Fraud is more prevalent in large businesses than small businesses and not-for-profit

organizations.

Statutory laws are laws that have been developed through court decisions rather than

through the U.S. Congress and other governmental units.

Sales returns and allowances are often ignored by auditors because they are often

immaterial.

Operations are approaches followed by the entity to achieve organizational objectives.

The ASB has revised its audit standards to converge with international standards.

ARIA measures the auditor’s desired assurance for an account balance.

Negative confirmations normally require a larger sample size than positive

confirmations.

The final step in the auditor’s decision process for audit reports is to write the audit

report.

Current professional auditing standards mandate the use of analytical procedures during

the testing phase of the audit.

The theft of cash can occur before receipts are entered in the records or after they are

entered in the records.

The auditor has a responsibility to notify law enforcement when fraud is suspected.

If auditors consider confirmations of accounts receivable to be ineffective evidence

because response rates will be inadequate or unreliable, they need not confirm accounts

receivable.

Benchmarking is one source of evaluation criteria for completing an operational audit.

Inherent risk is typically assessed at a low level for inventory due to the nature of the

asset.

The client may mail the bank confirmation requests if the auditor believes doing so will

increase the likelihood that the confirmation will be returned promptly.

Auditors often convince themselves that they only accept clients they can trust and who

have high integrity.

A vendor’s statement is unreliable and auditors rarely use it.

Management and the board of directors are responsible for setting the “tone at the top.”

An audit provides a guarantee that a material misstatement will not exist in the

financial statements.

The shareholders’ capital stock master file is used as the basis for the payment of

dividends and also acts as a check on the accuracy of the common stock balance in the

general ledger.

The type of audit evidence known as inquiry requires the auditor to obtain oral or

written information from the client in response to questions.

In some inventory systems, raw materials can be requisitioned by automated computer

software when raw materials reach a predetermined level.

Internal auditors are expected to provide value to the organization through improved

operational effectiveness.

An advantage of the principles of professional conduct in the Code of Professional

Conduct is that they are more easily enforced than are the specific rules of conduct.

An essential part of the auditor’s responsibility in auditing cash receipts is to identify

deficiencies in internal control that increase the likelihood of fraud.

Few large companies employ stock transfer agents, but small companies commonly do

so.

In an examination engagement for prospective financial statements, the CPA obtains

satisfaction as to the completeness and reasonableness of all the assumptions.

