If, when obtaining an understanding of control activities of a relatively small client, the

auditor identified no control activities, the auditor would probably set a high assessment

of control risk.

Depreciation expense is normally verified as a part of tests of details of balances rather

than as part of tests of controls or substantive tests of transactions.

Although there is confusion caused by the differing views of liability to third parties

under common law, the movement is clearly away from the foreseeable user approach.

The bank reconciliation control is enhanced when a qualified employee reviews the

monthly reconciliation as soon as possible after its completion.

The Securities and Exchange Commission requires companies listed on exchanges to

employ stock transfer agents.

Auditors of public companies must obtain certain representations from management

regarding internal control over financial reporting.

An exception in a test of control provides only an indication of the likelihood of

monetary misstatements in the financial statements because tests of controls do not

reveal whether monetary misstatements have actually occurred.

When controls are effective and control risk is assessed as low, auditors put heavy

emphasis on tests of balances.

Inquiries of the client are usually sufficient to provide appropriate evidence to satisfy an

audit objective.

The AICPA has discontinued the SysTrust seal program.

The risk of fraud should be assessed for the entire audit as well as by cycle, account,

and objective.

The term “audit failure” refers to the situation when the auditor has followed auditing

standards yet still fails to discover that the client’s financial statements are materially

misstated.

In selecting the sample, probabilistic methods must be used for both statistical and

nonstatistical sampling.

Interpretations of rules of conduct in the Code of Professional Conduct are not

officially enforceable and practitioners need not justify departure from them.

The board of directors must authorize the amount of the dividend per share and the

dates of record and payment of the dividend.

One result from the Escott et al. v. BarChris case was a greater emphasis being placed

on the audit staff’s understanding of the client’s business and industry.

A proof of cash includes a reconciliation of cash receipts deposited in the bank with the

cash disbursements records for a given period.

If an auditor performs a compilation but lacks independence, an additional paragraph

must be added which states that: “We are not independent with respect to XYZ

Company.”

An item with a “psychological” effect (e.g., where the item maintains an increasing

earnings trend) is a qualitative factor that may affect the auditors decision regarding

materiality.

For each key control, one or more tests of controls must be designed to verify its

effectiveness.

The emphasis in auditing manufacturing equipment is on the verification of

current-period disposals and acquisitions.

Under the Form of Organization and Name rule, a CPA firm may not designate itself as

“Members of the American Institute of Certified Public Accountants” unless a majority

of its owners are members of the Institute.

Effectiveness refers to the degree to which costs are reduced without reducing

efficiency.

Under the AICPA’s Code of Professional Conduct, CPAs are prohibited from offering

audit clients a discount for referring a prospective client even if they are disclosed.

When auditing sales returns and allowances, the emphasis is normally on testing the

completeness objective.

Auditors are required to obtain a letter of representation that describes management’s

planned solutions to all internal control weaknesses identified during an audit.

Tests of the realizable value balance-related audit objective are for the purpose of

evaluating the allowance for doubtful accounts.

Although auditors need to consider the interrelationships between cycles, they typically

treat cycles independently to the extent practical to manage complex audits effectively.

Confirmations are commonly used to verify additions of property, plant, and equipment.

Under the cycle approach, the only accounts that have two or more cycles associated

with them are cash and accounts receivable.

In many audits of sales transactions substantive tests of transactions can be reduced in

determining the completeness objective because

A) understatements of assets and income are a greater concern than overstatements.

B) overstatements of assets and income are a greater concern than understatements.

C) it doesn’t matter if income is understated because the savings on income tax offsets

the reduced revenue and net income is correct.

D) the unrecorded sales cause a reduction of accounts receivable; therefore, the ratios of

the two financial statements will not be misleading.

The audit and accounting concern addressed in a monthly proof of cash is with

A) adjusting account balances.

B) reconciling the amounts recorded in the books with the amounts included in the bank

statement.

C) determining the month-end balance.

D) identifying cash transfers.

In performing the audit of internal control over financial reporting, the auditor

emphasizes internal control over classes of transactions because

A) the accuracy of accounting system outputs depends heavily on the accuracy of inputs

and processing.

B) the class of transaction is where most fraud schemes occur.

C) account balances are less important to the auditor then the changes in the account

balances.

D) classes of transactions tests are the most efficient manner to compensate for inherent

risk.

When designing the audit program and the particular audit tests, the auditor should keep

in mind that

A) the audit program is broken down into two parts-the risk assessment procedures and

the tests of details of balances.

B) the tests of controls will not vary depending on assessed control risk.

C) analytical procedures performed during substantive testing are generally more

focused and more extensive than those done as part of planning.

D) auditing standards require that the tests contained in the audit program must be

approved by the PCAOB.

If the auditor were responsible for making certain that all of management’s assertions in

the financial statements were absolutely correct,

A) bankruptcies could no longer occur.

B) bankruptcies would be reduced to a very small number.

C) audits would be much easier to complete.

D) audits would not be economically practical.

The test of transactions which requires one to “reconcile recorded cash disbursements

with the cash disbursements on the bank statement” satisfies the objective of

A) occurrence.

