Archives

978-0078025877 Chapter 1 Lecture Note Part 1

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES CHAPTER 1 INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES IMPORTANT NOTE TO INSTRUCTORS The 11th edition of Advanced Financial Accounting continues the approach to consolidation which was used in the […]

978-0078025877 Chapter 1 Lecture Note Part 2

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C1-1 35 min. LO 1-2, LO 1-5 M Assignment of Acquisition Costs Students must research the current authoritative accounting standards as well as any […]

978-0078025877 Chapter 1 Solution Manual Part 1

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities CHAPTER 1 INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES ANSWERS TO QUESTIONS Q1-1 Complex organizational structures often result when companies do business in a complex business environment. New subsidiaries or […]

978-0078025877 Chapter 1 Solution Manual Part 2

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities E1-2 Multiple-Choice Questions on Recording Business Combinations [AICPA Adapted] 1. a – The excess sum of the consideration given over the sum of the fair value of identifiable assets less […]

978-0078025877 Chapter 1 Solution Manual Part 3

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities E1-20 Computation of Shares Issued and Goodwill a. 15,600 shares were issued, computed as follows: Par value of shares outstanding following merger $327,600 Paid-in capital following merger 650,800 Total par […]

978-0078025877 Chapter 1 Solution Manual Part 4

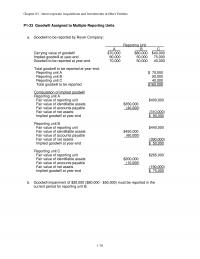

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities 1–30 P1-33 Goodwill Assigned to Multiple Reporting Units a. Goodwill to be reported by Rover Company: Reporting Unit A B C Carrying value of goodwill $70,000 $80,000 $40,000 Implied goodwill […]

978-0078025877 Chapter 10 Lecture Note

Chapter 10 – ADDITIONAL CONSOLIDATION REPORTING ISSUES CHAPTER 10 ADDITIONAL CONSOLIDATION REPORTING ISSUES OVERVIEW OF CHAPTER The following reporting issues related to the preparation of consolidated financial statements are discussed in Chapter 10: 1. The consolidated statement of cash flows […]

978-0078025877 Chapter 10 Solution Manual Part 1

Chapter 10 – Additional Consolidation Reporting Issues Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, […]

978-0078025877 Chapter 10 Solution Manual Part 2

Chapter 10 – Additional Consolidation Reporting Issues E10-6 Direct Method Cash Flow Statement Consolidated Enterprises Inc. and Subsidiary Consolidated Statement of Cash Flows For the Year Ended December 31, 20X3 Cash Flows from Operating Activities: Cash Received from Customers $ […]

978-0078025877 Chapter 10 Solution Manual Part 3

Chapter 10 – Additional Consolidation Reporting Issues P10-18 (continued) b. Consolidated statement of cash flows for 20X3 Metal Corporation and Subsidiary Consolidated Statement of Cash Flows Year Ended December 31, 20X3 Cash Flows from Operating Activities Consolidated Net Income $ […]

978-0078025877 Chapter 10 Solution Manual Part 4

Chapter 10 – Additional Consolidation Reporting Issues P10-22 Consolidated Statement of Cash Flows Weatherbee Company and Sun Corporation Consolidation Cash Flow Worksheet Year Ended December 31, 20X6 Balance Balance Item 1/1/X6 Debit Credit 12/31/X6 Cash 54,000 (a) 21,000 75,000 Accounts […]

978-0078025877 Chapter 10 Solution Manual Part 5

Chapter 10 – Additional Consolidation Reporting Issues P10-28 Deferred Tax Assets and Liabilities in a Consolidated Balance Sheet a. Peace Tax Basis Calculations: Deferred Tax Asset $8,000 Tax Rate ÷ 0.40 Book-Tax Difference (future deductible difference) Amount related to Vacation […]

978-0078025877 Chapter 10 Solution Manual Part 6

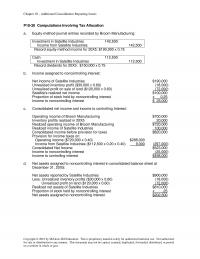

Chapter 10 – Additional Consolidation Reporting Issues P10-30 Computations Involving Tax Allocation a. Equity-method journal entries recorded by Broom Manufacturing: Investment in Satellite Industries 142,500 Income from Satellite Industries 142,500 Record equity-method income for 20X5: $190,000 x 0.75 Cash 112,500 […]

978-0078025877 Chapter 11 Lecture Note Part 1

Chapter 11 – MULTINATIONAL ACCOUNTING: FOREIGN CURRENCY TRANSACTIONS AND FINANCIAL INSTRUMENTS CHAPTER 11 MULTINATIONAL ACCOUNTING: FOREIGN CURRENCY TRANSACTIONS AND FINANCIAL INSTRUMENTS OVERVIEW OF CHAPTER Chapter 11 presents students with a foundation in the language of international business and the effects […]

978-0078025877 Chapter 11 Lecture Note Part 2

Chapter 11 – MULTINATIONAL ACCOUNTING: FOREIGN CURRENCY TRANSACTIONS AND FINANCIAL INSTRUMENTS 11-8 E11-1 LO 11-1 15 min. E Exchange Rates The direct exchange rates are given and students must compute indirect exchange rates and determine the amount of currency required […]

978-0078025877 Chapter 11 Solution Manual Part 1

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments CHAPTER 11 MULTINATIONAL ACCOUNTING: FOREIGN CURRENCY TRANSACTIONS AND FINANCIAL INSTRUMENTS ANSWERS TO QUESTIONS Q11-1 Indirect and direct exchange rates differ by which currency is desired to be expressed in […]

978-0078025877 Chapter 11 Solution Manual Part 2

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments E11-3 Basic Understanding of Foreign Exposure a. If the direct exchange rate increases, the U.S. dollar weakens relative to the foreign currency unit. If the indirect exchange rate increases, […]

978-0078025877 Chapter 11 Solution Manual Part 3

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments E11-10 (continued) February 14, 20X8 Foreign Currency Transaction Loss 700 Foreign Currency Receivable from Exchange Broker (SFr) 700 Revalue foreign currency receivable to current equivalent U.S. dollar value: $96,600 […]

978-0078025877 Chapter 11 Solution Manual Part 4

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments E11-15 (continued) 4. July 13 Foreign Currency Transaction Loss 450 Accounts Receivable (G) 450 Revalue foreign currency receivable to U.S. dollar equivalent on settlement date: $26,250 = G 50,000 […]

978-0078025877 Chapter 11 Solution Manual Part 5

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments P11-20 (continued) 5. a – January 30, 20X9 Foreign Currency Transaction Loss 200 Foreign Currency Receivable from Exchange Broker (Renminbi) 200 Adjust foreign currency receivable to current U.S. dollar […]

978-0078025877 Chapter 11 Solution Manual Part 6

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments P-11–23A (continued) c. Use of forward contract as cash flow hedge of forecasted foreign currency transaction. 12/1/X1 12/31/X1 1/30/X2 3/31/X2 Commitment Balance Sheet Transaction Settlement Date Date Date Date […]

978-0078025877 Chapter 11 Solution Manual Part 7

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments P11-24 Part II (continued) c. Maple would report a net loss in 20X6, of $150, as follows: 20X6 Loss Gain Transaction 3 Jan. 15, 20X6 — Part I 100 […]

978-0078025877 Chapter 11 Solution Manual Part 8

Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments P11-28B (continued) d. June 1, 20X2, entries to record the sale of the oil and other entries: June 1, 20X2 Cash 340,000 Sales 340,000 Record the sale of 10,000 […]

978-0078025877 Chapter 12 Lecture Note Part 1

Chapter 12 – MULTINATIONAL ACCOUNTING: ISSUES IN FINANCIAL REPORTING AND TRANSLATION OF FOREIGN ENTITY STATEMENTS CHAPTER 12 MULTINATIONAL ACCOUNTING: ISSUES IN FINANCIAL REPORTING AND TRANSLATION OF FOREIGN ENTITY STATEMENTS OVERVIEW OF CHAPTER Chapter 12 begins with a discussion that highlights […]

