Chapter 13 – Segment and Interim Reporting

E13-6 Multiple-Choice Questions on Income Taxes at Interim Dates [AICPA Adapted]

1.

a –

Income tax expense for an interim period is calculated

by multiplying the estimated income tax rate by pre-tax

accounting income for the interim period.

(b) incorrect. Pre-tax accounting income is used for this

calculation.

(c) incorrect. The estimated income tax rate is used for

this calculation.

(d) incorrect. The estimated income tax rate is used for

this calculation.

2.

b –

$170,000 x 0.45 = $ 76,500

$130,000 x 0.40 = (52,000)

Third quarter

$ 24,500

3.

c –

Net operating loss credit ($100,000 x 0.40)

$ 40,000

Other tax credit

10,000

Total credits

$ 50,000

Estimated annual operating loss

÷100,000

Tax benefit rate ($50,000 / $100,000)

.50

Operating loss in first quarter

x$20,000

Tax benefit in first quarter

$ 10,000

4.

c –

When calculating third quarter income tax expense you

must subtract your provision in the current year to

eliminate double counting.

(a) incorrect. The income number that is used is the to-

date earnings

(b) incorrect. The statutory rate is never used.

(d) incorrect. The statutory rate is never used.

5.

c –

.25 X $200,000 = $50,000.

6.

b –

Deferred taxes are computed only for temporary

differences. The other items are permanent differences.

E13-7 Significant Foreign Operations

Percent of

Sales to

Consolidated

Unaffiliated

Revenue of

Separately

Geographic Area

Customers

$793,000

Reportable

U.S.

$364,000

45.9

%

Yes

Britain

252,000

31.8

Yes

Brazil

72,000

9.1

No

Israel

58,000

7.3

No

Australia

47,000

5.9

No

Consolidated Revenue

$793,000

Note that the country-based revenue test is based on sales to unaffiliated

customers. All countries having material sales to unaffiliated customers of $79,300

($793,000 x 0.10) or more must be separately reported.

Chapter 13 – Segment and Interim Reporting

b.

Income Tax Expense

68,000

Income Tax Payable

68,000

Record first-quarter tax provision:

$170,000 total pre-tax earnings

+ 30,000 add back extraordinary loss that is reported separately with its own

income tax effect

$200,000 first-quarter income from continuing operations

x 0.34 effective annual tax rate

$ 68,000 first quarter tax provision for

continuing operations

(Note that the problem requires only the tax provision for the continuing operations.

The tax effect of the extraordinary loss would be recognized separately.)

E13-10 Operating Loss Tax Benefits

Income (Losses)

Estimated

Tax (Benefit)

Before Taxes

Effective

Less

Reported

Year-

Annual

Year-

Previously

In

Period

Period

to-Date

Tax Rate

to-Date (a)

Provided

Period

1

$(100,000)

$(100,000)

40%

$(40,000)

-0-

$ (40,000)

2

80,000

(20,000)

40%

(8,000)

$(40,000)

32,000

3

160,000

140,000

45%

63,000

(8,000)

