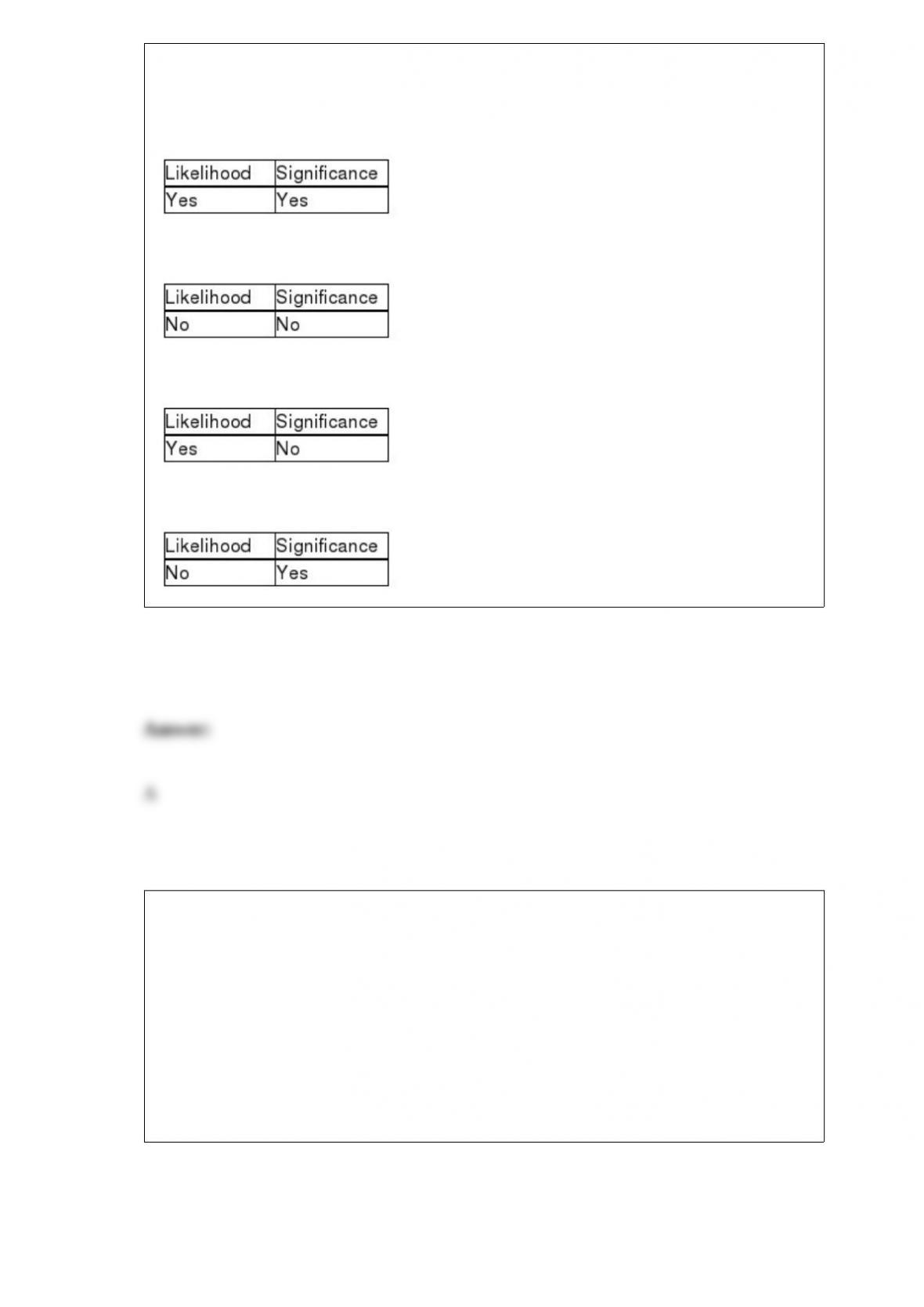

To determine if significant internal control deficiencies are material weaknesses, they

must be evaluated on their

A)

B)

C)

D)

Which of the following includes all payroll transactions processed by the accounting

system for a given period of time?

A) payroll journal

B) payroll transaction file

C) time report

D) payroll summary

Which audit procedure would the auditor use to test for the cutoff balance-related audit

objective?

