18-1

Chapter 18

Audit of the Acquisition and Payment Cycle:

Tests of Controls, Substantive Tests of Transactions,

and Accounts Payable

Concept Checks

P. 616

1. There are several balance sheet and income statement accounts related

significant income statement accounts are COGS accounts (including

expense, repairs and maintenance, or legal expense.

2. A voucher is a document used by an organization to establish a formal

recording of purchases by facilitating the recording in numerical order at

3. The point at which goods and services are received is ordinarily when title to

the goods and services passes and a liability that should be included in the

financial statements is established.

P. 623

1. The acquisition and payment cycle includes the recording of liabilities that

time, reconciling the vendors’ statements and testing the cutoff as year–end

2. It is important that the cutoff of accounts payable be coordinated with that of

the physical inventory to determine that they are established at the same

18-2

Concept Check, P. 623 (continued)

and shipping documents) to assist in the determination that an accurate

cutoff was established.

3. To test for completeness of accounts payable, the auditor conducts

various out–of-period liability tests (also called a search for unrecorded

accounts payable) designed to uncover unrecorded accounts payable.

These tests include examining underlying documentation for cash

disbursements occurring subsequent to year-end and verifying that a

Review Questions

18–1 The accounts in the acquisition and payment cycle are the following:

a. Asset accounts:

Office supplies

Delivery equipment

b. Liability accounts:

Accounts payable

Accrued property taxes

c. Expense accounts:

Purchases, purchase returns & allowances,

18-3

18–1 (continued)

Fines and penalties

Advertising expense

Repairs and maintenance

the shipment, such as unit price and freight. The vendor’s statement can be

used to verify the correct balance in accounts payable for an individual vendor.

The statement contains the ending balance and the individual transactions

period.

