Which financial statement is (are) required for a voluntary health and welfare

organization which is not required for a private, not-for-profit hospital?

I. A statement of operations.

II. A statement of functional expenses.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

When a parent and its subsidiary use a periodic inventory system rather than a perpetual

system, the income and asset balances reported in the consolidated financial statements

are:

I. affected only if there are upstream intercompany sales of inventory.

II. affected only if there are downstream intercompany sales of inventory.

A. I

B. II

C. Both I and II

D. Neither I nor II

Crisfield Company has two reportable segments, C and D. Segment C made $4,000,000

of sales to external customers and $400,000 of sales to other operating segments.

Segment D, on the other hand, made sales of $8,000,000 to external customers and

$1,600,000 of sales to other operating segments. Crisfield Company reported

$13,200,000 of revenues on its consolidated income statement. What calculation below

correctly determines whether Crisfield Company’s reportable segments satisfy the 75%

revenue test?

A. $14,000,000/$15,200,000

B. $14,000,000/$13,200,000

C. $12,000,000/$13,200,000

D. $12,000,000/$15,200,000

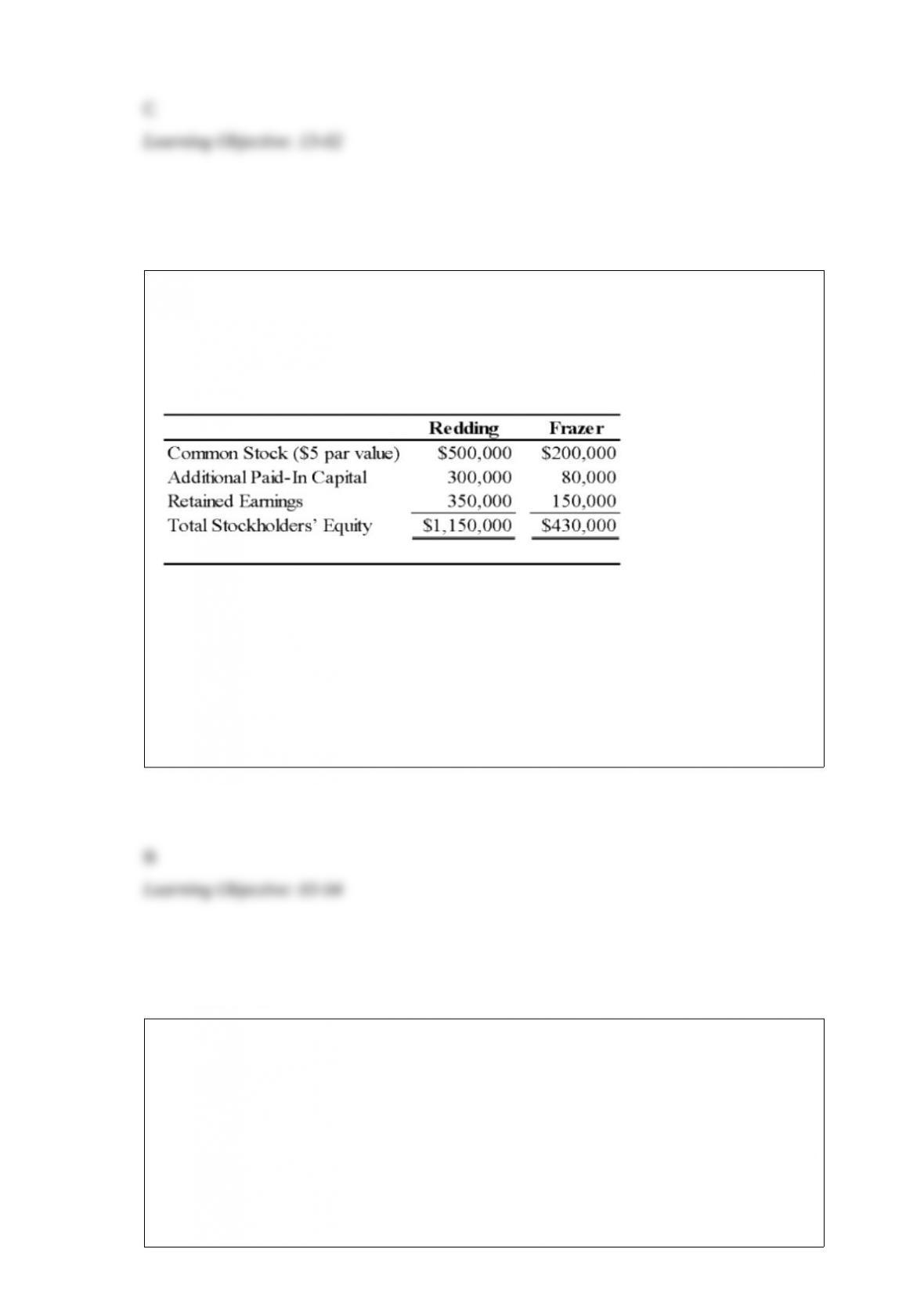

On January 3, 20X9, Redding Company acquired 80 percent of Frazer Corporation’s

common stock for $344,000 in cash. At the acquisition date, the book values and fair

values of Frazer’s assets and liabilities were equal, and the fair value of the

noncontrolling interest was equal to 20 percent of the total book value of Frazer. The

stockholders’ equity accounts of the two companies at the acquisition date are:

Noncontrolling interest was assigned income of $11,000 in Redding’s consolidated

income statement for 20X9.

Based on the preceding information, what will be the amount of net income reported by

Frazer Corporation in 20X9?

A. $44,000

B. $55,000

C. $66,000

D. $36,000

Suppose the direct foreign exchange rates in U.S. dollars are:

1 Singapore dollar = $0.7025

1 Cyprus pound = $2.5132

Based on the information given above, the indirect exchange rates for the Singapore

dollar and the Cyprus Pound (from a U.S. perspective) are:

A. 1.7655 Singapore dollars and 1.4235 Cyprus pounds respectively.

B. 0.2975 Singapore dollars and 1.5132 Cyprus pounds respectively.

C. 2.1622 Singapore dollars and 0.4625 Cyprus pounds respectively.

D. 1.4235 Singapore dollars and 0.3979 Cyprus pounds respectively.

Which of the following are established by ASC 280 as “enterprisewide disclosure”

standards to provide more information about the risks to a company?

I. Information about dominant industry segments.

II. Information about major customers.

III. Information about geographic areas

A. Both II and III

B. Both I and III

C. Both I and II

D. I, II, and II

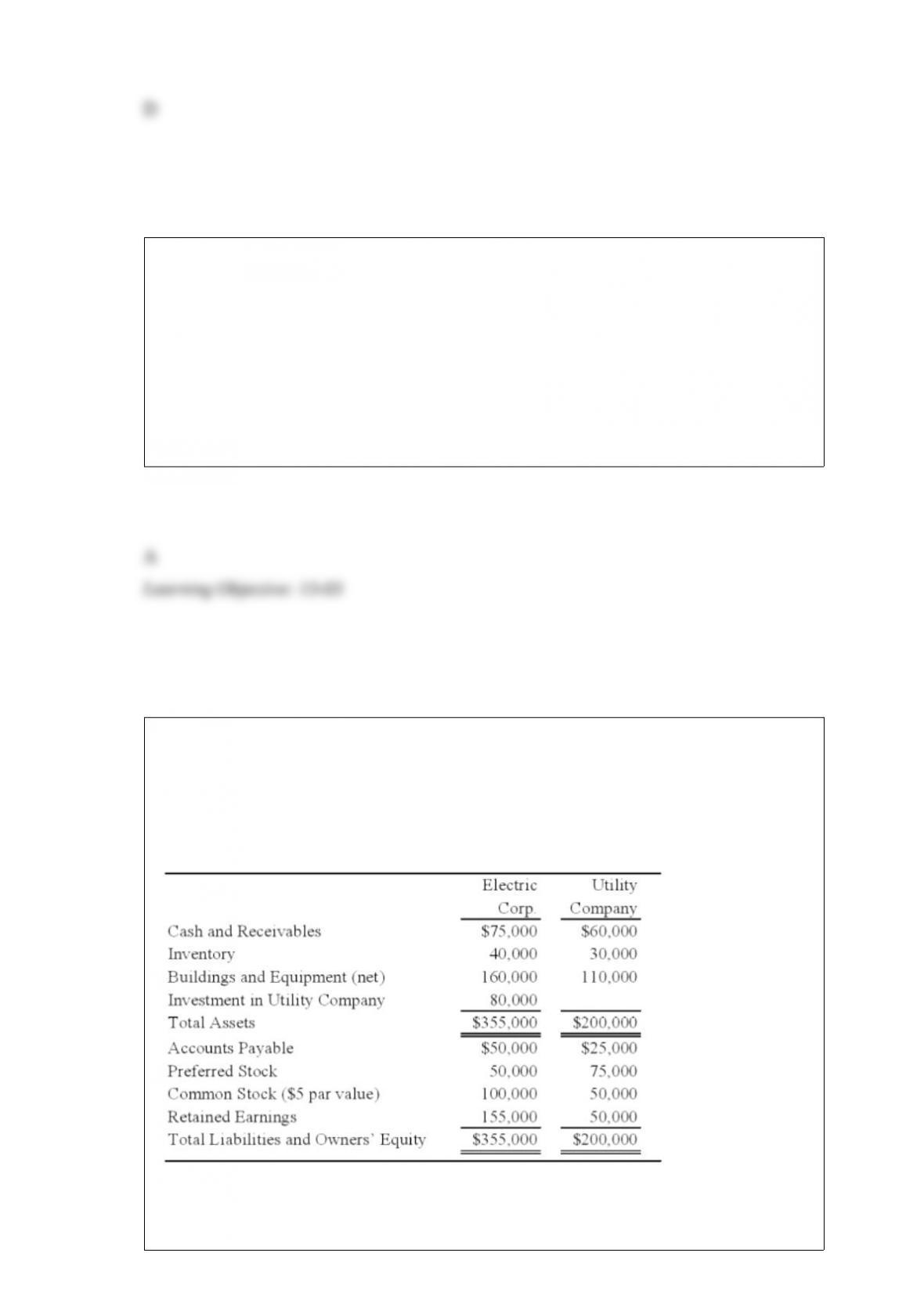

Electric Corporation holds 80 percent of Utility Company’s voting common shares,

acquired at book values, but none of its preferred shares. At the date of acquisition, the

fair value of the noncontrolling interest was equal to 20 percent of the book value of

Utility Company. Summary balance sheets for the companies on December 31, 20X8,

are as follows:

Neither of the preferred issues is convertible. Electric’s preferred pays a 8 percent

annual dividend, and Utility’s preferred pays a 12 percent dividend. Utility reported net

income of $30,000 and paid a total of $10,000 of dividends in 20X8. Electric reported

income from its separate operations of $70,000 and paid total dividends of $25,000 in

20X8.