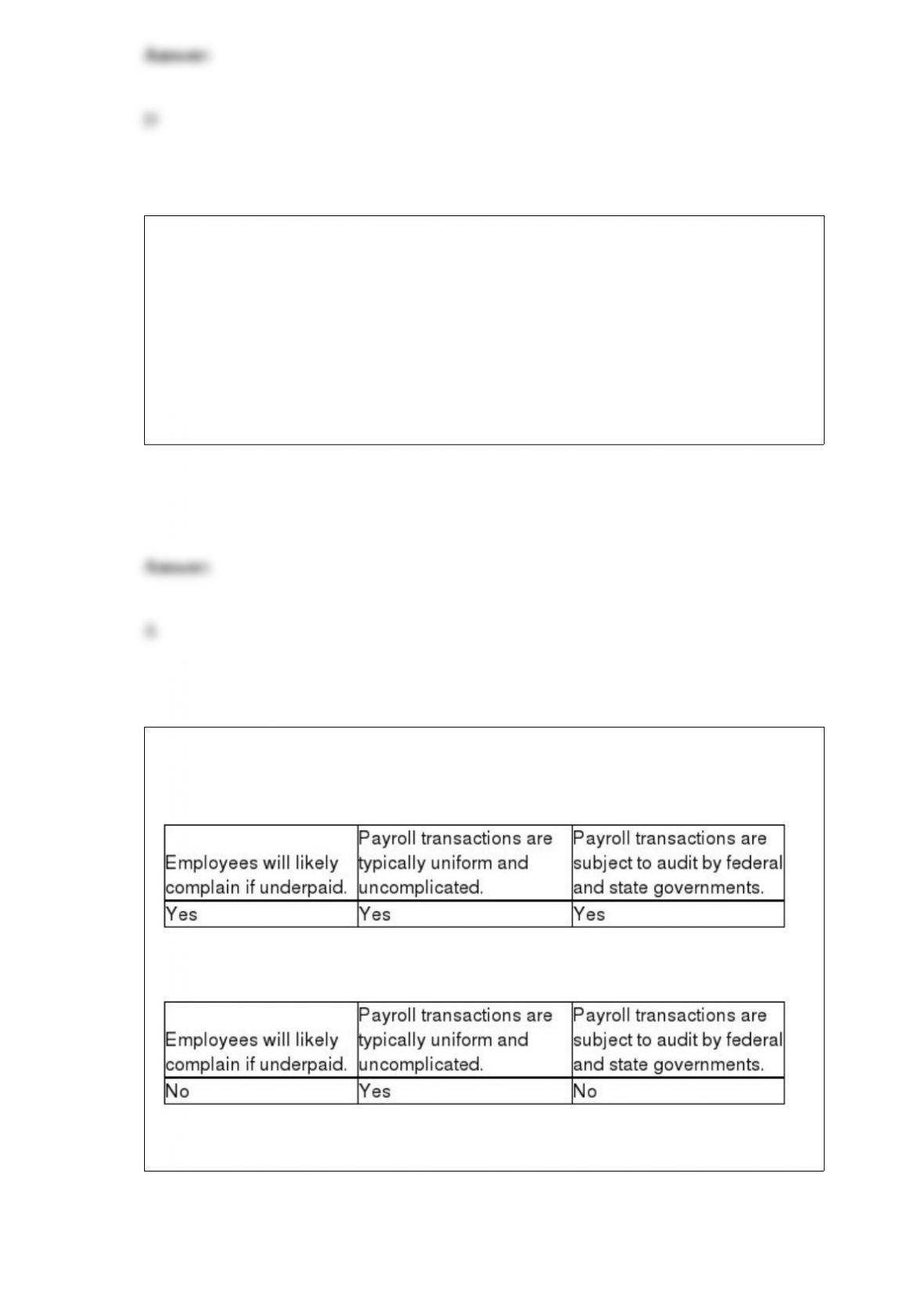

Hiring personnel initiates the payroll and personnel cycle.

The auditor should read the corporate minutes to obtain authorizations and other

information that is relevant to performing the audit.

When performing a preparation service, the CPA must issue a report and must be

independent.

In nonstatistical sampling, the calculated sampling error is the difference between the

tolerable exception rate and the sample exception rate.

The confirmations must be mailed by the auditor, but should contain the return address

of the client.

A CPA must meet continuing education requirements to maintain their license to

practice.

Most monetary misstatements of payroll are corrected by internal verification controls

or by the PCAOB.

A bill of lading is a special type of sales invoice used when goods are shipped interstate.

The date of the auditor’s report is indicative of the last day of the auditor’s responsibility

for the review of significant events occurring after the balance sheet date.

Which of the following does not describe a size category for a CPA firm?

A) Big Four national firms

B) Big Four international firms

C) local firms

D) national and regional firms

When assessing planned control risk for sales,

A) the key internal controls and deficiencies for sales will be the same for every

company.

B) the audit objectives for sales will differ from company to company.

C) a flowchart is required to help assess control risk for sales.

D) assessing control risk for sales is a highly subjective decision.

Who is responsible for setting the “tone at the top”?

A) management

B) PCAOB

C) audit committee

D) SEC

Audit tests of payroll are usually not extensive because

A)

B)

C)

D)

When should auditors generally assess a client’s ability to continue as a going concern?

A) upon completion of the audit

B) during the planning stages of the audit

C) throughout the entire audit process

D) during testing and completion phases of the audit

When dealing with the documentation of internal control,

A) in a narrative, most questions simply require a “yes” or “no” response.

B) questionnaires offer useful checklists to remind the auditor of the many different

types of internal controls that should exist.

C) questionnaires and flowcharts should not be used together.

D) flowcharts fail to show the segregation of duties in the company.

