Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-31

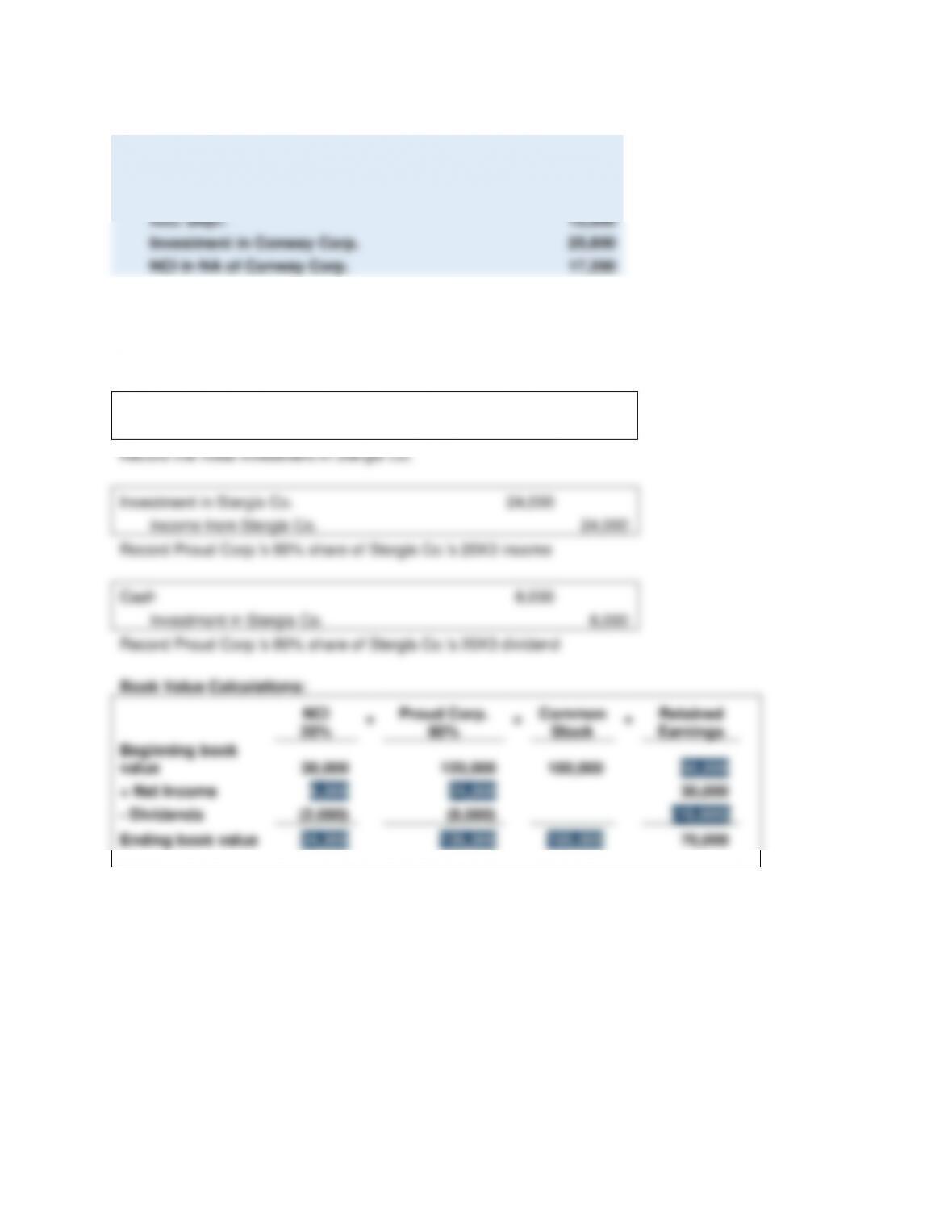

Excess Value (Differential) Reclassification entry:

Land

7,500

Equipment

40,000

Patent

10,500

Acc. Depr.

15,000

Investment in Conway Corp.

25,800

NCI in NA of Conway Corp.

17,200

E5-13 Consolidation Worksheet for Majority-Owned Subsidiary

a.

Equity Method Entries on Proud Corp.’s Books:

Investment in Stergis Co.

120,000

Cash

120,000

Record the initial investment in Stergis Co.

Investment in Stergis Co.

24,000

Income from Stergis Co.

24,000

Record Proud Corp.’s 80% share of Stergis Co.’s 20X3 income

Cash

8,000

Investment in Stergis Co.

8,000

Record Proud Corp.’s 80% share of Stergis Co.’s 20X3 dividend

Book Value Calculations:

NCI

20%

+

Proud Corp.

80%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

30,000

120,000

100,000

50,000

+ Net Income

6,000

24,000

30,000

– Dividends

(2,000)

(8,000)

(10,000)

Ending book value

34,000

136,000

100,000

70,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-13 (continued)

1/1/X3

Goodwill = 0

Identifiable

Excess = 0

$120,000

Initial

investment in

Stergis Co.