71,000

4

400,000

540,000

45%

243,000

63,000

180,000

Total

$ 540,000

$243,000

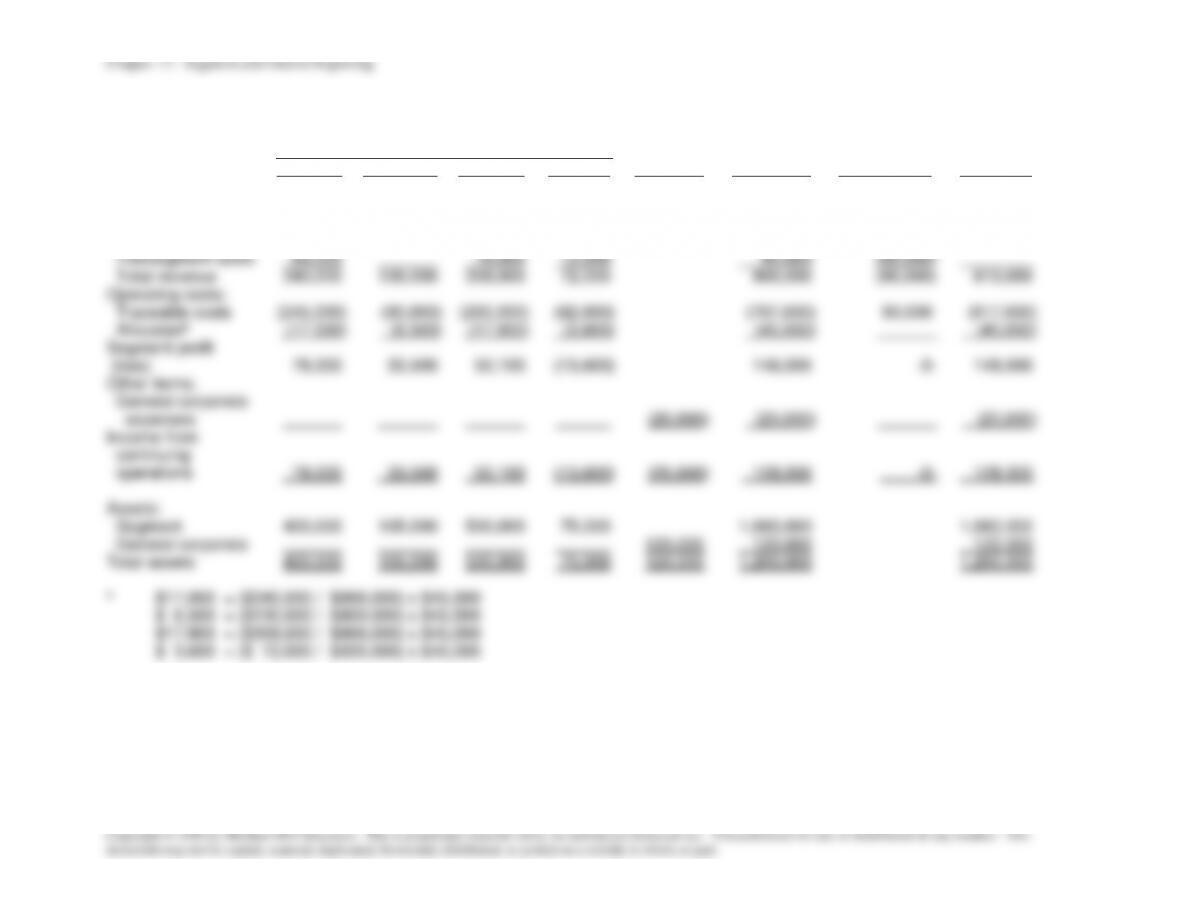

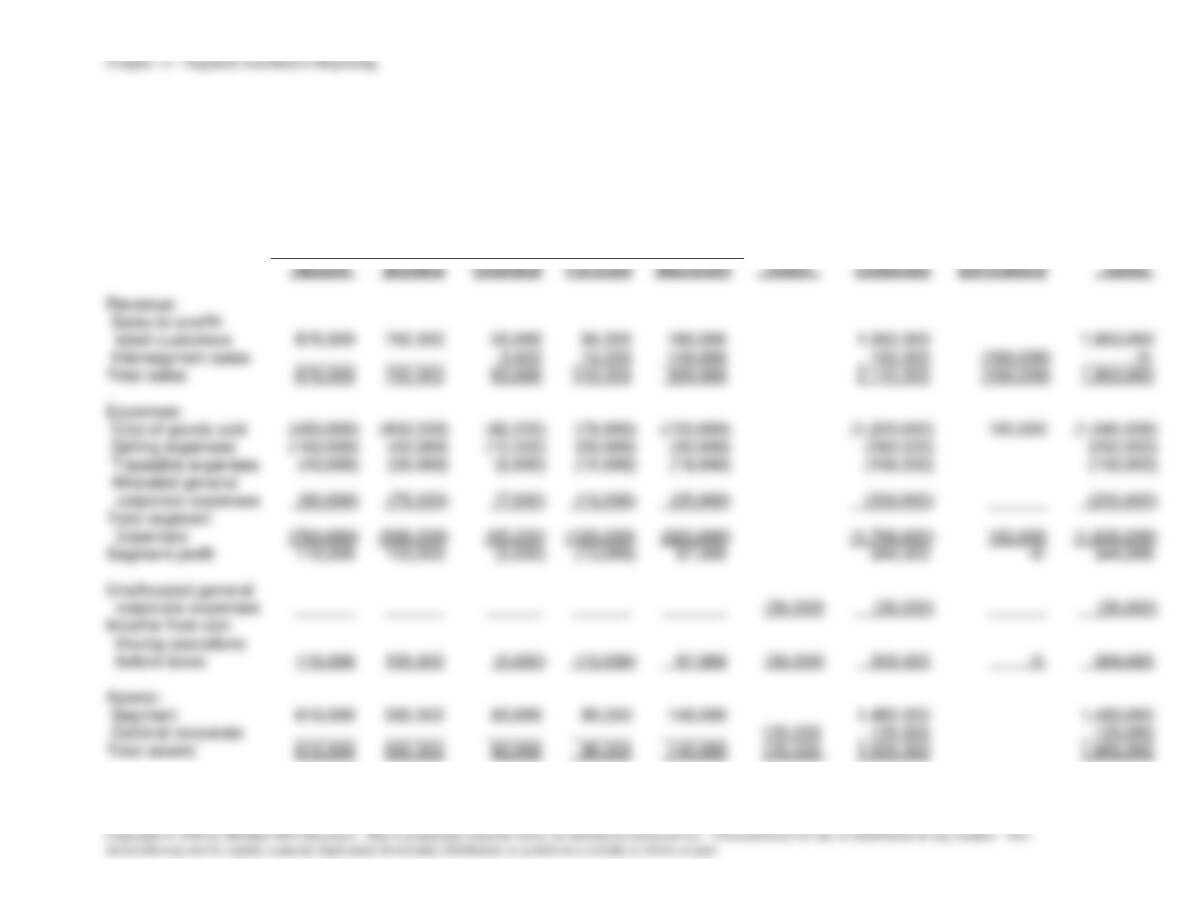

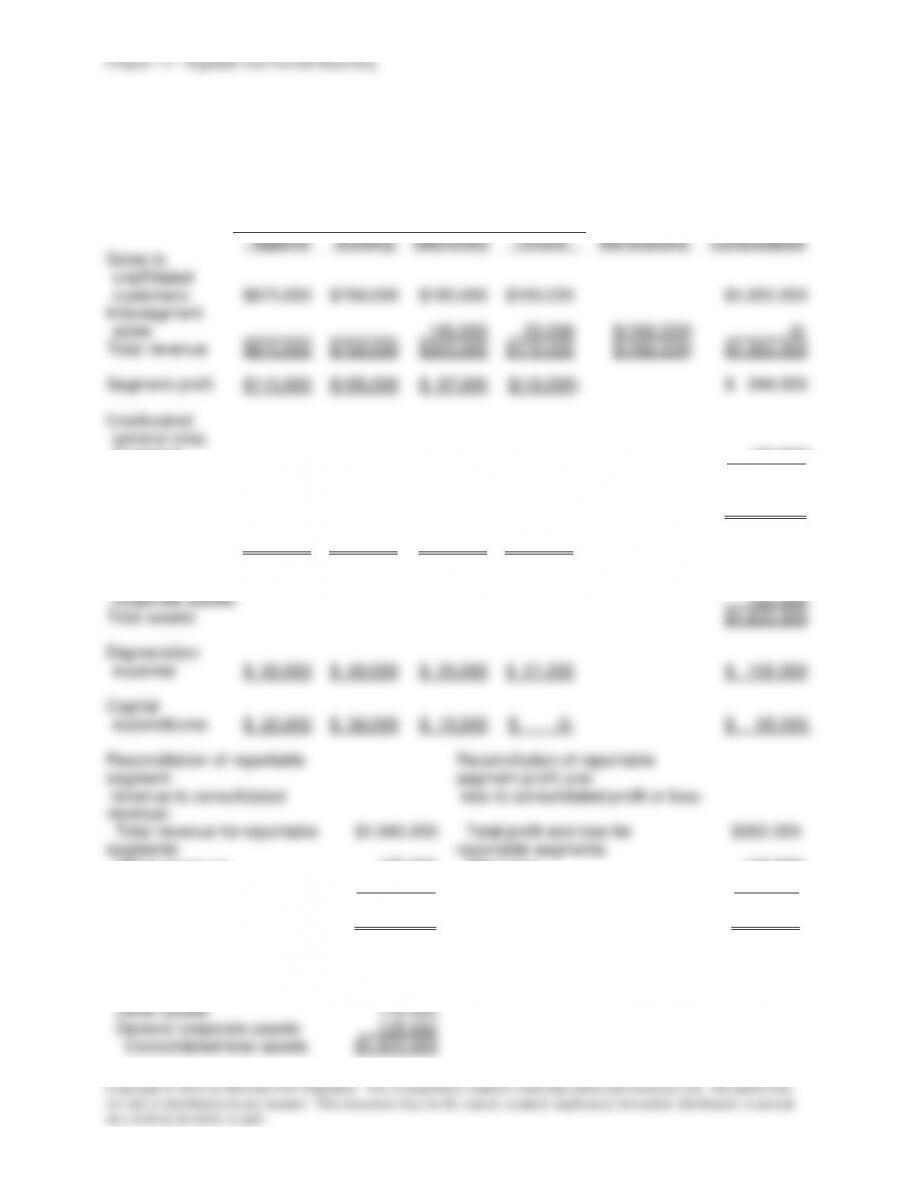

E13-11 Industry Segment and Geographic Area Revenue Tests

a.

Operating segments revenue test (in thousands)

Combined

Percent of Combined

Separately

Operating Segment

Revenue

Revenue of $1,385

Reportable

Ethical Drugs

$

320

23.1

%

Yes

Nonprescription Drugs

515

37.2

Yes

Generic Drugs

470

33.9

Yes

Industrial Chemicals

80

5.8

No

Total

$1,385

b.

Geographic Area revenue test (in thousands)

Unaffiliated

Percent of Consolidated

Separately

Geographic Area

Revenue

Revenue of $1,165

Reportable

Domestic

$ 820

70.4

%

Always

Mexico

245

21.0

Yes*

Taiwan