A(n) ________ is a computer resource deployment and procurement model that enables

an organization to obtain IT resources and applications from any location via an

Internet connection.

A) application service provider

B) firewall

C) cloud computing environment

D) local area network

When an auditor knows that an illegal act has occurred, she must

A) report it to the proper governmental authorities.

B) consider the effects on the financial statements, including the adequacy of

disclosure.

C) withdraw from the engagement.

D) issue an adverse opinion.

In testing for cutoff, the objective is to determine

A) whether all of the current period’s transactions are recorded.

B) whether transactions are recorded in the correct accounting period.

C) the proper cutoff between capitalizing and expensing expenditures.

D) the proper cutoff between disclosing items in footnotes or in account balances.

The test of details of balance procedure which requires the auditor to account for

unused inventory tag numbers to make sure none have been deleted is associated with

the audit objective of

A) accuracy.

B) existence.

C) detail tie-in.

D) completeness.

Which one of the following substantive analytical procedures would be most useful in

alerting the auditor to the possibility inventory and cost of goods sold being overstated

or understated?

A) Compare extended inventory value with that of previous years.

B) Compare unit costs of inventory with previous years.

C) Compare inventory turnover ratio with previous years.

D) Compare current year manufacturing costs with previous years.

The standards for preparation, compilation, and review engagements of financial

statements are the

A) AICPA’s Code of Professional Conduct.

B) Statements on Auditing Standards (SASs).

C) Statements of Standards on Attestation Engagements (SSAEs).

D) Statements on Standards for Accounting and Review Services (SSARS).

Which of the following is a correct relationship?

A) Acceptable audit risk and planned detection risk have an inverse relationship.

B) Control risk and planned detection risk have a direct relationship.

C) Planned detection risk and inherent risk have an inverse relationship.

D) All of the above are correct relationships.

The two most important qualities for an operational auditor are

A) personality and appearance.

B) independence and competence.

C) competence and technical training.

D) academic background and sufficient experience.

When an auditor believes that analytical procedures indicate a reasonable possibility of

misstatement, the auditor usually would

A)

B)

C)

D)

Based on audit evidence gathered and evaluated, an auditor decides to increase the

assessed level of control risk from that originally planned. To achieve an overall audit

risk level that is substantially the same as the planned audit risk level, the auditor would

A) increase materiality levels.

B) decrease detection risk.

C) decrease substantive testing.

D) increase inherent risk.

When using difference estimation, the precision interval is calculated by a statistical

formula.

Normally it may be unnecessary to examine supporting documentation for each

addition to property, plant, and equipment, but it would be customary to verify

A) all large transactions.

B) all unusual transactions.

C) a representative sample of typical additions.

D) all of the above.

Before making the final assessment of internal control at the end of an audit, the auditor

must

A)

B)

C)

D)