Based on the preceding information, what is the consolidated earnings per share for

20X8?

A. 4.46

B. 4.14

C. 4.35

D. 4.55

Blue Corporation holds 70 percent of Black Company’s voting common stock. On

January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected

economic life. Black uses straight-line depreciation for all depreciable assets. On

December 31, 20X8, Blue purchased the building from Black for $180,000. Blue

reported income, excluding investment income from Black, of $140,000 and $162,000

for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000

for 20X8 and 20X9, respectively.

Based on the preceding information, the amount to be reported as consolidated net

income for 20X9 will be:

A. $207,000.

B. $202,000.

C. $212,000.

D. $190,000.

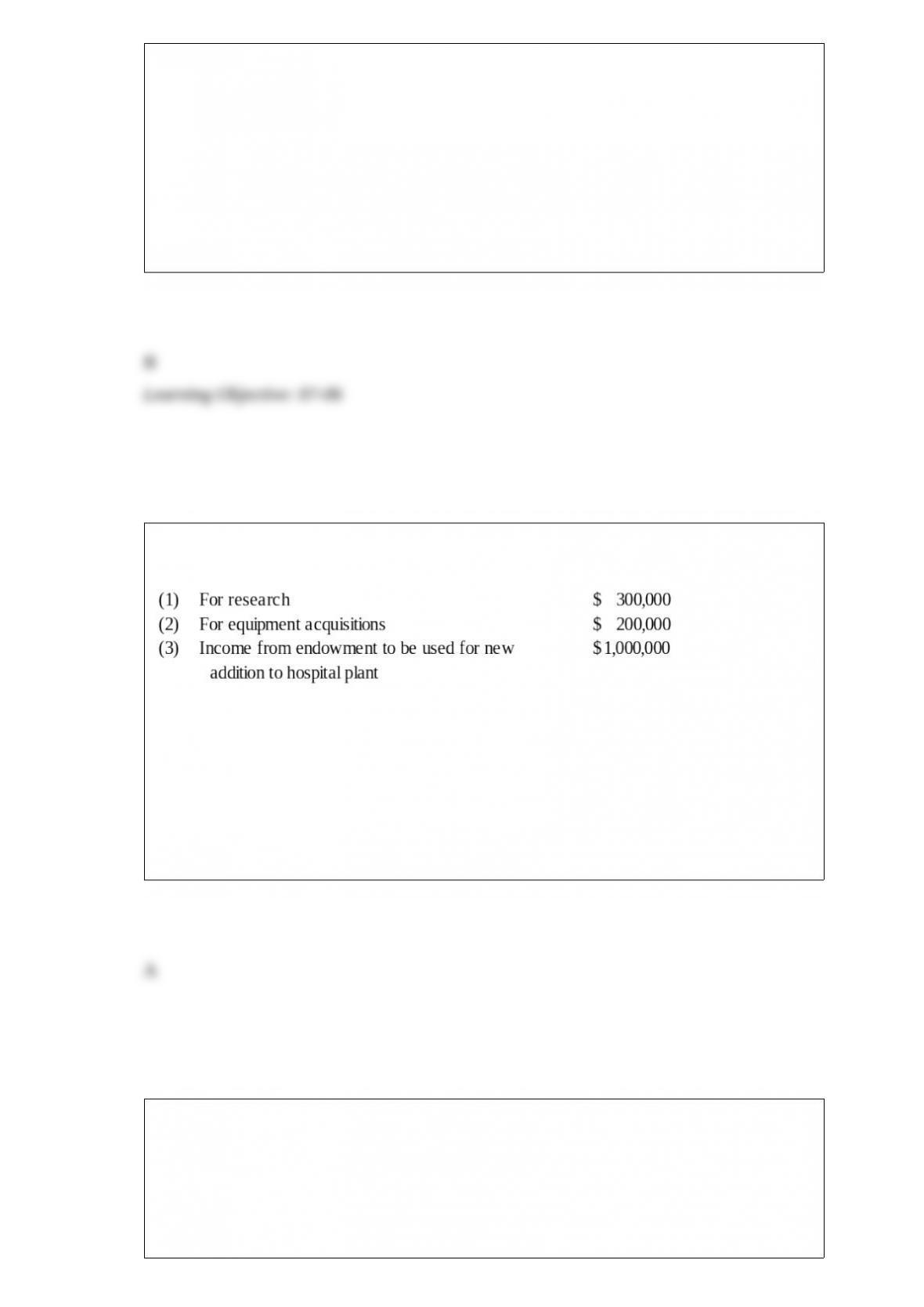

A private, not-for-profit hospital received the following restricted contributions and

other receipts during the year ended December 31, 20X8:

None of the contributions or other receipts were expended during the ended December

31, 20X8. For the year ended December 31, 20X8, what amount would be reported on

the hospital’s statement of changes in net assets as an increase in temporarily restricted

net assets?

A. $1,500,000

B. $1,200,000

C. $500,000

D. $300,000

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Received tuition revenue from hospital nursing program and cash from

sales of goods in the hospital gift shop.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

Which of the following observations regarding the use of fresh start accounting is true?

A. It is always required under Chapter 11 bankruptcy proceedings.

B. Prior shareholders will have control of the emerging company.

C. It results in a new reporting entity.

D. It is used under Chapter 7 bankruptcy proceedings.

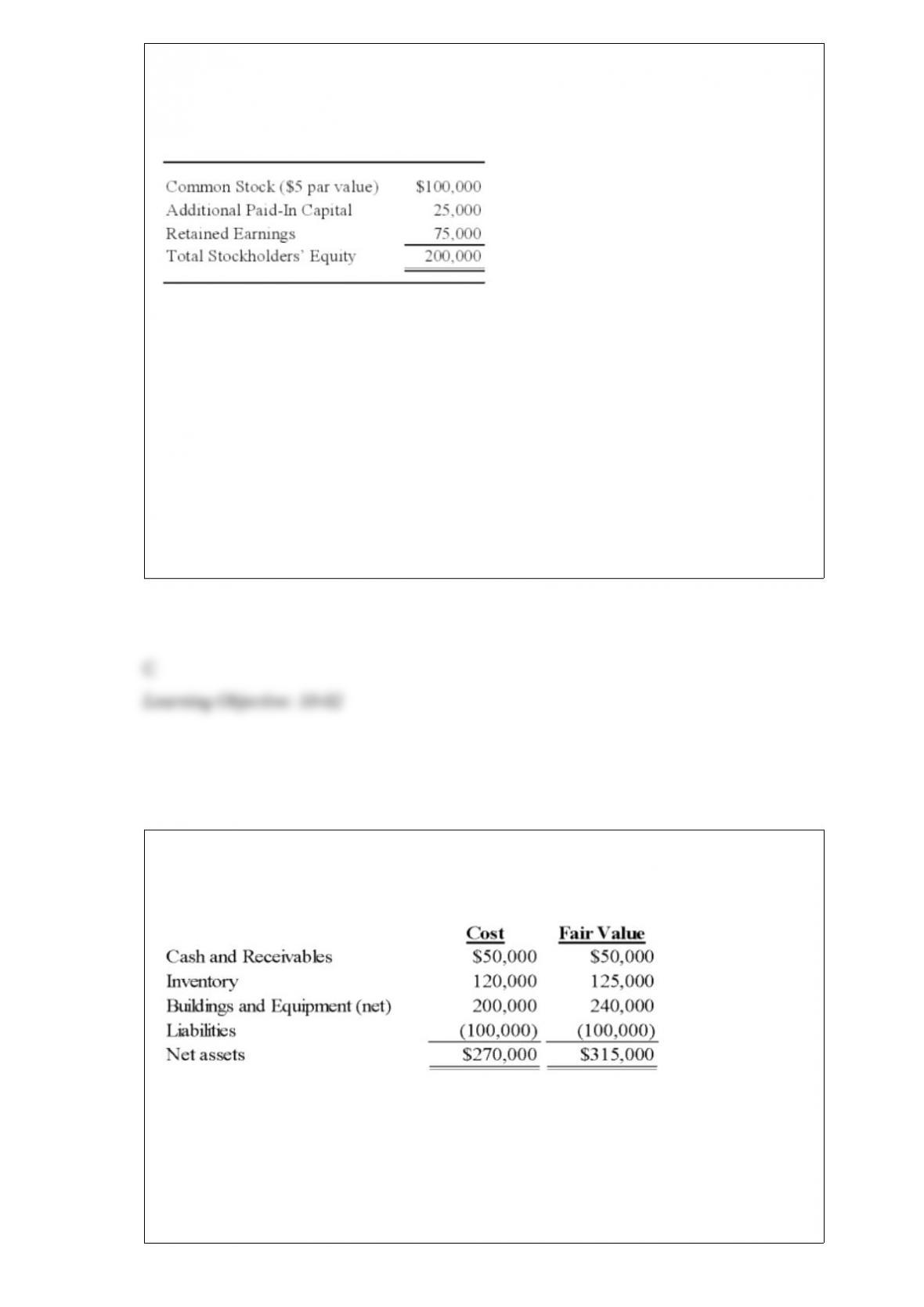

On January 1, 20X9, Heathcliff Corporation acquired 80 percent of Garfield

Corporation’s voting common stock. Garfield’s buildings and equipment had a book

value of $300,000 and a fair value of $350,000 at the time of acquisition.