18–4

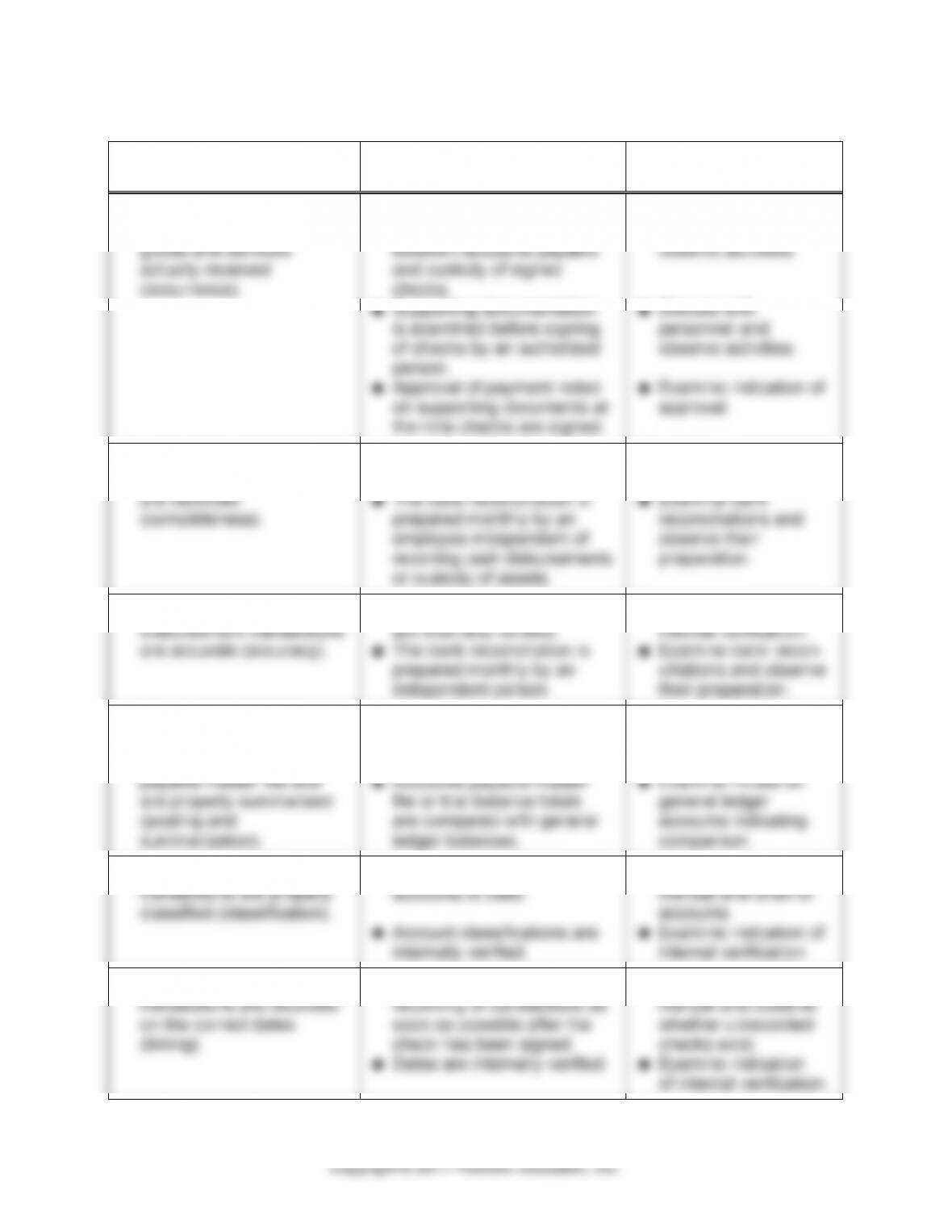

TRANSACTION–RELATED

AUDIT OBJECTIVE

POSSIBLE

INTERNAL CONTROLS

COMMON TESTS

OF CONTROLS

1. Recorded cash

disbursements are for

goods and services

actually received

(occurrence).

There is adequate

segregation of duties

between accounts payable

and custody of signed

checks.

Supporting documentation

is examined before signing

of checks by an authorized

person.

Approval of payment noted

on supporting documents at

the time checks are signed.

Discuss with

personnel and

observe activities.

Discuss with

personnel and

observe activities.

Examine indication of

approval.

2. Existing cash

disbursement transactions

are recorded

(completeness).

Checks are prenumbered

and accounted for.

The bank reconciliation is

prepared monthly by an

employee independent of

recording cash disbursements

or custody of assets.

Account for a

sequence of checks.

Examine bank

reconciliations and

observe their

preparation.

3. Recorded cash

disbursement transactions

are accurate (accuracy).

Calculations and amounts

are internally verified.

The bank reconciliation is

prepared monthly by an

independent person.

Examine indication of

internal verification.

Examine bank recon–

ciliations and observe

their preparation.

4. Cash disbursement

transactions are properly

included in the accounts

payable master file and

are properly summarized

(posting and

summarization).

Accounts payable master

file contents are internally

verified.

Accounts payable master

file or trial balance totals

are compared with general

ledger balances.

Examine indication of

internal verification.

Examine initials on

general ledger

accounts indicating

comparison.

5. Cash disbursement

transactions are properly

classified (classification).

An adequate chart of

accounts is used.

Account classifications are

internally verified.

Examine procedures

manual and chart of

accounts.

Examine indication of

internal verification.

6. Cash disbursement

transactions are recorded

on the correct dates

(timing).

Procedures require

recording of transactions as

soon as possible after the

check has been signed.

Dates are internally verified.

Examine procedures

manual and observe

whether unrecorded

checks exist.

Examine indication

of internal verification.

