Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

7-27 (continued)

ACCOUNT

NAME

FROM WHOM

CONFIRMED

INFORMATION

TO BE CONFIRMED

NOTES

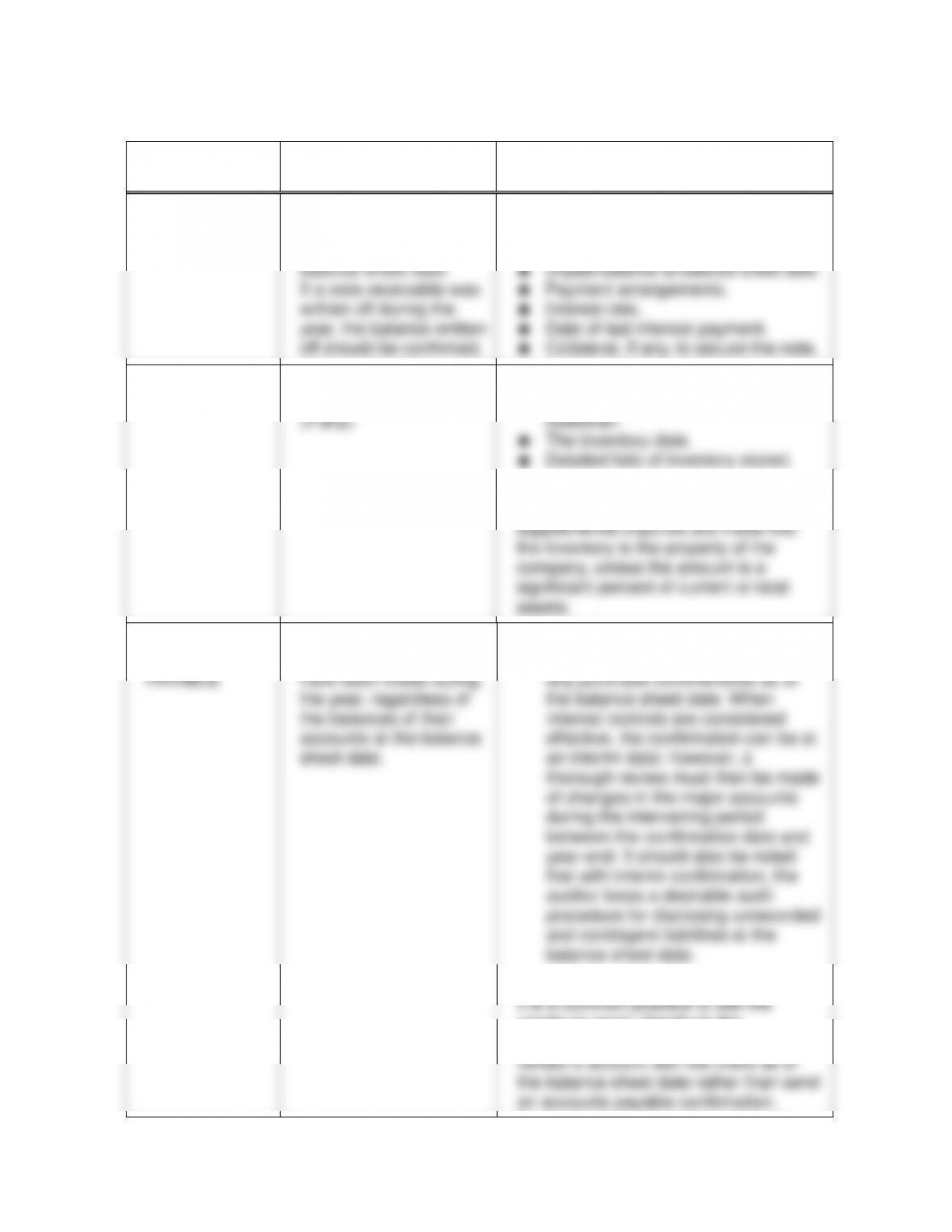

RECEIVABLE

A selected sample of

notes receivable

outstanding at the

balance sheet date.

If a note receivable was

written off during the

year, the balance written

off should be confirmed.

Name and address of the debtor.

