20–24 A flowchart of steps for each type of test is given below (requirements

a., b., and c.):

TESTS OF CONTROLS

OR SUBSTANTIVE TESTS

OF TRANSACTIONS

TESTS OF DETAILS

OF BALANCES

5

4

2

7

9

8

6

3

1

20–25

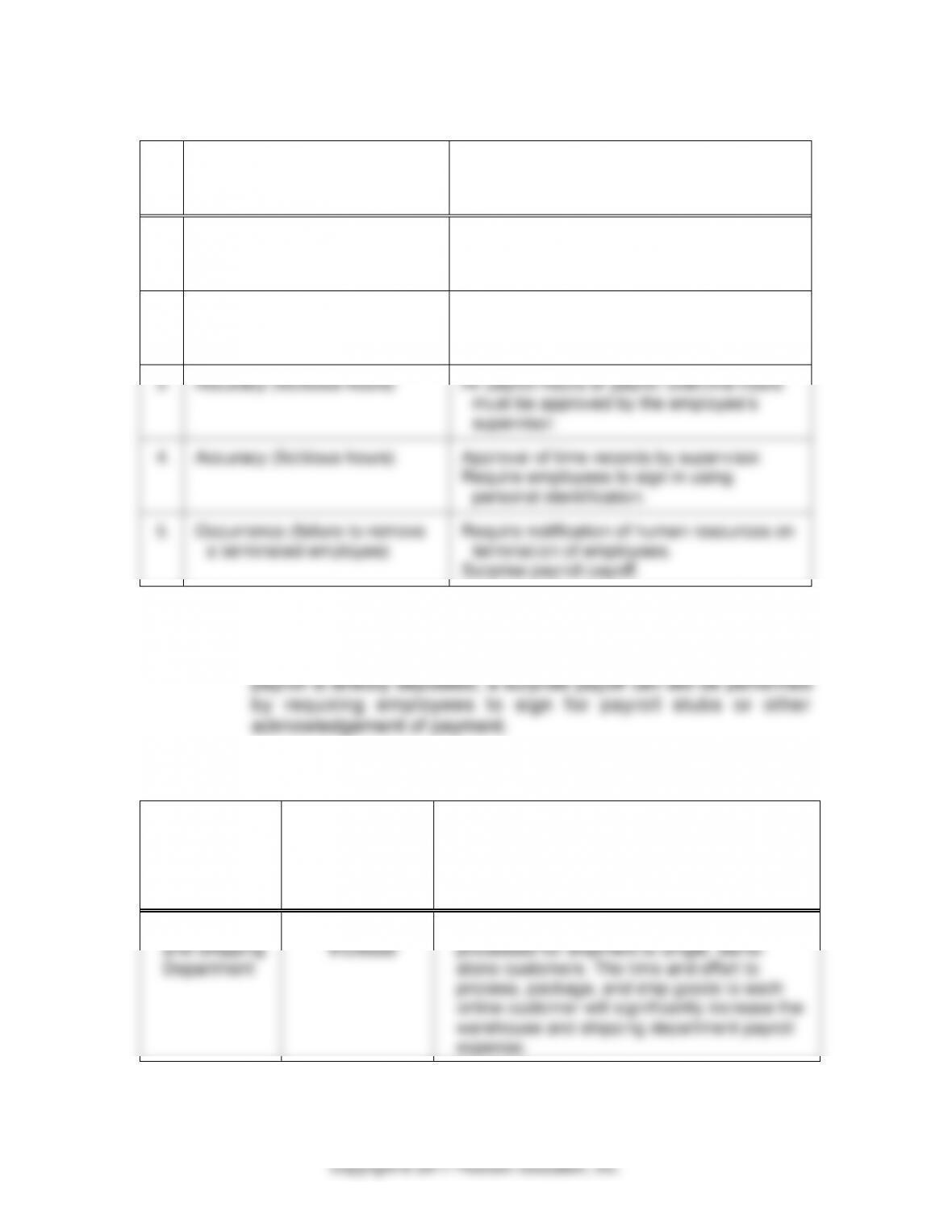

a.

INTERNAL

CONTROL DEFICIENCY

b.

TYPE OF MISSTATEMENT

1.

The foreman should not hire

employees.

The foreman may hire unqualified

employees, friends, or possibly a fictitious

person to be paid through the payroll

system.

2.

The foremen should not

recommend wages for

employees.

The foreman may provide inappropriate pay

rates or pay rates that are split between

an employee and the foreman.

3.

Time cards should not be left in

a box that employees have

access to.

Employees, including the foreman, can take

extra time cards and clock in for other

employees or fictitious employees.

