When analytical procedures reveal unusual fluctuations in an account balance, the

auditor will probably perform fewer tests of details for that account and increase the

tests of controls related to the account.

Companies using e-commerce systems to transact business electronically do not need to

be concerned about how their e-commerce partners manage IT systems risks.

If the audit assurance rate is 95%, then the level of acceptable audit risk is 5%.

Auditors are normally more concerned about violations of the completeness objective

for acquisitions than about violations of the occurrence objective for acquisitions.

Tests of controls provide evidence about the likelihood for misstatements in a client’s

financial statements.

It is equally acceptable under professional auditing standards for auditors to use either

statistical or nonstatistical sampling methods.

Firing personnel terminates the payroll and personnel cycle.

The shipping point is critical because it is the first point at which company assets are

released to another party.

For automated controls, the auditor’s procedures to determine whether the automated

control has been implemented cannot also serve as the test of that control.

Changes in reporting entities, such as the inclusion of an additional company in

combined financial statements, affect comparability but not consistency, and therefore

do not require an explanatory paragraph in the audit report.

One of the reasons that auditors verify equipment differently from current assets is the

amount of any given equipment acquisition is often material.

One major limitation in the application of the audit risk model is the difficulty of

measuring the components of the model.

The Private Securities Litigation Reform Act of 1995 capped damage awards against

auditors to the amount of the audit fees charged.

At the completion of the audit, management is typically asked to make a written

statement as a part of the engagement letter that it is aware of no undisclosed contingent

liabilities.

For financial auditing, the audit report typically goes to many users of financial

statements, whereas operational audit reports are intended primarily for management.

Quality controls are established for the entire CPA firm whereas auditing standards are

applicable to the individual engagement.

Management typically allocates overhead using total raw materials as the basis for the

allocation.

The sales journal is generated from the sales transaction file.

Violations of the occurrence/existence objective for sales are of greater concern to the

auditor than violations of the completeness objective.

The evidence mix includes risk assessment procedures.

The probability threshold for dealing with uncertainty in loss contingencies uses the

terms likely and unlikely.

Analytical procedures are the least costly type of audit test.

In vertical analysis, the account balance is compared to the previous period, and the

percentage change for the period is calculated.

Walkthroughs combine observation, inspection, and inquiry to assure that the controls

designed by management have been implemented.

Performance materiality impacts inherent risk and control risk.

An agreed-upon procedures engagement cannot be undertaken for a federal

government agency.

Recording a sale that did not occur violates the occurrence transaction-related audit

objective and the existence balance-related audit objective.

The emphasis in the audit of dividends is on the ending balance rather than the

transactions.

An auditor assesses the risk of material misstatement to determine the impact on the

audit plan and to determine the nature, extent, and timing of the audit procedures.

Professionals are expected to conduct themselves at a higher level than most other

members of society.

Expulsion from the AICPA for failing to follow the rules of conduct is, by itself,

sufficient to prevent a CPA from practicing public accounting.

The larger the sample size, the more confident the auditor can be that the point estimate

is close to the true population value.

Accounting standards require disclosure of inventory valuation methods.

The acquisition and payment cycle typically begins with the initiation of a purchase

requisition for goods and services from an authorized individual.

Fictitious revenue transactions have the same level of documentary evidence as

legitimate transactions.

Auditors use the results of the substantive tests of transactions of sales and the

collection cycle to determine the extent to which inherent risk is satisfied for each

accounts receivable balance-related audit objective.

A sales invoice is a document that usually indicates credit approval.

Separation of duties in the sales and collection cycle should mandate that the

credit-granting function be separate from the sales function.

Statements on Standards for Accounting and Review Services (SSARS) govern the

CPA’s association with unaudited financial statements of nonpublic companies.

Which of the following parties provides an assessment of the effectiveness of internal

control over financial reporting for public companies?

A)

B)

C)

D)

Which of the following audit procedures would not likely detect a client’s decision to

pledge or factor accounts receivable?