100

8.6

No*

Total

$1,165

Chapter 13 – Segment and Interim Reporting

*Assuming a 10% materiality threshold. Individual foreign countries exceeding 10%

would be listed separately. In this case, only Mexico would have to be separately

reported.

c.

Disclosure of operating segments‘ revenue (in thousands)

Nonpre-

Ethical

scription

Generic

Com-

Elimina-

Consol-

Drugs

Drugs

Drugs

Other

bined

tions

idated

Sales to

Unaffiliates

$300

$425

$370

$70

$1,165

$1,165

Intersegment

Revenue

20

90

100

10

220

$(220)

$320

$515

$470

$80

$1,385

$(220)

$1,165

d.

Disclosure of geographic areas‘ revenue (in thousands)

Geographic Area

Unaffiliated Revenue

United States

$ 820

Total Foreign

345

*

Total

$1,165

Significant country:

Mexico

$ 245

*Individual foreign countries exceeding 10% of total unaffiliated revenue ($1,165)

would be listed separately. In this case, only Mexico would be reported separately.

E13-12 Different Reporting Methods for Interim Reports [CMA Adapted]

1. Not acceptable. Revenue should be recognized when realized.

2. Acceptable. The gross profit method may be used for interim reports.

3. Acceptable. Costs may be allocated on a reasonable basis.

4. Acceptable. A recovery to original cost may be recorded in a subsequent interim

period.

5. Not acceptable. Gains are recognized in the period of the sale.

6. Acceptable. Costs may be allocated on a reasonable basis.

7. Not acceptable. ASC 250 requires that a change in depreciation in long-lived assets

be accounted for as a change in estimate affected by a change in accounting