4.

The foreman collects and

approves the time cards as

well as the duties described

in 1–3. (Note: It is appropriate

for the foreman to approve

times cards if he has none of

the other duties described in

1–3.)

The foreman can include fictitious time

cards for check preparation.

5.

There is no internal verification

of the payroll clerk’s input of

names or hours into the

payroll system.

The payroll clerk can make mistakes

entering the hours or names.

20–25 (continued)

a.

INTERNAL

CONTROL DEFICIENCY

b.

TYPE OF MISSTATEMENT

6.

The controller compares two

output records and fails to

compare the output to any

input records.

The controller will not find any existing

mistakes made by the payroll clerk.

7.

The foreman receives the

payroll checks for distribution.

The foreman can keep checks for which he

has submitted time cards for nonexistent

employees.

8.

The foreman mails checks to

absent employees.

Nonexistent or former employees who had

someone else prepare their time cards will

receive a check in the mail.

9.

The controller hires and

approves wages for salaried

employees and signs their

checks.

The controller can submit information for a

nonexistent employee, open a checking

account in the person’s name and receive

the direct deposit. She can also submit

the improper salary rate to the payroll

clerk and split the payment with the

employee.

10.

The controller has sole access

to pay rates.

The controller can include any pay rates

she desires, for herself or others,

including fictitious employees and friends

who will split the amounts with her.

11.

The payroll clerk can add

names to the payroll records.

The payroll clerk can add fictitious names

for either salaried or hourly employees.

She can set up a checking account in the

same manner discussed in 9.

12.

An accounting clerk does the

bank reconciliation each

month.

The person is unlikely to be qualified to

do quality bank reconciliation and will

thereby be unlikely to find the frauds

included previously.

20–26

a.

TRANSACTION–RELATED

AUDIT OBJECTIVE NOT MET

b.

CONTROL EFFECTIVE IN PREVENTING

OR DETECTING MISAPPROPRIATION

1.

Accuracy (unauthorized pay

rates)

Only the human resource function, which is

separate from the payroll function, can

change employee pay rates.

2.

Occurrence (fictitious

employee)

Only the human resource function, which is

separate from the payroll function, can

add employees to payroll.

3.

Accuracy (fictitious hours)

All payroll hours or payroll overtime hours

must be approved by the employee’s

supervisor.

4.

Accuracy (fictitious hours)

Approval of time records by supervisor.

Require employees to sign in using

personal identification.

5.

Occurrence (failure to remove

a terminated employee)

Require notification of human resources on

termination of employees.

Surprise payroll payoff.

