Statistical sampling eliminates any professional judgment for the auditor.

In the scope paragraph of the audit report issued for financial statements of a nonpublic

company, the auditor expresses an opinion about the internal controls of the company.

According to the Association of Certified Fraud Examiners, losses from

misappropriation schemes are higher than losses from financial statement frauds.

The objectives of internal auditors are considerably broader than the objectives of

external auditors.

The two most important factors when determining the appropriate sample size in an

audit are the auditor’s expectation of misstatements and the objectivity of the evidence.

Auditors are not always required to obtain bank confirmations.

An auditor should issue a qualified opinion with an explanatory paragraph whenever

there is a material uncertainty affecting the financial statements.

In a Type 2 engagement, the service auditor performs tests of the operating

effectiveness of the controls, but does not have to perform any of the procedures

performed in a Type 1 engagement.

If an attorney refuses to provide the auditor with information about material existing

lawsuits or unasserted claims, current professional standards require that the auditor

consider the refusal as a scope limitation.

Tracing outstanding checks to subsequent period bank statements tests the cutoff audit

objective.

A large portion of errors in IT systems result from data entry errors.

Assessing internal controls related to financial instruments may be necessary in order to

reduce audit risk to an acceptable level.

Tracing from source documents to the journal is useful for testing the existence

objective.

An integrated approach to auditing considers both the risk of misstatements and

operating controls intended to prevent misstatements.

The tolerable exception rate is the rate that the auditor will permit in the population and

still be willing to conclude a control is effective.

In a preparation service, if the financial statements are expected to be used by a third

party, the accountant must provide at least minimal assurance on the financial

statements.

Stratification of accounts receivable is desirable when using confirmations.

Auditors should obtain copies of the client’s code of ethics and minutes of the meetings

of the board of directors to aid in their understanding of the company’s management and

governance structure.

A tour of the client’s facilities can help the auditor assess physical safeguards over

assets and interpret accounting data related to assets such as factory equipment.

For most clients, the balance sheet accounts related to payroll are normally

insignificant, except for labor charged to inventory.

Because fraud perpetrators are often knowledgeable about audit procedures, auditors

should incorporate unpredictability into the audit plan.

When developing the audit objectives, the first step is to divide the financial statements

into cycles.

AICPA auditing standards provide uniform wording for the auditor’s report to enable

users of the financial statements to understand the audit report.

Transactions with related parties must be disclosed in the financial statements if they

are deemed to be material.

An example of auditor legal liability to third parties under common law would be the

federal government prosecuting an auditor for knowingly issuing an incorrect audit

report.

The first stop in the audit of contingencies is to determine the amount of the

contingency.

Many risks are common to all clients in certain industries.

During the professional judgment process, the analysis may identify only one

appropriate response to the issue.

To calculate the sample size using difference estimation sampling, it is not necessary

for the auditors to have an advance population standard deviation estimate.

A substantive test of transactions commonly used to test the completeness objective for

acquisitions is “Trace from a file of receiving reports to the acquisitions journal.”

To test for the completeness balance-related audit objective, the auditor should review

the accounts receivable trail balance for large or unusual items.

Despite the large dollar amounts involved in the payroll and personnel cycle, auditors

typically spend less time auditing this cycle than others.

The primary characteristic that distinguishes property, plant, and equipment from

inventory, prepaid expenses, and investments is the intention to use property, plant, and

equipment as a part of the operations of the client’s business over their expected life.