Based on the preceding information, what will be the amount at which Garfield’s

buildings and equipment will be reported in consolidated statements using the parent

company approach?

A. $350,000

B. $340,000

C. $280,000

D. $300,000

Which of the following observations is true of an S corporation?

A. It elects to be taxed in the same manner as a corporation.

B. It does not have the burden of double taxation of corporate income.

C. Its shareholders have personal liability for the corporation’s obligations.

D. Its primary income source should be passive investments.

All restricted funds of private, not-for-profit hospitals account for resources:

A. whose use is restricted by the donor.

B. received and expended in the hospital’s primary health care mission.

C. that are only temporarily restricted.

D. received or pledged by donors for use in future periods.

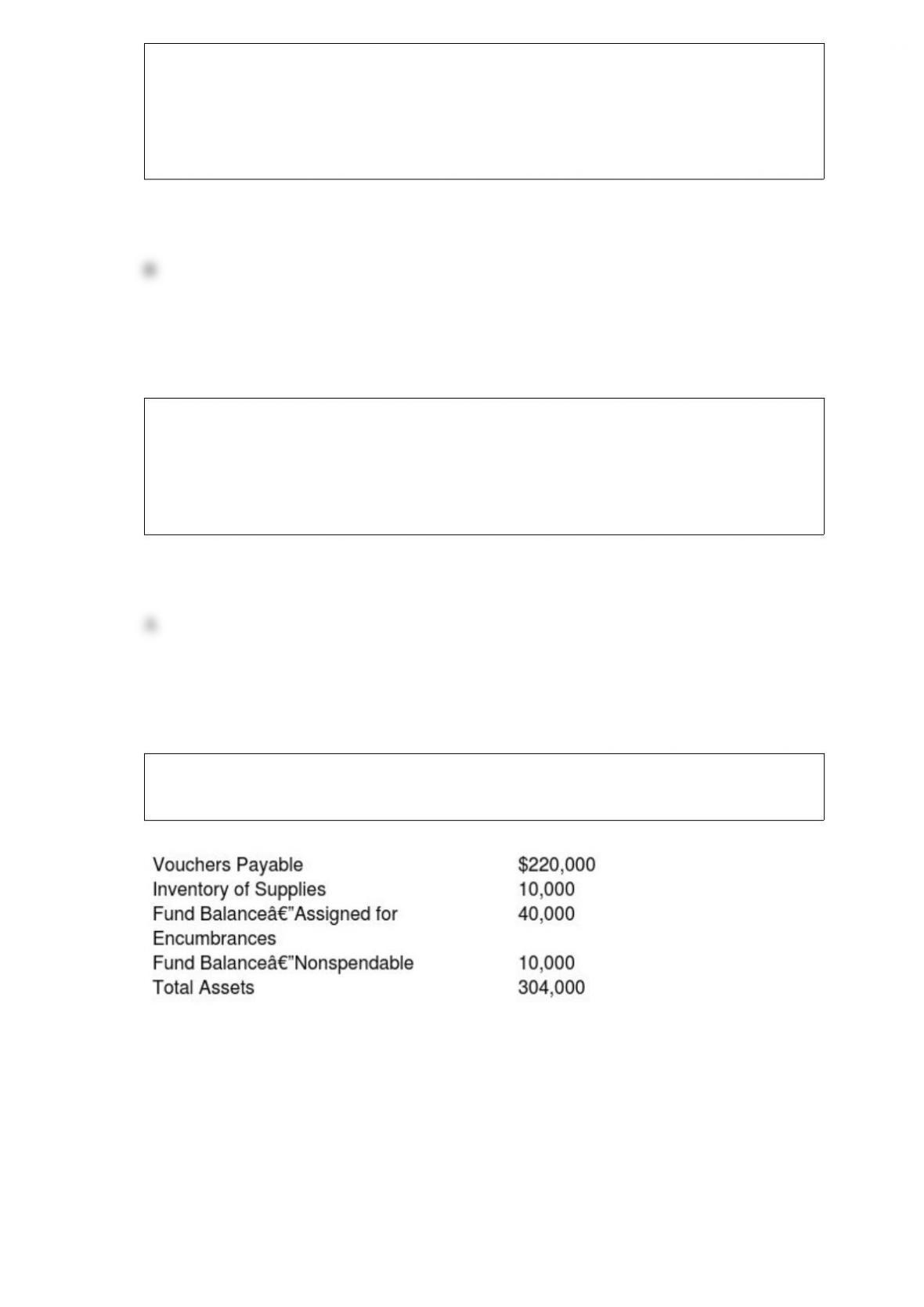

The following information was obtained from the general fund balance sheet of Lima

Village on June 30, 20X9, the close of its fiscal year:

On June 30, 20X9, what was Lima’s unassigned fund balance in its general fund?

A. $84,000

B. $44,000

C. $34,000

D. $24,000

Any intercompany gain or loss on a downstream sale of land should be recognized in

consolidated net income:

I. in the year of the downstream sale.

II. over the period of time the subsidiary uses the land.

III. in the year the subsidiary sells the land to an unrelated party.

A. I

B. II

C. III

D. I or II

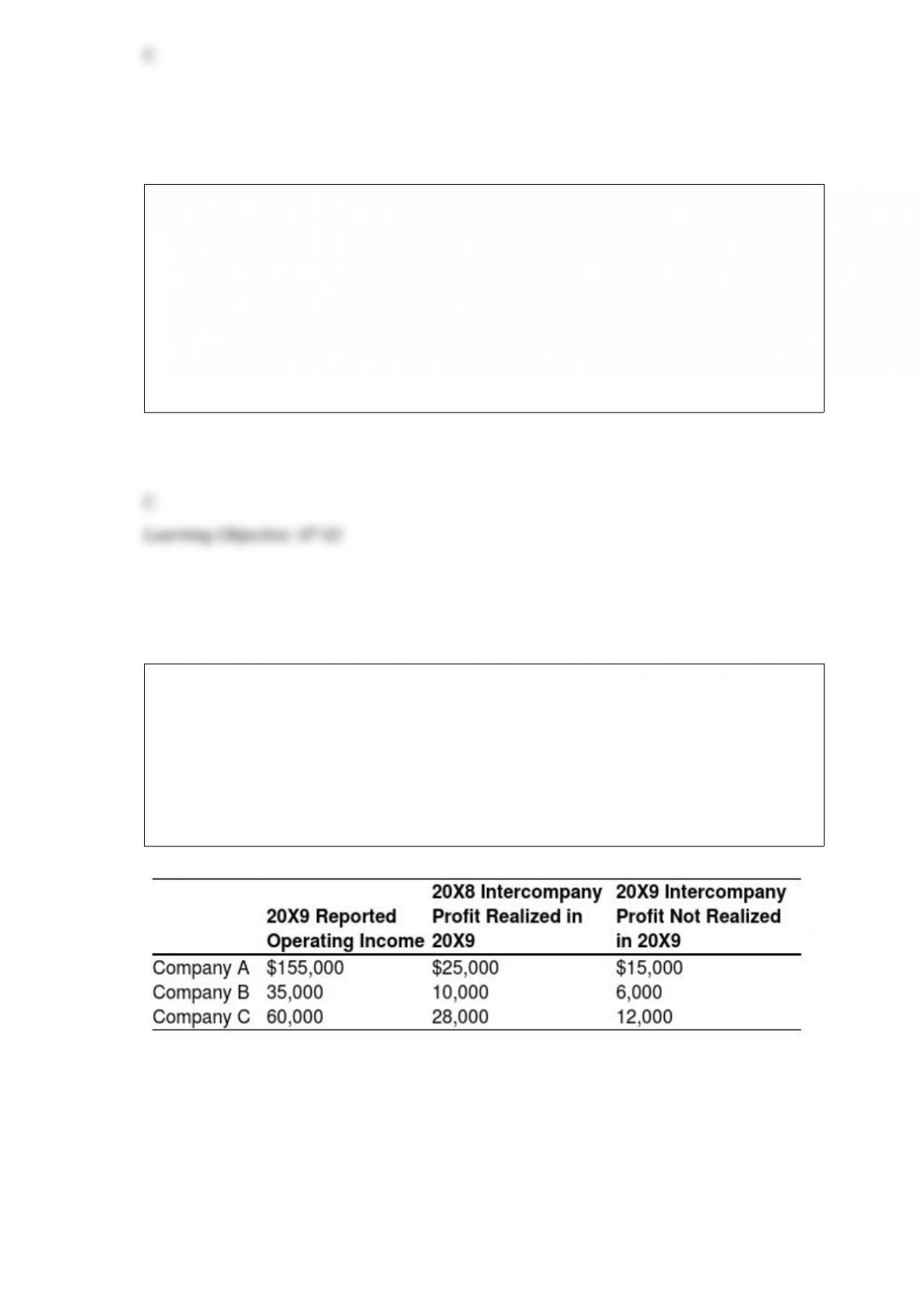

Company A owns 85 percent of Company B’s stock and 80 percent of Company C’s

stock. All acquisitions were made at book value. The fair values of noncontrolling

interests at the time of acquisition were equal to the proportionate share of the book

values of the companies. The companies file a consolidated tax return each year and in

20X9 paid a total tax of $112,000. Each company is involved in a number of

intercompany inventory transfers each period. Information on the companies’ activities

for 20X9 is as follows:

Company A does not record income tax expense on income from subsidiaries because a

consolidated tax return is filed.