A) a review of the minutes of the board of directors’ meetings

B) discussions with the client

C) confirmation of receivables

D) examination of correspondence files

The most significant effect of the results of the tests of controls and substantive tests of

transactions in the sales and collection cycle is on

A) bad debt expense.

B) the analytical tests to be performed.

C) the confirmation of accounts receivable.

D) the impact of processing cash receipts.

Which of the following verifications would generally not be performed by the auditor

in the month subsequent to the balance sheet date?

A) Foot the lists of all canceled checks, debit memos, deposits, and credit memos.

B) Verify the bank statement balances when the footed totals are used.

C) Verify the book statement balances tie to the cash receipts and disbursements

journals for the year under audit.

D) Review the items included in the footings to make sure that they were cancelled by

the bank.

Evidence is usually more persuasive for balance sheet accounts when it is obtained

A) as close to the balance sheet date as possible.

B) only from transactions occurring on the balance sheet date.

C) from various times throughout the client’s year.

D) from the time period when transactions in that account were most numerous during

the fiscal period.

The auditor obtained an aged list of receivables and traced the accounts to the master

file, footed the schedule, and traced the amounts to the general ledger. Which

balance-related audit objective was met?

A) existence

B) cutoff

C) detail tie-in

D) all of the above

For effective internal control, employees maintaining the accounts receivable subsidiary

ledger should not also approve

A) employee overtime wages.

B) credit granted to customers.

C) write-offs of customer accounts.

D) cash disbursements.

Under Sarbanes-Oxley, the audit committee of a public company

A) must meet on a monthly basis.

B) must be comprised entirely of financial experts.

C) is responsible for the oversight of the work of the independent auditor.

D) should have at least one independent member.

Backup and contingency plans should also identify alternative hardware that can be

used to process company data.

The audit procedures for the subsequent events review can be divided into two

categories:

(1) procedures normally integrated as a part of the verification of year-end account

balances, and (2) those performed specifically for the purpose of discovering

subsequent events. Which of the following procedures is in the second category?

A) Correspond with attorneys.

B) Test the collectability of accounts receivable by reviewing subsequent period cash

receipts.

C) Subsequent period sales and purchases transactions are examined to determine

whether the cutoff is accurate.

D) Compare the subsequent-period purchase price of inventory with the recorded cost

as a test of lower of cost or market valuation.

Management has recorded prepaid insurance as an asset in the previous year. This year,

to reduce record-keeping costs, it expenses insurance. If the amount is immaterial to the

financial statements,

A) a disclaimer opinion is issued.

B) a a qualified opinion is issued.

C) a standard unmodified opinion audit report is issued.

D) no audit report can be issued.

Which of the following modifications of the auditor’s report does not include an

explanatory paragraph?

A) A qualified report is due to a GAAP departure.

B) The report includes an emphasis of a matter.

C) There is a very material scope limitation.

D) A principal auditor accepts the work of an other auditor.

Which type of evidence is not used by the auditor to obtain an understanding of the

design and implementation of internal control?

A) inquiry

B) observation

C) confirmation

D) inspection

Which of the following is a major balance-related audit objective in testing payroll

liabilities?

A) Payroll tax expense is properly recorded.

B) Transactions in the payroll and personnel cycle are recorded in the proper period.

C) Accrual of salaries is the same as the amounts paid on the payroll tax returns.

D) Time records are recorded by supervisors.