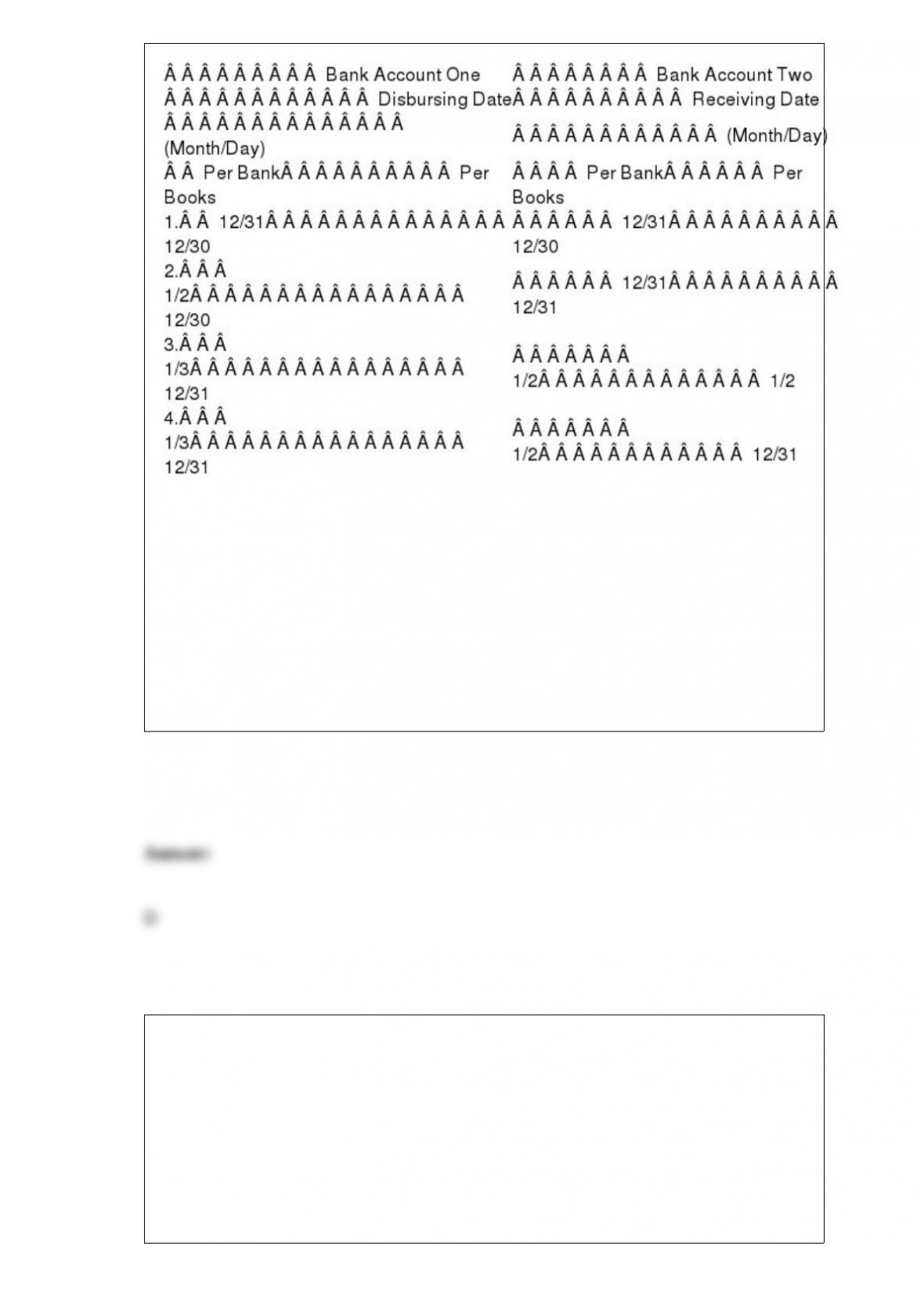

The following information applies to the questions below:

Listed below are four interbank cash transfers, indicated by the numbers 1, 2, 3, and 4,

of a client for late December 2015 and early January 2016:

Based on the schedule of interbank transfers above, which of the cash transfers would

appear as a deposit in transit on the December 31, 2015 bank reconciliation?

A) 1

B) 2

C) 3

D) 4

Auditing standards require auditors to evaluate whether there is substantial doubt about

a client’s ability to continue as a going concern. One of the most important audit

procedures to perform to assess the going concern question is

A) analytical procedures.