Date of the note.

Due date.

Unpaid balance at balance sheet date.

Payment arrangements.

Interest rate.

Date of last interest payment.

Collateral, if any, to secure the note.

INVENTORIES

Public warehouses or

other outside custodians

(if any).

Name and address of public

warehouse or other outside

custodian.

The inventory date.

Detailed lists of inventory stored.

Under auditing standards, direct

confirmation is acceptable provided

supplemental inquiries are made that

the inventory is the property of the

company, unless the amount is a

significant percent of current or total

assets.

TRADE

ACCOUNTS

PAYABLE

Suppliers from whom

substantial purchases

have been made during

the year, regardless of

the balances of their

accounts at the balance

sheet date.

Name and address of the supplier.

The amount due and the amount of

any purchase commitments as of

the balance sheet date. When

internal controls are considered

effective, the confirmation can be at

an interim date; however, a

thorough review must then be made

of changes in the major accounts

the balance sheet date rather than send

an accounts payable confirmation.

7-27 (continued)

ACCOUNT

NAME

FROM WHOM

CONFIRMED

INFORMATION

TO BE CONFIRMED

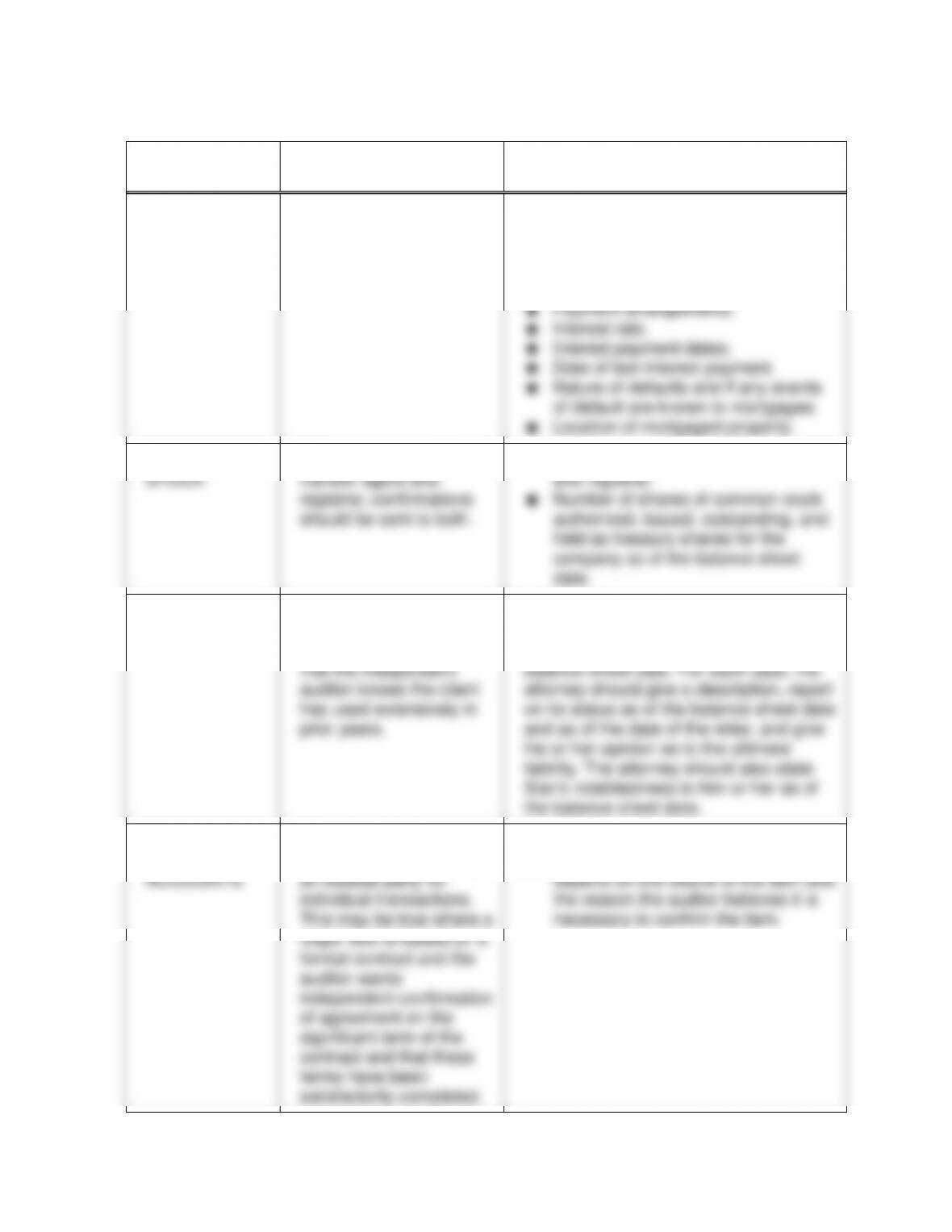

MORTGAGES

PAYABLE

Mortgagee for each

mortgage that has a

balance at the balance

sheet date.

Name and address of mortgagee.

Original amount.

Date of note.

Maturity date.

Balance due at balance sheet date.

Payment arrangements.

Interest rate.

Interest payment dates.

Date of last interest payment.

Nature of defaults and if any events

of default are known to mortgagee.

Location of mortgaged property.

CAPITAL

STOCK

If Star uses an outside

transfer agent and

registrar, confirmations

should be sent to both.

Name and address of transfer agent

and registrar.

Number of shares of common stock

authorized, issued, outstanding, and

held as treasury shares for the

company as of the balance sheet

date.

LEGAL FEES

All of Star’s major

attorneys. Letters should

also be sent to attorneys

that the independent

auditor knows the client

has used extensively in

prior years.

The auditor should request a letter from

each attorney as to litigation being

handled as of and subsequent to the

balance sheet date. For each case, the

attorney should give a description, report

on its status as of the balance sheet date

and as of the date of the letter, and give

his or her opinion as to the ultimate

liability. The attorney should also state

Star’s indebtedness to him or her as of

the balance sheet date.

SALES AND

EXPENSE

ACCOUNTS

Occasionally, confirmation

may be requested from

an outside party for

individual transactions.

This may be true where a

major item is based on a

formal contract and the

auditor wants

Name and address of outside party.

Other specific information would

depend on the nature of the item and

the reason the auditor believes it is

necessary to confirm the item.