B) completeness.

C) accuracy.

D) posting and summarization.

Which of the following best describes inherent risk for balance-related audit objectives

as they relate to payroll?

A) not considered

B) low

C) moderate

D) high

A record of insurance policies in force and the due date of each policy is contained in

the

A) voucher register.

B) insurance register.

C) insurance expense account.

D) prepaid insurance account.

In connection with the audit of financial statements, an independent auditor could be

responsible for failure to detect a material fraud if

A) statistical sampling techniques were not used on the audit engagement.

B) the auditor planned the audit in a negligent manner.

C) accountants performing important parts of the work failed to discover a close

relationship between the treasurer and the cashier.

D) the fraud was perpetrated by one employee who circumvented the existing internal

controls.

Listing all bank transfers made a few days before and after the balance sheet date and

tracing each to the accounting records for proper recording is a useful approach to test

for

A) kiting.

B) lapping.

C) income smoothing.

D) channel stuffing.

For effective internal control purposes, the accounts payable department generally

should

A) approve the purchase order.

B) have the authority to sign the checks.

C) establish the agreement of the vendor’s invoice with the receiving report and

purchase order.

D) supervise the preparation of the receiving report.

The assessment against a defendant of that portion of the damage caused by the

defendant’s negligence is called

A) separate and proportionate liability.

B) joint and several liability.

C) shared liability.

D) unitary liability.

An auditor is reviewing the minutes of board meetings to determine whether any

securities are pledged as collateral. This test of the detail of balances relates to the audit

objective of

A) rights.

B) cutoff.

C) realizable value.

D) classification.

Which of the following is an important source of information for determining whether

the presentation and disclosure-related objectives for capital stock activities are

satisfied?

A) the corporate charter

B) the minutes of board of directors meetings

C) the auditor’s analysis of capital stock transactions

D) all of the above

An auditor’s independence is considered impaired if the auditor has

A) an immaterial, indirect financial interest in a client.

B) an outstanding $8,000 balance on a credit card issued by a client.

C) an automobile loan from a client bank, collateralized by the automobile.

D) a joint, closely held business investment with the client that is material to the

auditor’s net worth.

Which of the following statements is correct regarding the capital acquisition and

payment cycle?

A) Bonds are frequently issued by companies in small amounts.

B) There are relatively few transactions and each transaction is typically highly

material.

C) A primary emphasis in auditing debt is on existence.

D) Audit procedures for notes payable and interest income are often performed

simultaneously.

Which one of the following is not true regarding the American Institute of Certified

Public Accountants peer review requirement?

A) A CPA firm must develop and adhere to quality control standards.

B) Peer reviews are mandatory.

C) A CPA firm will lose AICPA eligibility if a peer review is not performed.

D) Firms required to be registered with and inspected by the PCAOB are exempt.

The Public Company Accounting Oversight Board

A) performs inspections of the quality controls of firms that audit public companies.

B) establishes auditing standards that must be followed by CPAs on all audits.

C) oversees auditors of private companies.

D) performs all of the above functions.

