Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments

E11-15 (continued)

4.

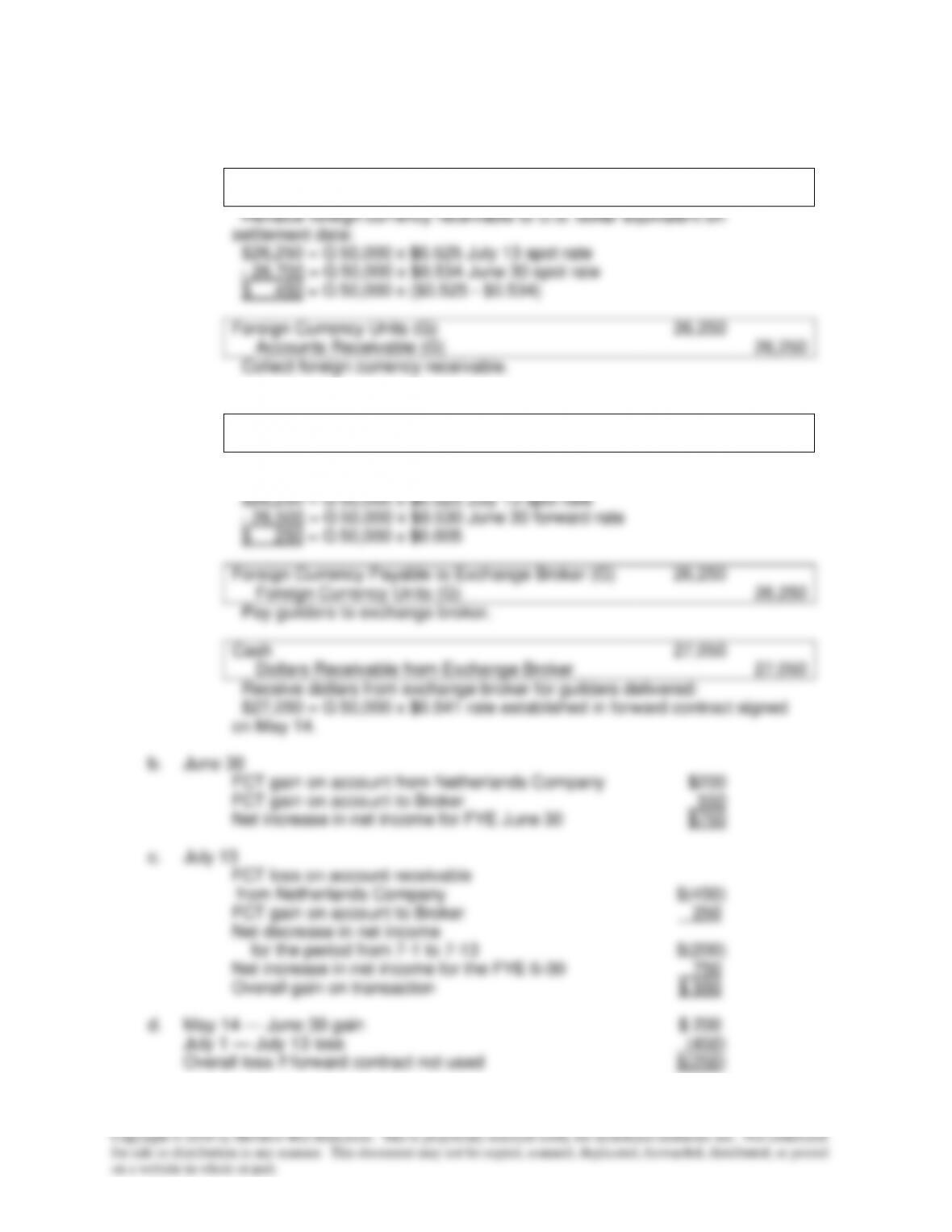

July 13

Foreign Currency Transaction Loss

450

Accounts Receivable (G)

450

Revalue foreign currency receivable to U.S. dollar equivalent on

settlement date:

$26,250 = G 50,000 x $0.525 July 13 spot rate

– 26,700 = G 50,000 x $0.534 June 30 spot rate

$ 450 = G 50,000 x ($0.525 – $0.534)

Foreign Currency Units (G)

26,250

Accounts Receivable (G)

26,250

Collect foreign currency receivable.

5.

July 13

Foreign Currency Payable to Exchange Broker (G)

250

Foreign Currency Transaction Gain

250

Revalue foreign currency payable to fair value at settlement date using

spot rate because the term of the contract has expired:

$26,250 = G 50,000 x $0.525 July 13 spot rate

– 26,500 = G 50,000 x $0.530 June 30 forward rate

$ 250 = G 50,000 x $0.005

Foreign Currency Payable to Exchange Broker (G)

26,250

Foreign Currency Units (G)

26,250

Pay guilders to exchange broker.