80%

Book value =

120,000

12/31/X3

Goodwill = 0

Identifiable

Excess = 0

$136,000

Net

investment in

Stergis Co.

80%

Book value =

136,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-33

E5-13 (continued)

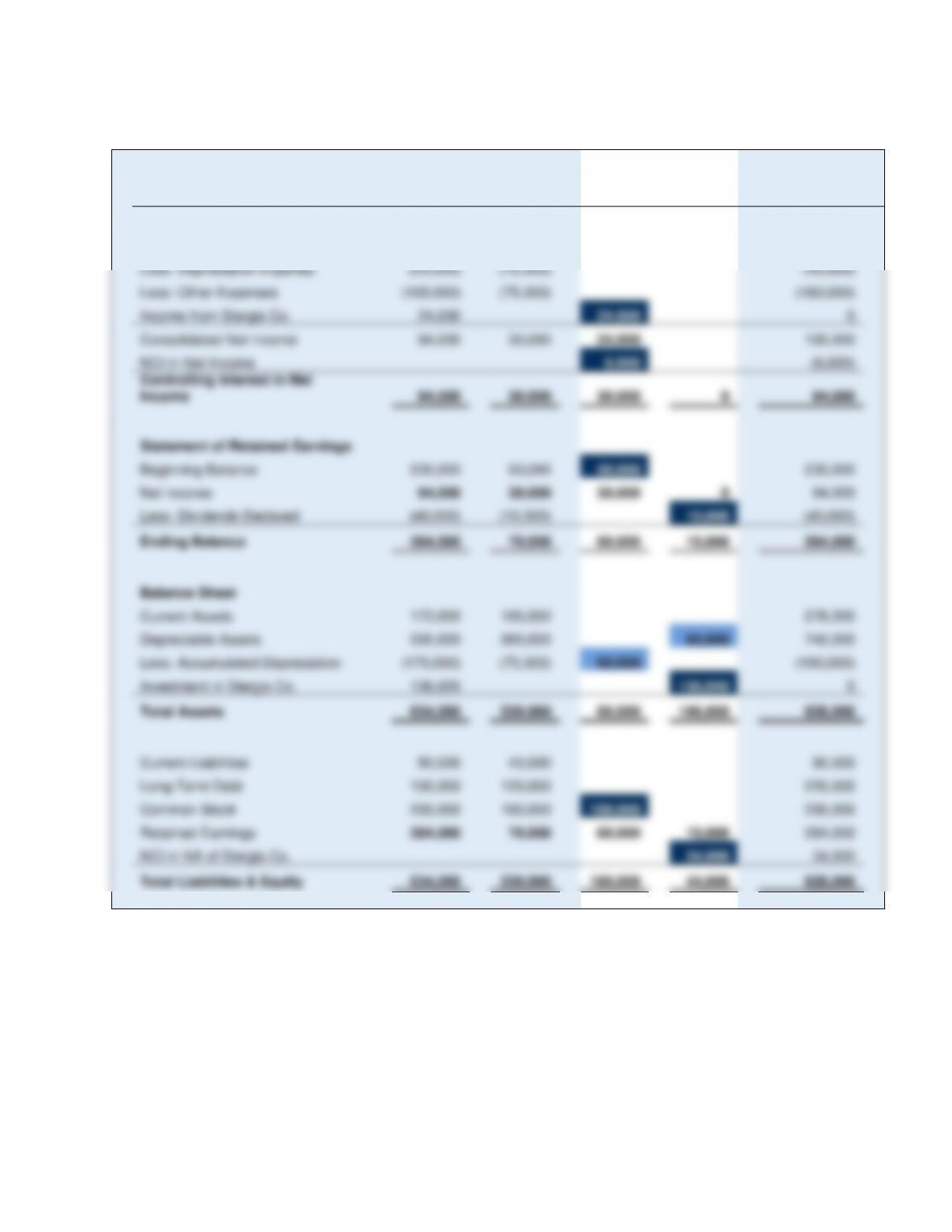

b.

Proud

Corp.

Stergis

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

200,000

120,000

320,000

Less: Depreciation Expense

(25,000)

(15,000)

(40,000)

Less: Other Expenses

(105,000)

(75,000)

(180,000)

Income from Stergis Co.

24,000

24,000

0

Consolidated Net Income

94,000

30,000

24,000

100,000

NCI in Net Income

6,000

(6,000)

Controlling Interest in Net

Income

94,000

30,000

30,000

0

94,000

Statement of Retained Earnings

Beginning Balance

230,000

50,000

50,000

230,000

Net Income

94,000

30,000

30,000

0

94,000

Less: Dividends Declared

(40,000)

(10,000)

10,000

(40,000)

Ending Balance

284,000

70,000

80,000

10,000

284,000

Balance Sheet

Current Assets

173,000

105,000

278,000

Depreciable Assets

500,000

300,000

60,000

740,000

Less: Accumulated Depreciation

(175,000)

(75,000)

60,000

(190,000)

Investment in Stergis Co.

