Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

C12-8 Changes in the Cumulative Translation Adjustment Account

a. Foreign transactions.

b. Johnson & Johnson Company applies the concepts presented in the chapter

1. The foreign subsidiaries could be increasing their local liabilities, i.e.,

2. The foreign subsidiaries could be decreasing their local assets, i.e.,

3. The direct exchange rate of the dollar versus the local currency units

of the countries in which the company has foreign subsidiaries has

been decreasing over time (i.e., the dollar had strengthened versus

the local currency units).

d. This footnote demonstrates these factors. Remember that it is assumed that

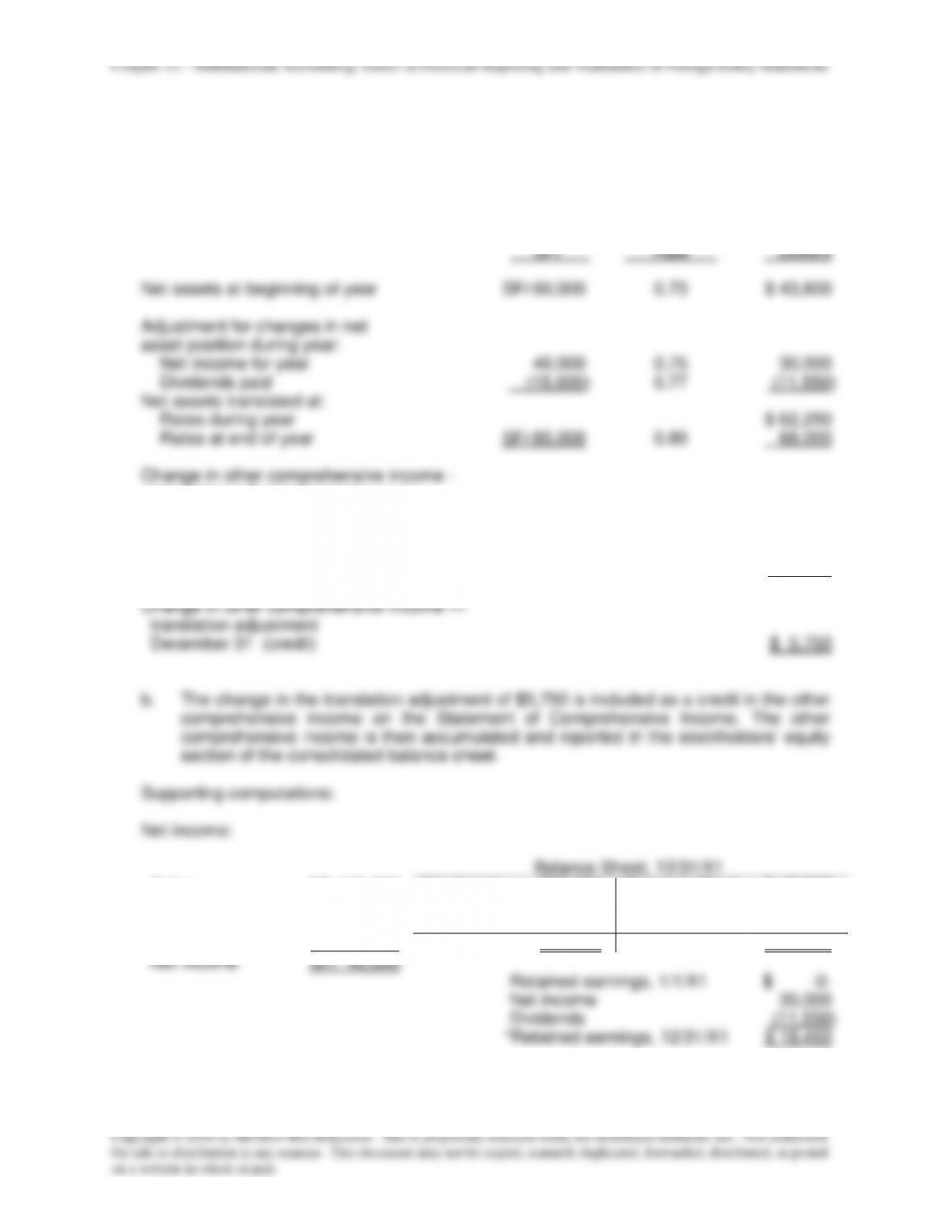

20X1 Translated Balance Sheets of All Foreign Subsidiaries

Net assets

$634

Stockholders’ equity:

Other than AOCI

AOCI Translation

Adjustment

$ 500

134

20X2 Translated Balance Sheets of All Foreign Subsidiaries

Net assets

$354

Stockholders’ equity:

Other than AOCI

AOCI Translation

Adjustment

$ 500

(146)

20X3 Translated Balance Sheets of All Foreign Subsidiaries

Net assets

$162

Stockholders’ equity:

Other than AOCI

AOCI Translation

Adjustment

$ 500

(338)

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

C12-10 Determining an Entity’s Functional Currency

MEMO

To: Garry Parise, CFO, Maxima Corporation

From: _______________ ____________________, CPA, Controller’s Department

Re: Functional Currency of Luz Maxima

According to ASC 830, the functional currency for a company is the primary currency

evaluating the functional currency of Luz Maxima are sales, expense, and financing

indicators.

• Sales market indicators – Luz Maxima now sells a significant amount of product in

Mexico and South America. These transactions are denominated in the peso.

• Expense indicators – Luz Maxima obtains a significant amount of materials from

most appropriate and relevant functional currency for this subsidiary. If a decision is

made to change the functional currency from the U. S. dollar to the Mexican peso, Luz

Maxima’s current financial statements should be converted to U.S. dollars using the

current rate translation method. Any adjustment that occurs as a result of translating

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

nonmonetary assets using the current rate method should be reported as a component

of other comprehensive income.

Authoritative support for the above memo can be found in ASC 830.

C12-11 Accounting for the Translation Adjustment

MEMO

To: Renee Voll, Controller

From: ___________ _______________, CPA

Re: Translation Adjustment for Valencia subsidiary

Since Sonoma has sold 30% of the investment in our Spanish subsidiary, the balance of