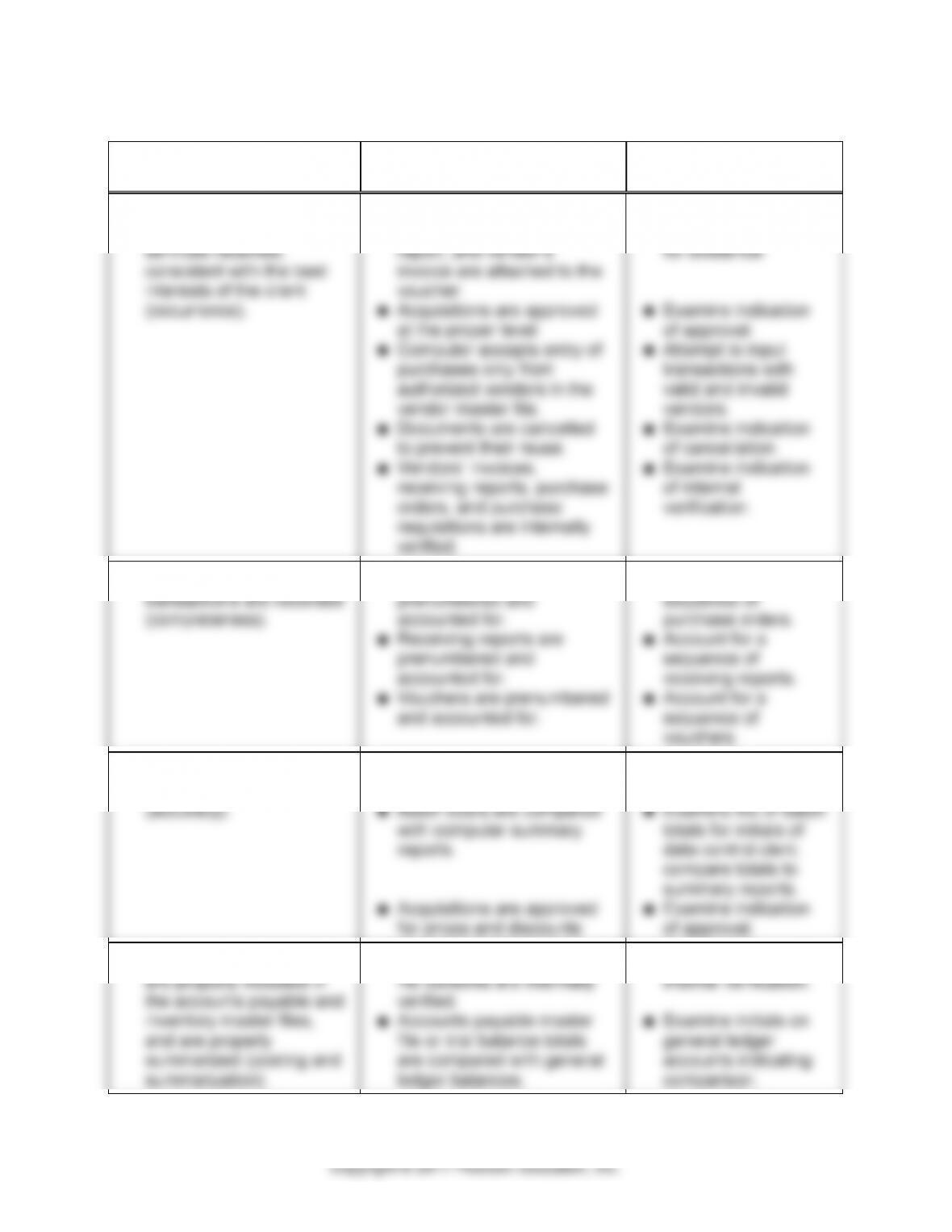

18–5

TRANSACTION–RELATED

AUDIT OBJECTIVE

POSSIBLE

INTERNAL CONTROLS

COMMON TESTS

OF CONTROLS

1. Recorded acquisitions

are for goods and

services received,

consistent with the best

interests of the client

(occurrence).

Purchase requisition,

purchase order, receiving

report, and vendor’s

invoice are attached to the

voucher.

Acquisitions are approved

at the proper level.

Computer accepts entry of

purchases only from

authorized vendors in the

vendor master file.

Documents are cancelled

to prevent their reuse.

Vendors’ invoices,

receiving reports, purchase

orders, and purchase

requisitions are internally

verified.

Examine documents

in voucher package

for existence.

Examine indication

of approval.

Attempt to input

transactions with

valid and invalid

vendors.

Examine indication

of cancellation.

Examine indication

of internal

verification.

2. Existing acquisition

transactions are recorded

(completeness).

Purchase orders are

prenumbered and

accounted for.

Receiving reports are

prenumbered and

accounted for.

Vouchers are prenumbered

and accounted for.

Account for a

sequence of

purchase orders.

Account for a

sequence of

receiving reports.

Account for a

sequence of

vouchers.

3. Recorded acquisition

transactions are accurate

(accuracy).

Calculations and amounts

are internally verified.

Batch totals are compared

with computer summary

reports.

Acquisitions are approved

Examine indication of

internal verification.

Examine file of batch

totals for initials of

data control clerk;

compare totals to

summary reports.

Examine indication

summarization).

comparison.

18–5 (continued)

TRANSACTION–RELATED

AUDIT OBJECTIVE

POSSIBLE

INTERNAL CONTROLS

COMMON TESTS

OF CONTROLS

5. Acquisition

transactions are

properly classified

(classification).

Adequate chart of accounts

is used.

Account classifications are

internally verified.

Examine procedures

manual and chart of

accounts.

Examine indication of

internal verification.

6. Acquisition

transactions are

recorded on the correct

dates (timing).

Procedures require

recording transactions as

soon as possible after the

goods and services have

been received.

Dates are internally

verified.

Examine procedures

manual and observe

whether unrecorded

vendors’ invoices

exist.

Examine indication of

internal verification.

18–6 Auditing standards require that the tests of controls and substantive

tests of transactions cover the entire accounting period in order to determine

that the system was operating in a consistent manner throughout the period. In

18–7 The importance of cash discounts to the client is that the client can

produce a substantial savings if it makes use of the cash discounts available.