Based on the information provided, what amount of income tax expense should be

assigned to Company A?

A. $72,000

B. $66,000

C. $112,000

D. $62,000

On January 1, 20X2, Ephraim Corporation acquired 80 percent of Lilac Corporation for

$200,000 cash. Lilac reported net income of $25,000 each year and dividends of $5,000

each year for 20X2, 20X3, and 20X4. On January 1, 20X2, Lilac reported common

stock outstanding of $160,000 and retained earnings of $40,000, and the fair value of

the noncontrolling interest was $50,000. It held land with a book value of $90,000 and a

market value of $100,000, and equipment with a book value of $40,000 and a market

value of $48,000 at the date of combination. The remainder of the differential at

acquisition was attributable to an increase in the value of patents, which had a

remaining useful life of eight years. All depreciable assets held by Lilac at the date of

acquisition had a remaining economic life of eight years. Ephraim uses the equity

method in accounting for its investment in Lilac.

Based on the preceding information, what balance would Ephraim report as its

investment in Lilac at January 1, 20X4?

A. $200,000

B. $224,000

C. $232,000

D. $240,000

Point Co. purchased 90% of Sharpe Corp.’s voting stock on January 1, 20X2 for

$5,580,000. Prior to the acquisition, Point held a 10% equity position in Sharpe

Company. On January 1, 20X2 Pointe’s 10% investment in Sharpe has a book value of

$340,000 and a fair value of $620,000. On January 1, 20X2 Point records the following:

A. Debit Gain on revaluation of Sharpe’s stock $280,000

B. Credit Gain on revaluation of Sharpe’s stock $280,000

C. Credit Investment in Sharpe stock $5,860,000

D. Debit Investment in Sharpe stock $6,200,000

Which of the following accounts could be found in the PQ partnership’s general ledger?

I. Due from P

II. P, Drawing

III. Loan Payable to Q

A. I, II

B. I, III

C. II, III

D. I, II, and III

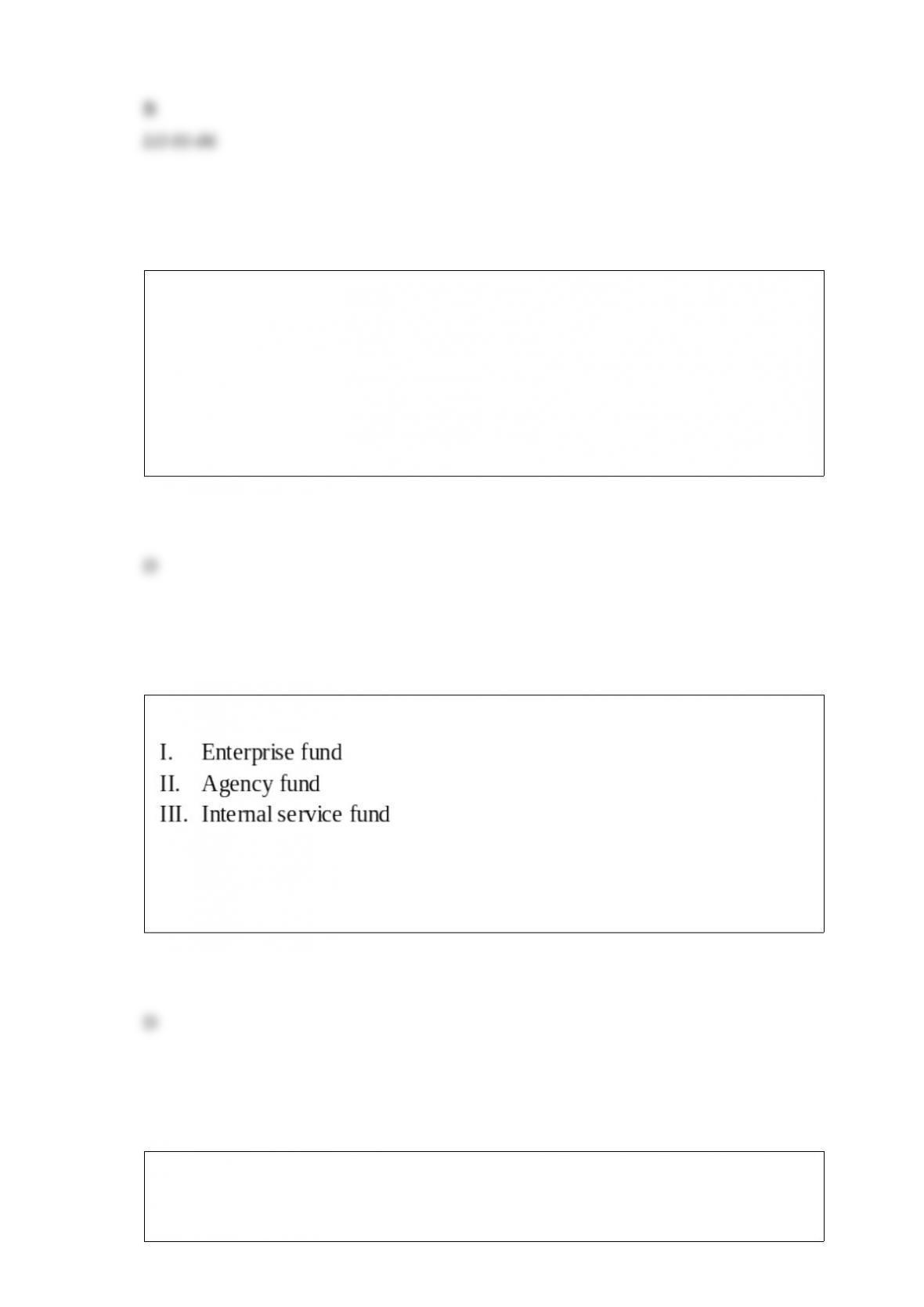

Which of the following funds use the accrual basis of accounting?

A. I only

B. II only

C. I and III only

D. I, II, and III

In accordance with ASC 958, contributions of services are recognized as increases in

unrestricted net assets by a private, not for profit entity if which of the following criteria

are satisfied?

I. The services received create or enhance nonfinancial assets.

II. The services require specialized skills, are provided by individuals possessing those

skills, and would typically need to be purchased if not provided by donations.

III. The services will be performed within the current fiscal year.

A. I or II.

B. I or III.

C. II or III.

D. I, II, III.

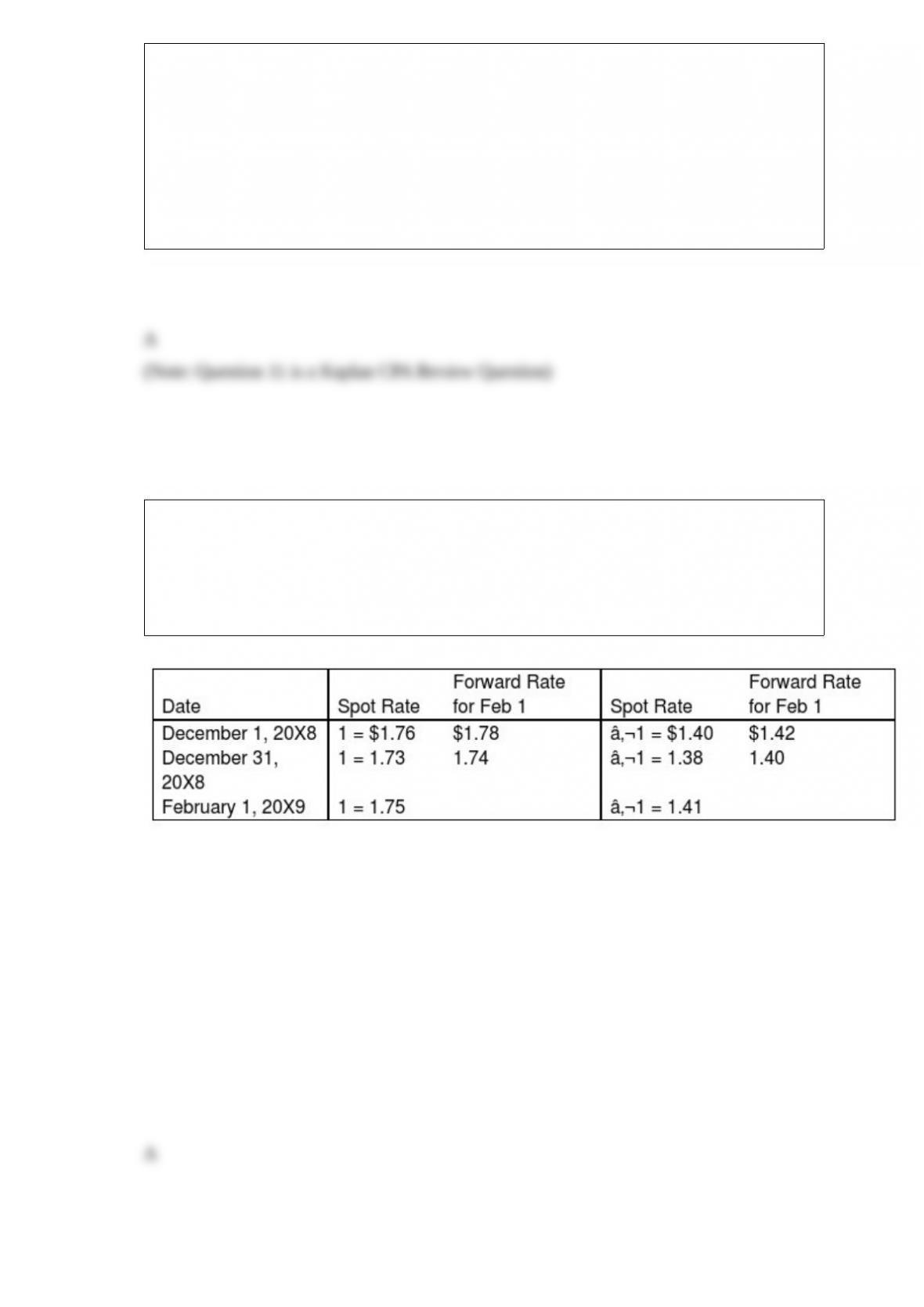

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the overall effect of speculation on 20X9 net

income?