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

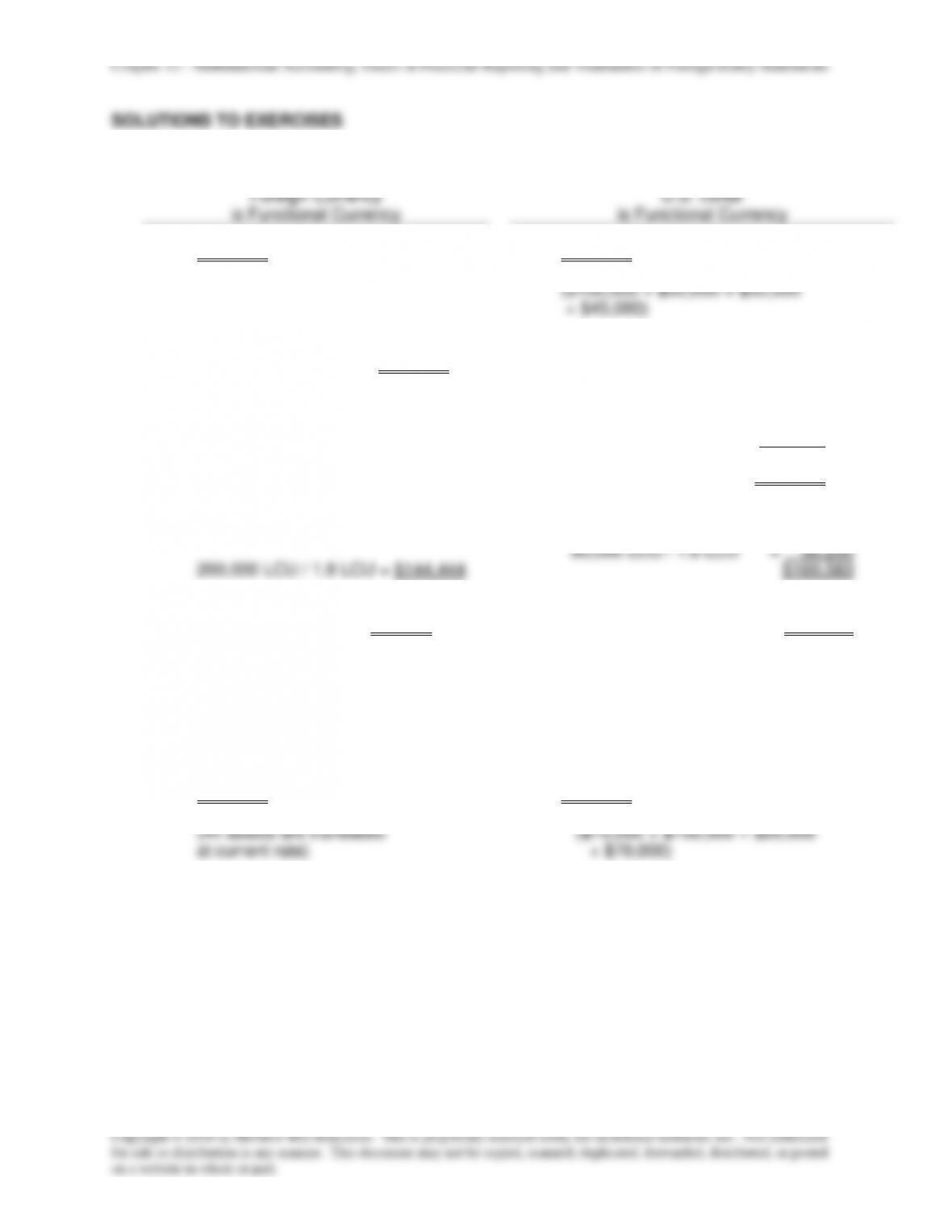

E12-1 Multiple-Choice Translation and Remeasurement [AICPA Adapted]

Foreign Currency

U.S. Dollar

is Functional Currency

is Functional Currency

1.

a –

$215,000

b –

$225,000

($100,000 + $50,000 + $30,000

+ $45,000)

2.

c –

400,000 LCU x $0.44 = $176,000

d –

120,000 LCU x

$0.50

= $ 60,000

80,000 LCU x

$0.44

= 35,200

200,000 LCU x

$0.44

= 88,000

$183,200

3.

a –

Indirect rates used

c –

170,000 LCU / 1.5 LCU

= $113,333

90,000 LCU / 1.6 LCU

=

56,250

260,000 LCU / 1.8 LCU = $144,444

$169,583

4.

d –

25,000 LCU / 2 LCU = $12,500

b –

25,000 LCU / 2.2 LCU

= $

11,364

5.

a

d

6.

a

c

7.

a –

$755,000

c –

$870,000

(All assets are translated

($75,000 + $700,000 + $25,000

at current rate)

+ $70,000)

Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

E12-4 Multiple-Choice Questions on Translation and Remeasurement

1.

b –

Investment cost

$160,000

Less:

Book and fair values of sub’s net assets

680,000 ringitts x $0.21 x 0.90 =

128,520

Goodwill

$ 31,480

2.

c –

Dollars

Ringitts

Goodwill

$10,500

RM 50,000

($10,500 / $.21)

Impairment

1,100

(RM 5,000 x $0.22)

5,000

(RM 50,000 / 10)

3.

a –

Impairment loss = $10,500 / 10 = $1,050

4.

b –

Sub’s Net Income (€25,000 x $1.24)

$31,000

Less:

Goodwill Impairment Loss

(€35,000 x 1.24 x 0.1)

4,340

Income from Sub

$ 26,660

Goodwill of €35,000 calculated as follows:

Amount paid for Common Stock

($402,000 / $1.2)

€335,000

Less: Fair value of identifiable assets

€300,000

Goodwill

€ 35,000

5.

d –

€ 5,000 x $1.30 = $6,500

6.

c –

Investment cost on January 1, 20X5

$402,000

Less:

Book and fair values of sub’s net assets:

€ 300,000 x $1.20

360,000

Goodwill

$ 42,000

Dollars

Euros

Goodwill

$42,000

€ 35,000

($ 42,000 / $1.20)

Impairment

4,340

(€ 3,500 x $1.24)

3,500

(€ 35,000 / 10)

Balance

$37,660

€ 31,500

Translated

balance

$41,580

(€ 31,500 x $1.32)

Translation adjustment: $41,580 minus $37,660 = $3,920 – use for

question 7.

7.

b –

Translation adjustment from

translating the trial balance

$12,000cr

Translation adjustment from

translating goodwill

3,920cr

Total translation adjustment

$15,920cr