7-13

7-28

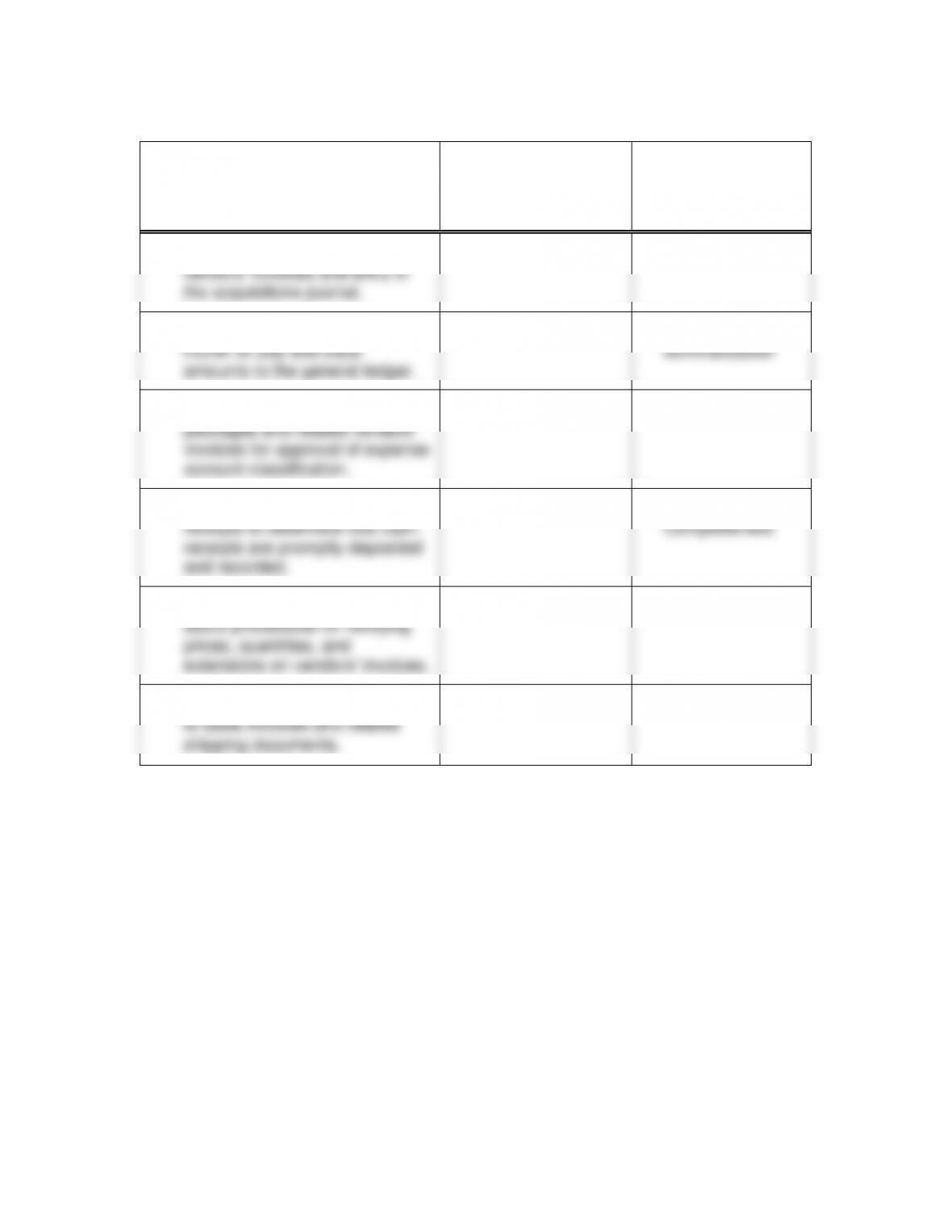

AUDIT PROCEDURE

a.

TYPE OF

AUDIT EVIDENCE

b.

TRANSACTION-

RELATED

AUDIT OBJECTIVE

1. Trace from receiving reports to

vendors’ invoices and entry in

the acquisitions journal.

Inspection

Completeness

2. Add the sales journal for the

month of July and trace

amounts to the general ledger.

Recalculation

Posting and

summarization

3. Examine expense voucher

packages and related vendors’

invoices for approval of expense

account classification.

Inspection

Classification

4. Observe opening of cash

receipts to determine that cash

receipts are promptly deposited

and recorded.

Observation

Timing and

Completeness

5. Ask the accounts payable clerk

about procedures for verifying

prices, quantities, and

extensions on vendors’ invoices.

Inquiries of client

Accuracy

6. Vouch entries in sales journal

to sales invoices and related

shipping documents.

