Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities

E1-20 Computation of Shares Issued and Goodwill

a.

15,600 shares were issued, computed as follows:

Par value of shares outstanding following merger

$327,600

Paid-in capital following merger

650,800

Total par value and paid-in capital

$978,400

Par value of shares outstanding before merger

$218,400

Paid-in capital before merger

370,000

(588,400)

Increase in par value and paid-in capital

$390,000

Divide by price per share

÷ $25

Number of shares issued

15,600

b.

The par value is $7, computed as follows:

Increase in par value of shares outstanding

($327,600 – $218,400)

Divide by number of shares issued

$109,200

Par value

÷ 15,600

$ 7.00

c.

Goodwill of $34,000 was recorded, computed as follows:

Increase in par value and paid-in capital

$390,000

Fair value of net assets ($476,000 – $120,000)

(356,000)

Goodwill

$ 34,000

E1-21 Combined Balance Sheet

Adam Corporation and Best Company

Combined Balance Sheet

January 1, 20X2

Cash and Receivables

$ 240,000

Accounts Payable

$ 125,000

Inventory

460,000

Notes Payable

235,000

Buildings and Equipment

840,000

Common Stock

244,000

Less: Accumulated Depreciation

(250,000)

Additional Paid-In Capital

556,000

Goodwill

75,000

Retained Earnings

205,000

$1,365,000

$1,365,000

Computation of goodwill

Fair value of compensation given

$480,000

Fair value of net identifiable assets

($490,000 – $85,000)

(405,000)

Goodwill

$ 75,000

Computation of APIC

Fair value of compensation given ($60 x 8,000 shares)

Less par value of shares issued ($8 x 8,000)

$480,000

(64,000)

Plus existing APIC from Adam’s books

140,000

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities

Additional Paid-In Capital

$ 556,000

E1-22 Recording a Business Combination

Merger Expense

54,000

Deferred Stock Issue Costs

29,000

Cash

83,000

Cash

70,000

Accounts Receivable

110,000

Inventory

200,000

Land

100,000

Buildings and Equipment

350,000

Goodwill (1)

30,000

Accounts Payable

195,000

Bonds Payable

100,000

Bond Premium

5,000

Common Stock

320,000

Additional Paid-In Capital (2)

211,000

Deferred Stock Issue Costs

29,000

Fair value of consideration given (40,000 x $14)

$560,000

Fair value of assets acquired

$830,000

Fair value of liabilities assumed

(300,000)

Fair value of net assets acquired

(530,000)

Goodwill

$ 30,000

Computation of additional paid-in capital

Number of shares issued

40,000

Issue price in excess of par value ($14 – $8)

x $6

Total

$240,000

Less: Deferred stock issue costs

(29,000)

Increase in additional paid-in capital

$211,000

E1-23 Reporting Income

20X2:

Net income

=

$6,028,000 [$2,500,000 + $3,528,000]

Earnings per share

=

$5.48 [$6,028,000 / (1,000,000 + 100,000*)]

20X1:

Net income

=

$4,460,000 [previously reported]

Earnings per share

=

$4.46 [$4,460,000 / 1,000,000]

* 100,000 = 200,000 shares x ½ year

Chapter 01 – Intercorporate Acquisitions and Investments in Other Entities

SOLUTIONS TO PROBLEMS

P1-24 Assets and Accounts Payable Transferred to Subsidiary

a. Journal entry recorded by Tab Corporation for its transfer of

assets and accounts payable to Collon Company:

Investment in Collon Company Common Stock

320,000

Accounts Payable

45,000

Accumulated Depreciation – Buildings

40,000

Accumulated Depreciation – Equipment

10,000

Cash

25,000

Inventory

70,000

Land

60,000

Buildings

170,000

Equipment

90,000

b. Journal entry recorded by Collon Company for receipt of assets

and accounts payable from Tab Corporation:

Cash

25,000

Inventory

70,000

Land

60,000

Buildings

170,000

Equipment

90,000

Accounts Payable

45,000

Accumulated Depreciation – Buildings

40,000

Accumulated Depreciation – Equipment

10,000

Common Stock

180,000

Additional Paid-In Capital

140,000

P1-25 Creation of New Subsidiary

a. Journal entry recorded by Eagle Corporation for transfer of assets

and accounts payable to Sand Corporation:

Investment in Sand Corporation Common Stock

400,000

Allowance for Uncollectible Accounts Receivable

5,000

Accumulated Depreciation

40,000

Accounts Payable

10,000

Cash

30,000

Accounts Receivable

45,000

Inventory

60,000

Land

20,000

Buildings and Equipment

300,000

b. Journal entry recorded by Sand Corporation for receipt of assets and

accounts payable from Eagle Corporation:

Cash

30,000

Accounts Receivable

45,000

Inventory

60,000

Land

20,000

Buildings and Equipment

300,000

Allowance for Uncollectible Accounts Receivable

5,000

Accumulated Depreciation

40,000

Accounts Payable

10,000

Common Stock

50,000

Additional Paid-In Capital

350,000

P1-26 Incomplete Data on Creation of Subsidiary

a. The book value of assets transferred was $152,000 ($3,000 + $16,000 + $27,000 + $9,000 +

$70,000 + $60,000 – $21,000 – $12,000).

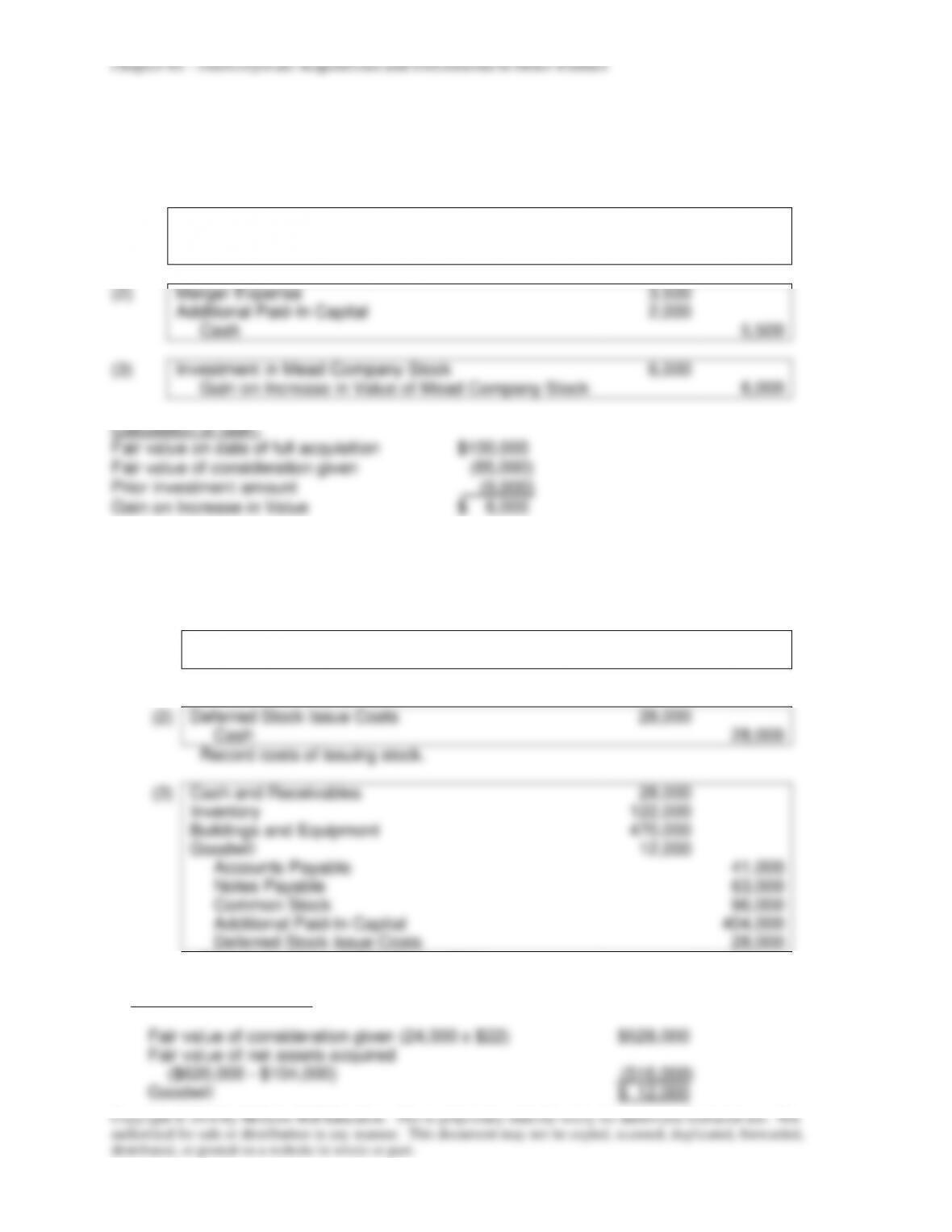

P1–27 Acquisition in Multiple Steps

Deal Corporation will record the following entries:

(1)

Investment in Mead Company Stock

85,000

Common Stock – $10 Par Value

40,000

Additional Paid-In Capital

45,000

(2)

Merger Expense

3,500

Additional Paid-In Capital

2,000

Cash

5,500

(3)

Investment in Mead Company Stock

6,000

Gain on Increase in Value of Mead Company Stock

6,000

P1–28 Journal Entries to Record a Business Combination

Journal entries to record acquisition of TKK net assets:

(1)

Merger Expense

14,000

Cash

14,000

Record payment of legal fees.

(2)

Deferred Stock Issue Costs

28,000

Cash

28,000

Record costs of issuing stock.

(3)

Cash and Receivables

28,000

Inventory

122,000

Buildings and Equipment

470,000

Goodwill

12,000

Accounts Payable

41,000

Notes Payable

63,000

Common Stock

96,000

Additional Paid-In Capital

404,000

Deferred Stock Issue Costs

28,000

Record purchase of TKK Corporation.

Computation of goodwill

Fair value of consideration given (24,000 x $22)

$528,000

Fair value of net assets acquired

($620,000 – $104,000)

(516,000)

Goodwill

$ 12,000

P1-30 Business Combination with Goodwill

a. Journal entry to record acquisition of Zink Company net assets:

Cash

20,000

Accounts Receivable

35,000

Inventory

50,000

Patents

60,000

Buildings and Equipment

150,000

Goodwill

38,000

Accounts Payable

55,000

Notes Payable

120,000

Cash

178,000

b. Balance sheet immediately following acquisition:

Anchor Corporation and Zink Company

Combined Balance Sheet

February 1, 20X3

Cash

$ 82,000

Accounts Payable

$140,000

Accounts Receivable

175,000

Notes Payable

270,000

Inventory

220,000

Common Stock

200,000

Patents

140,000

Additional Paid-In

Buildings and Equipment

530,000

Capital

160,000

Less: Accumulated

Retained Earnings

225,000

Depreciation

(190,000)

Goodwill

38,000

$995,000

$995,000

Investment in Zink Company Common Stock

178,000

Cash

178,000

Computation of goodwill

Fair value of consideration given

$178,000

Fair value of net assets acquired

($20,000 + $35,000 + $50,000 + $60,000

+ $150,000 – $55,000 -$120,000)

(140,000)

Goodwill

$ 38,000

Required fair value of reporting unit:

Fair value of assets at year-end

Fair value of liabilities at year-end (given)

Fair value of net assets at year-end

Original goodwill balance

Required fair value of reporting unit to avoid recognition of

impairment of goodwill

P1-31 Bargain Purchase

Journal entries to record acquisition of Lark Corporation net assets:

Merger Expense

5,000

Cash

5,000

Cash and Receivables

50,000

Inventory

150,000

Buildings and Equipment (net)

300,000

Patent

200,000

Accounts Payable

30,000

Cash

625,000

Gain on Bargain Purchase of Lark Corporation

45,000

Computation of gain

Fair value of consideration given

$625,000

Fair value of net assets acquired

($700,000 – $30,000)

(670,000)

Gain on bargain purchase

$ 45,000

P1-32 Computation of Account Balances

a.

Liabilities reported by the Aspro Division at year-end:

Fair value of reporting unit at year-end

$930,000

Acquisition price of reporting unit

($7.60 x 100,000)

$760,000

Fair value of net assets at acquisition

($810,000 – $190,000)

(620,000)

Goodwill at acquisition

$140,000

Impairment in current year

(30,000)

Goodwill at year-end

(110,000)

Fair value of net assets at year-end

$820,000

Fair value of assets at year-end

$950,000

Fair value of net assets at year-end

(820,000)

Fair value of liabilities at year-end

$130,000