A. $1,000 loss

B. $6,000 gain

C. $3,000 loss

D. $8,000 gain

Catalyst Corporation acquired 90 percent of Trigger Corporation’s common stock on

September 30, 20X8 for $225,000. At that date, the fair value of the noncontrolling

interest was $25,000. On January 1, 20X8, Trigger reported the following stockholders’

equity balances:

Trigger reported net income of $80,000 in 20X8, earned uniformly throughout the year,

and declared and paid dividends of $10,000 on June 30 and $30,000 on December 31,

20X8. Catalyst reported retained earnings of $250,000 on January 1, 20X8, and had

20X8 income of $120,000 from its separate operations. Catalyst paid dividends of

$50,000 on December 31, 20X8. Catalyst accounts for its investment in Trigger

Corporation using the fully adjusted equity method.

Based on the information provided, what is the amount of consolidated retained

earnings as of December 31, 20X8?

A. $340,000

B. $250,000

C. $338,000

D. $388,000

On July 1, 20X9, Link Corporation paid $340,000 for all of Tinsel Company’s

outstanding common stock. On that date, the costs and fair values of Tinsel’s recorded

assets and liabilities were as follows:

Based on the preceding information, what amount should be allocated to goodwill in

the consolidated balance sheet, prepared after this business combination?

A. $0

B. $25,000

C. $70,000

D. $45,000

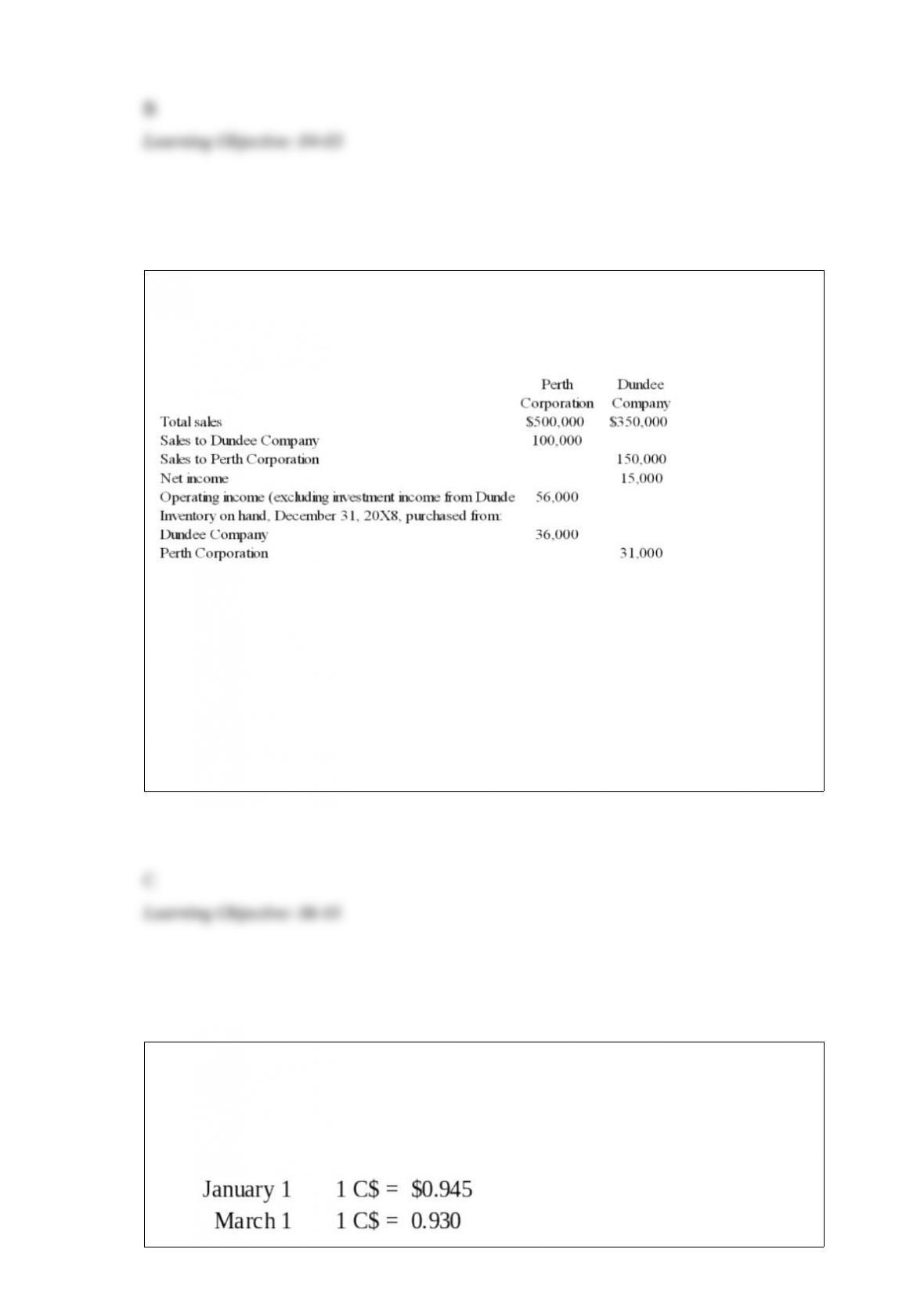

Perth Corporation owns 90 percent of Dundee Company’s stock. At the end of 20X8,

Perth and Dundee reported the following partial operating results and inventory

balances:

Perth regularly prices its products at cost plus a 30 percent markup for profit. Dundee

prices its sales at cost plus a 10 percent markup. The total sales reported by Perth and

Dundee include both intercompany sales and sales to nonaffiliates.

Based on the information given above, what amount of sales will be reported in the

consolidated income statement for 20X8?

A. $500,000

B. $850,000

C. $600,000

D. $800,000

Myway Company sold equipment to a Canadian company for 100,000 Canadian dollars

(C$) on January 1, 20X9 with settlement to be in 60 days. On the same date, Myway

entered into a 60-day forward contract to sell 100,000 Canadian dollars at a forward

rate of 1 C$ = $.94 in order to manage its exposed foreign currency receivable. The

forward contract is not designated as a hedge. The spot rates were:

Based on the preceding information, what is the overall effect on net income of

Myway’s use of the forward exchange contract?

A. Net loss of $1,000

B. Net gain of $1,500

C. Net loss of $500

D. No effect

Pro forma disclosures are:

A. used to disclose unscheduled material events.

B. interim financial statements need not be audited.

C. materials submitted to shareholders for votes on corporate matters.

D. “what-if” presentations often taking the form of summarized financial statements.

Mom Corporation acquired 75 percent of Daughter Company’s voting shares on

January 1, 20X7, at underlying book value. On December 31, 20X7, it also purchased

$300,000 par value 9 percent Daughter bonds, which had been issued on January 1,

20X3 to Parry Corporation (unaffiliated with either Mom or Daughter) at a $20,000

premium. The bonds were originally issued with a 10-year maturity and pay interest

annually on December 31. During preparation of the consolidated financial statements

for December 31, 20X7, the following consolidation entry was included in the

consolidation worksheet:

Bonds Payable 300,000

Bond Premium 11,902

Loss on Bond Retirement 12,098

Investment in Daughter Company Bonds 324,000

Based on the information given above, what is the interest income that must be

eliminated in preparing the 20X7 consolidated financial statements?

A. $11,902

B. $22,830

C. $24,000

D. $29,160

The JKL partnership liquidated its business in 20X9. Due to an expected long

liquidation period, a cash distribution plan was developed. The initial sale and

realization of cash from noncash assets resulted in partner K properly getting $24,000.

No other partners received cash along with K. Based upon this information, which of

the following statements is correct?

I. K’s loss absorption power (LAP) was higher than J’s LAP and L’s LAP.

II. K’s capital balance was substantially larger than the balances of J and L.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Parent Corporation owns 90 percent of Subsidiary 1 Company’s stock and 75 percent of

Subsidiary 2 Company’s stock. During 20X8, Parent sold inventory purchased in 20X7

for $48,000 to Subsidiary 1 for $60,000. Subsidiary 1 then sold the inventory at its cost

of $60,000 to Subsidiary 2. Prior to December 31, 20X8, Subsidiary 2 sold $45,000 of

inventory to a nonaffiliate for $67,000 and held $15,000 in inventory at December 31,

20X8.

Based on the information given above, what amount of cost of goods sold must be

eliminated from the consolidated income statement for 20X8?