136,000

136,000

0

Total Assets

634,000

330,000

60,000

196,000

828,000

Current Liabilities

50,000

40,000

90,000

Long-Term Debt

100,000

120,000

220,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

284,000

70,000

80,000

10,000

284,000

NCI in NA of Stergis Co.

34,000

34,000

Total Liabilities & Equity

634,000

330,000

180,000

44,000

828,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-34

E5-13 (continued)

c.

Proud Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X3

Current Assets

$278,000

Depreciable Assets

$740,000

Less: Accumulated Depreciation

(190,000)

550,000

Total Assets

$828,000

Current Liabilities

$

90,000

Long-Term Debt

220,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$200,000

Retained Earnings

284,000

Total Controlling Interest

$484,000

Noncontrolling Interest

34,000

Total Stockholders’ Equity

518,000

Total Liabilities and Stockholders’ Equity

$828,000

Proud Corporation and Subsidiary

Consolidated Income Statement

Year Ended December 31, 20X3

Sales

$320,000

Depreciation

$ 40,000

Other Expenses

180,000

Total Expenses

(220,000)

Consolidated Net Income

$100,000

Income to Noncontrolling Interest

(6,000)

Income to Controlling Interest

$ 94,000

Proud Corporation and Subsidiary

Consolidated Retained Earnings Statement

Year Ended December 31, 20X3

Retained Earnings, January 1, 20X3

$230,000

Income to Controlling Interest, 20X3

94,000

$324,000

Dividends Declared, 20X3

(40,000)

Retained Earnings, December 31, 20X3

$284,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-14 Consolidation Worksheet for Majority-Owned Subsidiary for Second Year

a.

Equity Method Entries on Proud Corp.’s Books:

Investment in Stergis Co.

28,000

Income from Stergis Co.

28,000

Record Proud Corp.’s 80% share of Stergis Co.’s 20X4 income

Cash

12,000

Investment in Stergis Co.

12,000

Record Proud Corp.’s 80% share of Stergis Co.’s 20X4 dividend

Book Value Calculations:

NCI

20%

+

Proud Corp.

80%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

34,000

136,000

100,000

70,000

+ Net Income

7,000

28,000

35,000

– Dividends

(3,000)

(12,000)

(15,000)

Ending book value

38,000

152,000

100,000

90,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-36

E5-14 (continued)

Basic Consolidation Entry

Common Stock

100,000

Retained Earnings

70,000

Income from Stergis Co.

28,000

NCI in NI of Stergis Co.

7,000

Dividends Declared

15,000

Investment in Stergis Co.

152,000

NCI in NA of Stergis Co.

38,000

Investment in

Income from

Stergis Co.

Stergis Co.

Beginning Balance

136,000

80% Net Income

28,000

28,000

80% Net Income

12,000

80% Dividends

Ending Balance

152,000

28,000

Ending Balance

152,000

Basic

28,000

0

0

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

60,000

Depreciable Assets

60,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-37

E5-14 (continued)