978-0078025877 Chapter 12 Lecture Note Part 2

Chapter 12 – MULTINATIONAL ACCOUNTING: ISSUES IN FINANCIAL REPORTING AND TRANSLATION OF FOREIGN ENTITY STATEMENTS E12-4 LO 12-4, LO 12-5 25 min. M Multiple-Choice Questions on Translation and Remeasurement Seven multiple-choice questions are presented which ask questions regarding goodwill, income […]

978-0078025877 Chapter 12 Solution Manual Part 1

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements CHAPTER 12 MULTINATIONAL ACCOUNTING: ISSUES IN FINANCIAL REPORTING AND TRANSLATION OF FOREIGN ENTITY STATEMENTS ANSWERS TO QUESTIONS Q12-1 Interest is increasing because of the expected […]

978-0078025877 Chapter 12 Solution Manual Part 2

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements C12-8 Changes in the Cumulative Translation Adjustment Account a. Foreign transactions. b. Johnson & Johnson Company applies the concepts presented in the chapter for translating […]

978-0078025877 Chapter 12 Solution Manual Part 3

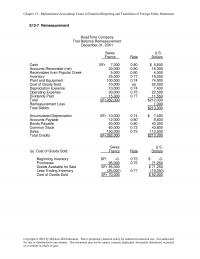

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements E12-7 Remeasurement RoadTime Company Trial Balance Remeasurement December 31, 20X1 Swiss U.S. Francs Rate Dollars Cash SFr 7,000 0.80 $ 5,600 Accounts Receivable (net) 20,000 […]

978-0078025877 Chapter 12 Solution Manual Part 4

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements E12-13 (continued) c. Translated December 31, 20X7, balance sheet: Subsidiary’s Direct Translated Trial Balance Exchange Trial Balance (in rupees) Rate (in $) Cash R 80,000 […]

978-0078025877 Chapter 12 Solution Manual Part 5

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements P12-17 (continued) c. Taft’s consolidated comprehensive income for 20X5: 1. Income from Taft’s operations for 20X5, exclusive of income from the Norwegian subsidiary $ 275,000 […]

978-0078025877 Chapter 12 Solution Manual Part 6

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements P12-23 Translation a. Western Ranching Company Trial Balance Translation December 31, 20X3 Australian Exchange U.S. Dollars Rate Dollars Cash A$ 44,100 0.60 $ 26,460 Accounts […]

978-0078025877 Chapter 12 Solution Manual Part 7

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements P12-27 (continued) NOT REQUIRED: Entries posted to T-accounts Investment in Income from Western Ranching Western Ranching Acquisition Price 140,000 80% Net Income 50,088 50,088 80% […]

978-0078025877 Chapter 13 Lecture Note Part 1

Chapter 13 – SEGMENT AND INTERIM REPORTING CHAPTER 13 SEGMENT AND INTERIM REPORTING OVERVIEW OF CHAPTER Chapter 13 presents the financial disclosure standards for reporting segments and for interim reports. Interim reports frequently are referred to as “quarterly reports,” however, […]

978-0078025877 Chapter 13 Lecture Note Part 2

Chapter 13 – SEGMENT AND INTERIM REPORTING 13-8 E13-7 LO 13-3 25 min. E Significant Foreign Operations Students must prepare a schedule determining which of five geographic areas are separately reportable. E13-8 LO 13-3 20 min. E Major Customers A […]

978-0078025877 Chapter 13 Solution Manual Part 1

Chapter 13 – Segment and Interim Reporting CHAPTER 13 SEGMENT AND INTERIM REPORTING ANSWERS TO QUESTIONS Q13-1 Information on a company’s operations in different industries would be helpful to investors in their assessments concerning the different profit rates, different degrees […]

978-0078025877 Chapter 13 Solution Manual Part 2

Chapter 13 – Segment and Interim Reporting C13-9 Questions about Interim Reporting a. In its third-quarter 10-Q, a company would have the following four income statements for the respective reporting periods: 1. An income statement for the third quarter. 2. […]

978-0078025877 Chapter 13 Solution Manual Part 3

Chapter 13 – Segment and Interim Reporting E13-6 Multiple-Choice Questions on Income Taxes at Interim Dates [AICPA Adapted] 1. a – Income tax expense for an interim period is calculated by multiplying the estimated income tax rate by pre-tax accounting […]

978-0078025877 Chapter 13 Solution Manual Part 4

Chapter 13 – Segment And Interim Reporting P13-15 Interim Income Statement a. Estimate of effective annual tax rate at end of second quarter: Estimated Annual Amounts Income from continuing operations $600,000 Less: Dividend exclusion (30,000) Estimated annual taxable income $570,000 […]

978-0078025877 Chapter 13 Solution Manual Part 5

Chapter 13 – Segment And Interim Reporting P13-19 Segment Disclosures in Financial Statements a. Multiplex Inc. Schedule for 10% Revenue Test For the Year Ended December 31, 20X5 (in millions) Segment Percent of Combined Reportable Segment Revenue Revenue of $628 […]

978-0078025877 Chapter 14 Lecture Note

Chapter 14 – SEC REPORTING CHAPTER 14 SEC REPORTING OVERVIEW OF CHAPTER Chapter 14 begins with a presentation of the history of securities regulation and the creation of the Securities and Exchange Commission (SEC). The Securities Act of 1933 requires […]

978-0078025877 Chapter 14 Solution Manual Part 1

Chapter 14 – SEC Reporting CHAPTER 14 SEC REPORTING ANSWERS TO QUESTIONS Q14-1 The basis of the SEC’s legal authority to regulate accounting principles stems from the Securities Exchange Act of 1934. In the 1934 Act, the SEC was given […]

978-0078025877 Chapter 14 Solution Manual Part 2

Chapter 14 – SEC Reporting C14-8 Audit Committees [CMA Adapted] a. The Sarbanes-Oxley Act specifies that audit committees be composed of nonmangement members of a company’s board of directors. Generally, the chair of the audit committee has financial experience. The […]

978-0078025877 Chapter 15 Lecture Note Part 1

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP CHAPTER 15 PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP OVERVIEW OF CHAPTER Chapter 15 is the first of two chapters on the accounting and financial reporting for partnerships. Chapter 15 […]

978-0078025877 Chapter 15 Lecture Note Part 2

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP 15-7 DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C15-1 LO 15-1, LO 15-5 30 min. E Partnership Agreement This case points out the necessity for a partnership agreement and focuses on […]

978-0078025877 Chapter 15 Solution Manual Part 1

Chapter 15 – Partnerships: Formation, Operation, and Changes in Membership CHAPTER 15 PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP ANSWERS TO QUESTIONS Q15-1 Partnerships are a popular form of business because they are easy to form (informal methods of organization) […]

978-0078025877 Chapter 15 Solution Manual Part 2

Chapter 15 – Partnerships: Formation, Operation, and Changes in Membership Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, […]

978-0078025877 Chapter 15 Solution Manual Part 3

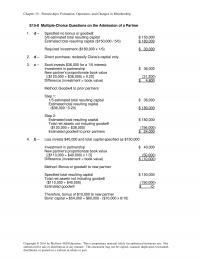

Chapter 15 – Partnerships: Formation, Operation, and Changes in Membership E15-8 Multiple-Choice Questions on the Admission of a Partner 1. d – Specified no bonus or goodwill: 5/6 estimated total resulting capital $ 150,000 Estimated total resulting capital ($150,000 / […]

978-0078025877 Chapter 15 Solution Manual Part 4

Chapter 15 – Partnerships: Formation, Operation, and Changes in Membership P15-13 Determining a New Partner’s Investment Cost a. $200,000 (No goodwill or bonus recorded) Cash 200,000 Snider, Capital ($800,000 x 1/4) 200,000 0.75 estimated total resulting capital $ 600,000 Estimated […]