Cash

27,050

Dollars Receivable from Exchange Broker

27,050

Receive dollars from exchange broker for guilders delivered:

$27,050 = G 50,000 x $0.541 rate established in forward contract signed

on May 14.

b.

June 30

FCT gain on account from Netherlands Company

$200

FCT gain on account to Broker

550

Net increase in net income for FYE June 30

$750

c.

July 13

FCT loss on account receivable

from Netherlands Company

$(450)

FCT gain on account to Broker

250

Net decrease in net income

for the period from 7-1 to 7-13

$(200)

Net increase in net income for the FYE 6-30

750

Overall gain on transaction

$ 550

d.

May 14 — June 30 gain

$ 200

July 1 — July 13 loss

(450)

Overall loss if forward contract not used

$(250)

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

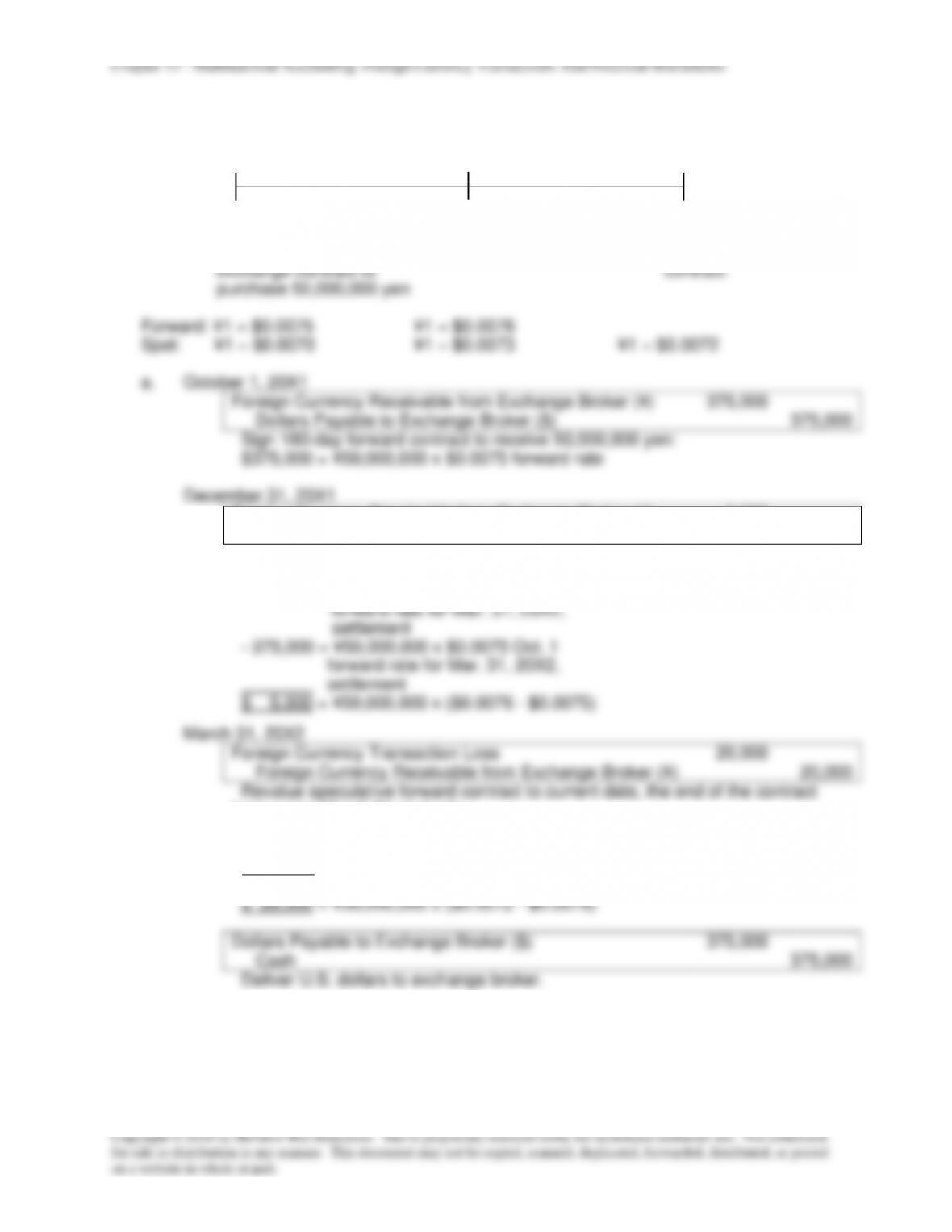

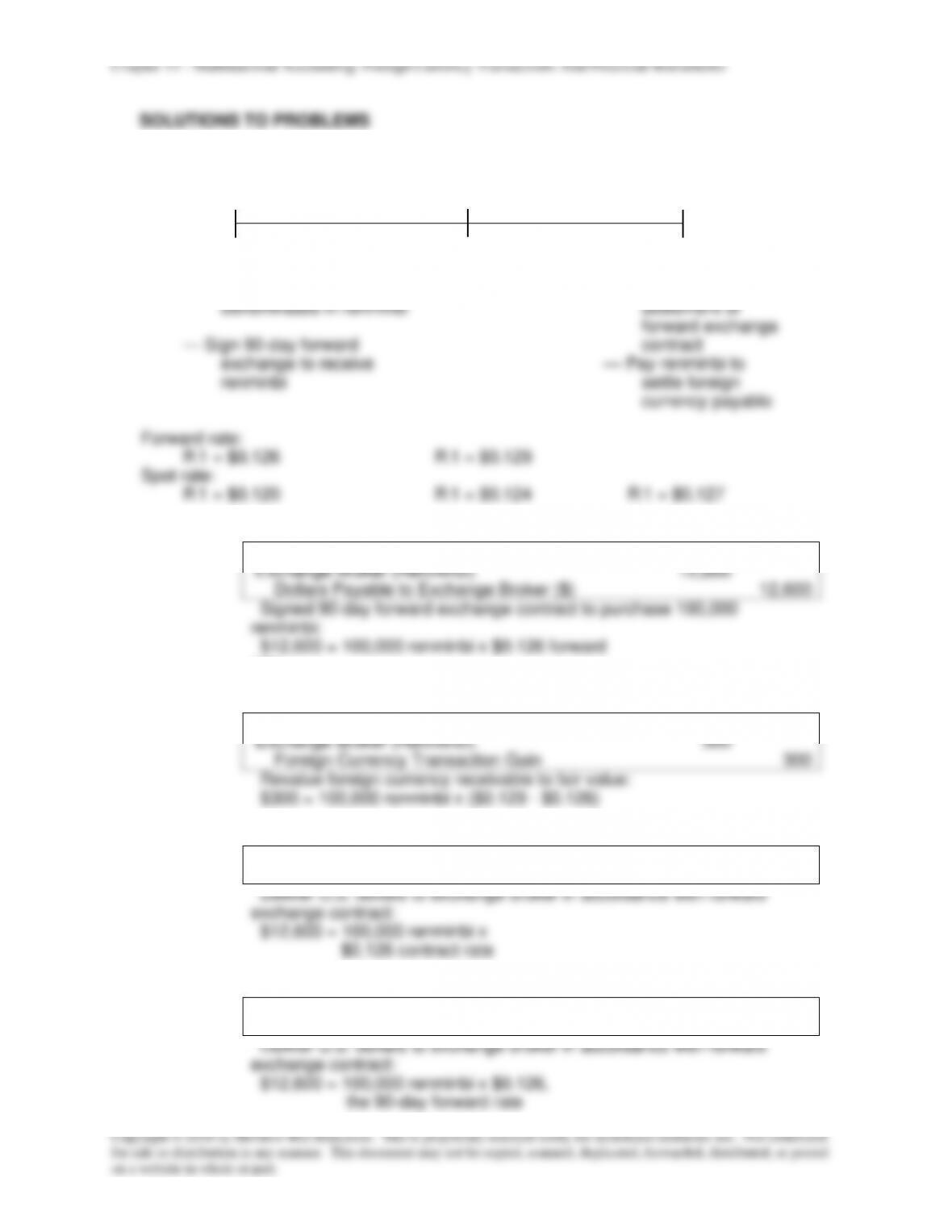

P11-20 Multiple-Choice Questions on Foreign Currency Transactions

11/1/X8

12/31/X8

1/30/X9

Transaction Date

Balance Sheet Date

Settlement Date

— Purchase with payable

— Receive renminbi upon

denominated in renminbi

settlement of

forward exchange

— Sign 90-day forward

contract

exchange to receive

— Pay renminbi to

renminbi

settle foreign

currency payable

Forward rate:

R 1 = $0.126

R 1 = $0.129

Spot rate:

R 1 = $0.120

R 1 = $0.124

R 1 = $0.127

1.

b –

November 1, 20X8

Foreign Currency Receivable from

Exchange Broker (Renminbi)

12,600

Dollars Payable to Exchange Broker ($)

12,600

Signed 90-day forward exchange contract to purchase 100,000

renminbi:

$12,600 = 100,000 renminbi x $0.126 forward

rate

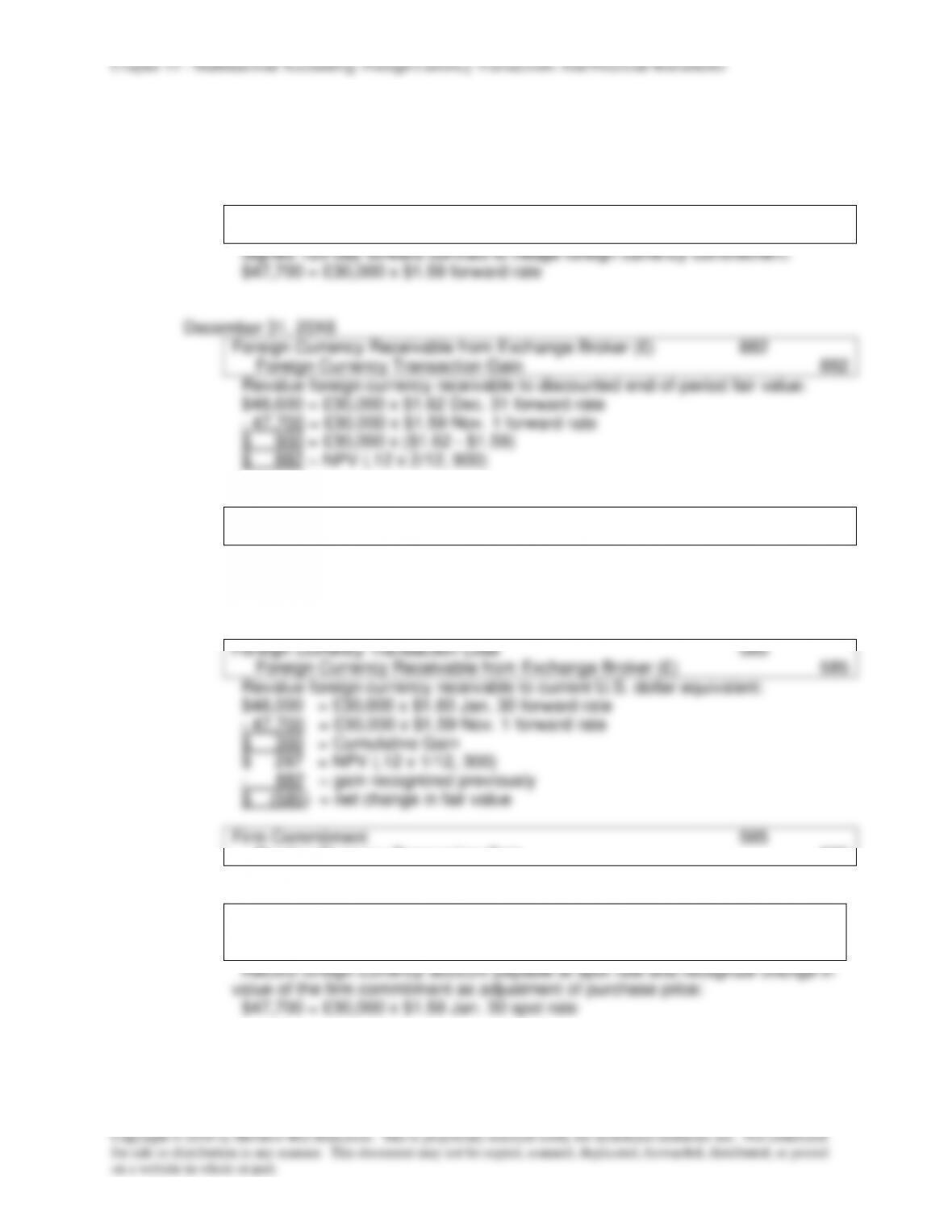

2.

c –

December 31, 20X8

Foreign Currency Receivable from

Exchange Broker (Renminbi)

300

Foreign Currency Transaction Gain

300

Revalue foreign currency receivable to fair value:

$300 = 100,000 renminbi x ($0.129 – $0.126)

3.

b –

January 30, 20X9

Dollars Payable to Exchange Broker ($)

12,600

Cash

12,600

Deliver U.S. dollars to exchange broker in accordance with forward

exchange contract:

$12,600 = 100,000 renminbi x

$0.126 contract rate

4.

b –

January 30, 20X9

Dollars Payable to Exchange Broker ($)

12,600

Cash

12,600

Deliver U.S. dollars to exchange broker in accordance with forward

exchange contract:

$12,600 = 100,000 renminbi x $0.126,

the 90-day forward rate