A. $117,000

B. $120,000

C. $150,000

D. $128,000

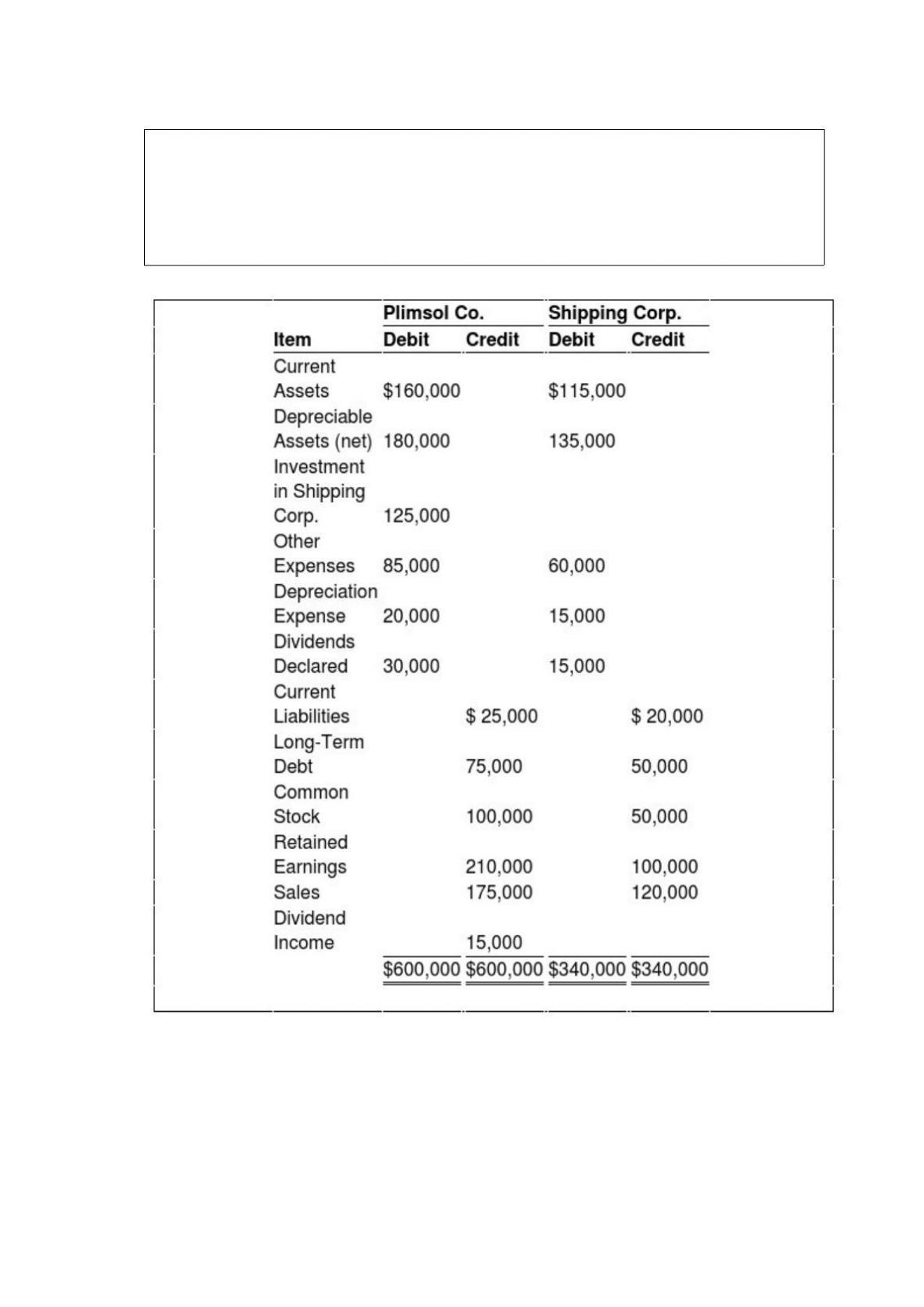

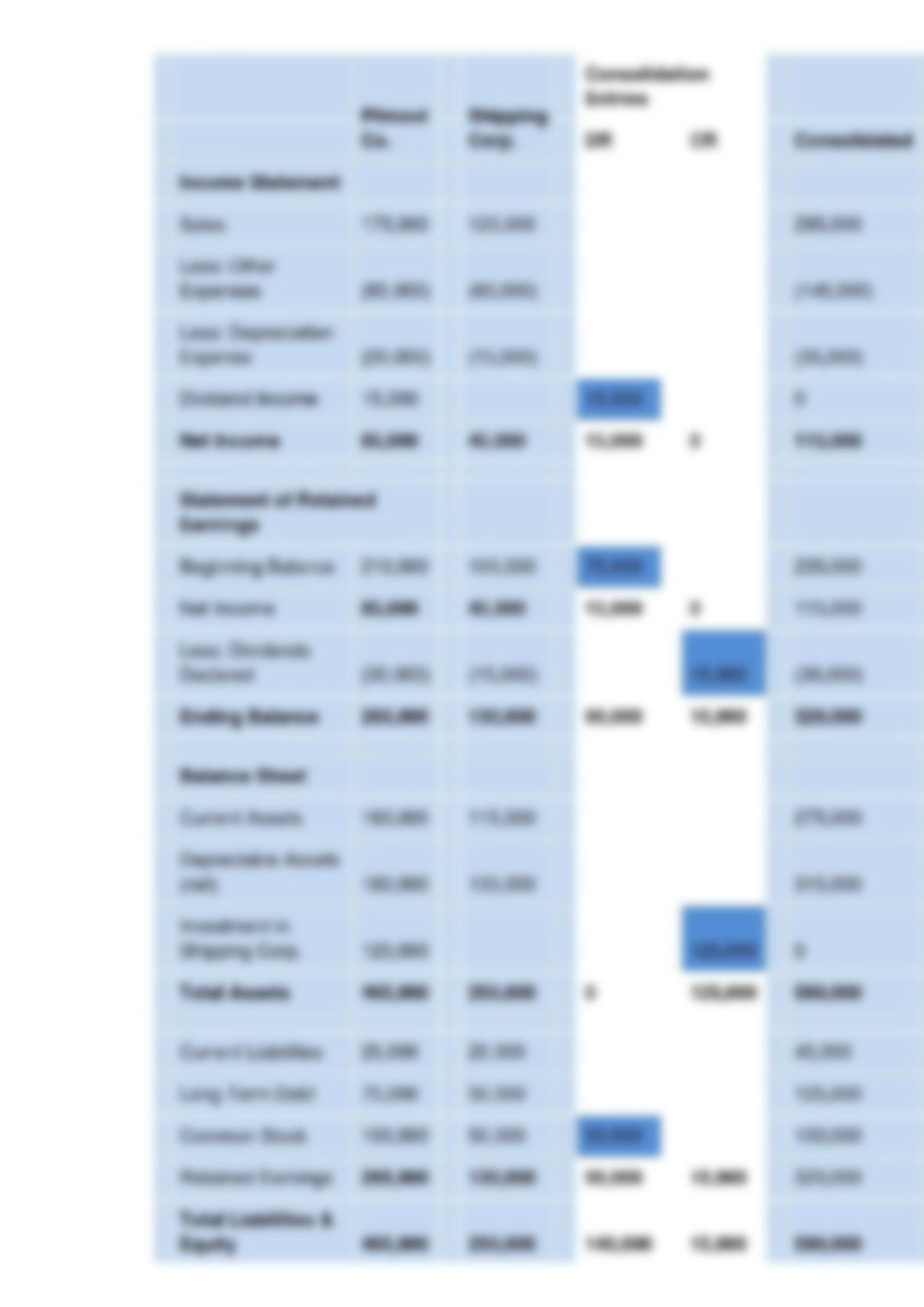

On January 1, 20X7, Plimsol Company acquired 100 percent of Shipping Corporation’s

voting shares, at underlying book value. Plimsol uses the cost method in accounting for

its investment in Shipping. Shipping’s reported retained earnings of $75,000 on the date

of acquisition. The trial balances for Plimsol Company and Shipping Corporation as of

December 31, 20X8, follow:

Required:

1) Provide all consolidating entries required to prepare a full set of consolidated statements

for 20X8.

2) Prepare a three-part consolidation worksheet in good form as of December 31, 20X8.

Pepper Company acquired 60 percent of the common stock of Safton Corporation on

December 31, 20X9. On the date of acquisition, Pepper held land with a book value of

$200,000 and a fair value of $350,000; Safton held land with a book value of $150,000

and fair value of $300,000. At what amount would land be reported in a consolidated

balance sheet prepared immediately after the combination?

