An auditor must evaluate a specialist’s professional qualifications and understand the

objectives of the specialist’s work.

The starting point for the verification of the balance in the general bank account is to

obtain a bank cut-off statement.

When there are a number of controls tested in prior audits that have not been changed,

auditing standard require auditors to test some of those controls each year to ensure

there is a rotation of controls testing throughout the three-year period.

An independent review must be performed of all audits.

The Conceptual Framework for AICPA Independence Standards can be used when

making decisions on ethical matters not explicitly addressed in the Code.

Auditing standards require a written audit program.

To determine the sampling interval, the population is divided by the confidence factor.

A common source of business risk for inventory is the reliance on a few key suppliers.

Auditing standards prohibit reliance on the work of internal auditors due to the lack of

independence of the internal auditors.

The auditor obtains a sufficient understanding of internal control to assess the risk of

material misstatement at the overall financial statement level and at the relevant

assertion level.

The phrase “accounting principles generally accepted in the United States of America”

can be found in the opinion paragraph of a standard unmodified opinion report.

Because of confidentiality requirements and potential losses of payroll funds, outside

service center systems are rarely used by companies for payroll-related functions.

The SEC requires the auditors of public companies to retain e-mail correspondence

related to the audit.

Accounts that require considerable judgment have a higher inherent risk.

Auditing capital stock transactions as part of a merger is challenging because judgment

is often involved.

Inherent risk and control risk are directly related.

The pressure to do “whatever it takes” to meet goals is one of the main reasons why

financial statement fraud occurs.

The PCAOB requires annual inspections of accounting firms that audit more than ten

public companies.

The upper limit of the interval estimate is also known as the confidence interval.

An engagement letter establishes a clear understanding of the terms of the engagement

between the client and the auditor.

In the audit of inventory, the auditor and client are jointly responsible for making and

recording the count of physical inventory; while the auditor is responsible for drawing

conclusions about the adequacy of the physical inventory.

The receipt of a customer order from a customer is the starting point for the entire sales

and collection cycle.

The auditor’s responsibility for reviewing subsequent events is normally limited to

thirty days after the balance sheet date.

The primary purpose of a surprise payroll payoff is to detect employees who have

reported more time than was actually worked (fraudulent hours).

Examining payroll records for an indication of authorization is part of the timing

transaction-related audit objective.

Section 404 of the Sarbanes-Oxley Act requires that both private and public companies

issue an internal control report.

When auditing financial instruments, the most difficult objective to test is existence.

For most audits, a proper cash receipts cutoff is less important than either the sales or

the sales returns and allowances cutoff since cash only affects the balance sheet, and not

earnings.

The starting point for testing the ending balance of financial instruments accounts is to

obtain a gain or loss schedule for the year.

Financial statement users are typically more concerned with an unmodified report with

explanatory paragraphs than they are with a disclaimer of opinion.

For a public company, the Sarbanes-Oxley Act requires audit committee approval of all

nonaudit services prior to their performance by the company’s external auditor.

In stratified sampling, a maximum of four stratum can be used.

In the audit of accrued property taxes, the two most important balance-related audit

objectives are completeness and accuracy.

In IT systems, if general controls are effective, it increases the auditor’s ability to rely

on application controls to reduce control risk.

When performing inventory valuation tests, the auditor must be concerned that the

method is in accordance with accounting standards.

When may auditors observe the physical inventory count?

A)

B)

C)

D)

If a short-term note payable is included in the accounts payable balance on the financial

statement, there is a violation of the

A) completeness assertion.

B) existence assertion.

C) cutoff assertion.

D) classification assertion.

Which of the following is not one of the five Trust Services principles?

A) security

B) confidentiality

C) completeness

D) availability

Financial instruments

A) include debt securities and money market funds.

B) such as derivatives can be used as a way of hedging.

C) must be classified as held-to-maturity securities.

D) All of the above are correct.

William Gregory, CPA, is the principal auditor for an international corporation. Another

CPA has examined and reported on the financial statements of a significant subsidiary

of the corporation. Gregory is satisfied with the independence and professional

reputation of the other auditor, as well as the quality of the other auditor’s examination.

