19–11

19–25 a. Both U.S. GAAP and IFRS standards generally contain similar

requirements for assessing the impairment of assets, including

value of goodwill exceeds its fair value.

b. The auditor would need to examine evidence and assumptions

management used to determine its estimate of the fair value of

goodwill, which is used to determine the impairment amount.

future developments.

c. Arriving at estimates of expected discounted future cash flows of a

business can be extremely complex, requiring an extensive amount

of business judgment. Because financial statement auditors may

macroeconomic conditions, industry and market conditions,

anticipated changes in costs of business, and other relevant

company–specific events, among a number of other matters.

Business valuation specialists have unique skills and

values are reasonable and appropriate.

Case – Ward Publishing Company

and lease acquisitions and cash disbursements, even though the

specific sample tested does not include any such transaction.

Thus, if the results of the tests are favorable, it is concluded that

19–12

19–26 (continued)

met at a satisfactory level except:

1. All supporting documents are not always attached to the

their estimate of CUER. However, most students will likely

conclude that the results are unacceptable.

2. All vendors’ invoices are not initialed for internal

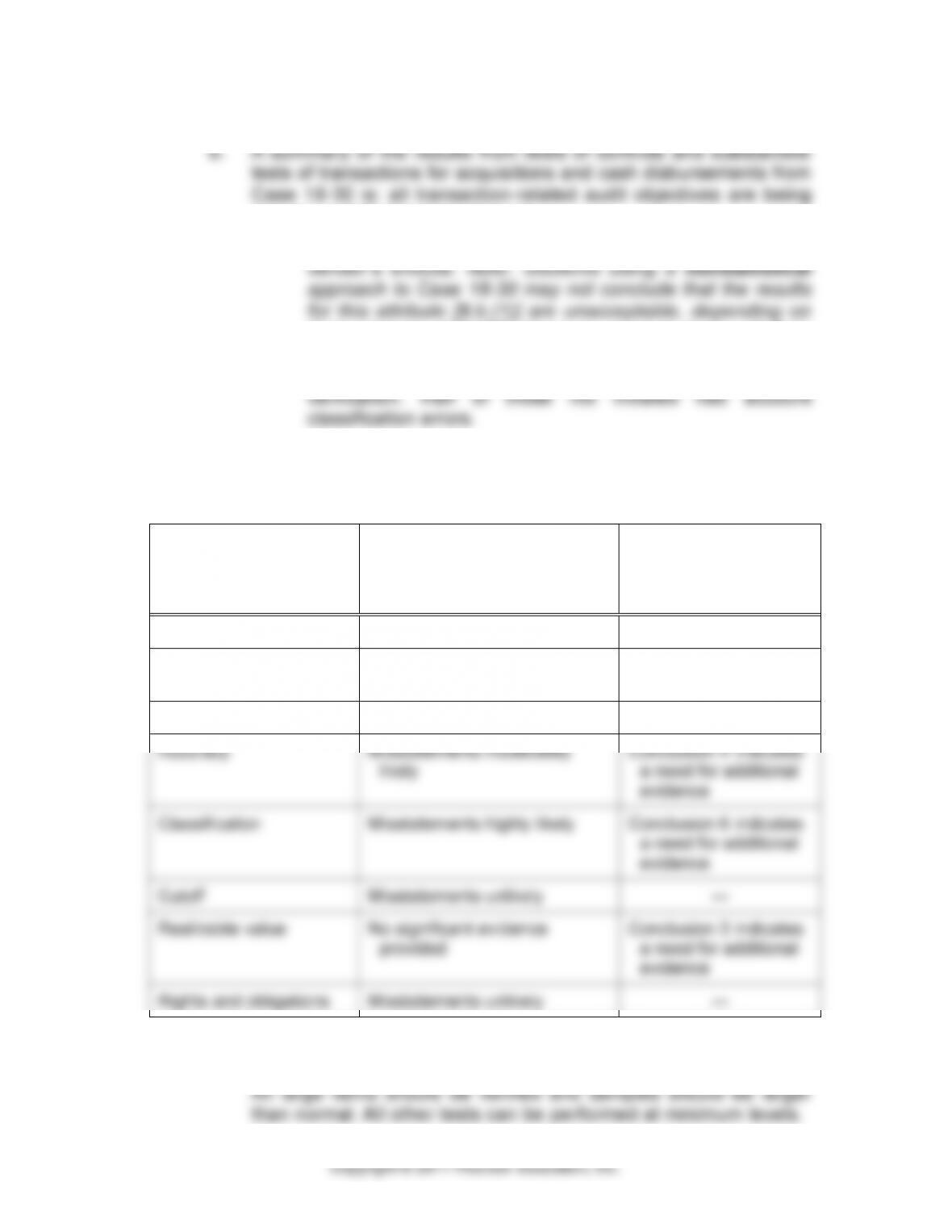

The impact of these results and the results from items 1

through 7 affect the balance–related audit objectives for plant and

equipment in the following way:

BALANCE–RELATED

AUDIT OBJECTIVE

RESULTS OF

TESTS OF CONTROLS AND

SUBSTANTIVE TESTS OF

TRANSACTIONS

RESULTS FROM

CONCLUSIONS 1–7

Detail tie–in

Misstatements unlikely

—

Existence

Misstatements moderately

likely

—

Completeness

Misstatements unlikely

Conclusion 1 supports

Accuracy

Misstatements moderately

likely

Conclusion 4 indicates

a need for additional

evidence

Classification

Misstatements highly likely

Conclusion 6 indicates

a need for additional

evidence

Cutoff

Misstatements unlikely

—

Realizable value

No significant evidence

provided

Conclusion 3 indicates

a need for additional

evidence

Rights and obligations

Misstatements unlikely

—

Conclusions 3, 5, and 7 indicate a need for more extensive

auditing for existence, completeness, accuracy, and classification.

19–13

19–14

19–26 (continued)

c. The results of tests of controls and substantive tests of transactions