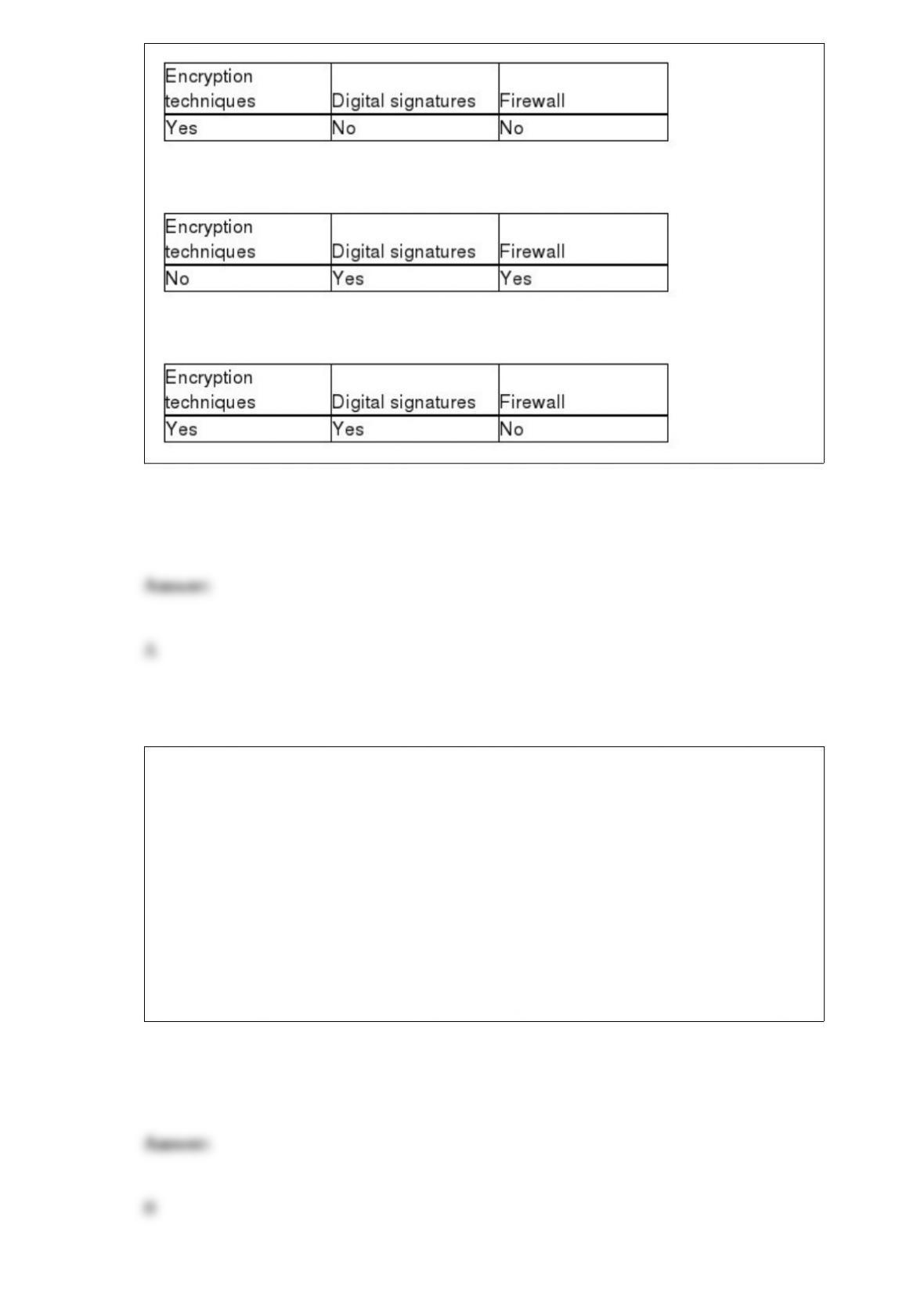

What tools do companies use to limit access to sensitive company data?

A)

B)

C)

D)

When auditing prepaid insurance,

A) for many audits, significant substantive procedures are needed if the control risk is

low.

B) companies often have a standard monthly journal entry to reclassify prepaid

insurance as insurance expense.

C) the emphasis in the tests of details of balances is on insurance expense.

D) the auditor must prepare the insurance register.