B) confirmations from creditors.

C) statistical sampling procedures.

D) tests of internal controls.

Which of the following audit procedures would be the most correct in determining the

audit objective of existence for the equipment account in the fixed asset master file?

A) Examine vendor invoices and receiving reports.

B) Review transactions near the balance sheet date.

C) Recalculate vendor invoices.

D) Examine vendor invoices for correct accounting treatment.

If the balance sheet of a private company is dated December 31, 2016, the audit report

is dated February 8, 2017, and both are released on February 15, 2017, this indicates

that the auditor has searched for subsequent events that occurred up to

A) December 31, 2016.

B) January 1, 2017.

C) February 8, 2017.

D) February 15, 2017.

The auditor is likely to accumulate more evidence when the audit is for a company

A)

B)

C)

D)

Which of the following is false concerning the principal CPA firm’s alternatives when

issuing a report when another CPA firm performs part of the audit?

A) Issue a joint report signed by both CPA firms.

B) Make no reference to the other CPA firm in the audit report, and issue the standard

unqualified opinion.

C) Make reference to the other auditor in the report by using modified wording (a

shared opinion or report).

D) A qualified opinion or disclaimer, depending on materiality, is required if the

principal auditor is not willing to assume any responsibility for the work of the other

auditor.

Which balance-related audit objective is important for uncovering both errors and

fraud?

A) completeness

B) existence

C) accuracy

D) detail tie-in

When making the sampling decisions for accounts receivable confirmations,

A) it is important to sample some items for every material segment of the population.

B) if management refuses to allow the auditor to send confirmation requests to certain

customers, the auditor must withdraw from the engagement.

C) inherent risk does not impact the sample size.

D) stratification of the sample is discouraged under current auditing standards.

In attributes sampling, an estimate of the expected population exception rate is

necessary to plan the sample size. The relationship of expected population exception

rate (EPER) to sample size is

A) direct (small EPER = small sample).

B) inverse (small EPER = large sample).

C) a variable (sometimes small, sometimes large) dependent on other factors present.

D) indeterminate.

The most important part of the observation of inventory is to determine whether

A) all counts are accurate.

B) the inventory-takers are qualified.

C) obsolete inventory has been identified.

D) the physical count is being taken in accordance with the client’s instructions.

When designing tests of controls and substantive tests of transactions for cash receipts,

it is important to remember that

A) the test of controls are designed to test for monetary misstatements.

B) auditors use the same methodology for designing tests of controls and substantive

tests of transactions for cash receipts as they use for sales.

C) the tests of controls are not dependent on the controls the auditor identifies.

D) the tests of controls is not dependent on whether the company being audited is

publicly traded.

Which of the following test of controls is useful to test the completeness objective for

cash receipts?

A) Compare shipping documents with sales records.

B) Observe endorsement of incoming checks.

C) Examine evidence that the receivable master file is reconciled to the general ledger.

D) Observe if the client reconciles the bank account.

Auditors begin their assessments of inherent risk during audit planning. Which of the

following would not help in assessing inherent risk during the planning phase?

A) obtaining client’s agreement on the engagement letter

B) obtaining knowledge about the client’s business and industry

C) touring the client’s plant and offices

D) identifying related parties

Most companies recognize sales revenue when

A) sales are invoiced.

B) payment is received from the customer.

C) goods are shipped.

D) the customer’s order is received.

Which of the following is a correct statement regarding audit evidence?

A) A large sample of evidence provided by an independent party is always considered

persuasive evidence.

B) A small sample of only one or two pieces of highly appropriate evidence is always

considered persuasive evidence.

C) The auditor must obtain a sufficient amount of relevant and reliable evidence to form

an opinion on the fairness of the financial statements.

D) Evidence is usually more reliable for balance sheet accounts when it is obtained

within six months of the balance sheet date.