are directly related to the tests of many expense accounts,

primarily through tests for account classification, but also through

tests of accuracy and existence. For example, if the auditor

concludes that the internal controls are effective for recording

acquisition transactions, the likelihood of misstatements for accounts

such as supplies, purchases, and repairs and maintenance is

d. The results of tests of controls and substantive tests of transactions

indicate the potential for significant classification misstatements.

(See the results for Audit Procedure 9b(5) for classification in Part

2 of Case 18–30.) This potential for misclassification misstatement

combined with the substantive analytical procedures results in

19–27 a. Items 1 through 6 would have been found in the following way:

1. The company’s policies for depreciating equipment are

available from several sources:

Form 10–K.

c) Company procedures manuals.

d) Detailed fixed asset records.

2. The ten–year lease contract would be found when supporting

data for current year’s equipment additions were examined.

19–15

19–27 (continued)

3. The building wing addition would be apparent by the addition

method was followed, the actual costs could be determined

4. The paving and fencing could be discovered when support

was examined for the addition to land.

5. The details of the retirement transactions could be deter–

retirement in the machinery account or the review of cash

receipts records.

6. The auditor would become apprised of a new plant in several

ways:

a) Volume would increase.

location.

c) The transaction may be indicated in documents such

as the minutes of the board, press releases, and

reports to stockholders.

new plant.

One or more of these occurrences should lead the

auditor to investigate the reasons and circumstances

examined to determine the details involved.

b. The appropriate adjusting journal entries are as follows:

1. No entry necessary.

19–16

19–27 (continued)

2. This is an operating lease and should not have been

capitalized.

Prepaid rent $ 50,000

Lease liability 354,000

9/12 x $50,000 = $37,500

3. The wing should have been recorded at its cost to the

company.

(Accounts originally credited) $15,000

Buildings $15,000

calculations:

Depreciation on beginning balance

1,200,000/25 = 48,000

Depreciation recorded on addition

51,500 – 48,000 = 3,500

Correct depreciation for addition:

Remaining useful life of addition is 12 years