978-0078025877 Chapter 15 Solution Manual Part 5

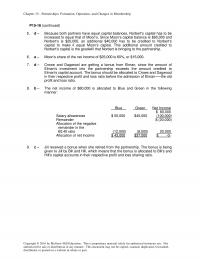

Chapter 15 – Partnerships: Formation, Operation, and Changes in Membership P15-16 (continued) 5. d – Because both partners have equal capital balances, Norbert’s capital has to be increased to equal that of Moon’s. Since Moon’s capital balance is $60,000 and […]

978-0078025877 Chapter 16 Lecture Note

Chapter 16 – PARTNERSHIPS: LIQUIDATION CHAPTER 16 PARTNERSHIPS: LIQUIDATION OVERVIEW OF CHAPTER 16 Chapter 16 completes the two-chapter sequence on partnership accounting and financial reporting. The Uniform Partnership Act of 1997 (UPA) contains many of the basic liquidation provisions that […]

978-0078025877 Chapter 16 Solution Manual Part 1

Chapter 16 – Partnerships: Liquidation Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025877 Chapter 16 Solution Manual Part 2

Chapter 16 – Partnerships: Liquidation 16–11 E16-2 Multiple-Choice Questions on Partnership Liquidation 1. a – Casey Dithers Edwards Profit and loss ratio 5 3 2 Beginning capital 80,000 90,000 70,000 Actual loss on assets (15,000) (9,000) (6,000) Potential loss on […]

978-0078025877 Chapter 16 Solution Manual Part 3

Chapter 16 – Partnerships: Liquidation 16–21 E16-8 (continued): Based on practical approach: APB Partnership Cash Distribution Plan Loss Absorption Potential Capital Accounts Adams Peters Blake Adams Peters Blake Profit and loss percentages 20% 30% 50% Preliquidation capital balances 55,000 75,000 […]

978-0078025877 Chapter 16 Solution Manual Part 4

Chapter 16 – Partnerships: Liquidation 16–31 P16-14 Installment Liquidation [AICPA Adapted] ABC Partnership Statement of Partnership Realization and Liquidation For the period from January 1, 20X1, through March 31, 20X1 Capital Balances Other Accounts Art Bru Chou Cash + Assets […]

978-0078025877 Chapter 16 Solution Manual Part 5

Chapter 16 – Partnerships: Liquidation 16–41 P16-19 Matching 1. G 2. D 3. A 4. J 5. K 6. C 7. E 8. B 9. H 10. I Chapter 16 – Partnerships: Liquidation 16–42 P16-20 Partnership Agreement Issues [AICPA Adapted] […]

978-0078025877 Chapter 16 Solution Manual Part 6

Chapter 16 – Partnerships: Liquidation 16–47 ¶9 On February 27, 1998, Brower requested copies of the Partnership’s accounting records from the date of its inception until July 1994, when Don departed to San Francisco, and copies of Ray’s and Doug’s […]

978-0078025877 Chapter 17 Lecture Note Part 1

Chapter 17 – GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING CHAPTER 17 GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING OVERVIEW OF CHAPTER Chapter 17 begins a two-chapter sequence on the accounting and financial reporting standards for governmental entities such as […]

978-0078025877 Chapter 17 Lecture Note Part 2

Chapter 17 – GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING 17–11 P17-19 LO 17-7, LO 17-8 25 min. M Questions on Fund Items [AICPA Adapted] Revenues and expenditures and transfers amounts together with additional relating information are provided. Students must […]

978-0078025877 Chapter 17 Solution Manual Part 1

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting CHAPTER 17 GOVERNMENTAL ENTITIES: INTRODUCTION AND GENERAL FUND ACCOUNTING ANSWERS TO QUESTIONS Q17-1 A fund is an independent fiscal and accounting entity with a self-balancing set of accounts recording cash […]

978-0078025877 Chapter 17 Solution Manual Part 2

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting 17–11 C17-5 Examining Deposit and Investment Risk Disclosures of a Governmental Entity (Note to the Instructor: Students may become frustrated because they may feel that the information presented in the […]

978-0078025877 Chapter 17 Solution Manual Part 3

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting 17–21 E17-8 (continued) (8) The revenue from liquor licenses is the amount collected, not the amount expected (9) The $15,000 reimbursement is not reported as revenue in the general fund. […]

978-0078025877 Chapter 17 Solution Manual Part 4

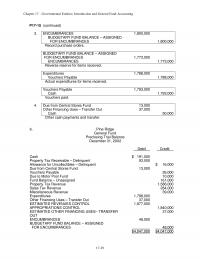

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting 17–29 P17-15 (continued) 3. ENCUMBRANCES 1,800,000 BUDGETARY FUND BALANCE – ASSIGNED FOR ENCUMBRANCES 1,800,000 Record purchase orders. BUDGETARY FUND BALANCE – ASSIGNED FOR ENCUMBRANCES 1,773,000 ENCUMBRANCES 1,773,000 Reverse reserve for […]

978-0078025877 Chapter 18 Lecture Note Part 1

Chapter 18 – GOVERNMENTAL ENTITIES: SPECIAL FUNDS AND GOVERNMENT–WIDE FINANCIAL STATEMENTS CHAPTER 18 GOVERNMENTAL ENTITIES: SPECIAL FUNDS AND GOVERNMENT-WIDE FINANCIAL STATEMENTS OVERVIEW OF CHAPTER Chapter 18 completes the two-chapter presentation on the accounting and financial reporting standards for governmental entities. […]

978-0078025877 Chapter 18 Lecture Note Part 2

Chapter 18 – GOVERNMENTAL ENTITIES: SPECIAL FUNDS AND GOVERNMENT–WIDE FINANCIAL STATEMENTS 18–10 E18-2 LO 18-1, LO 18-3 25 min. E Multiple-Choice Items on Governmental Funds [AICPA Adapted] Six multiple-choice questions on the general theory of accounting for the different funds […]

978-0078025877 Chapter 18 Solution Manual Part 1

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements CHAPTER 18 GOVERNMENTAL ENTITIES: SPECIAL FUNDS AND GOVERNMENT-WIDE FINANCIAL STATEMENTS ANSWERS TO QUESTIONS Q18-1 A governmental entity would use a special revenue fund rather than a general fund when […]

978-0078025877 Chapter 18 Solution Manual Part 2

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be […]

978-0078025877 Chapter 18 Solution Manual Part 3

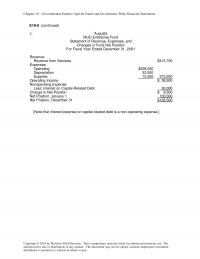

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements E18-8 (continued) c. Augusta MUD Enterprise Fund Statement of Revenue, Expenses, and Changes in Fund Net Position For Fiscal Year Ended December 31, 20X1 Revenue: Revenue from Services $413,700 […]

978-0078025877 Chapter 18 Solution Manual Part 4

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements P18-13 (continued) Fund Journal Entries 7. Capital ENCUMBRANCES 75,000 Projects BUDGETARY FUND BALANCE – ASSIGNED Fund FOR ENCUMBRANCES 75,000 BUDGETARY FUND BALANCE – ASSIGNED FOR ENCUMBRANCES 75,000 ENCUMBRANCES 75,000 […]

978-0078025877 Chapter 18 Solution Manual Part 5

Chapter 18 – Governmental Entities: Special Funds and Government–Wide Financial Statements P18-20 Matching Questions Involving the Statement of Revenues, Expenditures, and Changes in Fund Balance for a Capital Projects Fund and a Debt Service Fund 1. C 2. D 3. […]

978-0078025877 Chapter 19 Lecture Note Part 1

Chapter 19 – NOT-FOR-PROFIT ENTITIES CHAPTER 19 NOT-FOR-PROFIT ENTITIES OVERVIEW OF CHAPTER Chapter 19 presents the accounting and reporting for not-for-profit entities. The beginning of the chapter provides an overview of FASB standards that directly address not-for- profit entities. ASC […]