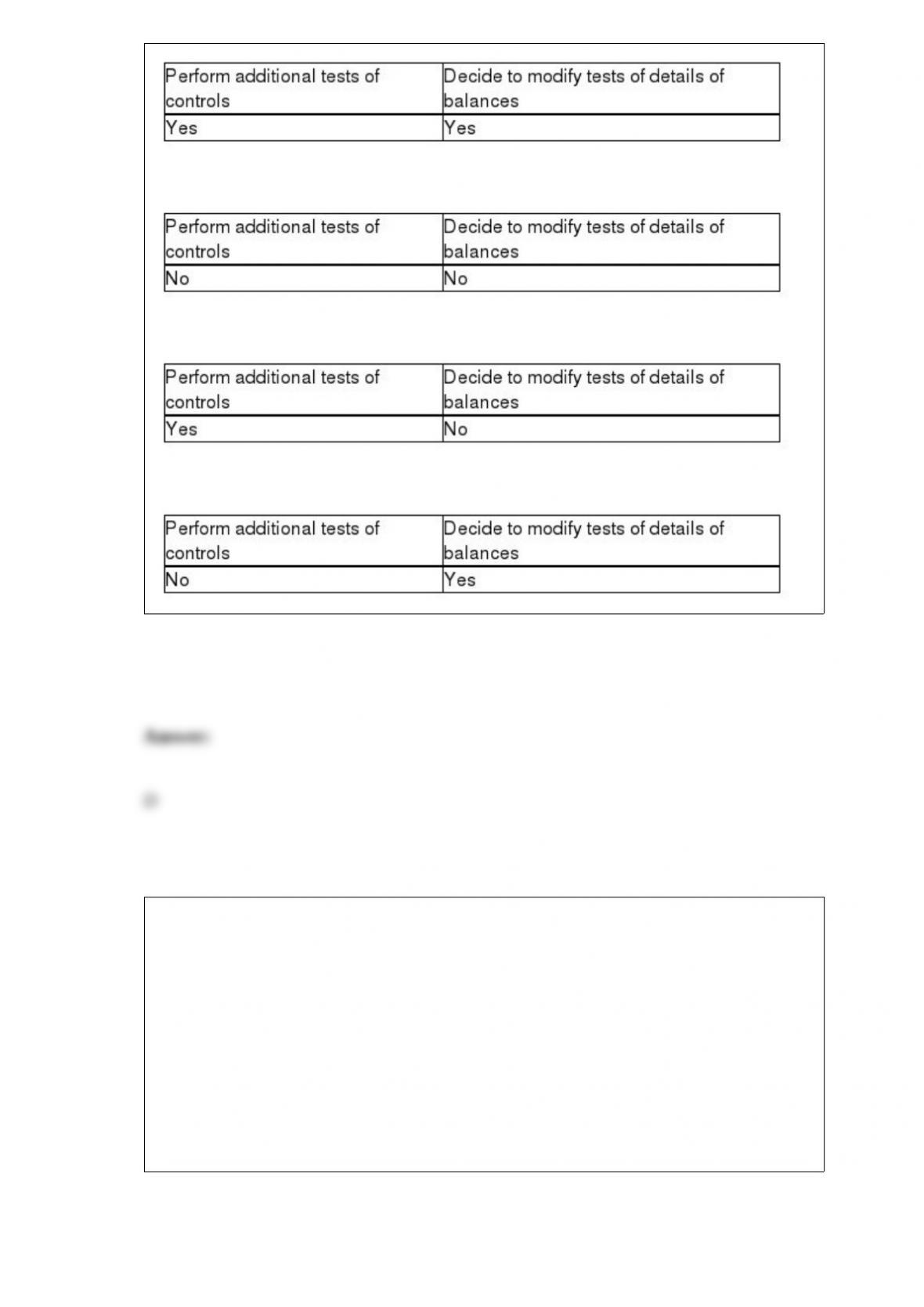

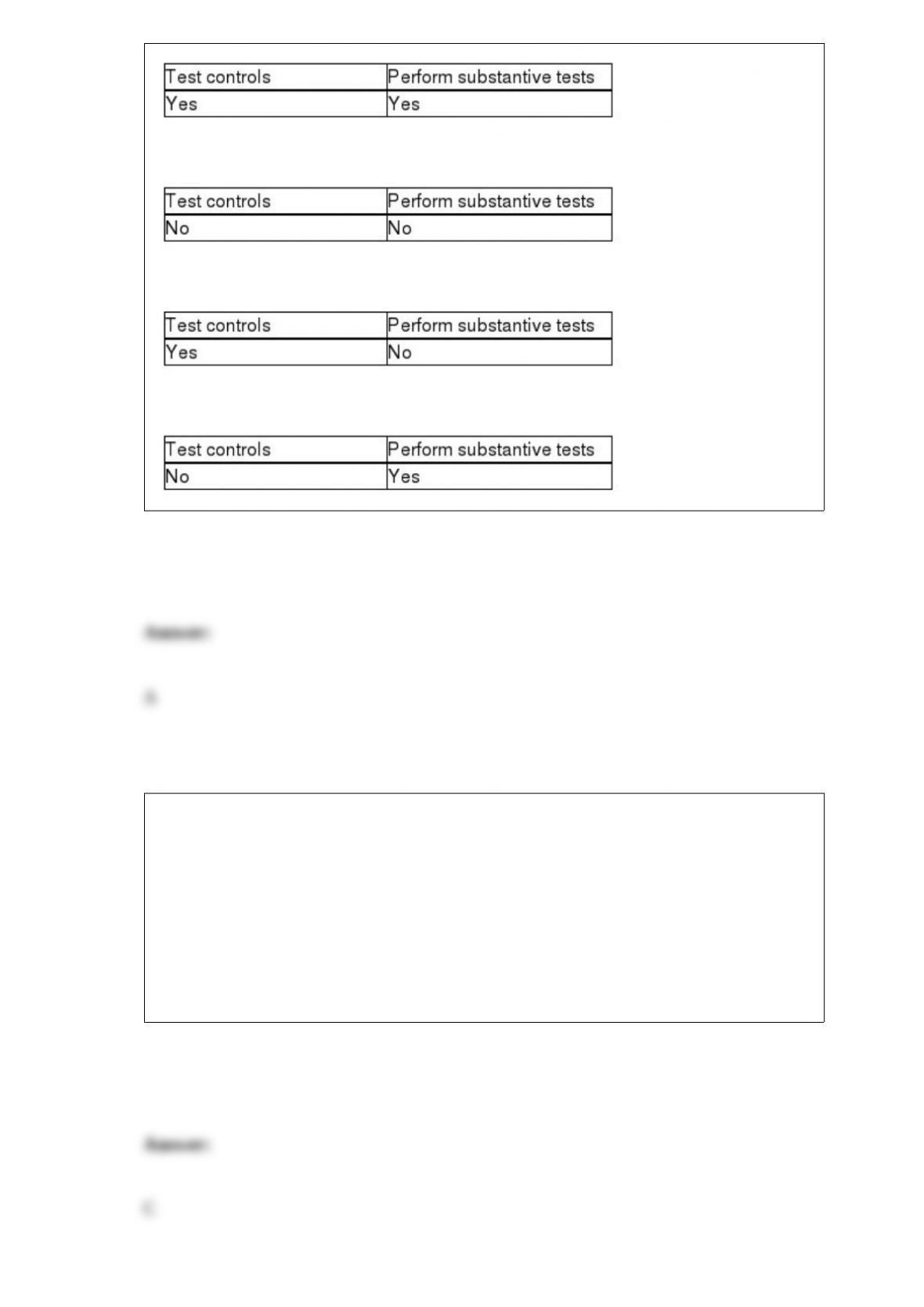

An increased extent of tests of controls is most likely to occur when

A) it is a first-year audit.

B) the auditor is doing a “fraud audit.”

C) controls are effective and the preliminary control risk assessment is low.

D) controls are ineffective and the preliminary control risk assessment is high.

For audit evidence to be compelling to the auditor it must be sufficient and appropriate.

Which statement below is not correct regarding the appropriateness of audit evidence?

A) The more effective the internal control system, the more assurance it provides the

auditor about the reliability of financial reporting by the client.

B) An auditor’s opinion, to be economically useful and profitable to the auditing firm

needs to be formed within a reasonable time and based on evidence obtained that

assures profits for the auditing firm.

C) Evidence obtained from independent sources outside the entity is generally more

reliable than evidence secured solely within the entity.

D) The independent auditor’s direct personal knowledge, obtained through inquiry,

observation and inspection, is generally more persuasive than information obtained

indirectly.

The cycle approach to auditing

A) ties to the way transactions are recorded in journals and then summarized in the

general ledger and financial statements.

B) cannot combine transactions recorded in different journals with the general ledger

balances that result from those transactions.

C) is the only way of segmenting an audit.

D) assumes that each account has two or more cycles associated with it.

A key internal control over the acquisition cycle is to ensure that the company requires

recording transactions as soon as possible after the goods and services have been

received. This satisfies the transaction-related audit objective of

A) accuracy.

B) completeness.

C) timing.

D) occurrence.

When using monetary unit sampling, the recorded dollar population is a definition of all

the items in the

A) population.

B) population which the auditor has included in the sample.

C) population which contain errors.

D) sample which contain errors.

When a client fails to follow GAAP, the audit report can be unmodified, qualified, or

adverse depending on the materiality. What factors affect materiality that an auditor

should consider?