With respect to his report on the consolidated financial statements, taken as a whole,

Gregory

A) must not refer to the examination of the other auditor.

B) must refer to the examination of the other auditor.

C) may refer to the examination of the other auditor.

D) must refer to the examination of the other auditors along with the percentage of

consolidated assets and revenue that they audited.

If an auditor fails to fulfill a certain requirement in the contract, they may be guilty of

A) contract fraud.

B) breach of contract.

C) constructive fraud.

D) criminal neglect.

After the balance sheet date, but prior to the issuance of the audit report, the client

suffers an uninsured loss of their inventory as a result of a fire. The amount of the loss

is material. The auditor should

A) adjust the financial statements for the year under audit.

B) add a paragraph to the audit report.

C) advise the client to disclose the event in the notes to the financial statements.

D) advise the client to delay issuing the financial statements until the economic loss can

be determined.

When setting a preliminary judgment about materiality,

A) more evidence is required for a low dollar amount than for a high dollar amount.

B) less evidence is required for a low dollar amount than for a high dollar amount.

C) the same amount of evidence is required for either low or high dollar amounts.

D) there is no relationship between materiality and the dollar amount of evidence

needed.

Which of the following statements is true with respect to audit committees?

A) Audit committee members should consist of members of the company’s

management.

B) All members of the audit committee must be financial experts.

C) The audit committee of a public company is responsible for hiring the auditor.

D) Audit committees must have a minimum of ten members.