18–8 The difference in the purpose of the steps is that Procedure 1 ascertains

whether all existing acquisitions are recorded properly (completeness and

accuracy), whereas Procedure 2 is designed to determine whether recorded

18-7

18–9 The acquisition and payment cycle is related to the inventory accounts

in that normally all purchases of raw materials in the case of a manufacturing

operation or merchandise in the case of a distribution or retail company are

18–10 In order to streamline ordering and purchasing, many businesses

electronically link their internal accounting systems to suppliers’ systems. By

sharing information electronically, suppliers can access inventory records to

anticipate an order, or plan their own production schedule, or suppliers can

Companies may also make changes in the way inventory physically

moves through the supply or distribution channel. For example, a company may

18–11 The following are substantive analytical procedures related to

purchases and accounts payable, and the possible misstatements that may be

uncovered.

Substantive Analytical Procedure

Possible Misstatement

Compare acquisition–related expense

account balances with prior years

Misstatement of expenses and

account payable

Calculate the ratio of purchases to

accounts payable, and compare

with prior year

Unrecorded or nonexistent accounts,

or misstatements

Compare individual accounts payable

with previous years

Unrecorded or nonexistent accounts,

or misstatements

Review purchases by month and

compare trends with prior year

Misstatement (overstatement or

understatement) of expenses

18-8

Copyright © 2017 Pearson Education, Inc.

18–12 The procedure will most likely uncover the misstatement in item b. The

search for unrecorded invoices is designed to detect an understatement of

accounts payable.

18–13 Unless evidence is discovered that indicates that a different approach

should be followed, auditors traditionally follow a conservative approach in

selecting vendors for accounts payable confirmations and customers for accounts

the larger dollar balances and is not as concerned with “zero balances.”

18–14 There are several reasons why it is not as common to confirm accounts

payable at an interim date as it is for accounts receivable:

interim date.

In auditing accounts payable, it is common for the auditor to

confirm only those accounts for which vendors’ statements are not

of reducing year–end audit time.

18–15 F. O.B. destination means that the title to the goods passes when they

are received by the purchaser. F.O.B. origin signifies that the title passes to the

buyer when the goods are shipped by the seller.

Multiple Choice Questions From CPA Examinations

18–18 a. (2) b. (3) c. (4)

Discussion Questions and Problems

18–19

QUESTION

a.

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

b.

TEST OF

CONTROL

c.

POTENTIAL

MISSTATEMENT(S)

d.

SUBSTANTIVE

PROCEDURE

1

Recorded

acquisitions and

payments are for

goods and

services

received,

consistent with

the best interests

of the client

(occurrence).

Observe and

inquire about

personnel

performing

purchasing,

shipping,

payables, and

disbursing

functions.

Goods received and

not recorded or

recorded and not

received.

Disbursements

made for goods

not received.

Vendor

statement

reconciliation.

Review of

physical

inventory

shortages.

2

Existing

acquisitions are

recorded

(completeness).

Account for

numerical

sequence of

receiving reports

and determine

that all were

recorded.

Receiving reports

are misplaced and

acquisitions not

recorded.

Vendor

statement

reconciliation.

3

Acquisitions are

recorded on the

correct dates

(timing).

Existing

acquisitions are

recorded

(completeness).

Observe and

inquire about the

procedure

performed by

mail clerk.

Compare date

mail is received

to date

accounting

received invoices.

Late recording or

non–recording of

liabilities to

suppliers.

Vendor

statement

reconciliation.

Search for

unrecorded

liabilities.