A) Review minutes of the board of directors meetings.

B) Review the accounts receivable trial balance for large items.

C) Use audit software to foot and cross-foot the aged trial balance.

D) Select the last 20 sales transaction from the current year’s sales journal and the first

20 from the subsequent year’s and trace each to the related shipping documents.

Which of the following statements regarding types of operational audits is likely

incorrect?

A) A functional audit has the advantage of permitting specialization by auditors.

B) An advantage of functional auditing is its ability to evaluate interrelated functions.

C) The emphasis in an organizational audit is on how efficiently and effectively

functions interact.

D) Special operational auditing assignments arise at the request of management.

Which of the following services provides the lowest level of assurance on a financial

statement?

A) review

B) audit

C) Neither service provides assurance on financial statements.

D) Each service provides the same level of assurance on financial statements.

The risk that audit evidence for an audit objective will fail to detect misstatements

exceeding performance materiality levels is

A) audit risk.

B) control risk.

C) inherent risk.

D) planned detection risk.

________ risk represents the auditor’s assessment of the susceptibility of an assertion to

material misstatement, before considering the effectiveness of the client’s internal

control.

A) Material

B) Account balance

C) Control

D) Inherent

When auditors examine vendors’ statements or receive confirmations, there must be a

reconciliation of the statement or confirmation with the

A) accounts payable list.

B) vendors’ invoices.

C) purchase orders.

D) receiving reports.

Which is a true statement about audit risk?

A) Audit risk measures the risk that a material misstatement could occur and not be

detected by internal control.

B) When auditors decide on a higher acceptable audit risk, they want to be more certain

that the financial statements are not materially misstated.

C) Audit assurance is the complement of acceptable audit risk.

D) There is an inverse relationship between acceptable audit risk and planned detection

risk.

A related party transaction may be indicated when another company

A) subsidizes certain operating expenses of the company.

B) purchases its securities at their fair value.

C) loans to company at market rates.

D) has had a distributor relationship with the company for 10 years.

Under which of the following circumstances would it be advisable for the auditor to

confirm accounts payable with creditors?

A) The internal accounting control over accounts payable is effective, and there is

sufficient evidence on hand to minimize the risk of a material misstatement.

B) The confirmation response is expected to be favorable, and accounts payable

balances are of immaterial amounts.

C) The creditor statements are not available and internal control over payables is

deficient.

D) The majority of accounts payable balances are with associated companies.

If the financial statements include an income statement and a balance sheet but exclude

the statement of cash flows, the auditors

A) can issue an unqualified report.

B) should issue a qualified opinion due to the departure from GAAP.

C) should issue a qualified opinion because the missing statement of cash flows

constitutes a scope limitation.

D) should include the statement of cash flows, modify the report and issue an

unqualified opinion.

Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

When an auditor tests to determine if all existing accounts receivable are included in the

aged trial balance,

A) they cannot rely on the self-balancing nature of the accounts receivable master file.

B) if all sales to a customer are omitted from the sales journal, it is easy to uncover the

understatement of accounts receivable by tests of details of balances.

C) auditors rarely send accounts receivable confirmations to customers with zero

balances.

D) unrecorded sales to a new customer are easy to identify for confirmation because

that customer is included in the accounts receivable master file.

Assessed control risk and results of substantive tests of transactions are normally

unimportant for designing tests of details of balances for which of the following

accounts?

A) accounts receivable

B) inventory

C) accounts payable

D) notes payable

Fraudulent financial reporting

A) always involves inadequate disclosures.

B) can be intentional or unintentional.

C) can involve understating net income in order to reduce income taxes.

D) all of the above

Which of the following is true regarding audit risk for segments?

A) Control risk must be assessed at the same level for all accounts.

B) Factors affecting inherent risk do not differ from account to account.

C) Acceptable audit risk is ordinarily assessed by the auditor during the substantive test

of balances phase and is held constant for each major cycle and account.

D) In some cases, a lower acceptable audit risk may be more appropriate for one

account than for others.

If a client has violated federal tax laws,

A) the auditor must notify the IRS.

B) and the amount is significant, the auditor should communicate with those charged

with governance.