c. The surprise payroll payoff is effective in detecting fictitious employees

that have been placed on the payroll, or terminated employees

that were not properly removed from the payroll (occurrence). If

20–27

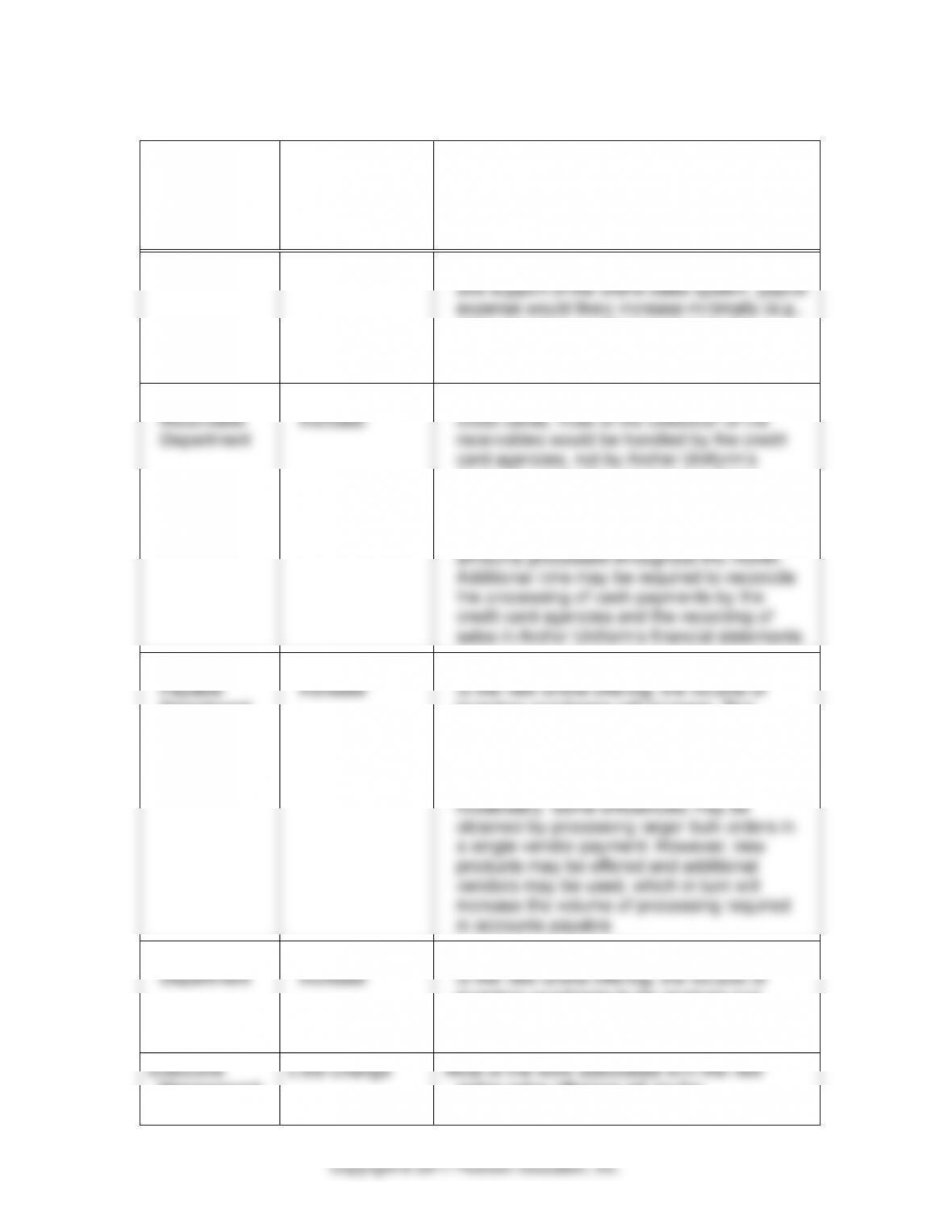

DEPARTMENT

EXTENT

OF INCREASE

OR DECREASE

IN PAYROLL

EXPENSE

EXPLANATION FOR

EXPECTED CHANGE IN

DEPARTMENT’S PAYROLL EXPENSE

Warehouse

and Shipping

Department

Extensive

Increase

Each online sale must be individually

processed for shipment to single, stand–

alone customers. The time and effort to

process, package, and ship goods to each

online customer will significantly increase the

warehouse and shipping department payroll

expense.

20–27 (continued)

DEPARTMENT

EXTENT

OF INCREASE

OR DECREASE

IN PAYROLL

EXPENSE

EXPLANATION FOR

EXPECTED CHANGE IN

DEPARTMENT’S PAYROLL EXPENSE

IT Department

Little Change

Because the company outsourced the creation

and support of the online sales system, payroll

expense would likely increase minimally (e.g.,

some increase would occur despite the

outsourcing). However, consulting expense

would be expected to increase extensively.

Accounts

Receivable

Department

Little to Moderate

Increase

Because online sales are applied to customer

credit cards, most of the collection of the

receivables would be handled by the credit

card agencies, not by Archer Uniform’s

accounts receivable department. Some

increase in payroll expense may occur, if

there are disputes between Archer Uniforms

and the credit card agencies over the

amounts processed throughout the month.

Additional time may be required to reconcile

the processing of cash payments by the

credit card agencies and the recording of

sales in Archer Uniform’s financial statements.

Accounts

Payable

Department

Moderate

Increase

Assuming total sales significantly increase due

to the new online offering, the volume of

inventory purchases will increase. This

increase in inventory purchasing will result in

an increase in vendor payments to be

processed. Thus, payroll expense for the

accounts payable department may increase

moderately. Some efficiencies may be

obtained by processing larger bulk orders in

a single vendor payment. However, new

products may be offered and additional

vendors may be used, which in turn will

increase the volume of processing required

in accounts payable.

Receiving

to the new online offering, the volume of

Extensive

Assuming total sales significantly increase due

inventory purchases to be received and

correspondingly increase.