978-0078025877 Chapter 19 Lecture Note Part 2

Chapter 19 – NOT-FOR-PROFIT ENTITIES 19-8 DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C19-1 LO 19-3, LO 19-4, LO 19-5 40 min. M Accounting for Donations Students must specify the criteria for recognizing the value of donated services for hospitals, VHWOs, […]

978-0078025877 Chapter 19 Solution Manual Part 1

Chapter 19 – Not-for-Profit Entities CHAPTER 19 NOT-FOR-PROFIT ENTITIES ANSWERS TO QUESTIONS Q19-1 Initially, tuition scholarships are included in revenue for the period in order to measure fully the revenue obtainable. If the university requires an employment-type work for the […]

978-0078025877 Chapter 19 Solution Manual Part 2

Chapter 19 – Not-for-Profit Entities C19-6 An Analysis of the Financial Statements for the American Red Cross, a Voluntary Health and Welfare Organization The consolidated financial statements can be found by clicking on the “Publications” link at the top of […]

978-0078025877 Chapter 19 Solution Manual Part 3

Chapter 19 – Not-for-Profit Entities E19-5 Multiple-Choice Questions on Voluntary Health and Welfare Organization Accounting [AICPA Adapted] 1. c – The accrual basis is used for all funds. 2. b – $800,000 x .50 = $400,000 $400,000 x .10 = […]

978-0078025877 Chapter 19 Solution Manual Part 4

Chapter 19 – Not-for-Profit Entities P19-12 (continued) Adjustments March 31, 20X3 1. Investments 7,000 Unrealized Gain on Investment 7,000 Note: ONPOs may value investments at full market values 2&3. Depreciation Expense – House 9,000 Depreciation Expense – Snack Bar and […]

978-0078025877 Chapter 19 Solution Manual Part 5

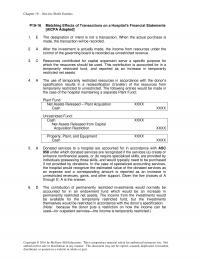

Chapter 19 – Not-for-Profit Entities P19-16 Matching Effects of Transactions on a Hospital’s Financial Statements [AICPA Adapted] 1. E The designation of intent is not a transaction. When the actual purchase is made, the transaction will be recorded. 2. A […]

978-0078025877 Chapter 19 Solution Manual Part 6

Chapter 19 – Not-for-Profit Entities P19-24 True-False Questions about Not-for-Profit Accounting and Reporting 1. F Per ASC 958, a statement of functional expenses is required only for voluntary health and welfare organizations. 2. T According to ASC 958, pledge revenue […]

978-0078025877 Chapter 2 Lecture Note Part 1

Chapter 2 – REPORTING INTERCORPORATE INTERESTS AND CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES WITH NO DIFFERENTIAL CHAPTER 2 REPORTING INTERCORPORATE INTERESTS AND CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES WITH NO DIFFERENTIAL IMPORTANT NOTE TO INSTRUCTORS The 11th edition uses a building block […]

978-0078025877 Chapter 2 Lecture Note Part 2

Chapter 02 – REPORTING INTERCORPORATE INTERESTS 2-9 DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C2-1A 20 min. LO 2-2, LO 2-3 E Choice of Accounting Method The criteria used in determining significant influence are reviewed. Students also must specify when investment […]

978-0078025877 Chapter 2 Solution Manual Part 1

Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential CHAPTER 2 REPORTING INTERCORPORATE INVESTMENTS AND CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES WITH NO DIFFERENTIAL ANSWERS TO QUESTIONS Q2-1 (a) An investment in the voting common […]

978-0078025877 Chapter 2 Solution Manual Part 2

Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential 5. d – Since these are liquidating dividends they would decrease the investment account under the cost method and decrease the investment account under the […]

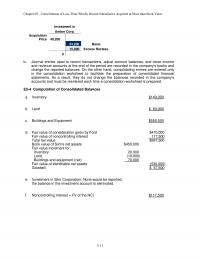

978-0078025877 Chapter 2 Solution Manual Part 3

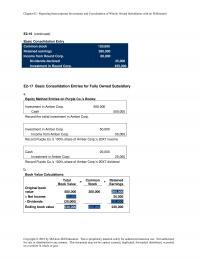

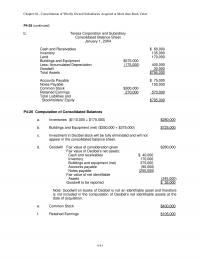

Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential Common stock 120,000 Retained earnings 280,000 Income from Round Corp. 80,000 Dividends declared 25,000 E2-17 Basic Consolidation Entries for Fully Owned Subsidiary a. Equity Method […]

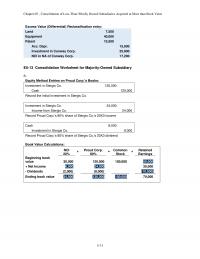

978-0078025877 Chapter 2 Solution Manual Part 4

Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential P2-24 Consolidated Worksheet at End of the Second Year of Ownership (Equity Method) a. Equity Method Entries on Peanut Co.’s Books: Investment in Snoopy Co. […]

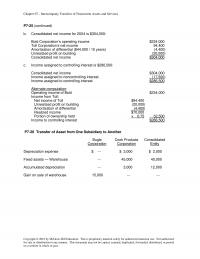

978-0078025877 Chapter 2 Solution Manual Part 5

Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential P2–26 (continued) Paper Co. Scissor Co. Consolidation Entries DR CR Consolidated Income Statement Sales 880,000 355,000 1,235,000 Less: COGS (278,000) (178,000) (456,000) Less: Depreciation Expense […]

978-0078025877 Chapter 20 Lecture Note

Chapter 20 – CORPORATIONS IN FINANCIAL DIFFICULTY CHAPTER 20 CORPORATIONS IN FINANCIAL DIFFICULTY OVERVIEW OF CHAPTER Chapter 20 presents the actions available to corporations experiencing financial difficulty. A series of nonjudicial actions are available, including debt restructuring, creditor’s committee management, […]

978-0078025877 Chapter 20 Solution Manual Part 1

Chapter 20 – Corporations in Financial Difficulty CHAPTER 20 CORPORATIONS IN FINANCIAL DIFFICULTY ANSWERS TO QUESTIONS Q20-1 The nonjudicial actions available to a financially distressed company are debt restructuring arrangements, creditor’s committee management, and transferring assets. The judicial actions available […]

978-0078025877 Chapter 20 Solution Manual Part 2

Chapter 20 – Corporations in Financial Difficulty E20-2 (continued) b. Journal entries to record reorganization: (1) Accounts Payable 80,000 Notes Payable, 10% 150,000 Interest Payable 40,000 Cash 6,000 Accounts Receivable (net) 72,000 Land 85,000 Gain on Disposal of Land 40,000 […]

978-0078025877 Chapter 20 Solution Manual Part 3

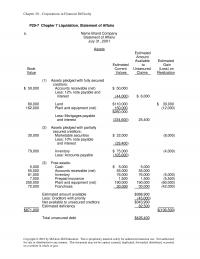

Chapter 20 – Corporations in Financial Difficulty P20-7 Chapter 7 Liquidation, Statement of Affairs a. Name Brand Company Statement of Affairs July 31, 20X1 Assets Estimated Amount Available Estimated Estimated to Gain Book Current Unsecured (Loss) on Value Values Claims […]

978-0078025877 Chapter 3 Lecture Note Part 1

Chapter 3 – THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES WITH NO DIFFERENTIAL CHAPTER 3 THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN- WHOLLY-OWNED SUBSIDIARIES WITH NO DIFFERENTIAL IMPORTANT NOTE TO INSTRUCTORS The 11th edition uses a building block approach […]

978-0078025877 Chapter 3 Lecture Note Part 2

Chapter 03 – THE REPORTING ENTITY AND CONSOLIDATED FINANCIAL STATEMENTS 3–10 E3-7 20 min. LO 3-5 M Subsidiary Acquired for Cash A simple consolidated balance sheet is prepared following an acquisition of subsidiary shares using cash. E3-8 20 min. LO […]