Inspection

Occurrence

7-29

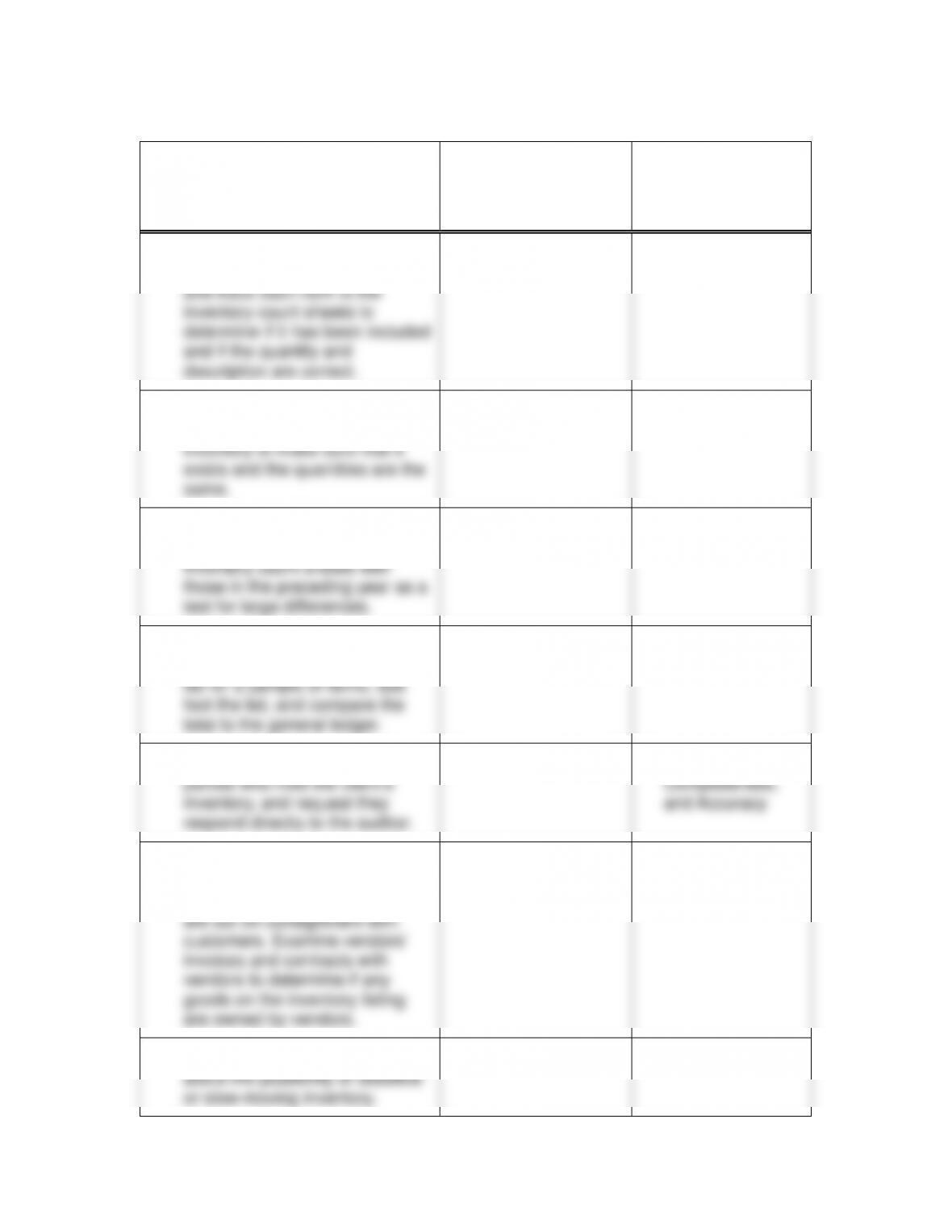

AUDIT PROCEDURE

a.

TYPE OF

AUDIT EVIDENCE

b.

BALANCE-

RELATED

AUDIT OBJECTIVE

1. Select a sample of inventory

items in the factory warehouse

and trace each item to the

inventory count sheets to

determine if it has been included

and if the quantity and

description are correct.

Physical examination

Completeness

and Accuracy

2. Trace selected quantities from

the inventory list to the physical

inventory to make sure that it

exists and the quantities are the

same.

Physical examination

Existence and

Accuracy

3. Compare the quantities on hand

and unit prices on this year’s

inventory count sheets with

those in the preceding year as a

test for large differences.

Analytical procedures

Accuracy

4. Test the extension of unit prices

times quantity on the inventory

list for a sample of items, test

foot the list, and compare the

total to the general ledger.

Recalculation

Detail tie-in

5. Send letters directly to third

parties who hold the client’s

inventory, and request they

respond directly to the auditor.

Confirmation

Existence,

Completeness,

and Accuracy

6. Examine sales invoices and

contracts with customers to

determine whether any goods

are out on consignment with

customers. Examine vendors’

invoices and contracts with

vendors to determine if any

goods on the inventory listing

are owned by vendors.

Inspection

Rights

7. Question operating personnel

about the possibility of obsolete

or slow-moving inventory.