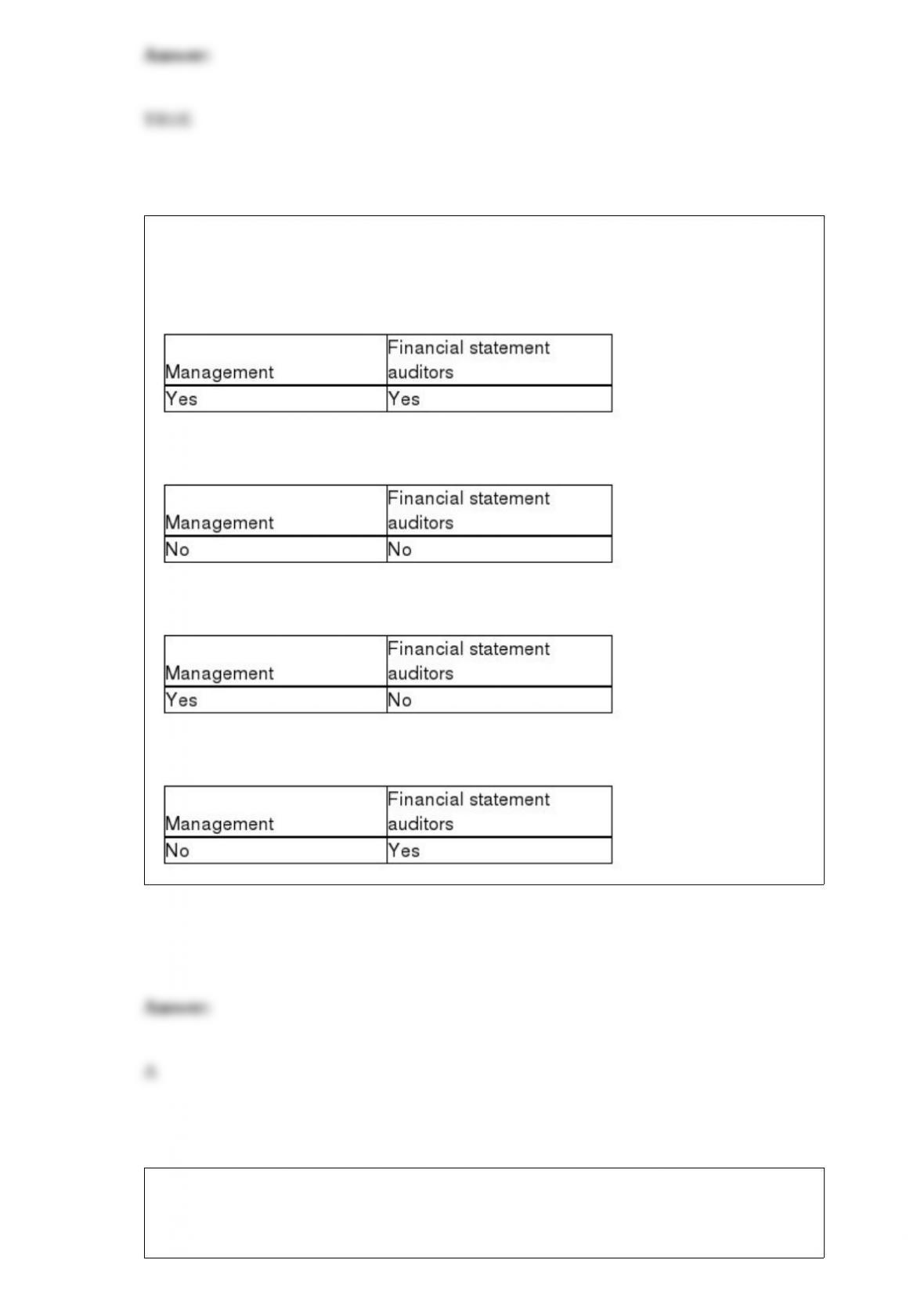

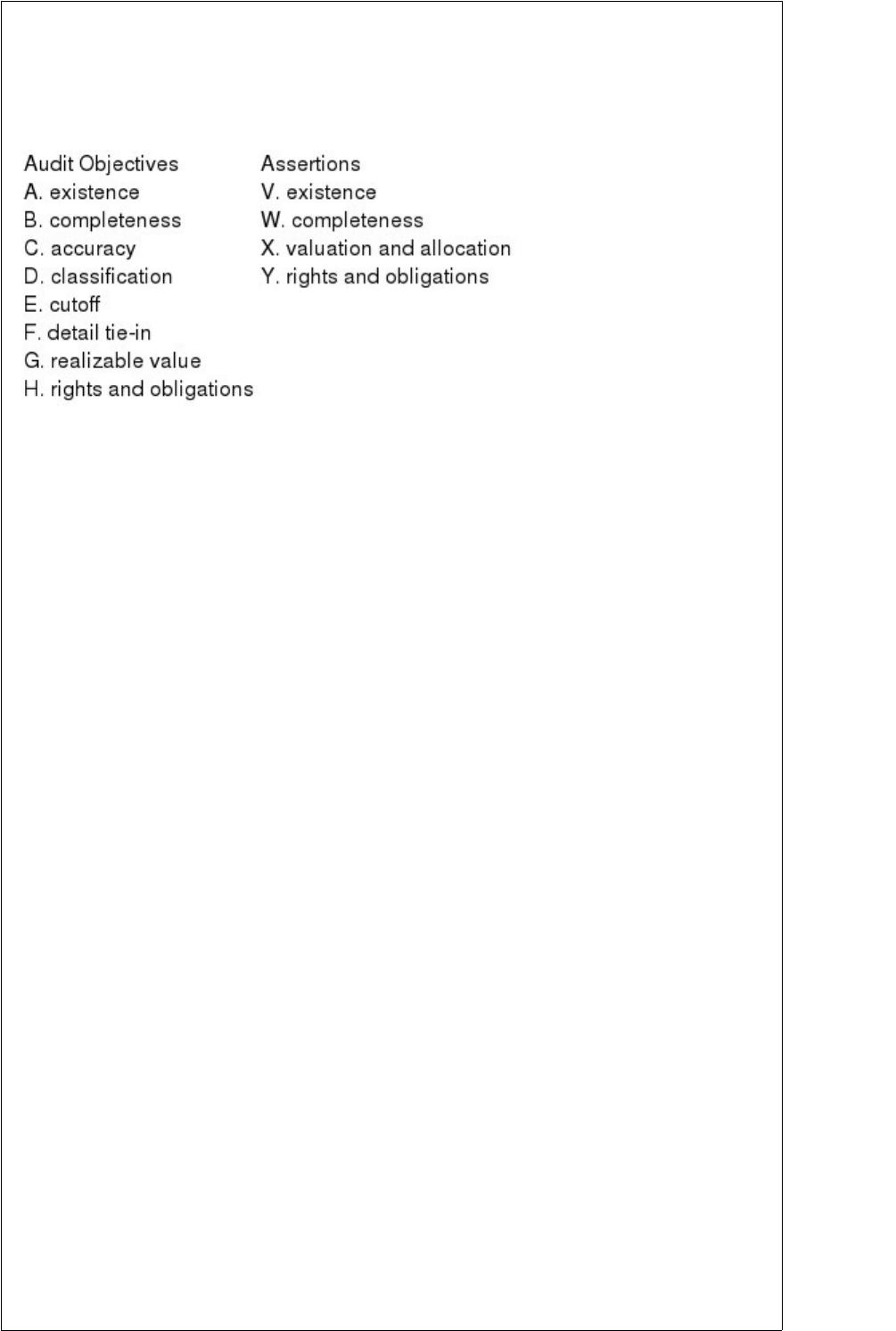

Below are five audit procedures, all of which are tests of balances associated with the

audit of accounts receivable. Also below are the eight general balance-related audit

objectives and the four management assertions. For each audit procedure, indicate (1)

its audit objective, and (2) the management assertion being tested.