A. $290,000

B. $500,000

C. $590,000

D. $650,000

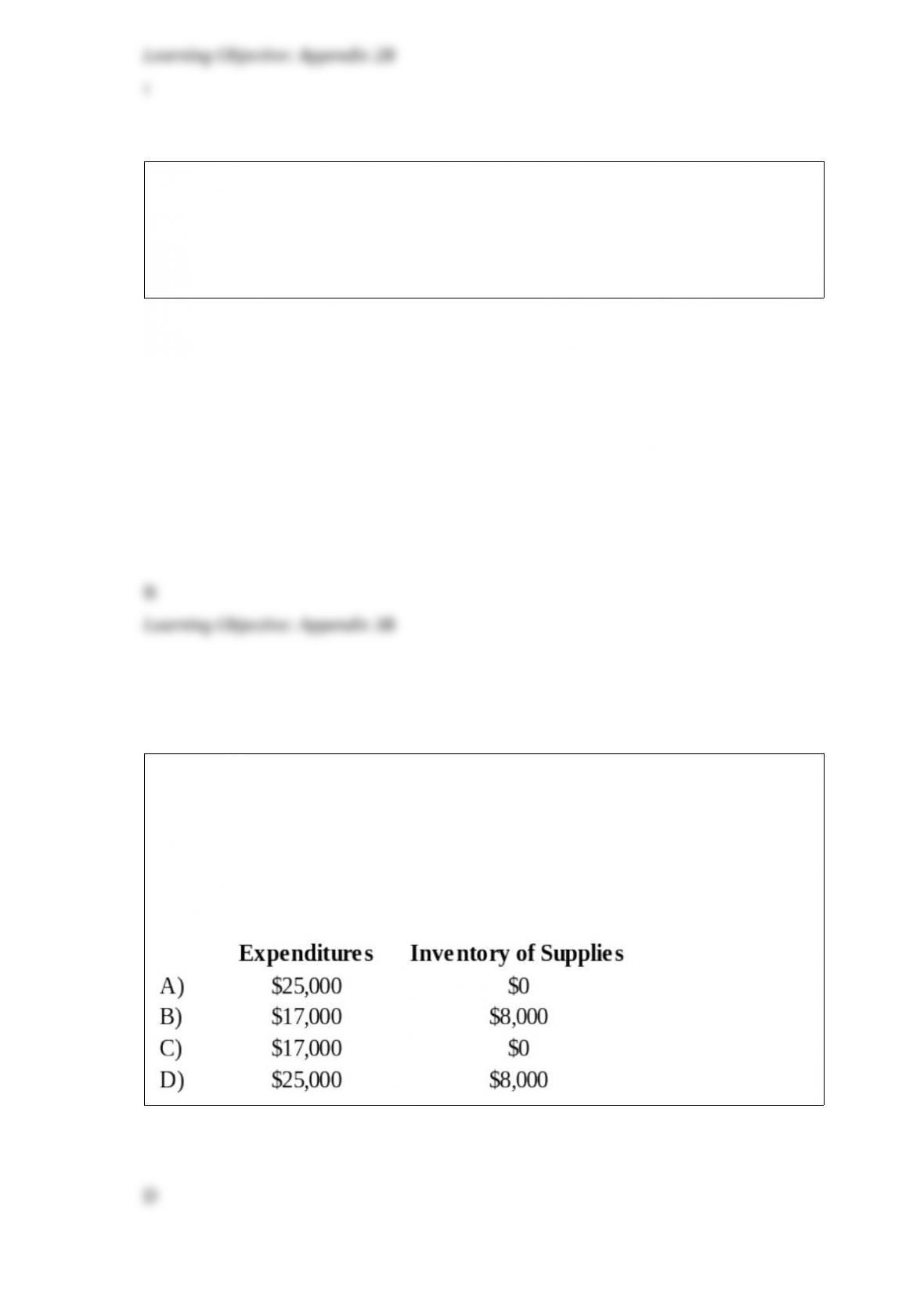

Gotham City acquires $25,000 of inventory on November 1, 20X7, having held no

inventory previously. On December 31, 20X7, the end of Gotham City’s fiscal year, a

physical count shows $8,000 still in stock. During 20X8, $6,500 of this inventory is

used, resulting in a $1,500 remaining balance of supplies on December 31, 20X8.

Based on the preceding information, which of the following would be the correct

account balances for 20X7 if Gotham City used the purchase method of accounting for

inventories?

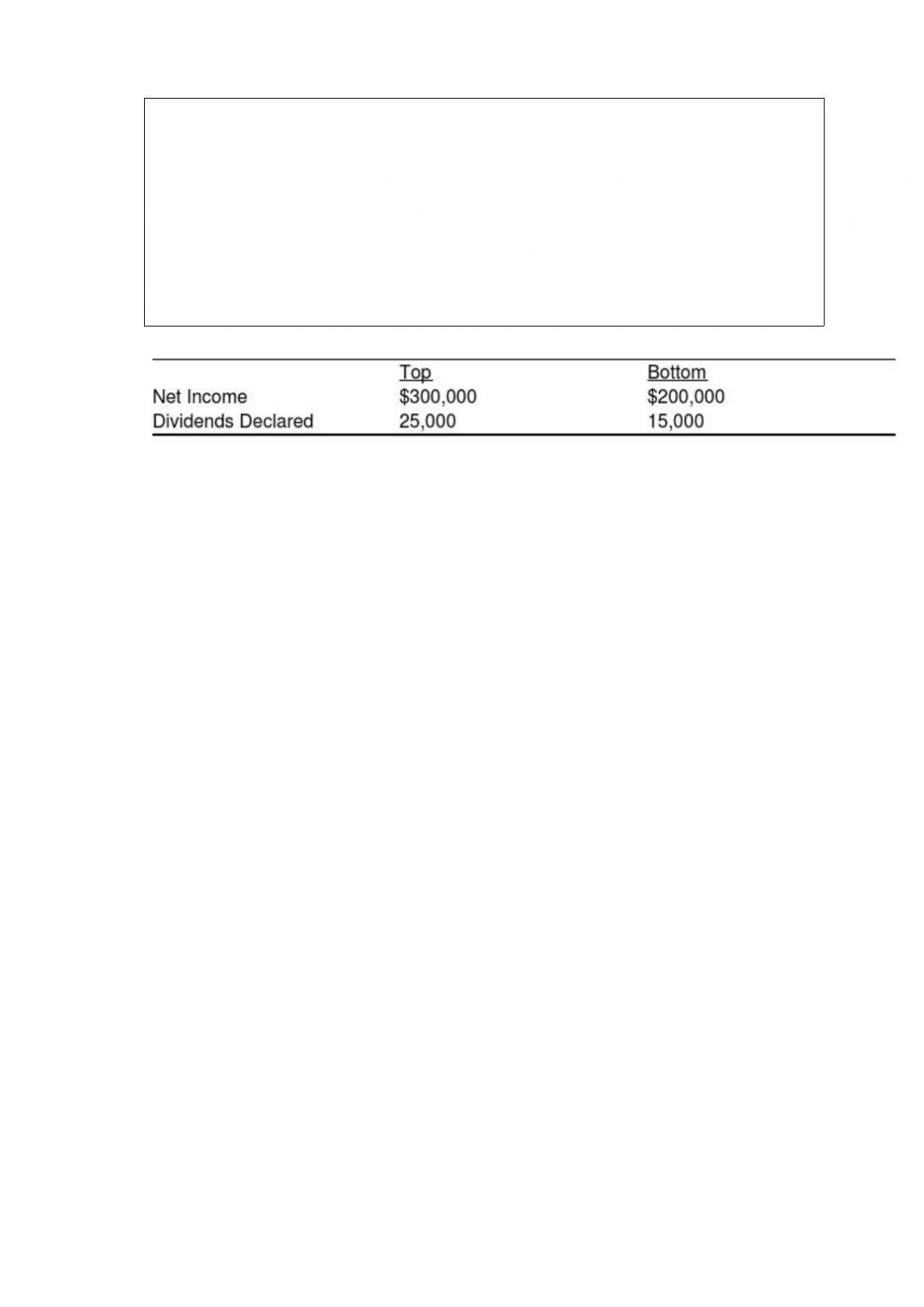

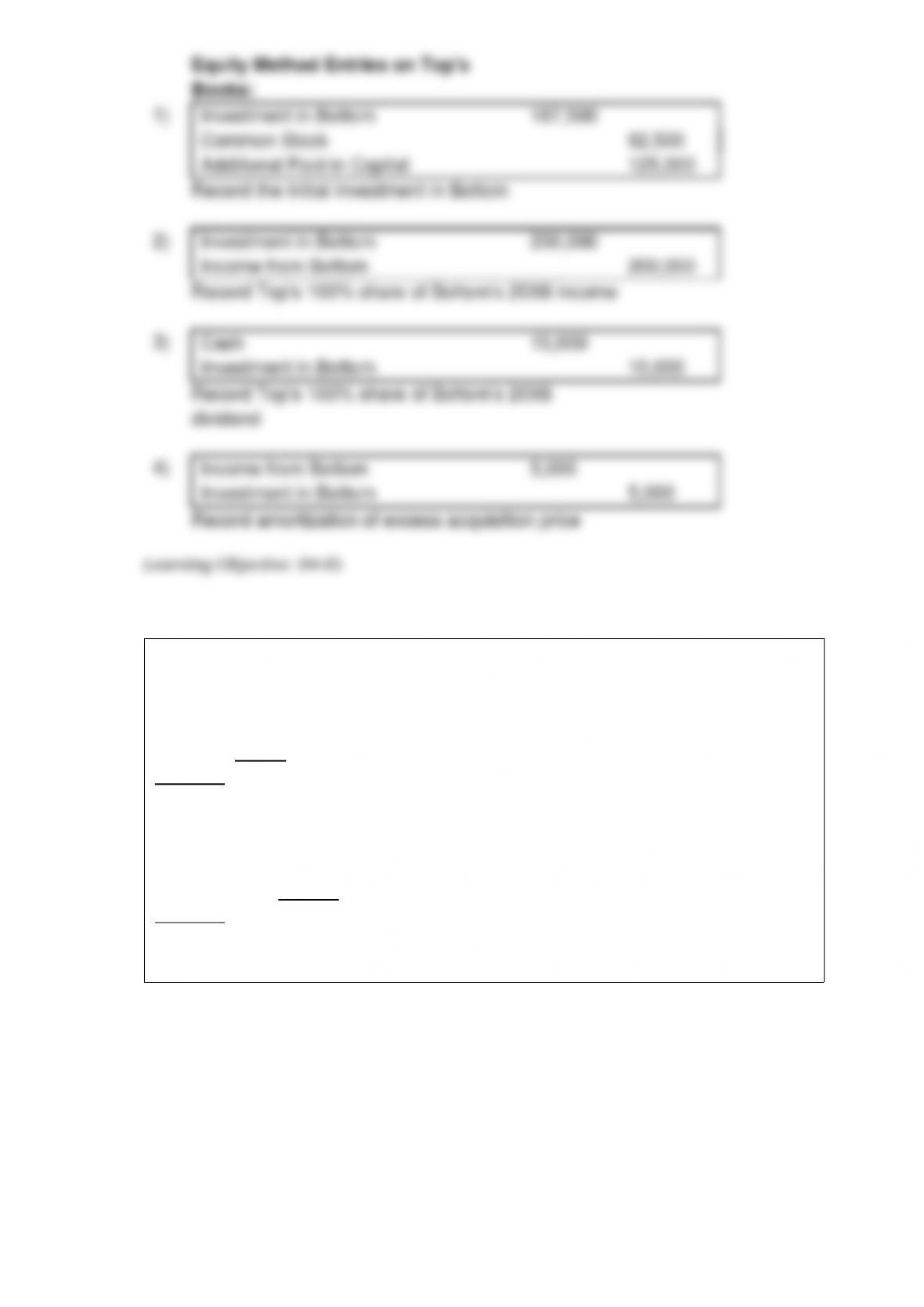

Top Company obtained 100 percent of Bottom Company’s common stock on January 1,

20X6 by issuing 12,500 shares of its own common stock, which had a $5 par value and

a $15 fair value on that date. Bottom reported a net book value of $150,000 and its

shares had a $20 per share fair value on that date. However, some of its plant assets

(with a 5-year remaining life) were undervalued by $20,000 in the company’s

accounting records. Bottom had also developed a customer list with an estimated fair

value of $10,000 and a remaining life of 10 years. Top Company uses the

equity-method to account for its investment in Bottom. During 20X6 Top and Bottom

reported the following:

Required:

Prepare each of the journal entries listed below related to Top’s investment in Bottom.