Inquiries of the client

Realizable value

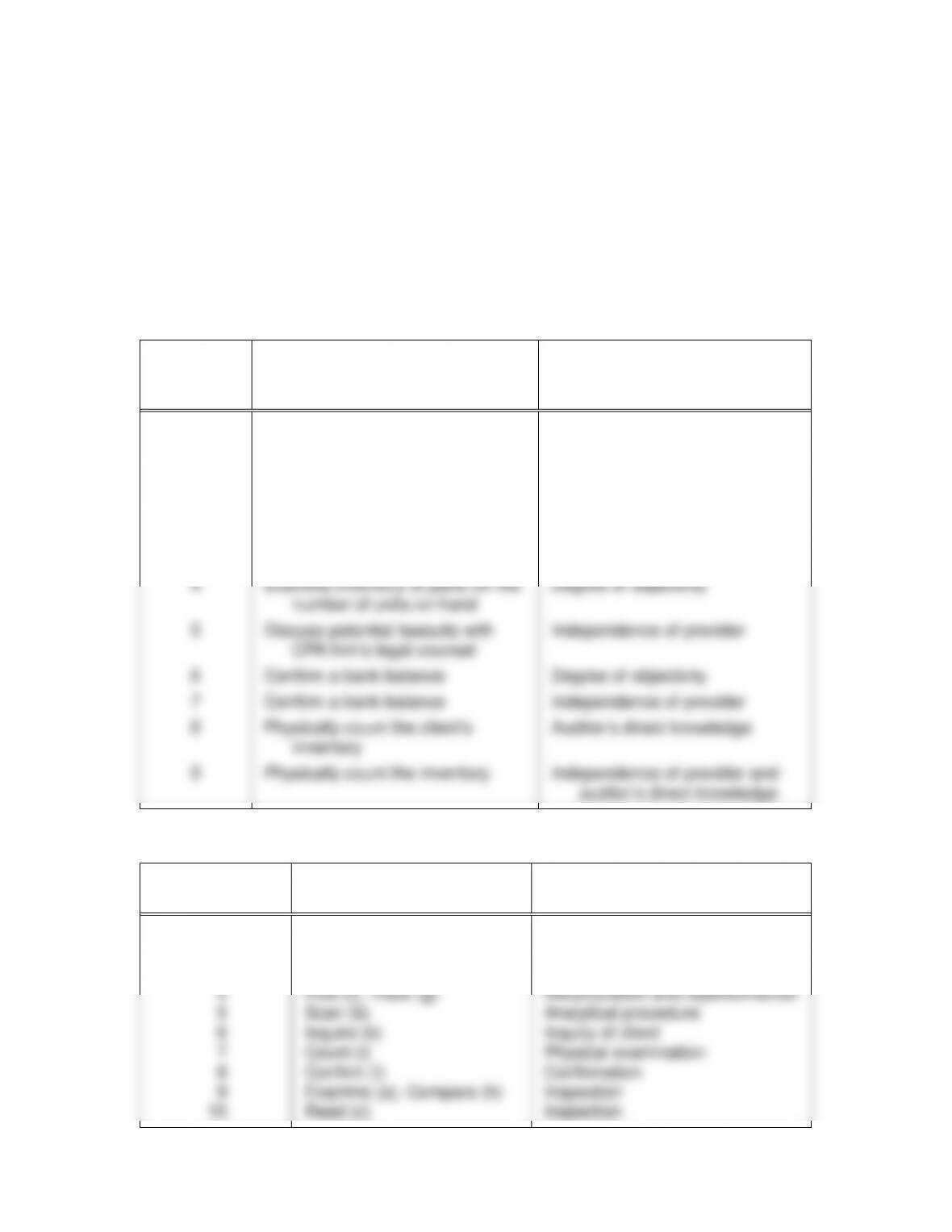

7-30 a. The six factors determining the reliability of evidence are:

1. Independence of provider

2. Effectiveness of client’s internal controls

3. Auditor’s direct knowledge

4. Qualifications of individuals providing the information

5. Degree of objectivity

6. Timeliness

b.

and

c.

SITUATION

b.

TYPE OF EVIDENCE

THAT IS MORE RELIABLE

c.