Executive

Management

Little Change

Most of the work associated with the new

online sales offerings will be the

20–27 (continued)

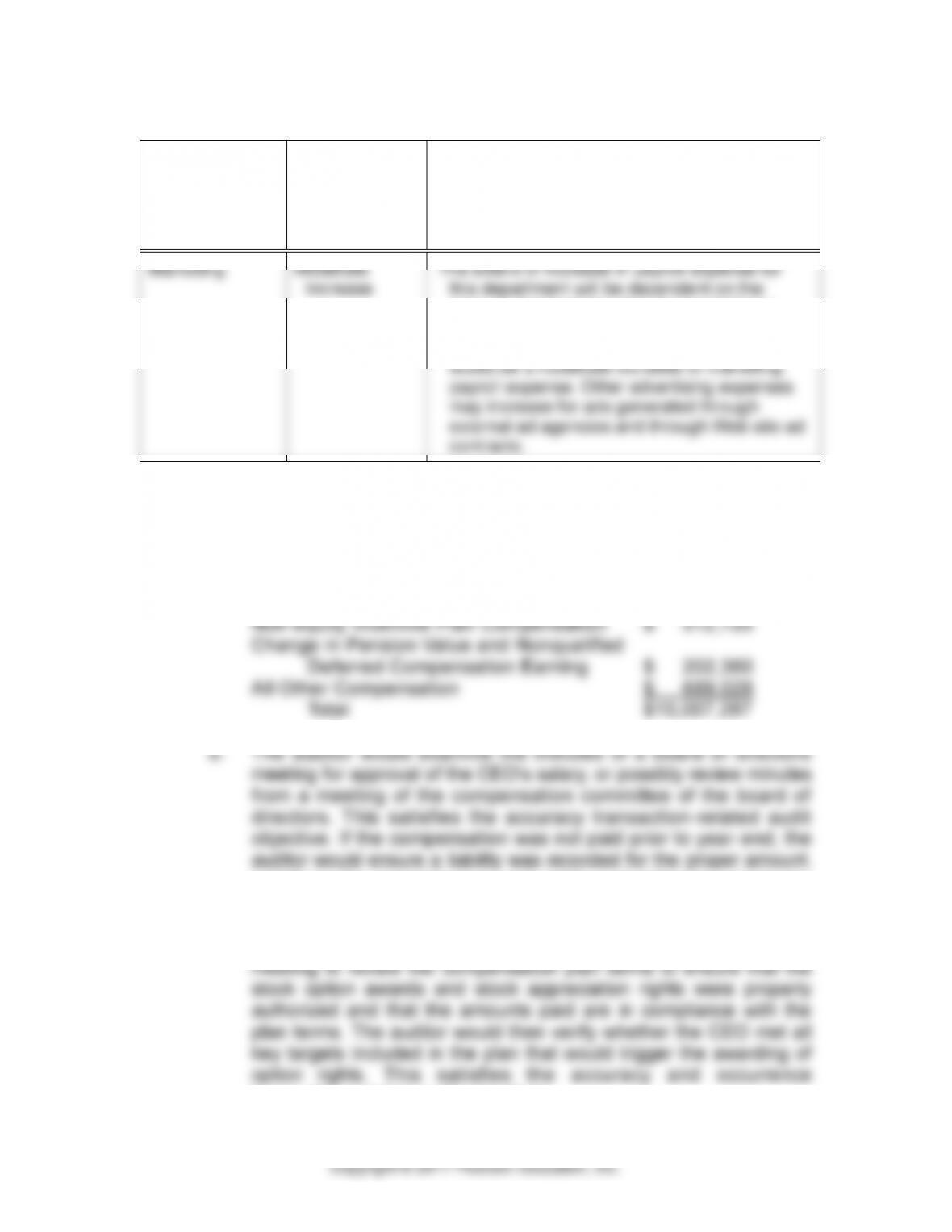

DEPARTMENT

EXTENT OF

INCREASE OR

DECREASE IN

PAYROLL

EXPENSE

EXPLANATION FOR

EXPECTED CHANGE IN

DEPARTMENT’S PAYROLL EXPENSE

Marketing

Moderate

Increase

The extent of increase in payroll expense for

this department will be dependent on the

amount of advertising that Archer Uniforms

creates to promote its new Web site.

Assuming some advertising is created, there

would be a moderate increase in marketing

payroll expense. Other advertising expenses

may increase for ads generated through

external ad agencies and through Web site ad

contracts.

20–28 a. The compensation components for the David C. Novak, Chairman

and CEO, for 2014 consists of the following:

Salary $ 1,450,000

Stock Awards $ 1,925,037

Option/SAR Awards $ 5,228,142

satisfying the completeness and rights and obligations balance–

related audit objectives.

c. The auditor would examine the minutes of a board of directors

transaction–related audit objectives.

20–16

20–28 (continued)

methodologies used by the company to value the awards.

According to Note 14 in the consolidated financial statements for

the year ended December 27, 2014, the company estimates the

fair value of each stock option and SAR award as of the date of

compensation specialist to assist with the examination of the stock

option and SAR computations.

e. Presentation and disclosure audit objectives are important for

financial statements as well as in proxy statements for publicly

traded companies.