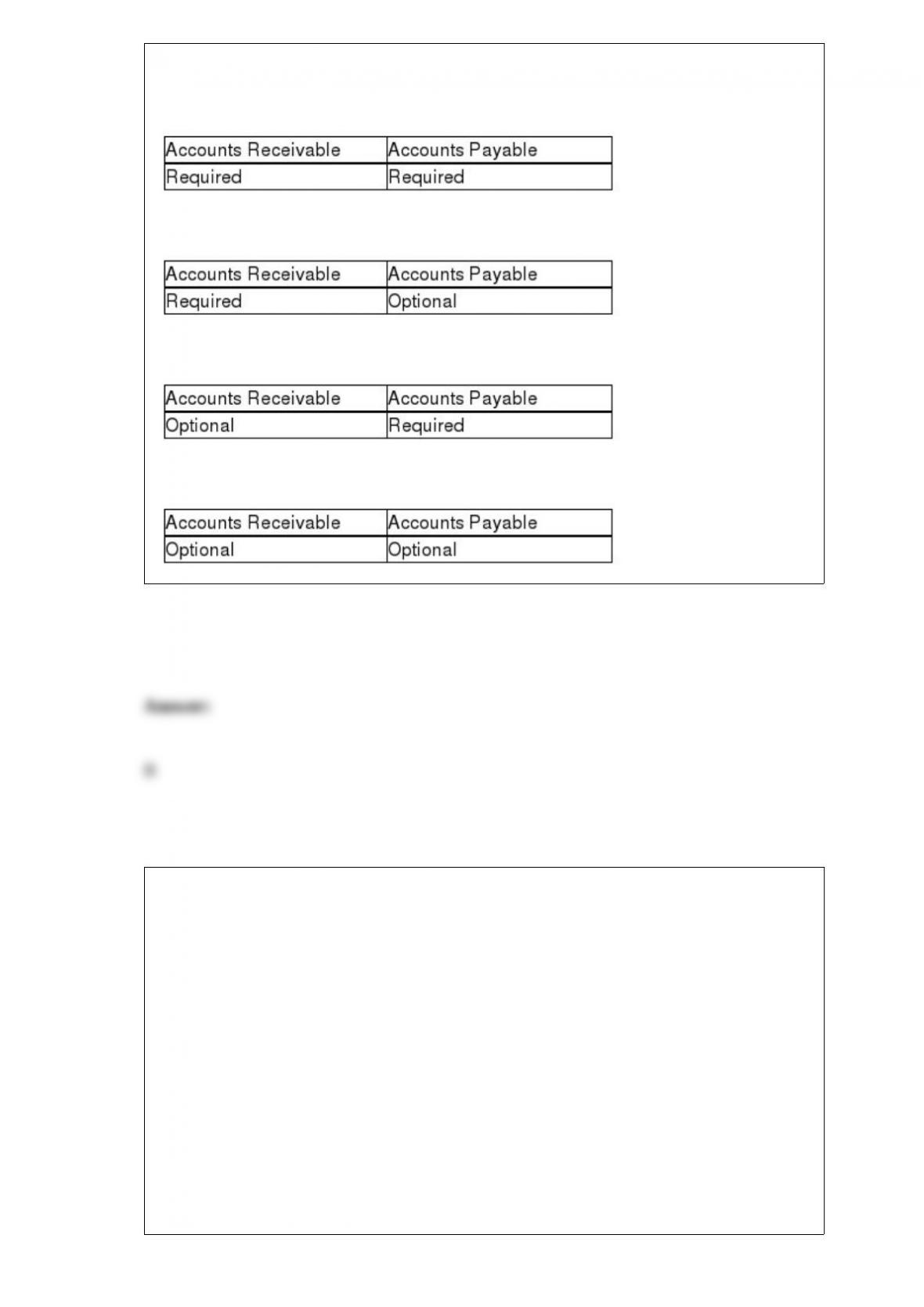

Indicate whether confirmation of accounts receivable and accounts payable, provided

they each are significant accounts, is required or optional.

A)

B)

C)

D)

The audit firm issues an audit report for its client. The auditors have no obligation to

make further inquiries with respect to the client’s audited financial statements unless

A) a development occurs that may affect the company’s long term viability as a

company.

B) final resolution was made on disclosed contingency for which no liability needed to

be accrued.

C) new information comes to the auditor’s attention concerning an event that occurred

prior to the date of the audit report that, if known, would have impacted the audit

opinion.

D) a lawsuit, in which the risk of loss was considered remote, was resolved in the

company’s favor.

Which one of the choices below is most correct regarding a cause of sampling risk?

A) ineffective use of audit procedures

B) testing less than the entire population

C) use of extensive tests of controls

D) use of random sampling

Laws that have been passed by the U.S. Congress and other governmental units are

A) statutory laws.

B) judicial laws.

C) federal laws.

D) common laws.

Which of the following errors gives the auditor concern in auditing payroll

transactions?

A) an error that indicates possible fraud

B) computational errors in formulas when a computerized system is used

C) classification errors in charging labor to inventory and job cost accounts

D) Each of the above gives the auditor significant concern.

Compilation reports may be of all except which of the following types?

A) compilation with limited independence

B) compilation with full disclosure

C) compilation without independence

D) compilation that omits substantially all disclosures

When determining what type of report to issue on internal control under Section 404,

A) an adverse opinion on internal control must be given if any weaknesses in a key

internal control is discovered.

B) a scope limitation requires the auditor to disclaim an opinion on internal controls.

C) if the auditor gives a qualified opinion on the financial statements, they must give a

qualified opinion on internal controls.

D) a scope limitation requires the auditor to express a qualified opinion or a disclaimer

of opinion on internal controls.

The auditor’s primary concern in performing audit procedures of the write-off of

uncollectible accounts relates to the risk that the client writes off customer accounts that

have already been collected. The primary control for preventing this fraud is

A) examining authorized credit memos.

B) examining the uncollectible account authorization form.

C) examining debit memos.

D) examining the vouchers payable register.

Which of the following audit objectives is least important in the audit of capital stock

and paid-in-capital in excess of par?

A) completeness

B) accuracy

C) rights and obligations

D) presentation and disclosure

Which of the following is not a step in the professional judgment process?

A) make the decision

B) perform the analysis

C) determine the type of audit opinion

D) review and document the rationale for the conclusion

What type of supporting schedule is designed to show detailed tests performed, does

not tie in to the general ledger, but must state a positive or negative conclusion about

the objective of the test?

A) outside documentation

B) reconciliation of amounts

C) examination of supporting documents

D) substantive analytical procedures

A ________ is responsible for controlling the use of computer programs, transaction

files and other computer records and documentation and releases them to the operators

only when authorized.

A) software engineer

B) chief computer operator

C) librarian

D) data control operator

Which of the following is a correct statement regarding the SEC?

A) The Securities Act of 1934 requires most companies planning to issue new securities

to the public to submit a registration statement to the SEC for approval.

B) All public companies must file monthly statements with the SEC.

C) The Form 10-K must be filed within 30 days after the close of the fiscal year.

D) The SEC has the power to establish rules for any CPA associated with audited

financial statements submitted to the commission.