978-0078025877 Chapter 3 Solution Manual Part 1

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential CHAPTER 3 THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES WITH NO DIFFERENTIAL ANSWERS TO QUESTIONS Q3-1 The basic idea underlying the preparation of consolidated financial […]

978-0078025877 Chapter 3 Solution Manual Part 2

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential E3-2 Multiple-Choice Questions on Variable Interest Entities 1. c – SPE’s are typically financed primarily by debt, while equity financing is only a small portion. SPE’s […]

978-0078025877 Chapter 3 Solution Manual Part 3

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential E3–10 Reporting for a Variable Interest Entity Gamble Company Consolidated Balance Sheet Cash $ 18,600,000(a) Buildings and Equipment $370,600,000(b) Less: Accumulated Depreciation (10,100,000) 360,500,000 Total Assets […]

978-0078025877 Chapter 3 Solution Manual Part 4

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential 270,000 Basic Entry 3-31 0 Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential 3-32 P3-26 (continued) Peanut Co. Snoopy Co. […]

978-0078025877 Chapter 3 Solution Manual Part 5

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential 3-39 P3–29 Consolidated Worksheet and Balance Sheet on the Acquisition Date (Equity Method) a. Equity Method Entries on Paper Co.’s Books: Investment in Scissor Co. 296,000 […]

978-0078025877 Chapter 4 Lecture Note Part 1

Chapter 4 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE CHAPTER 4 CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE IMPORTANT NOTE TO INSTRUCTORS The 11th edition uses a building block approach to […]

978-0078025877 Chapter 4 Lecture Note Part 2

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C4-1 40 min. LO 4-1 H Reporting Significant Investments in Common Stock Students must research aspects of intercorporate investments held by Harley- Davidson, Chevron, PepsiCo, and […]

978-0078025877 Chapter 4 Solution Manual Part 1

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value CHAPTER 4 CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE ANSWERS TO QUESTIONS Q4-1 The carrying value of the investment is reduced under […]

978-0078025877 Chapter 4 Solution Manual Part 2

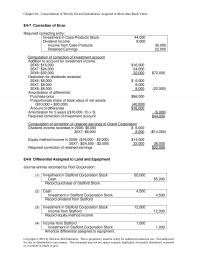

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value E4-7 Correction of Error Required correcting entry: Investment in Case Products Stock 44,000 Dividend Income 8,000 Income from Case Products 30,000 Retained Earnings 22,000 Computation of […]

978-0078025877 Chapter 4 Solution Manual Part 3

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value 4-21 E4-16 (continued) b. Gold Enterprises Premium Builders Consolidation Entries DR CR Consolidated Balance Sheet Cash and Receivables 80,000 30,000 2,000 108,000 Inventory 150,000 350,000 7,000 […]

978-0078025877 Chapter 4 Solution Manual Part 4

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value 4-31 E4-22 Consolidation Worksheet with Differential a. Equity Method Entries on Kennelly Corp.’s Books: Investment in Short Co. 180,000 Cash 180,000 Record the initial investment in […]

978-0078025877 Chapter 4 Solution Manual Part 5

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value 4-41 P4-25 (continued) b. Teresa Corporation and Subsidiary Consolidated Balance Sheet January 1, 20X4 Cash and Receivables $ 60,000 Inventory 135,000 Land 170,000 Buildings and Equipment […]

978-0078025877 Chapter 4 Solution Manual Part 6

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value P4–31 Intercorporate Receivables and Payables a. Consolidation entries: Equity Method Entries on Kim Corp.’s Books: Investment in Normal Co. 305,000 Cash 305,000 Record the initial investment […]

978-0078025877 Chapter 4 Solution Manual Part 7

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value P4-34 Consolidation Worksheet at End of Second Year of Ownership a. Equity Method Entries on Mill Corp.’s Books: Investment in Roller Co. 36,000 Income from Roller […]

978-0078025877 Chapter 4 Solution Manual Part 8

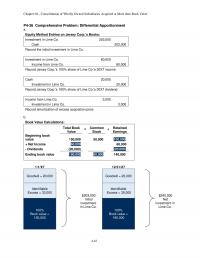

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value P4-36 Comprehensive Problem: Differential Apportionment a. Equity Method Entries on Jersey Corp.’s Books: Investment in Lime Co. 203,000 Cash 203,000 Record the initial investment in Lime […]

978-0078025877 Chapter 5 Lecture Note Part 1

Chapter 5 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE CHAPTER 5 CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE IMPORTANT NOTE TO INSTRUCTORS The 11th edition uses a building block approach to our coverage […]

978-0078025877 Chapter 5 Lecture Note Part 2

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES 5–10 P5-20 LO 5-1 10 min. E Acquisition Price Students must determine the acquisition price given two separate situations. Additionally, students are required to determine the amount assigned to the noncontrolling interest at […]

978-0078025877 Chapter 5 Solution Manual Part 1

CHAPTER 5 CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK VALUE ANSWERS TO QUESTIONS Q5-1 The noncontrolling interest is reported as a separate item in the stockholders’ equity section of the balance sheet. Q5-2 The consolidated balance sheet always […]

978-0078025877 Chapter 5 Solution Manual Part 2

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value 5-11 Investment in Amber Corp. Acquisition Price 49,200 34,200 Basic 15,000 Excess Reclass. 0 E5-4 Computation of Consolidated Balances a. Inventory $140,000 b. Land $ 60,000 […]

978-0078025877 Chapter 5 Solution Manual Part 3

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value E5-10 Differential Assigned to Amortizable Asset a. Lancaster Company’s common stock, January 1, 20X1 $120,000 Lancaster Company’s retained earnings, January 1, 20X1 380,000 Book value of […]

978-0078025877 Chapter 5 Solution Manual Part 4

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value 5-31 Excess Value (Differential) Reclassification entry: Land 7,500 Equipment 40,000 Patent 10,500 Acc. Depr. 15,000 Investment in Conway Corp. 25,800 NCI in NA of Conway Corp. […]

978-0078025877 Chapter 5 Solution Manual Part 5

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value E5-17A Consolidation of Subsidiary with Negative Retained Earnings Equity Method Entries on General Corp.’s Books: Investment in Strap Co. 138,000 Cash 138,000 Record the initial investment […]

978-0078025877 Chapter 5 Solution Manual Part 6

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value 5-51 P5-29 (continued) Excess Value (Differential) Reclassification Entry: Inventory 6,000 Buildings & Equipment 15,000 Investment in Darla Corp. 14,700 NCI in NA of Darla Corp. 6,300 […]

978-0078025877 Chapter 5 Solution Manual Part 7

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value P5-34 Consolidation Worksheet at End of Second Year of Ownership a. Equity Method Entries on Power Corp.’s Books: Investment in Best Co. 27,000 Income from Best […]

978-0078025877 Chapter 5 Solution Manual Part 8

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value P5–37 Subsidiary with Other Comprehensive Income in Year of Acquisition a. Equity Method Entries on Amber Corp.’s Books: Investment in Sparta Co. 96,000 Cash 96,000 Record […]

978-0078025877 Chapter 6 Lecture Note Part 1

Chapter 06 – INTERCOMPANY INVENTORY TRANSACTIONS CHAPTER 6 INTERCOMPANY INVENTORY TRANSACTIONS OVERVIEW OF CHAPTER Chapters 6 and 7 focus on the elimination of the effects of transfers of assets and services between companies included in a consolidated entity. The procedures […]

978-0078025877 Chapter 6 Lecture Note Part 2

Chapter 06 – INTERCOMPANY INVENTORY TRANSACTIONS 6-8 E6-1 LO 6-3, LO 6-4 15 min. E Multiple-Choice Questions on Intercompany Inventory Transfers [AICPA Adapted] Six multiple-choice questions cover issues associated with the valuation of inventory and determination of consolidated net income […]

