws.

D) civil laws.

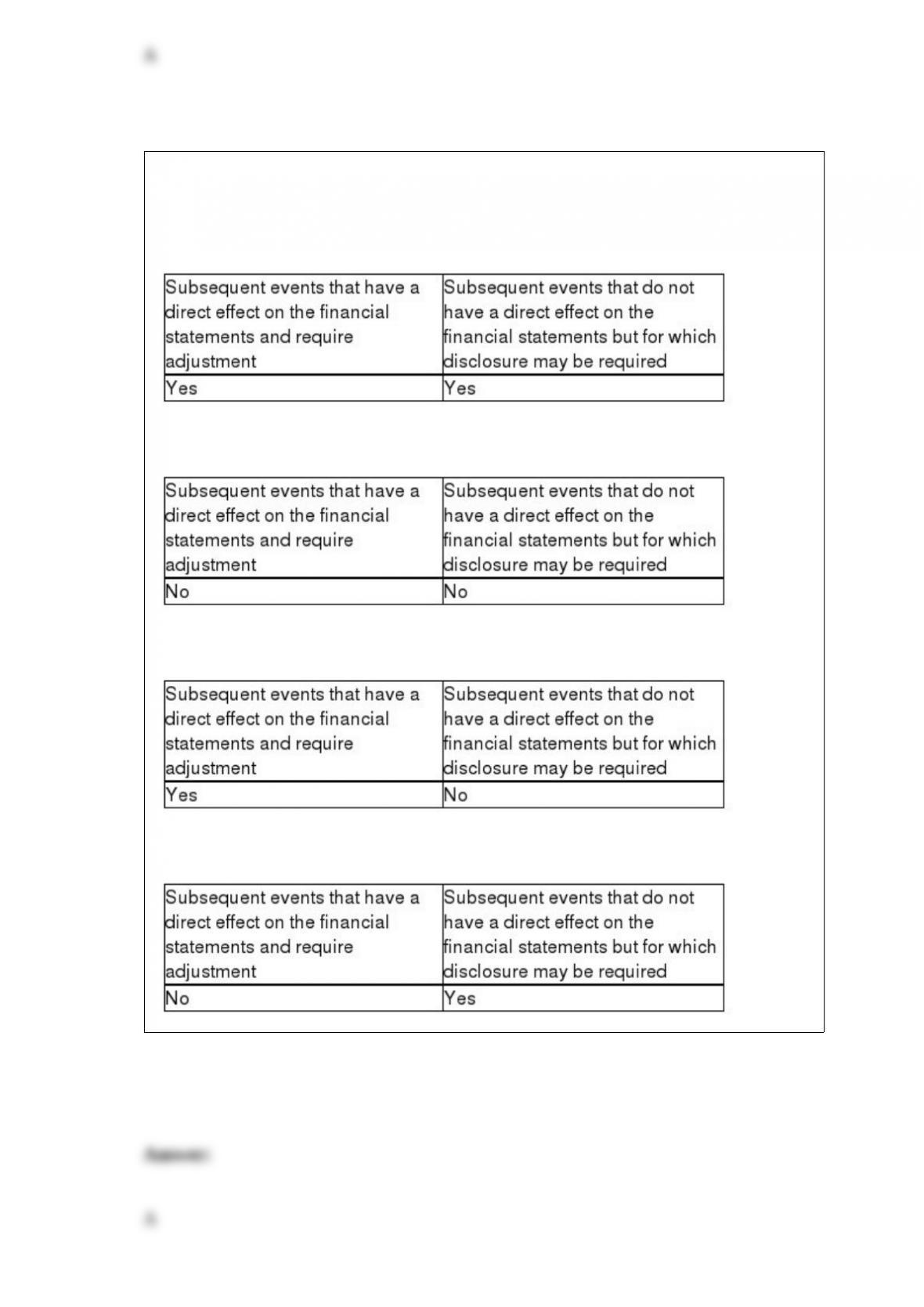

Which type of subsequent event requires consideration by management and evaluation

by the auditor?

A)

B)

C)

D)

Auditing standards require the auditor to ________ other information included in

annual reports pertaining directly to the financial statements.

A) audit

B) express an opinion on

C) read

D) analyze

Which department should be authorized to add and delete employees from the payroll

or change pay rates and deductions?

A) the supervising department

B) the accounting department

C) the human resources department

D) the treasurer’s department