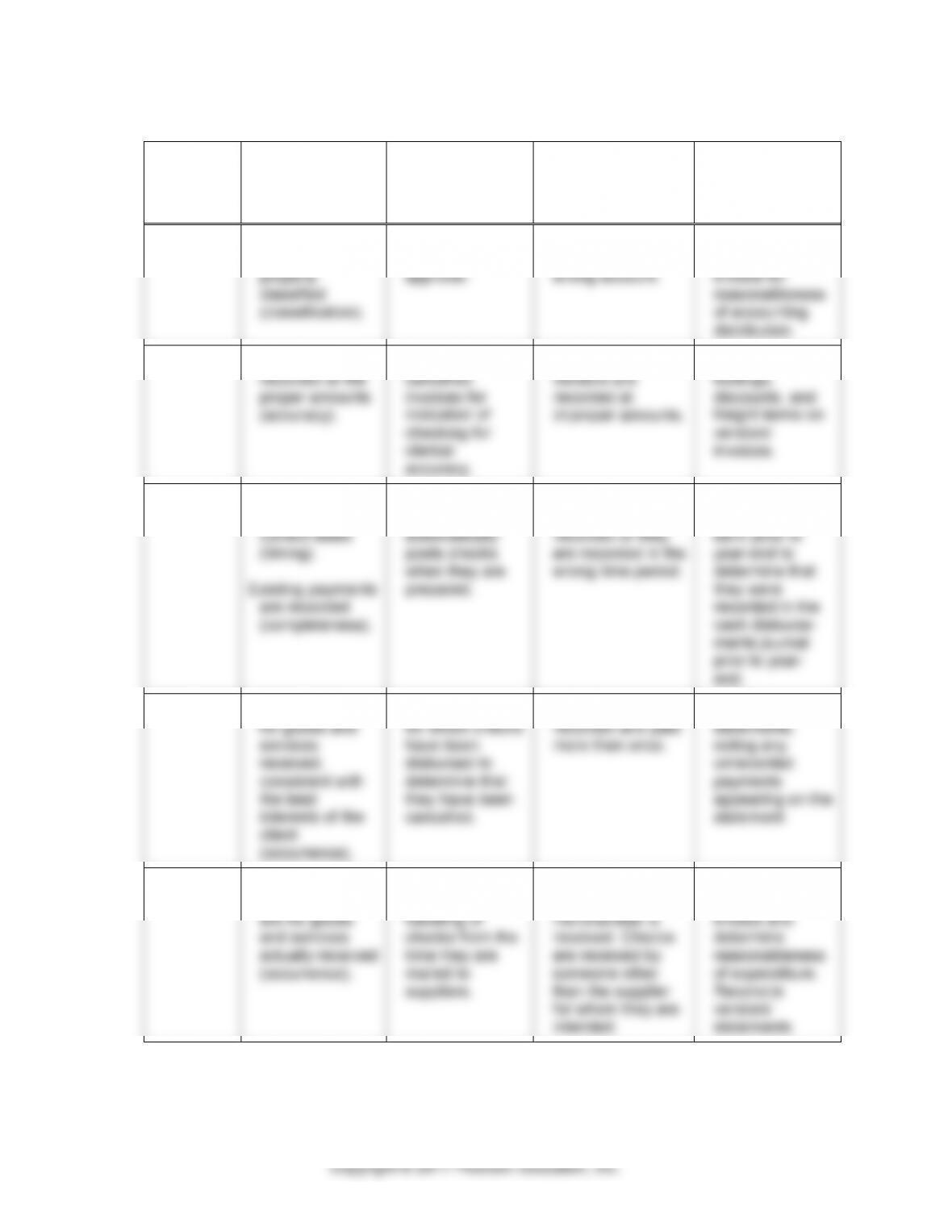

18-19 (continued)

QUESTION

a.

TRANSACTION–

RELATED AUDIT

OBJECTIVE(S)

b.

TEST OF

CONTROL

c.

POTENTIAL

MISSTATEMENT(S)

d.

SUBSTANTIVE

PROCEDURE

4

Acquisition

transactions are

properly

classified

(classification).

Examine

indication of

approval.

Acquisitions are

recorded in the

wrong account.

Examine

supporting

invoice for

reasonableness

of accounting

distribution.

5

Acquisitions are

recorded at the

proper amounts

(accuracy).

Examine

cancelled

invoices for

indication of

checking for

clerical

accuracy.

Acquisitions from

vendors are

recorded at

improper amounts.

Test extensions,

footings,

discounts, and

freight terms on

vendors’

invoices.

6

Payments are

recorded on the

correct dates

(timing).

Existing payments

are recorded

(completeness).

Observe whether

the system

automatically

posts checks

when they are

prepared.

Checks are

disbursed and not

recorded or they

are recorded in the

wrong time period.

Examine checks

clearing the

bank prior to

year–end to

determine that

they were

recorded in the

cash disburse–

ments journal

prior to year–

end.

7

Acquisitions are

for goods and

services

received,

consistent with

the best

interests of the

client

(occurrence).

Examine invoices

for which checks

have been

disbursed to

determine that

they have been

cancelled.

Invoices are

recorded and paid

more than once.

Examine vendor

statements,

noting any

unrecorded

payments

appearing on the

statement.

8

Recorded cash

disbursements

are for goods

and services

actually received

(occurrence).

Observe and

inquire about the

handling of

checks from the

time they are

mailed to

suppliers.

Checks are

disbursed and no

merchandise is

received. Checks

are received by

someone other

than the supplier

for whom they are

intended.

Trace checks to

supporting

invoice and

determine

reasonableness

of expenditure.

Reconcile

vendors’

statements.