1. Obtain an aged listing of accounts receivable. For a sample of individual customers

on the listing, agree the customer’s name, amount, and other information with the

corresponding information in the accounts receivable master file.

(1) ________

(2) ________

2. Examine details of sales for five days before and five days after year-end to

determine whether sales have been recorded in the proper period.

(1) ________

(2) ________

3. Assess the reasonableness of the balance in the allowance for doubtful accounts.

(1) ________

(2) ________

4. Inquire as to whether any accounts receivable have been factored or sold during the

period.

(1) ________

(2) ________

5. Inquire as to whether there are any receivables from related parties.

(1) ________

(2) ________

Which of the following is not a factor that relates to opportunities to misappropriate

assets?

A) inadequate internal controls over assets

B) presence of large amounts of cash on hand

C) inappropriate segregation of duties or independent checks on performance

D) adverse relationships between management and employees

Balance-related audit objectives

A) are never applied to income statement accounts.

B) are designed to detect fraud.

C) provide a framework to help the auditor accumulate sufficient appropriate evidence

related to account balances.

D) can have only one specific-related audit objectives.

If material, all of the following are required to be separately disclosed in the financial

statements except for

A) accounts receivable from officers.

B) accounts receivable from affiliates.

C) sales and assets for different business segments.

D) sales for the last ten days of the fiscal year.

The auditor’s internal control objective to determine that “recorded acquisitions are for

goods and services received” satisfies the audit objective of

A) accuracy.

B) occurrence.

C) authorization.

D) completeness.

Which of the following is an accurate statement regarding principles and auditing

standards?

A) The principles underlying an audit give specific guidance to an auditor when a

problem arises in an audit.

B) The principles underlying an audit state that the only objective of an audit is to

provide financial statement users with an opinion.

C) All auditing standards issued by the PCAOB are given two classification numbers.

D) The SAS number identifies the order in which it was issued in relation to other

SASs.

Which of the following is an accurate statement regarding the audit of pricing and

compilation of inventory?

A) Inventory compilation tests include all of the tests of the client’s unit prices to

determine whether they are correct.

B) The review for obsolete inventory should be performed by the accounting

department.

C) The most important internal control for accurate unit costs is external verification by

an outside consultant.

D) Inventory compilation internal controls are needed to ensure that the physical counts

are correctly summarized and priced.

One significant result of the Escott et al. v. BarChris Construction Corporation case

was

A) a greater emphasis on subsequent events procedures.

B) new standards for unaudited statements.

C) a broader definition of third party beneficiaries.

D) a requirement that more companies file annual reports with the SEC.

An imprest petty cash fund

A) is a bank account.

B) is used for large, unusual purchases.

C) is usually reimbursed at least once a week for good internal control.

D) is being replaced by pre-approved purchase cards in many companies.

________ is fraud that involves theft of an entity’s assets.

A) Fraudulent financial reporting

B) A “cookie jar” reserve

C) Misappropriation of assets

D) Income smoothing

Which of the following is not a “cash equivalent”?

A) time deposits

B) certificates of deposit

C) money market funds

D) marketable securities

When a CPA performs an examination engagement under the attestation standards, the

amount of evidence gathered is ________ and the level of assurance is ________.

A) extensive; varying

B) significant; high

C) extensive; high

D) significant; moderate

In using audit sampling for exception rates

A) the auditor wants to know the most the exception rate is likely to be.

B) sampling error is the likelihood that the auditor will miss a monetary misstatement.

C) the upper limit of the interval estimate is known as the sampling risk.

D) the computed upper exception rate (CUER) cannot be considered in the context of

specific audit objectives.

Which of the following deals with ongoing or periodic assessment of the quality of

internal control by management?

A) verifying activities

B) monitoring activities

C) oversight activities

D) management activities

Which of the following is a prescribed set of moral principles or values?