Prenumbered documents are intended to help

A)

B)

C)

D)

Which of the following is not a correct statement regarding business risk and financial

instruments?

A) Business risks associated with financial instruments will vary depending of the

aggressiveness of a company’s investing activity.

B) Business risk will be higher for companies investing in less liquid securities.

C) Financial services firms are exposed to very little risk with their financial

instruments.

D) Business risk for a company will be higher when investments represent a greater

proportion of total assets.

Which of the following describes the process of implementing a new system in one part

of the organization, while other locations continue to use the current system?

A) parallel testing

B) online testing

C) pilot testing

D) control testing

Match seven of the terms for documents and records (a-k) with the descriptions

provided below (1-7):

a. customer order form

b. sales order

c. bill of lading

d. sales invoice

e. summary sales report

f. accounts receivable master file

g. monthly statement

h. remittance advice

i. prelisting of cash receipts

j. credit memo

k. uncollectible account authorization form

________ 1. A list prepared when cash is received by someone who has no

responsibility for recording sales, accounts receivable, or cash, and has no access to the

accounting records. It is used to verify whether cash received was recorded and

deposited at the correct amounts and on a timely basis.

________ 2. A document indicating a reduction in the amount due from a customer

because of returned goods or an allowance.

________ 3. A document prepared to initiate shipment of goods, indicating the

description of the merchandise, the quantity shipped, and other relevant data. It is a

written contract between the carrier and seller of the receipt and shipment of goods.

________ 4. A document for communicating the description, quantity, and related

information for goods ordered by a customer. This is frequently used to indicate credit

approval and authorization for shipment.

________ 5. A document mailed to the customer and typically returned to the seller

with the cash payment.

________ 6. A document used internally to indicate authority to write-off an account

receivable as uncollectible.

________ 7. A document or electronic record indicating the description and quantity of

goods sold, the price, freight charges, insurance, terms, and other relevant data.

During the course of an audit, a CPA observes that the recorded interest expense seems

to be excessive in relation to the balance in the long-term debt account. This

observation could lead the auditor to suspect that

A) long-term debt is understated.

B) discount on bonds payable is overstated.

C) long-term debt is overstated.

D) premium on bonds payable is understated.

Reasonable assurance allows for

A) low likelihood that material misstatements will not be prevented or detected by

internal controls.

B) no likelihood that material misstatements will not be prevented or detected by

internal control.

C) moderate likelihood that material misstatements will not be prevented or detected by

internal control.

D) high likelihood that material misstatements will not be prevented or detected by

internal control.

Confirmation of accounts receivable balances normally provides evidence concerning

the

A) valuation of the balances.

B) rights of the balances.

C) existence of the balances.

D) completeness of the balances.

Which of the following statements is correct when dealing with sampling for exception

rates?

A) The term exception refers to both deviations from the client’s control procedures and

amounts that are not monetarily correct.

B) When used with sampling, the term deviation is synonymous with the term

exception.

C) The actual population exception rate is the same as the sample exception rate.

D) In using audit sampling for exception rates, the auditor is most concerned with the

confidence interval.

The primary accounting record for manufacturing equipment and other fixed assets is

the

A) depreciation ledger.

B) fixed asset master file.

C) asset inventory.

D) equipment roster.

A company has changed its method of inventory valuation from an unacceptable one to

one in conformity with generally accepted accounting principles. The auditor’s report

on the financial statements of the year of the change should include

A) no reference to consistency.

B) a reference to a prior period adjustment in the opinion paragraph.

C) an explanatory paragraph that justifies the change and explains the impact of the

change on reported net income.

D) an explanatory paragraph explaining the change.

Which of the following is not an example of an applications control?

A) Back-up of data is made to a remote site for data security.

B) There is a preprocessing authorization of the sales transactions.

C) There are reasonableness tests for the unit selling price of a sale.

D) After processing, all sales transactions are reviewed by the sales department.

For which of the following audit procedures would audit sampling not be appropriate?