C) the noncompliance generally will not impact the financial statements.

D) the auditor does not need to evaluate the effects of the noncompliance on other

aspects of the audit.

You are auditing the acquisition and payment cycle and note the presence of excessive

recurring losses on retired assets. You may conclude that

A) insured values are greater than book values.

B) there are a large number of fully depreciated assets.

C) depreciation charges may by insufficient.

D) the company has a policy of selling relatively new assets.

Recording, classifying, and summarizing economic events in a logical manner for the

purpose of providing financial information for decision making is commonly called

A) finance.

B) auditing.

C) accounting.

D) economics.

To obtain reasonable assurance about whether the financial statements as a whole are

free from material misstatement, the auditor must fulfill several performance

responsibilities, including

A) verifying that all audit work is performed by a CPA with a minimum of three years’

experience.

B) obtaining sufficient, appropriate audit evidence.

C) exercising professional judgment.

D) providing an opinion on the financial statements.

If planned detection risk is reduced, the amount of evidence the auditor accumulates

will

A) increase.

B) decrease.

C) remain unchanged.

D) be indeterminate.

Which is not one of the tests that would be used in the audit of equipment, depreciation

expense, and accumulated depreciation?

A) Verify the ending balance in the asset account.

B) Send confirmations to the sales personnel who sold the equipment to the company.

C) Perform substantive analytical procedures.

D) Verify current year acquisitions.

A ________ exists if one or more control deficiencies exist that are less severe than a

material weakness, but are important enough to merit attention by those responsible for

oversight of the company’s financial reporting.

A) potential misstatement

B) significant weakness

C) significant deficiency

D) fraud symptom

Which of the following cycles does not affect cash in bank?

A) capital acquisitions cycle

B) inventory and warehousing

C) payroll and personnel cycle

D) acquisitions and disbursements

An auditor using nonstatistical sampling cannot formally measure sampling error and

therefore must subjectively consider the possibility that the true population

misstatement exceeds a tolerable amount. Which of the following factors should be

considered by the auditor in making this assessment?

A)

B)

C)

D)

The “Principles Underlying an Audit in Accordance with Generally Accepted Auditing

Principles” provides a framework to help auditors

A) understand the ten GAAS standards.

B) obtain complete assurance that the financial statements are free from any error.

C) report on the financial statements.

D) prevent fraud.

Which of the following loans would be prohibited between a CPA firm or its members

and an audit client?

A) automobile loans

B) loans fully collateralized by cash deposits at the same financial institution

C) new home mortgage loans

D) unpaid credit card balances not exceeding $10,000 in total

When determining the timing of the accounts receivable confirmations,

A) the receivables cannot be confirmed at an interim date.

B) if accounts receivable are confirmed before year-end, the auditor typically prepares a

roll-forward schedule.

C) if the receivables are confirmed at an interim date, they must also be confirmed at

year-end.

D) if internal controls are adequate, the accounts receivable must be confirmed at

year-end.

The legal right to perform audits is granted to a CPA firm by regulation of

A) each state.

B) the Financial Accounting Standards Board (FASB).

C) the American Institute of Certified Public Accountants (AICPA).

D) the Auditing Standards Board.

When there is a lack of consistent application in accounting principles

A) the nature and impact of the change should be adequately disclosed.

B) the auditor should discuss the nature of the change and point the reader to the

footnote that discusses the change.

C) the materiality of the change is evaluated based on the current year effect of the

change.

D) all of the above.

Which of the following is a correct statement?

A) There is no relationship between materiality and risk in auditing.

B) Risk is a measure of magnitude or size.

C) The combination of performance materiality and the audit risk model factors

determines planned audit evidence.

D) Performance materiality is part of the audit risk model.

________ is the information technology and internal control processes an organization

has in place to protect computers, networks, programs, and data from unauthorized

access.

A) Encryption

B) A firewall

C) Cybersecurity

D) A processing control

For clients with highly sophisticated computerized accounting systems, auditors

perform tests throughout the year to identify significant or unusual transactions. This

approach is called ________ and is frequently used in integrated audits of financial

statements and internal control for public companies.

A) continuous audit program

B) continuous auditing

C) continuous analytical testing

D) continuous audit mix