978-0078025877 Chapter 6 Solution Manual Part 1

Chapter 06 – Intercompany Inventory Transactions CHAPTER 6 INTERCOMPANY INVENTORY TRANSACTIONS ANSWERS TO QUESTIONS Q6-1 All inventory transfers between related companies must be eliminated to avoid an overstatement of revenue and cost of goods sold in the consolidated income statement. […]

978-0078025877 Chapter 6 Solution Manual Part 2

Chapter 06 – Intercompany Inventory Transactions 6. b – 14 years = ($28,000 / [(28,000 – $20,000) / 4 years] E6-3 Multiple Choice – Consolidated Income Statement 1. c – The only sales recorded are sales to non-affiliates. 2. b […]

978-0078025877 Chapter 6 Solution Manual Part 3

Chapter 06 – Intercompany Inventory Transactions E6-13 Consolidated Balance Sheet Worksheet a. Equity Method Entries on Doorst Corp.’s Books: Investment in Hingle Co. 49,000 Income from Hingle Co. 49,000 Record Doorst Corp.’s 70% share of Hingle Co.’s 20X8 income Cash […]

978-0078025877 Chapter 6 Solution Manual Part 4

Chapter 06 – Intercompany Inventory Transactions P6-21 Incomplete Data a. Increase in fair value of buildings and equipment: Consolidated total $ 680,000 Balance reported by Lever (400,000) Balance reported by Tropic (240,000) Increase in value $ 40,000 b. Accumulated depreciation […]

978-0078025877 Chapter 6 Solution Manual Part 5

Chapter 06 – Intercompany Inventory Transactions P6–24 (continued) Adjustment to Basic Consolidation Entry NCI Priority Net Income 9,000 81,000 +Reverse GP deferral (down) 8,000 +Reverse GP deferral (up) 600 5,400 – Gross profit deferral (down) (2,000) – Gross profit deferral […]

978-0078025877 Chapter 6 Solution Manual Part 6

Chapter 06 – Intercompany Inventory Transactions P6-27 (continued) 20X9 Downstream Transactions Total = Re-sold + Ending Inventory Sales 90,000 70,000 20,000 COGS 54,000 42,000 12,000 Gross Profit 36,000 28,000 8,000 Gross Profit % 40.00% 20X9 Upstream Transactions Total = Re-sold […]

978-0078025877 Chapter 6 Solution Manual Part 7

Chapter 06 – Intercompany Inventory Transactions P6-30 Consolidation Using Financial Statement Data a. Equity Method Entries on Bower Corp.’s Books: Investment in Concerto Co. 21,000 Income from Concerto Co. 21,000 Record Bower Corp.’s 60% share of Concerto Co.’s 20X6 income […]

978-0078025877 Chapter 6 Solution Manual Part 8

Chapter 06 – Intercompany Inventory Transactions P6-32 (continued) Pine Corp. Slim Corp. Consolidation Entries DR CR Consolidated Balance Sheet Cash 105,000 15,000 120,000 AR & Other Receivables 410,000 120,000 900 334,100 90,000 100,000 5,000 Merchandise Inventory 920,000 670,000 3,000 1,587,000 […]

978-0078025877 Chapter 6 Solution Manual Part 9

Chapter 06 – Intercompany Inventory Transactions P6-34 (continued) Randall Corp. Sharp Co. Consolidation Entries DR CR Consolidated Income Statement Sales 500,000 250,000 57,000 693,000 Other Income 20,400 30,000 50,400 Less: COGS (416,000) (202,000) 10,000 (564,000) 44,000 Less: Depreciation & Amortization […]

978-0078025877 Chapter 7 Lecture Note Part 1

Chapter 7 – Intercompany Transfers of Services and Noncurrent Assets CHAPTER 7 INTERCOMPANY TRANSFERS OF SERVICES AND NONCURRENT ASSETS OVERVIEW OF CHAPTER Chapter 7 focuses on the elimination of the effects of transfers of services and noncurrent assets between companies […]

978-0078025877 Chapter 7 Lecture Note Part 2

Chapter 7 – INTERCOMPANY TRANSFERS OF SERVICES AND NONCURRENT ASSETS 7-8 E7-1 LO 7-5, LO 7-6 15 min. E Multiple-Choice Questions on Intercompany Transfers [AICPA Adapted] Five questions relating to the elimination of unrealized profits on intercorporate transfers and the […]

978-0078025877 Chapter 7 Solution Manual Part 1

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, […]

978-0078025877 Chapter 7 Solution Manual Part 2

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services E7-2 (continued) 5. b – Reported net income of Gold Company $ 45,000 Reported gain on sale of equipment $15,000 Intercompany profit realized in 20X6 (5,000) (10,000) Realized net income […]

978-0078025877 Chapter 7 Solution Manual Part 3

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services E7-16 Intercompany Sale at a Loss a. Consolidated net income for 20X8 will be greater than Parent Company’s income from operations plus Sunway’s reported net income. The consolidation entries at […]

978-0078025877 Chapter 7 Solution Manual Part 4

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services P7–25 (continued) b. Consolidated net income for 20X4 is $304,000: Bold Corporation’s operating income $234,000 Toll Corporation’s net income 94,400 Amortization of differential ($44,000 / 10 years) (4,400) Unrealized profit […]

978-0078025877 Chapter 7 Solution Manual Part 5

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services P7-32 (continued) c. Prime Company and Subsidiary Consolidated Balance Sheet December 31, 20X6 Cash and Receivables $ 141,000 Inventory 350,000 Land 150,000 Buildings and Equipment $655,000 Less: Accumulated Depreciation (273,000) […]

978-0078025877 Chapter 7 Solution Manual Part 6

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services P7–35 (continued) Adjustments to Basic Consolidation Entry: NCI Topp Corp. Net Income 9,000 21,000 – Gain on Equip (Up) (2,880) (6,720) +Extra Depreciation (Up) 360 840 Income to be eliminated […]

978-0078025877 Chapter 7 Solution Manual Part 7

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services d. Rossman Corp. Schmid Dist. Consolidation Entries DR CR Consolidated Income Statement Sales 4,801,000 985,000 5,786,000 Other Income or Loss 90,000 (35,000) 80,000 40,000 15,000 Less: COGS (2,193,000) (525,000) (2,718,000) […]

978-0078025877 Chapter 8 Lecture Note Part 1

Chapter 08 – INTERCOMPANY INDEBTEDNESS CHAPTER 8 INTERCOMPANY INDEBTEDNESS OVERVIEW OF CHAPTER Chapter 8 illustrates the consolidation procedures needed to eliminate the financial statement effects of direct and indirect intercorporate debt transfers. Elimination of direct sale of bonds between the […]

978-0078025877 Chapter 8 Lecture Note Part 2

Chapter 08 – INTERCOMPANY INDEBTEDNESS 8-9 E8-9A LO 8-3 15 min. M Retirement of Bonds Sold at a Discount (Straight-Line Method) Parent company bonds issued at a discount are purchased by a subsidiary from a nonaffiliate seven years after the […]

978-0078025877 Chapter 8 Solution Manual Part 1

Chapter 08 – Intercompany Indebtedness Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or […]

978-0078025877 Chapter 8 Solution Manual Part 10

Chapter 08 – Intercompany Indebtedness E8–12A (continued) e. Consolidation entries, December 31, 20X7: Bonds Payable 200,000 Premium on Bonds Payable 4,000 Interest Income 23,200 Investment in Bundle Company Bonds 194,000 Interest Expense 21,200 Investment in Bundle Co. 8,400 NCI in […]

978-0078025877 Chapter 8 Solution Manual Part 11

Chapter 08 – Intercompany Indebtedness P8–16A (continued) d. Fern Corp. Vincent Co. Consolidation Entries DR CR Consolidated Income Statement Sales 300,000 200,000 500,000 Interest income 4,500 4,500 0 Less: Other Expenses (198,500) (161,000) 4,000 (363,500) Less: Interest Expense (27,000) (9,000) […]