A) Review sales transactions for large and unusual amounts.

B) Examine a sample of duplicate sales invoices for credit approval.

C) Compare the quantity on duplicate sales invoices with the quantity on related

shipping documents.

D) Audit sampling is appropriate for each of the above procedures.

Which of the following is an accurate statement regarding assets and fraud risk?

A) Companies will often capitalize repairs as fixed assets.

B) Since fixed assets are often large, there is little theft of fixed assets.

C) Intangible assets are recorded at cost and valuation issues therefore are not a fraud

risk.

D) Since companies have few fixed assets, there is no need for them to be periodically

inventoried.

If the auditor decides not to confirm accounts receivable that are material, the auditor

should

A) always use alternative procedures to audit the accounts receivable.

B) include copies of customer statements in the audit files.

C) document the reasons for such a decision in the audit files.

D) include copies of customer sales invoices in the audit files.

Absent disputed amounts and minor timing differences, the vendor’s statements should

reconcile to the

A) acquisition journal.

B) accounts payable master file.

C) cash disbursements amount for purchases.

D) vouchers payable amount for vendors.

The auditor’s best defense when material misstatements are not uncovered is to have

conducted the audit

A) in accordance with generally accepted auditing standards.

B) as effectively as reasonably possible.

C) in a timely manner.

D) only after an adequate investigation of the management team.

The inventory and warehousing cycle can be thought of as having two separate but

closely related systems, one involving the actual physical flow of goods, and the other

the

A) related costs.

B) storage of the goods.

C) internal control over those goods.

D) prevention of waste, obsolescence, and theft.

When auditing accounting data, auditors focus on

A) determining whether recorded information properly reflects the economic events

that occurred during the accounting period.

B) determining if fraud has occurred.

C) determining if taxable income has been calculated correctly.

D) analyzing the financial information to be sure that it complies with government

requirements.

Discuss the key internal controls that should be present in the processing purchase

ordersfunction in the acquisitions and payment cycle.

Discuss each of the three phases of an operational audit.

Auditors generally use a financial statement cycle approach when performing a

financial statement audit. Describe the transaction flow, using specific examples, from

journals to financial statements that produce financial statements.

Briefly explain each management assertion related to presentation and disclosure.

Discuss each of the four defenses a CPA firm can normally use when facing legal

claims by clients.

Listed below are some management assertions made for the acquisition and payment

cycle. For each one give an example of how the auditor by using the documents

normally found in the process can apply an auditing procedure to test the assertion.

completeness

timing

accuracy

From an internal control perspective, what challenges arise when a company outsources

computer functions?

Discuss the sanctions the Securities and Exchange Commission can impose on auditors.

Generally, is the inherent risk level for the audit of the payroll and personnel set at low,

moderate, or high? Explain.

Discuss some of the steps practicing auditors can take to minimize their legal liability.