A) the dollar amount in comparison to a base

B) if the misstatement can be measured

C) the nature of the item

D) All the above are factors an auditor should consider regarding materiality.

Which of the following items would not normally appear on bank reconciliations?

A) balance per bank

B) list of deposits in transit

C) outstanding deposits

D) outstanding checks

Audits

A) are an assurance service, but not an attestation service.

B) are designed to provide absolute assurance that the financial statements are free of

material misstatement.

C) are required for publicly traded companies in the United States.

D) do not require the auditor to express their opinion in a written report.

Which of the following statements is true regarding communications between

predecessor and successor auditors?

A) The burden of initiating the communication rests with the predecessor.

B) The predecessor’s response can be limited to stating that no information will be

provided.

C) The predecessor should communicate with the successor only if the client is public.

D) The predecessor auditor of a public company does not need permission from the

client before communicating with the successor auditor.

Which of the following is generally not included in the “evidence mix”?

A) tests of controls

B) substantive tests of transactions

C) risk assessment procedures

D) tests of details of balances

All corporations must have

A) preferred stock.

B) capital stock.

C) paid-in capital in excess of par.

D) dividends payable.

If there is collusion among management, the chance a normal audit would uncover such

acts is

A) very low.

B) very high.

C) zero.

D) none of the above.

CPAs are prohibited from which of the following forms of advertising?

A) self-laudatory advertising

B) celebrity endorsement advertising

C) use of trade names, such as “Awesome Auditors”

D) use of phrases, such as “Guaranteed largest tax refunds in town!”

________ is an attitude that includes a questioning mind, being alert to conditions that

might indicate possible misstatements due to fraud or error, and a critical assessment of

audit evidence.

A) Reasonableness

B) Diligence

C) Professional skepticism

D) Competence

Which of the following is not one of the major differences between financial and

operational auditing?

A) The financial audit is oriented to the past, but an operational audit concerns

performance for the future.

B) The financial audit report has widespread distribution, but the operational audit

report has limited distribution.

C) Financial audits deal with the information on the financial statements, but

operational audits are concerned with the information in the ledgers.

D) Financial audits are limited to matters that directly affect the fairness of the financial

statement presentation, but operational audits cover any aspect of efficiency and

effectiveness.

The International Standards for the Professional Practice of Auditing list seven

performance standards. List three.