FACTOR

AFFECTING RELIABILITY

1

2

3

4

5

6

7

8

9

Confirmation with business

organizations

Physically examine three-inch

steel plates

Examine documents when

several competent people are

checking each other’s work

Examine inventory of parts for the

number of units on hand

Discuss potential lawsuits with

CPA firm’s legal counsel

Confirm a bank balance

Confirm a bank balance

Physically count the client’s

inventory

Physically count the inventory

Qualifications of provider

Qualifications of provider

(in this case the auditor)

Effectiveness of internal controls

Degree of objectivity

Independence of provider

Degree of objectivity

Independence of provider

Auditor’s direct knowledge

Independence of provider and

auditor’s direct knowledge

7-31

PROCEDURE

a.

APPROPRIATE TERM

b.

TYPE OF EVIDENCE

1

2

3

4

Recompute (e)

Observe (j)

Compute (d)

Foot (f), Trace (g)

Recalculation

Observation

Analytical procedure

Recalculation and reperformance

7-16

7-32 a. The purposes of analytical procedures are:

1. Understanding the client’s business and industry.

2. Assessment of the entity’s ability to continue as a going concern.

financial statements.

4. Reduction of detailed audit tests.

b. Analytical procedures are required in the planning and completion

phases of the audit because of their importance in planning the

c. The extent to which the auditor will use the results of analytical

procedures to reduce detailed tests depends on the effectiveness

of the analytical procedure and whether it supports the correctness

7-33

STATEMENT

RELATED STAGE OF AUDIT

1. Should focus on enhancing the

auditor’s understanding of the

client’s business and the

transactions and events that have

occurred since the last audit date.

a. Planning the audit

2. Should focus on identifying areas

that may represent specific risks

relevant to the audit.

a. Planning the audit

3. Require documentation in the

working papers of the auditor’s

expectation of the ratio or account

balance.

b. Substantive testing

4. Do not result in detection of

misstatements.

d. Statement is not correct concerning

analytical procedures

5. Designed to obtain evidential matter

about particular assertions related to

account balances or classes of

transactions.

b. Substantive testing

6. Generally use data aggregated at a

lower level than the other stages.

b. Substantive testing

7-17

7-33 (continued)

STATEMENT

RELATED STAGE OF AUDIT

7. Should include reading the financial

statements and notes to consider the

adequacy of evidence gathered.

c. Overall review

8. Not required during this stage.

b. Substantive testing

9. Involve reconciliation of confirmation

replies with recorded book amounts.

d. Statement is not correct concerning

analytical procedures

10. Use the preliminary or unadjusted

working trial balance as a source of

data.

a. Planning the audit

7-34 a. The company’s financial position is deteriorating significantly. The

company’s ability to pay its bills is marginal (quick ratio = 0.97), and

its ability to generate cash is weak (days to convert inventory to

cash = 266.7 in 2016 versus 173.8 in 2012). The earnings per share

figure is misleading because it appears stable while the ratio of net

b.

ADDITIONAL INFORMATION

REASON FOR ADDITIONAL INFORMATION

1. Debt repayment

requirements, lease payment

requirements, and preferred

dividend requirements

To project the cash requirements for the next several

years in order to estimate the company’s ability to

meet its obligations.

2. Debt to equity ratio

To see the company’s capital investment and ability of

the company to exist on its present investment.

3. Industry average ratios

To compare the company’s ratios to those of the

average company in its industry to identify possible

problem areas in the company.

7-18

7-34 (continued)

ADDITIONAL INFORMATION

REASON FOR ADDITIONAL INFORMATION

4. Aging of accounts

receivable, bad debt history,

and analysis of allowance for

uncollectible accounts

To see the collection potential and experience in

accounts receivable. To compare the allowance for

uncollectible accounts to the collection experience

and determine the reasonableness of the allowance.

5. Aging of inventory and

history of markdown taken

To compare the age of the inventory to the markdown

experience since the turnover has decreased

significantly. To evaluate the net realizable value of

the inventory.

6. Short- and long-term liquidity

trend ratios

To indicate whether the company may have liquidity

problems within the next five years.

1. Ability of the company to continue to acquire inventory, replace

2. Reasonableness of the allowance for uncollectible accounts

increase in days to collect receivables.

3. Reasonableness of the inventory valuation based on the

4. Computation of the earnings per share figure. It appears