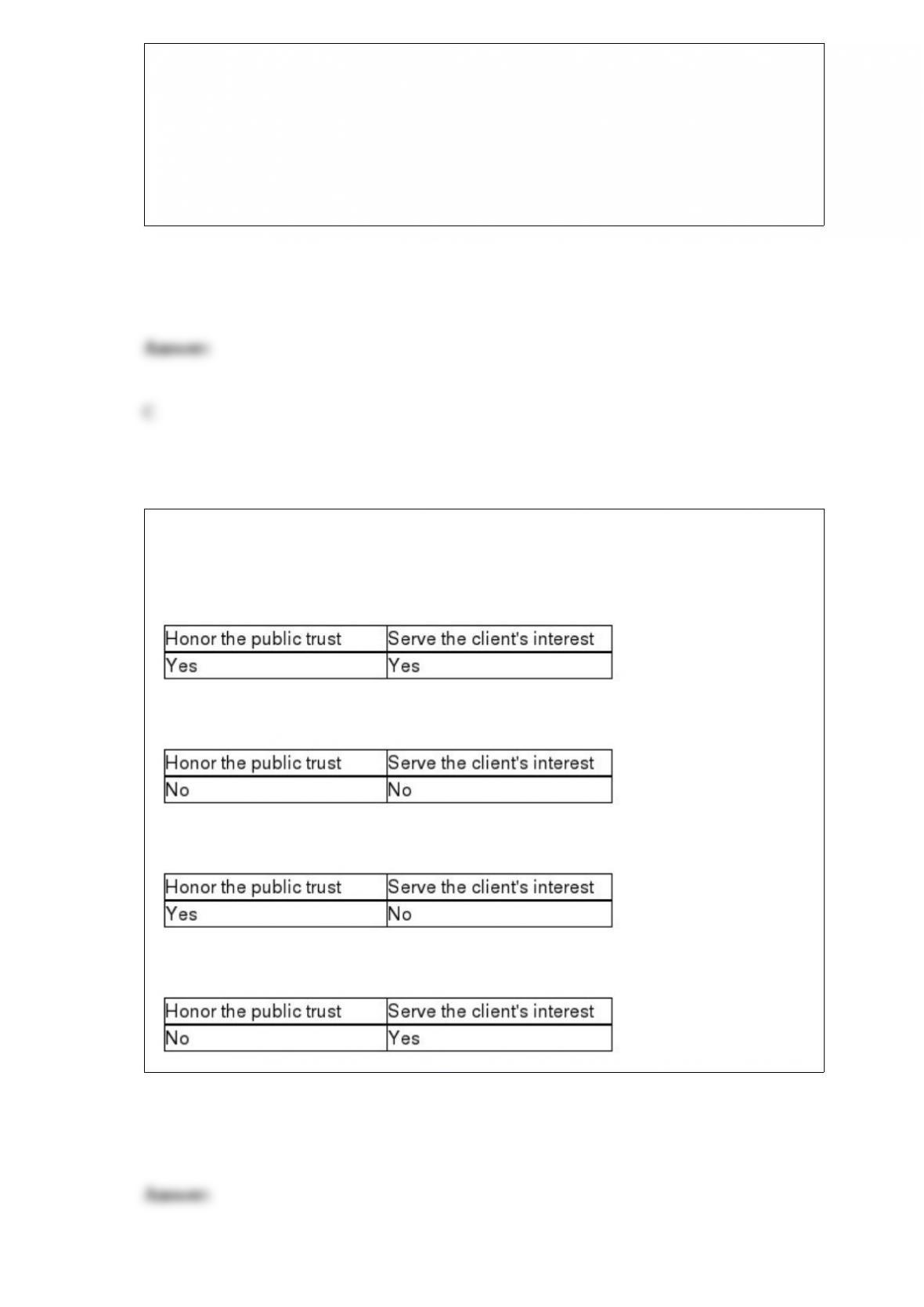

One of the AICPA’s Ethical Principles deals with the public interest. It states that

members should accept the obligation to act in a way that will

A)

B)

C)

D)

The standard unmodified audit report

A) is sometimes called a clean opinion.

B) can be issued only with an explanatory paragraph.

C) can be issued if only a balance sheet and income statement are included in the

financial statements.

D) is sometimes called a disclaimer report.

When auditing inventory cost accounting, the auditor is concerned with all of the

following except for

A) net realizable value.

B) unit cost records.

C) physical controls over inventory.

D) documents and records for transferring inventory.

Which of the following balance-related audit objectives is not applicable to the audit of

notes payable?

A) realizable value

B) detail tie-in

C) cutoff

D) classification

An official record of meetings of the board of directors and stockholders is included in

the corporate

A) bylaws.

B) charter.

C) minutes.

D) license.

When auditors use documentation to support recorded transactions and amounts, the

process is usually called

A) tracing.

B) confirmations.

C) vouching.

D) reperformance.

An auditor is comparing the write-off of uncollectible accounts as a percentage of total

accounts receivable with previous years. A possible misstatement this procedure could

uncover is

A) overstatement or understatement of sales.

B) overstatement or understatement of accounts receivable.

C) overstatement or understatement of bad debt expense.

D) overstatement or understatement of sales returns and allowances.

Statements on Standards for Attestation Engagements (SSAEs ) are issued by the

Auditing Standards Board of the AICPA.

What event initiates a transaction in the sales and collection cycle?

A) receipt of cash

B) delivery of product to a customer

C) identification of a new customer

D) customer request for goods or services

Auditors follow a four step approach to reduce assessed control risk. Which of the

following is not one of the four?

A) Apply transaction-related audit objectives to a class of transactions.

B) Identify accounts that have high inherent risk.

C) Identify key controls that reduce control risk.

D) For potential misstatements, design appropriate substantive tests of transactions.

Which of the following is not one of the subcomponents of the control environment?

A) management’s philosophy and operating style

B) organizational structure

C) adequate separation of duties

D) commitment to competence

When the auditor decides to select less than 100 percent of the population for testing,

the auditor is said to use

A) audit sampling.

B) representative sampling.

C) poor judgment.

D) estimation sampling.

One of the primary objectives in examining the repairs and maintenance accounts is to

obtain evidence that

A) expenditures of equipment have not been charged to expense.

B) the actual amount recorded is the same as the budgeted amount.

C) expenditures for equipment have been recorded in the proper period.

D) revenue expenditures made on behalf of equipment have been recorded in the proper

period.

Planned detection risk

I. determines the amount of substantive evidence the auditor plans to accumulate.

II. is dependent on inherent risk and business risk.

A) I only

B) II only

C) I and II

D) neither I nor II

Assume that the client’s valuation of an inventory item is $10 per unit for 1,000 units,

using first-in, first-out (FIFO). If the most recent acquisition of inventory was for 600

units at $10 per unit and the immediately preceding acquisition was for 700 units at $9

per unit, the inventory item is in error and it is

A) understated $400.