Case

following:

Personnel records

Deduction authorization forms

Rate authorization forms

Time cards and job time tickets

20–29 (continued)

form is not a problem, as long as the service bureau has

adequate backup and recovery controls.

The above analysis reflects the fact that Leggert’s internal

controls in the payroll area are generally good. There is good

and reports are comprehensive and well–designed.

The only potential deficiency in internal control is that errors

b.

PAYROLL

TRANSACTION–

RELATED

AUDIT OBJECTIVE

PROCEDURES

TYPE OF

PROCEDURE

1. Recorded payroll

payments are for

work performed by

existing employees

(occurrence).

a. Observe existence of

personnel files in president’s

care.

b. Observe use of time clock

and control of time cards by

clerk.

c. Examine time cards for

president’s approval.

d. Observe distribution of

payroll checks by president.

e. Examine cancelled checks

for proper endorsement.

f. Compare cancelled checks

with personnel records.

g. Examine cancelled check for

president’s signature.

Test of control

Test of control

Test of control

Test of control

Substantive test of

transactions

Substantive test of

transactions

Test of control

2. Existing payroll

transactions are

a. Account for the numerical

sequence of payroll checks.

Test of control and

substantive test of

20–29 (continued)

PAYROLL

TRANSACTION–

RELATED

AUDIT

OBJECTIVE

PROCEDURES

TYPE OF

PROCEDURE

3. Recorded payroll

transactions are for

the amount of time

actually worked

and at the proper

pay rate;

withholdings are

properly calculated

(accuracy).

a. Observe use of time clock

and control of time cards by

Clark.

b. Observe Clark rechecking

hours.

c. Recompute gross pay,

deductions, and net pay.

d. Trace rates and

authorizations to personnel

file.

e. Examine payroll journal or

listing for approval by Clark.

f. Compare rates in payroll

journal or listing with

personnel files to determine

that rate actually paid is

authorized.

Test of control

Test of control

Substantive test of

transactions

Substantive test of

transactions

Test of control

Substantive test of

transactions

4. Payroll

transactions are

properly classified

(classification).

a. Review chart of accounts.

b. Examine payroll journal or

listing for approval by Clark.

c. Compare classification with

chart of accounts or

procedures manual.

Test of control

Test of control

Substantive test of

transactions

5. Payroll

transactions are

recorded on the

correct dates

(timing).

a. Observe collection and

processing of time cards by

Clark.

b. Examine payroll journal or

listing for approval by Clark.

c. Observe posting of ledger by

Clark.

d. Observe preparation of

payroll bank reconciliation by

president.

e. Compare date of check

recorded in payroll journal

Test of control

Test of control

Test of control

Test of control

Substantive test of

transactions

20–29 (continued)

PAYROLL

TRANSACTION–

RELATED

AUDIT OBJECTIVE

PROCEDURES

TYPE OF

PROCEDURE

6. Payroll

transactions are

properly included in

the employee

earnings record;

they are properly

summarized

(posting and

summarization).

a. Observe re–adding of payroll

journal or listing and posting

by Clark.

b. Examine payroll journal or

listing for approval by Clark.

c. Observe posting of ledger by

Clark.

d. Trace postings from payroll

journal to general ledger.

Test of control

Test of control

Test of control

Substantive test of

transactions

c. Procedures in performance format:

d) Posting of general ledger.

2. Make observations of the following activities by the president:

a) Maintenance of personnel files.

activities:

4. Select a sample of payroll check numbers and:

c) Examine checks for proper endorsement.

d) Compare cancelled checks with personnel records.

listing and perform the following steps:

20–29 (continued)

and deductions.

c) Recompute gross pay, deductions, and net pay.

steps:

a) Examine payroll journal for approval by Clark.

b) Trace postings to general ledger.

d. A sampling data sheet follows. Note that this sampling data sheet

sizes will vary.

DESCRIPTION OF ATTRIBUTES

PLANNED AUDIT

INITIAL

SAMPLE

SIZE***

EPER*

TER**

ARO**

1. Payroll check number accounted

for

2. Payroll check signed by president

3. Time card approved by president

4. Time card hours agree with payroll

journal or listing

5. Personnel file is complete

6. Pay rate and deductions supported

by authorization

7. Gross pay, deductions, and net pay

correctly computed

0%

0%

1%

1%

0%

1%

0%

5%

4%

6%

6%

6%

4%

5%

5%

5%

5%

5%

5%

5%

5%

59

74

78

78

49

156

59

* These amounts are arbitrary to complete data sheet.

Information to determine actual appropriate amounts is not given in problem.

** These amounts are judgments and are not the only acceptable amounts.

*** Determined from attributes sampling tables.