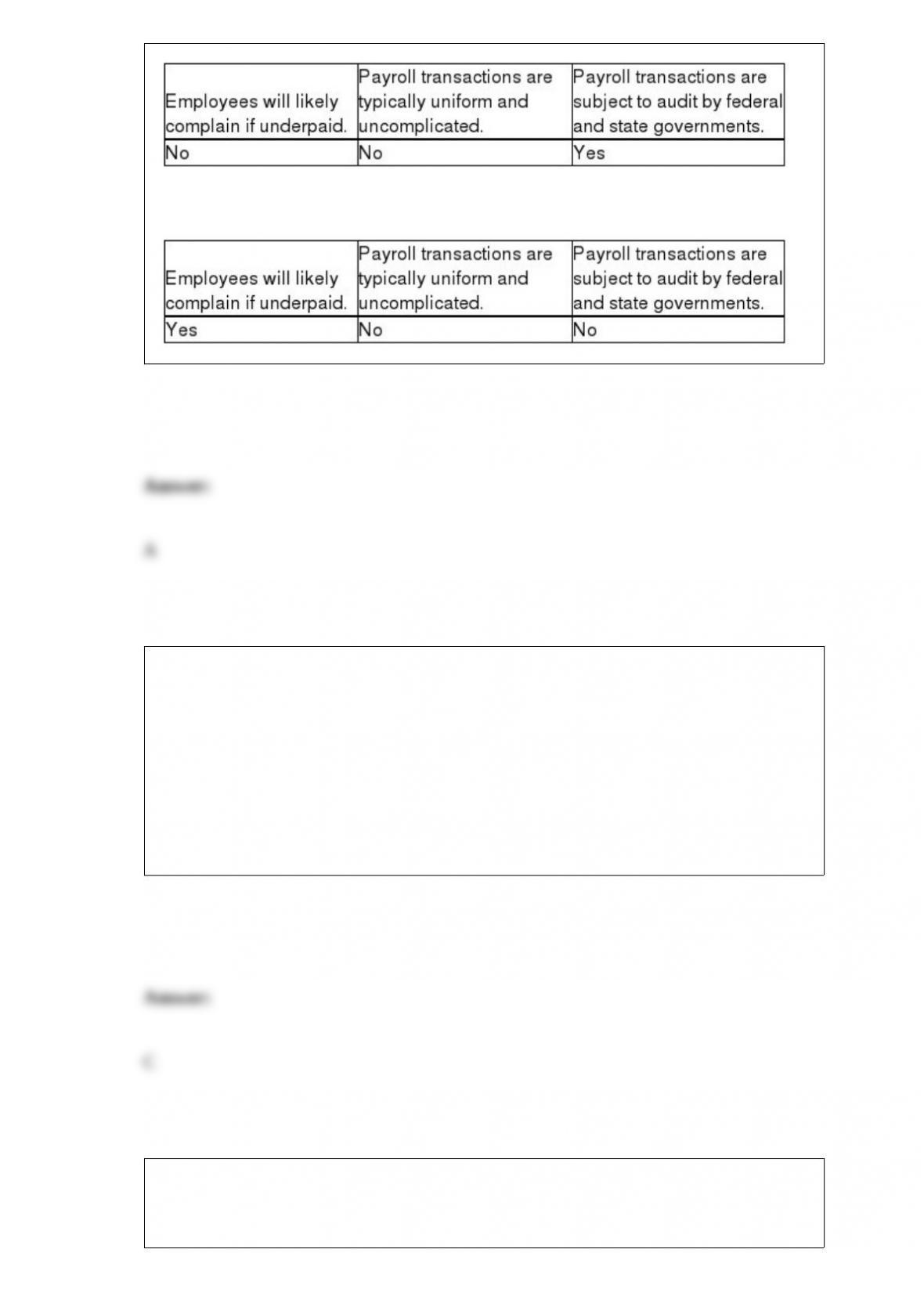

List the four business functions in the acquisition and payment cycle.

The Sarbanes-Oxley Act established the Public Company Accounting Oversight Board

(PCAOB). What are the PCAOB’s primary functions?

Given the following information about your audit client, perform analytical procedures

and comment on your findings.

Processing controls include the following tests:

Validation

Sequence

Data Reasonableness

Completeness

Describe what each control is designed to do:

What should be audited on an interbank transfer schedule?

There are 14 steps to audit sampling for tests of details of balances, divided into three

sections: plan the sample, select the sample and perform the audit procedures, and

evaluate the results. Discuss each of the steps included in the “evaluate the results”

section for nonstatistical sampling.

Discuss the alternative procedures an auditor can perform to test the existence objective

for accounts receivable when customers do not respond to confirmation requests.

List two common tests of details of balances procedures the auditor would perform

when testing for the balance-related audit objective of realizable value.

Discuss the similarities and differences between the roles of independent auditors, GAO

auditors, internal revenue agents, and internal auditors.

Identify the six categories of general controls and give one example of each.

Discuss three of the following characteristics of relevant evidence.

1. Independence of provider

2. Effectiveness of client’s internal controls

3. Auditor’s direct knowledge

4. Qualification of individuals providing the information

5. Degree of objectivity

6. Timeliness

Auditors examine supporting documentation for cash disbursements subsequent to the

balance sheet date in order to determine whether the cash disbursement was for a

current period liability.

Describe at least two audit procedures the auditor would perform to provide evidence

that the cash disbursement was made for a current period liability.

Describe the differences between positive and negative confirmations. Which type is

generally viewed as more reliable?

CPA firms perform numerous services that generally fall outside the scope of assurance

services. Give three examples of such services.

State the two primary types of subsequent events that require consideration by

management and evaluation by the auditor, and give two examples of each type.

How do the risk and materiality thresholds change in a government audit compared to a

financial statement audit of a public company?