A) codes of business ethics for professional groups

B) laws and regulations

C) codes of conduct within an organization

D) all of the above

Which of the following is a correct statement?

A) The proof of cash receipts is a test of the balance in the cash account at a point in

time.

B) The proof of cash disbursements is effective for discovering a check written for the

incorrect amount for which the dollar amount in cash disbursements is also incorrect.

C) It is extremely difficult for an auditor to detect thefts of cash, especially omitted

transactions and account balances.

D) Segregation of duties is not an important control procedure for cash in a small

business.

Which of the following is a correct statement regarding performance materiality?

A) Determining performance materiality is necessary because auditors accumulate

evidence by segments.

B) The level of performance materiality does not affect the amount of evidence needed.

C) Performance materiality cannot vary for different classes of transactions.

D) Performance materiality is required for public companies, but not for private

companies.

The separate report on internal control over financial reporting

A) cannot contain a cross-reference to the auditor’s report on the financial statements.

B) includes a paragraph that addresses the inherent limitations of internal controls.

C) is addressed to the PCAOB.

D) includes a scope paragraph which refers to the framework used to evaluate internal

controls.

While performing a substantive test of details during an audit, the auditor determined

that the sample results supported the conclusion that the recorded account balance was

not materially misstated. It was, in fact, materially misstated. This situation illustrates

the risk of

A) incorrect rejection.

B) incorrect acceptance.

C) assessing control risk too low.

D) assessing control risk too high.

Describe the audit procedures used to verify the accuracy and detail tie-in objectives for

prepaid insurance.

Explain what is meant by a cutoff bank statement, and discuss the purpose of the cutoff

bank statement in the audit of cash.

The auditor receives the client’s schedule of recorded disposals and then performs detail

tie-in tests of the recorded disposals schedule. What procedures does the auditor

perform on the client’s schedule of recorded disposals?

Define forecast and projection.

In evaluating the operational effectiveness of internal controls, the auditor is likely to

use four types of audit procedures. List the procedures below.

Explain why there is a special need for ethical conduct in the auditing profession.

You are part of the audit team that is auditing Hillsburg Hardware Co. and you have

been assigned to the sales and collection cycle. You are testing whether the cash

receipts are deposited and recorded at the amounts received (accuracy objective). List

two tests of controls and one test of transactions that you would do to satisfy yourself

regarding the accuracy objective.

In phase IV of the audit, complete the audit and issue an audit report, there are five

activities required. List below the activities.

The examination of prospective financial statements contains four elements that

comprise the examination. List the four elements below.

What are several substantive analytical procedures used in the audit of prepaid

insurance and insurance expense?

Due to qualitative factors, certain types of misstatements are likely to be more

important to users than others, even if the dollar amounts are the same. Identify two

qualitative factors that might significantly affect an auditor’s materiality judgment, and

give an example of each.

Why do auditors use the audit risk model when planning an audit?

For each of the following potential misstatements, provide one potential audit test that

could be used to detect the misstatement.

– sales included in the journals for which there was no shipment

– sale recorded more than once

– shipments made to nonexistent customers and recorded as sales

Distinguish between internal documentation and external documentation as types of

audit evidence. Give two examples of each. Which type is considered more reliable?

Discuss each of the three broad categories (types) of operational audits.

Identify each of the seven factors that influence sample size for nonstatistical tests of

details of balances, and state whether each factor is directly or inversely related to

sample size.

U.S. auditing standards indicate that auditors should use external confirmations for

accounts receivable. However, there are certain circumstances where confirmation may

not be appropriated. List these three situations.

Assuming the client’s internal controls are effective, describe how the auditor can verify

proper cutoff of sales transactions.

CPAs can be held liable for criminal activity under both state and federal laws.

Infamous cases include United States vs. Natelli and ESM Government Securities v.

Alexander Grant and Co. Discuss what occurred in each case.

What are three factors that have increased the importance of obtaining an understanding

of a client’s business and industry? How can an auditor obtain this understanding?