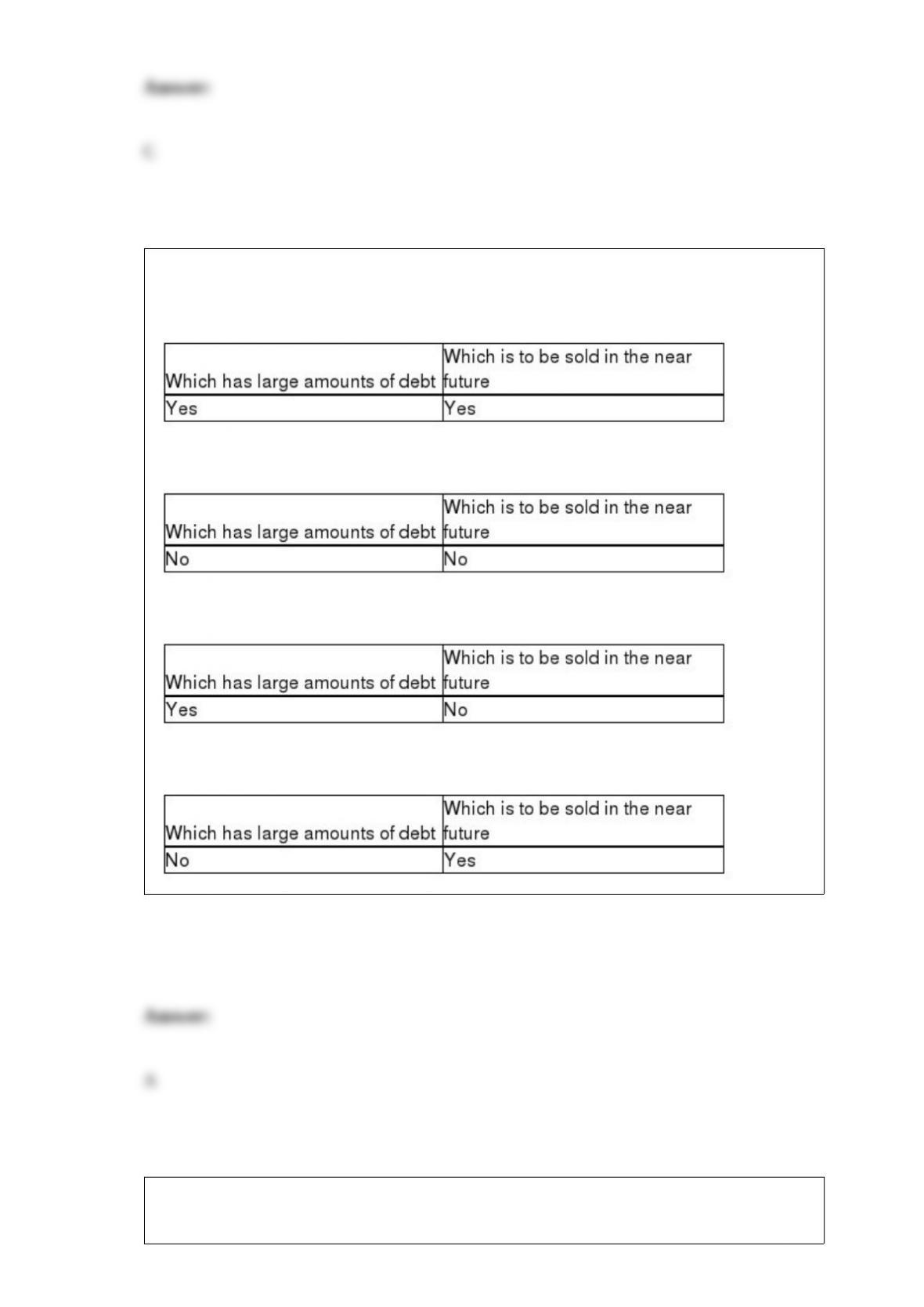

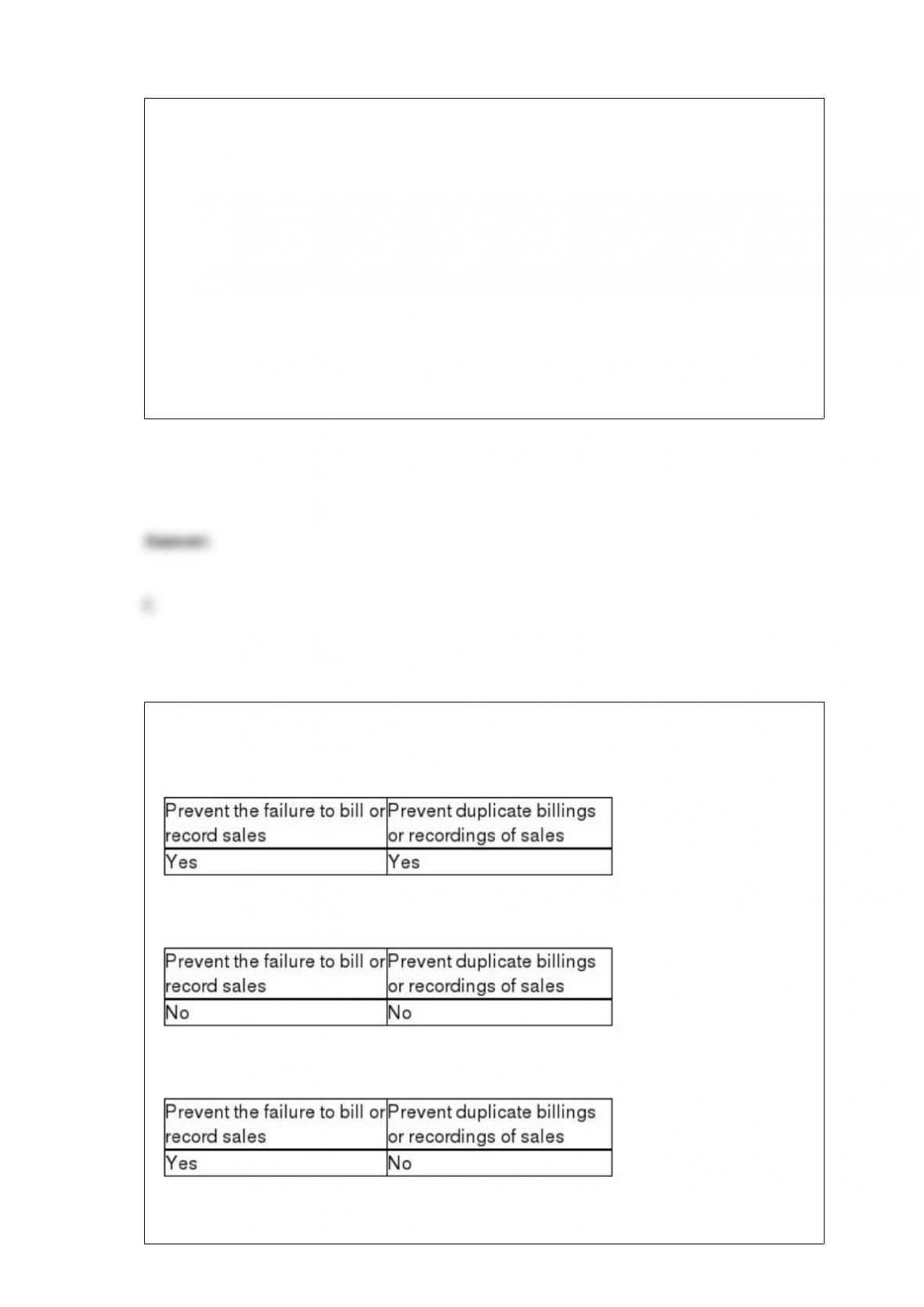

In practice, auditors rarely assign numerical probabilities to inherent risk, control risk,

or acceptable audit risk. It is more common to assess these risks as high, medium, or

low. For each of the four situations below, fill in the blanks for planned detection risk

and the amount of evidence you would plan to gather (“planned evidence”) using the

terms high, medium, or low.

Describe how the auditor tests the accuracy objective for accounts receivable.

What is the key advantage and disadvantage associated with systematic sample

selection? How must auditors address this disadvantage?

Explain kiting, and discuss how it is performed.

The Institute of Internal Auditors has established Ethical Principles for its members.

List each of the principles.

The risk of material misstatement is a combination of two client controlled factors:

inherent risk and control risk. What is inherent risk, why is it important and give

examples of inherent risk factors.

Describe what analytical procedures and tests of details of balances are and give an

example of each.

When a company maintains its own records of stock transactions and capital stock

outstanding, its internal controls must be adequate to accomplish three objectives. List

them below.

Discuss the Confidential Client Information Rule, including the four exceptions to the

rule.