1. Top’s acquisition of Bottom.

2. Top’s share of Bottom’s 20X6 income.

3. Top’s share of Bottom’s 20X6 dividend income.

4. Top’s amortization of excess acquisition price.

The following condensed balance sheet is presented for the partnership of Finn, Gary,

and Eugene who share profits and losses in the ratio of 2:4:4, respectively:

Cash $70,000

Other assets 730,000

Finn, loan 20,000

$820,000

Accounts payable $250,000

Eugene, loan 30,000

Finn, Capital 110,000

Gary, Capital 230,000

Eugene, Capital 200,000

$820,000

Assume that the partners decide to liquidate the partnership. If the other assets are sold

for $600,000, how much of the available cash should be distributed to Finn?

A. $64,000

B. $84,000

C. $90,000

D. $110,000

In the LMN partnership, Lynn’s capital is $60,000, Marty’s is $80,000, and Nancy’s is

$70,000. They share income in a 4:3:3 ratio, respectively. Nancy is retiring from the

partnership. Each of the following questions is independent of the others.

Refer to the above information. Nancy is paid $76,000, and all implied goodwill is

recorded. What is the total amount of goodwill recorded?

A. $20,000

B. $14,000

C. $6,000

D. $0

Interim income statements are required for Smith Orchards. Smith does most of its sales

in the fall quarter of the year. These sales are both to individual and commercial

customers. How do you recommend Smith report sales during the spring quarter of the

year?

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Tangible fixed assets not depreciated by a private college or university” describes

which term listed above?

On January 1, 20X5, Seaside Company acquires 90 percent ownership in Rainbow

Corporation for $180,000. The fair value of the noncontrolling interest at that time is

determined to be $20,000. Rainbow reports net assets with a book value of $160,000

and fair value of $175,000. Seaside Company reports net assets with a book value of

$480,000 and a fair value of $525,000 at that time, excluding its investment in

Rainbow. What will be the amount of goodwill that would be reported immediately

after the combination?

A. $5,000

B. $20,000

C. $25,000

D. $40,000

Daniel Corporation, which has a fiscal year ending December 31, had the following

pretax accounting income and estimated effective annual income tax rates for the first

three quarters of the year ended December 31, 20X6:

Estimated Effective Annual

Quarter Pretax Accounting income Income Tax Rate at End of Quarter

Q1 $100,000 36%

Q2 90,000 35%

Q3 110,000 32%

Daniel’s income tax expense in its interim income statement for the third quarter is

A. $29,500

B. $35,200

C. $66,500

D. $96,000

Binary Company acquired 75 percent ownership of Fordham Corporation in 20X5, at

underlying book value. On that date, the fair value of the noncontrolling interest was

equal to 25 percent of the book value of Fordham Corporation. Binary purchased

inventory from Fordham for $150,000 on July 24, 20X6, and resold 90 percent of the

inventory to unaffiliated companies on November 11, 20X6, for $160,000. Fordham

produced the inventory sold to Binary for $120,000. The companies had no other

transactions during 20X6.

Based on the information given above, what amount of consolidated net income will be

assigned to the controlling interest for 20X6?

A. $12,000

B. $25,000

C. $45,250

D. $52,000

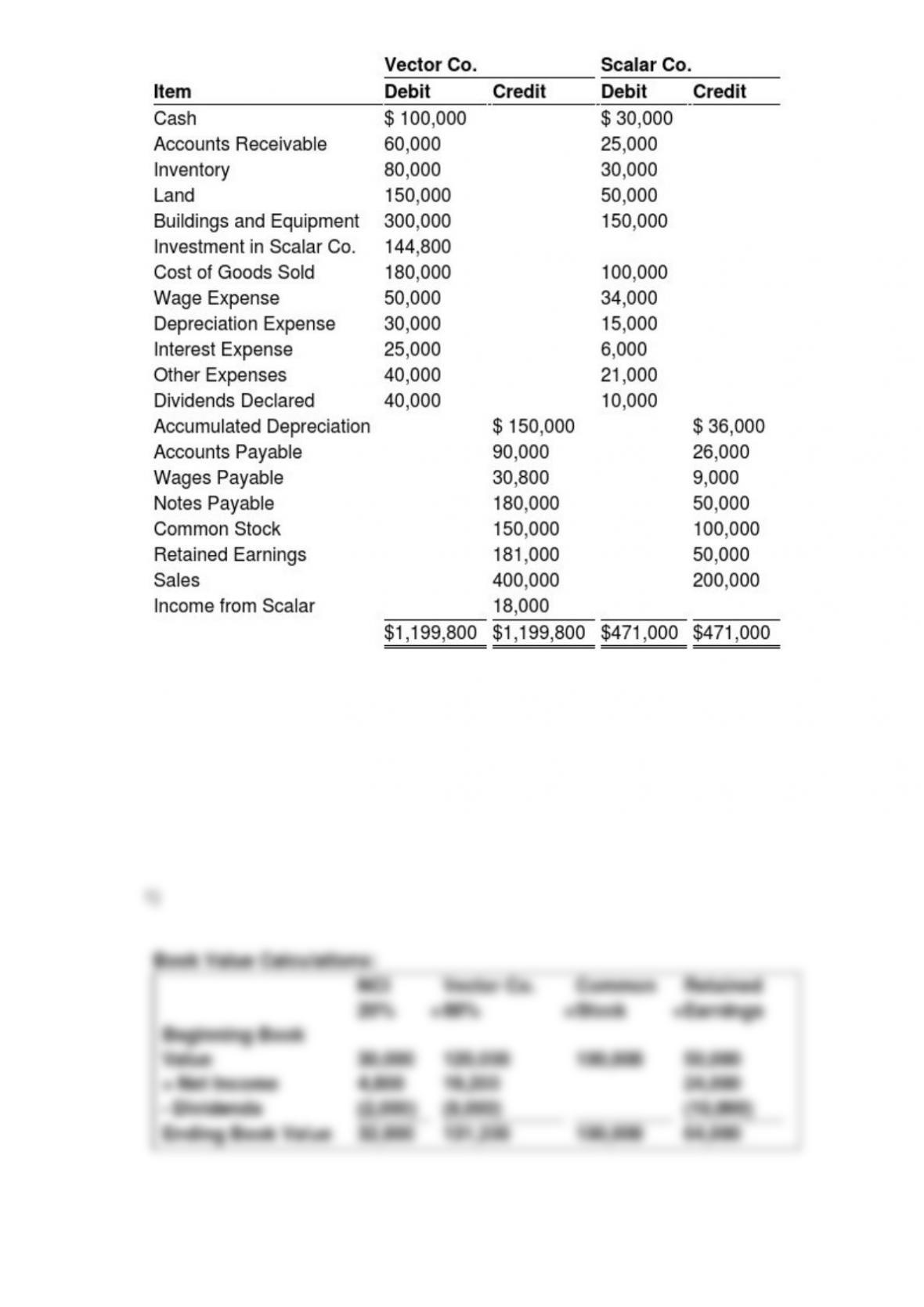

On January 1, 20X8, Vector Company acquired 80 percent of Scalar Company’s

ownership on for $120,000 cash. At that date, the fair value of the noncontrolling

interest was $30,000. The book value of Scalar’s net assets at acquisition was $125,000.

The book values and fair values of Scalar’s assets and liabilities were equal, except for

buildings and equipment, which were worth $15,000 more than book value. Buildings

and equipment are depreciated on a 10-year basis. Although goodwill is not amortized,

the management of Vector concluded at December 31, 20X8, that goodwill from its

acquisition of Scalar shares had been impaired and the correct carrying amount was

$5,000. Goodwill and goodwill impairment were assigned proportionately to the

controlling and noncontrolling shareholders. No additional impairment occurred in

20X9.

Trial balance data for Vector and Scalar on December 31, 20X9, are as follows:

Required:

1) Provide all consolidating entries needed to prepare a three-part consolidation worksheet

as of December 31, 20X9.

2) Prepare a three-part consolidation worksheet for 20X9 in good form.

Alpha Company acquired 100 percent of the voting common shares of Gamma

Corporation by issuing bonds with a par value and fair value of $200,000. Immediately

prior to the acquisition, Alpha reported total assets of $600,000, liabilities of $370,000,

and stockholders’ equity of $230,000. At that date, Gamma reported total assets of

$500,000, liabilities of $300,000, and stockholders’ equity of $200,000. Included in

Gamma’s liabilities was an account payable to Alpha in the amount of $50,000, which

Alpha included in its accounts receivable.

Based on the preceding information, what amount of total liabilities was reported in the

consolidated balance sheet immediately after the acquisition?

A. $370,000

B. $670,000

C. $820,000

D. $870,000

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Erin invests $50,000 for a one-fifth interest in

the total capital of $230,000. The journal entry to record Erin’s admission into the

partnership would include

A. a debit to Jacob, Capital for $2,400.

B. a credit to Erin, Capital for $50,000.

C. a credit to Katy, Capital for $1,600.

D. a credit to Cash for $50,000.