978-0078025877 Chapter 8 Solution Manual Part 12

Chapter 08 – Intercompany Indebtedness P8-23A (continued) Bond Consolidation Entry: Bonds Payable 50,000 Bond Premium 7,000 Investment in Brown Bonds 50,000 Gain on Bond Retirement 7,000 Tyler Brown Corp. Consolidation Entries DR CR Consolidated Income Statement Sales 400,000 200,000 600,000 […]

978-0078025877 Chapter 8 Solution Manual Part 13

Chapter 08 – Intercompany Indebtedness P8–25A (continued) 20X7 Downstream Transactions Total = Re-sold + Ending Inventory Sales 60,000 33,000 27,000 COGS 40,000 22,000 18,000 Gross Profit 20,000 11,000 9,000 Gross Profit % 33.33% Deferral of This Year’s Unrealized Profits on […]

978-0078025877 Chapter 8 Solution Manual Part 14

Chapter 08 – Intercompany Indebtedness P8–28A (continued) Excess Value (Differential) Calculations: NCI 10% + Topp Co. 90% = Land + Goodwill Beginning balance 8,000 72,000 30,000 50,000 Changes (2,500) (22,500) (25,000) Ending balance 5,500 49,500 30,000 25,000 Amortized Excess Value […]

978-0078025877 Chapter 8 Solution Manual Part 15

Chapter 08 – Intercompany Indebtedness P8–29B (continued) Impairment Loss Goodwill Impairment Loss 25,000 Goodwill 25,000 NCI’s Portion of Impairment Loss NCI in NA of Bussman Corp. 2,500 NCI in NI of Bussman Corp. 2,500 Copyright © 2016 by McGraw-Hill Education. […]

978-0078025877 Chapter 8 Solution Manual Part 2

Chapter 08 – Intercompany Indebtedness E8-3 Bond Sale at Discount a. $16,731 = ($25,073.73 + $25,119.36) x 1/3 b. Journal entries recorded by Wood Corporation: January 1, 20X4 Cash 16,000 Interest Receivable 16,000 July 1, 20X4 Cash 16,000 Investment in […]

978-0078025877 Chapter 8 Solution Manual Part 3

Chapter 08 – Intercompany Indebtedness E8-8 Constructive Retirement at Beginning of Year 576,000.00 579,200.00 3,200.00 Face Value of Bonds PMT # Interest $ PMT Interest Income Amort of Discount (Premium) Premium (Discount) Bonds Payable BV of Bonds 400,000.00 1/1/20X5 ($3,200.00) […]

978-0078025877 Chapter 8 Solution Manual Part 4

Chapter 08 – Intercompany Indebtedness E8–12 (continued) d. Consolidation entries, December 31, 20X6: Bonds Payable 200,000 Premium on Bonds Payable 5,718 Interest Income 11,415 Investment in Bundle Company Bonds 192,615 Interest Expense 10,662 Gain on Bond Retirement 13,856 Eliminate intercompany […]

978-0078025877 Chapter 8 Solution Manual Part 5

Chapter 08 – Intercompany Indebtedness P8–16 (continued) c. Book Value Calculations: NCI 30% + Fern Corp. 70% = Common Stock + Retained Earnings Beginning Book Value 45,202 105,470 50,000 100,672 + Net Income 9,071 21,165 30,236 – Dividends (3,000) (7,000) […]

978-0078025877 Chapter 8 Solution Manual Part 6

Chapter 08 – Intercompany Indebtedness P8-20 (continued) Bond and other Debt Consolidation Entries: Bonds Payable 100,000 Bond Premium 13,246 Investment in Stang Bonds 101,607 Investment in Stang Stock 9,311 NCI in NA of Stang 2,328 Note: Interest revenue and expense […]

978-0078025877 Chapter 8 Solution Manual Part 7

Chapter 08 – Intercompany Indebtedness P8-24 Consolidation Worksheet — Year after Retirement a. Book Value Calculations: NCI 40% + Bennett Corp. 60% = Common Stock + Retained Earnings Beginning Book Value 68,000 102,000 100,000 70,000 + Net Income 20,000 30,000 […]

978-0078025877 Chapter 8 Solution Manual Part 8

Chapter 08 – Intercompany Indebtedness P8–26 (continued) Accumulated Depreciation 1,500 Depreciation Expense 1,500 Eliminate the Gain on Land: Investment in Skate Co. Stock 9,750 NCI in NA of Skate Co. Stock 3,250 Land 13,000 Copyright © 2016 by McGraw-Hill Education. […]

978-0078025877 Chapter 8 Solution Manual Part 9

Chapter 08 – Intercompany Indebtedness P8-28 (continued) Eliminate Intercompany Holding of Bussman Bonds: Bonds Payable 1,000,00 0 Premium on Bonds Payable 4,268 Other Income (Interest) 124,121 Investment in Bussman Bonds 984,121 Gain on Retirement of Bonds 25,394 Other Expenses (Interest) […]

978-0078025877 Chapter 9 Lecture Note Part 1

Chapter 09 – CONSOLIDATION OWNERSHIP ISSUES CHAPTER 9 CONSOLIDATION OWNERSHIP ISSUES OVERVIEW OF CHAPTER The illustrations and discussions in Chapter 9 are intended to provide students with a basic understanding of some of the consolidation issues and problems arising from […]

978-0078025877 Chapter 9 Lecture Note Part 2

Chapter 09 – CONSOLIDATION OWNERSHIP ISSUES 9-7 DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS C9-1 LO 9-1 15 min. E Effect of Subsidiary Preferred Stock A number of things must be known about subsidiary preferred shares outstanding before their impact on […]

978-0078025877 Chapter 9 Solution Manual Part 1

Chapter 9 – Consolidation Ownership Issues CHAPTER 9 CONSOLIDATION OWNERSHIP ISSUES ANSWERS TO QUESTIONS Q9-1 Preferred stock of the subsidiary is eliminated in the consolidation process in a manner comparable to that used in eliminating the common stock of the […]

978-0078025877 Chapter 9 Solution Manual Part 2

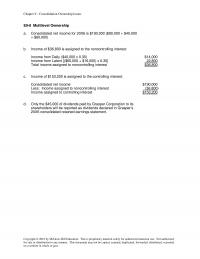

Chapter 9 – Consolidation Ownership Issues E9-8 Multilevel Ownership a. Consolidated net income for 20X6 is $190,000 ($90,000 + $40,000 + $60,000) b. Income of $36,800 is assigned to the noncontrolling interest: Income from Dally ($40,000 x 0.35) $14,000 Income […]

978-0078025877 Chapter 9 Solution Manual Part 3

Chapter 9 – Consolidation Ownership Issues E9-16 Sale of Shares by Subsidiary to Nonaffiliate a. Computation of change in book value of Schroeder Corporation shares held by Browne Corporation: Before After Sale Sale Common stock, $10 par value $150,000 $ […]

978-0078025877 Chapter 9 Solution Manual Part 4

Chapter 9 – Consolidation Ownership Issues P9-21 (continued) g. Consolidation entries: Basic Consolidation Entry: Preferred Stock 200,000 Premium on Preferred Stock 5,000 Common Stock 500,000 Additional Paid-In Capital 797,600 Retained Earnings 1,650,000 Income from Jacobs Jacuzzi 156,000 Dividends Income—Preferred 8,000 […]

978-0078025877 Chapter 9 Solution Manual Part 5

Chapter 9 – Consolidation Ownership Issues P9-24 (continued) b. Penn Corp. ENC Co. Consolidation Entries DR CR Consolidated Income Statement Sales 280,000 170,000 450,000 Less: COGS (210,000) (100,000) (310,000) Less: Depreciation Expense (20,000) (15,000) (35,000) Less: Other Expenses (21,000) (25,000) […]

AC 74922

Suppose the direct foreign exchange rates in U.S. dollars are: 1 Singapore dollar = $0.7025 1 Cyprus pound = $2.5132 Based on the information given above, how many Singapore dollars are required to purchase goods costing 10,000 US dollars? A. […]

AC 77046

Burrough Corporation paid $80,000 to acquire all of Helyar Company’s net assets. Helyar reported assets with a book value of $60,000 and fair value of $98,000 and liabilities with a book value and fair value of $23,000 on the date […]