B) understated $300.

C) overstated $400.

D) overstated $700.

Which of the following discoveries through the use of analytical procedures would

most likely indicate a relatively high risk of financial failure?

A) a decline in gross margin percentages

B) an increase in the balance in fixed assets

C) an increase in the ratio of allowance for uncollectible accounts to gross accounts

receivable, while at the same time accounts receivable turnover also decreased

D) a higher than normal ratio of long-term debt to net worth as well as a lower than

average ratio of profits to total assets

The auditor would design which of the following audit tests to detect possible monetary

errors in the financial statements?

A) control tests

B) substantive analytical procedures

C) risk assessment procedures

D) tests of operating effectiveness of controls over revenue and cash

There are three reasons why an experienced member of the audit firm must thoroughly

review audit documentation of the completion of the audit, including

A) to evaluate the performance of inexperienced personnel.

B) to make sure that the audit meets the CPA firm’s standard of performance.

C) to counteract the bias that often enters into the auditor’s judgment.

D) all of the above.

A ________ risk represents an identified and assessed risk of material misstatement

that, in the auditor’s professional judgment, requires special audit consideration.

A) material

B) substantial

C) financial statement

D) significant

Auditors are likely to prepare a proof of cash when the client has

A) material internal control weaknesses in cash.

B) material internal control weaknesses in accounts receivable and revenue.

C) material internal control weaknesses in accounts payable and inventory.

D) material internal control weaknesses in payroll.

When analyzing the various types of opinions that the auditor can issue,

A) an adverse opinion must contain the phrase “except for” in the opinion paragraph.

B) an adverse opinion can only be issued when there is a lack of knowledge by the

auditor.

C) a disclaimer of opinion can be issued for material or immaterial misstatements.

D) a qualified opinion report can be used only when the auditor concludes that the

overall financial statements are fairly stated.

For which of the following professional services must CPAs be independent?

A) management advisory services

B) audits of financial statements

C) preparation of tax returns

D) all of the above

Using your knowledge of the relationships among acceptable audit risk, inherent risk,

control risk, planned detection risk, performance materiality, and planned evidence,

state the effect on planned evidence (increase or decrease) of changing each of the

following factors, while the other factors remain unchanged.

1. an increase in acceptable audit risk ________

2. an increase in inherent risk ________

3. a decrease in control risk ________

4. an increase in planned detection risk ________

5. an increase in performance materiality ________

Discuss each of the following documents and records used in the timekeeping and

payroll preparationfunction in the payroll and personnel cycle: time record, job time

ticket, payroll transaction file, payroll journal and payroll master file.

Discuss what is meant by ‘sampling risk” and “nonsampling risk.”

Describe purchase requisitions and purchase orders. What is a key difference between

the two documents?

Explain the purpose of testing the client’s bank reconciliation, and discuss the major

audit procedures involved.

There are four major sources of an auditor’s legal liability. One source is liability to the

audit client. List the other three sources.

In auditing depreciation expense, one of the auditor’s concerns is determining that the

client’s calculations are correct. In making this determination, the auditor must weigh

four considerations. List these four considerations.

Describe the two tests auditors can perform to test for the existence and completeness

of insurance policies in force.

Define the term contingent liability and discuss the criteria accountants and auditors use

to classify these accounting events.

Explain each of the following types of documents and indicate the class of transactions

in which they are commonly used.

1. customer order

2. shipping document

3. remittance advice

4. sales returns and allowance journal

5. uncollectible account authorization form

State three types of assurance services that fall within the auditing standards but are not

audits, reviews, or compilations of financial statements in accordance with GAAP.

Distinguish between what is meant by business failure and audit failure.

Identify three substantive analytical procedures commonly performed for notes payable.

When performing an attestation engagement, a CPA is required to adhere to the

Statements on Standards for Attestation Engagements. Describe below the Standards of

Field Work for attestation engagements.

One category of general controls is physical and online access controls. Describe the

control and give at two examples of implementation of the control.

Threats to compliance with the AICPA’s Code of Professional Conduct fall into seven

broad categories. List and explain three of these categories.