AC 82252

During its inception, Devon Company purchased land for $100,000 and a building for $180,000. After exactly 3 years, it transferred these assets and cash of $50,000 to a newly created subsidiary, Regan Company, in exchange for 15,000 shares of Regan’s […]

ACC 17068

On the statement of operations prepared for a private, not-for-profit hospital, patient service revenue earned during the year is reported net of amounts for which of the following items? I. Contractual adjustments II. Bad debts expense A. I only B. […]

Acc 28457

The trial balance of WM Partnership is as follows: Wilfred and Mike decide to incorporate their partnership. The partnership’s books will be closed, and new books will be used for W & M Corporation. The following additional information is available: […]

Acc 59043

Sub Company sells all its output at 20 percent above cost to Par Corporation. Par purchases its entire inventory from Sub. The incomes reported by the companies over the past three years are as follows: Sub Company sold inventory for […]

ACC 63637

In a statement of revenues, expenditures, and changes in fund balance, the unassigned fund balance will be increased by: I. a decrease in the fund balance—Nonspendable II. an excess of other financing sources over other financing uses. A. I only […]

ACC 78461

ABC, a holder of a $400,000 XYZ Inc. bond, collected the interest due on June 30, 20X8, and then sold the bond to DEF Inc. for $365,000. On that date the bond issuer, XYZ, a 90 percent owner of DEF, […]

ACC 79484

ABC Corporation owns 75 percent of XYZ Company’s voting shares. During 20X8, ABC produced 50,000 chairs at a cost of $79 each and sold 35,000 chairs to XYZ for $90 each. XYZ sold 18,000 of the chairs to unaffiliated companies […]

Acc 88806

In accounting for governmental funds, which of the following items could appear only on government-wide financial statements? A. I only B. I and II C. I and III D. I, II, III On January 1, 20X6, Polka Co. (Polka) and […]

ACC 98397

Hunter Corporation holds 80 percent of the voting shares of Moss Company. On January 1, 20X8, Moss purchased $100,000 par value 12 percent Hunter bonds from Cruse Corporation for $115,000. Hunter originally issued the bonds to Cruse on January 1, […]

Accounting 64908

Pursuing an inorganic growth strategy, Wilson Company acquired Venus Company’s net assets and assigned them to four separate reporting divisions. Wilson assigned total goodwill of $134,000 to the four reporting divisions as given below: Based on the preceding information, what […]

Accounting 80619

Suppose the direct foreign exchange rates in U.S. dollars are as follows: 1 Swiss franc = $1.0371 1 Swedish krona = $0.1526 Based on the information given above, how many Swiss francs are required to purchase goods costing $5,000 U.S.? […]

Acct 22655

On January 1, 20X8, William Company acquired 30 percent of eGate Company’s common stock, at underlying book value of $100,000. eGate has 100,000 shares of $2 par value, 5 percent cumulative preferred stock outstanding. No dividends are in arrears. eGate […]

Acct 29506

Wright Company recently petitioned for bankruptcy and is now in the process of preparing a statement of affairs. The carrying values and estimated fair values of the assets of Wright Company are as follows: Carrying Value Fair Value Cash $10,000 […]

ACCT 35119

Which financial statement is (are) required for a voluntary health and welfare organization which is not required for a private, not-for-profit hospital? I. A statement of operations. II. A statement of functional expenses. A. I only B. II only C. […]

Acct 51228

Senior Corporation acquired 80 percent of Junior Company’s voting shares on January 1, 20X8, at underlying book value. On Dec. 31, 20X8, it also purchased $500,000 par value 8 percent Junior bonds, which had been issued on January 1, 20X5 […]

ACCT 57630

Riviera Township reported the following data for its governmental activities for the year ended June 30, 20X9: Additional information available is as follows: All of the long-term debt was used to acquire capital assets. Cash of $475,000 is restricted for […]

ACCT 64520

On the statement of functional expenses prepared for a voluntary health and welfare organization, depreciation expense is allocated to I. expenses for program services. II. expenses for supporting services. A. I only B. II only C. Both I and II […]

ACCT 72067

A private, not-for-profit hospital received a contribution of $40,000 on June 15, 20X8. The donor restricted the contribution to funding research activities currently being performed by the hospital. For the year ended December 31, 20X8, the hospital spent $30,000 of […]

ACCT 77650

The transactions listed in the following questions occurred in a private, not-for-profit hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement of operations for the year ended December 31, 20X8. Transaction: The governing board designated assets […]

ACCT 78323

During the fiscal year ended June 30, 20X9, the city of Moorhead constructed a new courthouse which was budgeted to cost $5,000,000. Moorhead used a capital projects fund to account for the construction activities. In July of 20X8, a bid […]

ACT 28038

The APB partnership agreement specifies that partnership net income be allocated as follows: Average capital balances for the current year were $50,000 for A, $30,000 for P, and $20,000 for B. Refer to the information given. Assuming a current year […]

ACT 40348

ASC 958 requires that an “other not-for-profit entity” (ONPO) provide three financial statements. Which of the following is NOT one among them? A. A statement of functional expenses B. A statement of financial position C. A statement of activities D. […]

ACT 56170

Collins Company reported consolidated revenue of $120,000,000 in 20X8. Collins operates in two geographic areas, domestic and Asia. The following information pertains to these two areas: What calculation below is correct to determine if the revenue test is satisfied for […]

ACT 97071

In accordance with the Single Audit Act of 1984, external auditors issue the standard audit report on the governmental unit’s financial statements and must also issue: I. a special report on the effectiveness with which the governmental unit is achieving […]

MET MG 17840

If the functional currency is the local currency of a foreign subsidiary, what exchange rates should be used to translate the items below, assuming the foreign subsidiary is in a country which has not experienced hyperinflation over three years? A. […]

MET MG 28211

The general fund of the Town of Dean levied property taxes of $3,000,000 for the fiscal year beginning on January 1, 20X8. It was estimated that 1% of the levy would be uncollectible. During the period January 1, 20X8, through […]

MET MG 30549

On September 1, 20X1, Brady Corp. entered into a foreign exchange contract for speculative purposes by purchasing 50,000 deutsche marks for delivery in 60 days. The rates to exchange $1 for 1 deutsche mark follow: 9/1/20X1 9/30/20X1 Spot-rate 0.75 0.70 […]

MET MG 54487

Patch Corporation purchased land from Sub1 Corporation for $350,000 on December 3, 20X5. This purchase followed a series of transactions between Patch-controlled subsidiaries. On January 23, 20X5, Sub3 Corporation purchased the land from a nonaffiliate for $240,000. It sold the […]

MET MG 84103

Wally Corporation acquired 70 percent of the common shares and 60 percent of the preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At that date, the fair value of the noncontrolling interest in Safety’s common […]

MET MG 86487

A not-for-profit private college in Virginia created a separate foundation responsible for obtaining financial support from alumni and others. Foundation assets are used for the benefit of the college. Donations made to the foundation and subsequently transferred to the college […]

SMG AC 40061

Janet Corporation holds 75 percent of Slider Corporation’s voting common stock, acquired at book value. The fair value of the noncontrolling interest at the date of acquisition was equal to 25 percent of the book value of Slider Corporation. On […]

SMG AC 73497

A private university offers graduate assistantships to qualified students each year. In exchange for the waiver of tuition, graduate assistants are required to assist faculty members with research and other activities. Assume a graduate assistant received a $4,000 tuition waiver […]

SMG AC 84729

During its inception, Devon Company purchased land for $100,000 and a building for $180,000. After exactly 3 years, it transferred these assets and cash of $50,000 to a newly created subsidiary, Regan Company, in exchange for 15,000 shares of Regan’s […]

SMG AC 94329

Plummet Corporation reported the book value of its net assets at $400,000 when Zenith Corporation acquired 100 percent ownership. The fair value of Plummet’s net assets was determined to be $510,000 on that date. Based on the preceding information, what […]