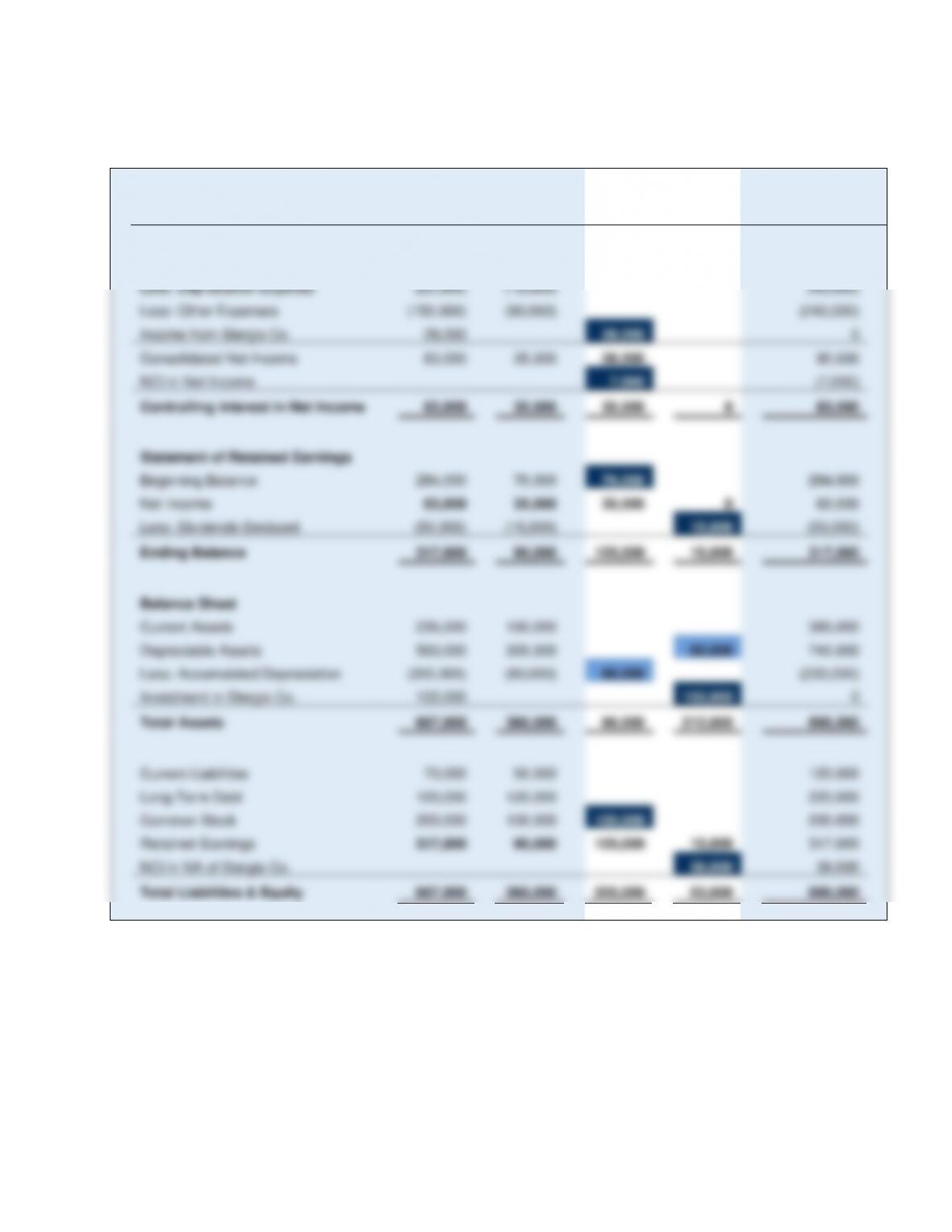

b.

Proud

Corp.

Stergis

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

230,000

140,000

370,000

Less: Depreciation Expense

(25,000)

(15,000)

(40,000)

Less: Other Expenses

(150,000)

(90,000)

(240,000)

Income from Stergis Co.

28,000

28,000

0

Consolidated Net Income

83,000

35,000

28,000

90,000

NCI in Net Income

7,000

(7,000)

Controlling Interest in Net Income

83,000

35,000

35,000

0

83,000

Statement of Retained Earnings

Beginning Balance

284,000

70,000

70,000

284,000

Net Income

83,000

35,000

35,000

0

83,000

Less: Dividends Declared

(50,000)

(15,000)

15,000

(50,000)

Ending Balance

317,000

90,000

105,000

15,000

317,000

Balance Sheet

Current Assets

235,000

150,000

385,000

Depreciable Assets

500,000

300,000

60,000

740,000

Less: Accumulated Depreciation

(200,000)

(90,000)

60,000

(230,000)

Investment in Stergis Co.

152,000

152,000

0

Total Assets

687,000

360,000

60,000

212,000

895,000

Current Liabilities

70,000

50,000

120,000

Long-Term Debt

100,000

120,000

220,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

317,000

90,000

105,000

15,000

317,000

NCI in NA of Stergis Co.

38,000

38,000

Total Liabilities & Equity

687,000

360,000

205,000

53,000

895,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-38

E5-15 Preparation of Stockholders‘ Equity Section with Other Comprehensive Income

a.

Consolidated net income:

20X8

20X9

Operating income of Broadmore

$120,000

$ 140,000

Net income of Stem

40,000

60,000

Amortization of differential ($580,000 – $500,000) / 10

Years

(8,000)

(8,000)

Consolidated net income

$152,000

$ 192,000

Comprehensive gain reported by Stem

10,000

5,000

Consolidated comprehensive income

$162,000

$ 197,000

b.

Comprehensive income attributable to controlling interest:

20X8

20X9

Consolidated comprehensive income

$162,000

$ 197,000

Comprehensive income attributable to

Noncontrolling interest

($50,000 – $8,000) x .25

(10,500)

($65,000 – $8,000) x .25

(14,250)

Comprehensive income attributable to controlling interest

$151,500

$ 182,750

c.

Consolidated stockholders’ equity:

20X8

20X9

Controlling Interest:

Common Stock

$320,000

$ 320,000

Retained Earnings*

504,000

613,000

Accumulated Other Comprehensive Income#

7,500

11,250

Total Controlling Interest

831,500

944,250

Noncontrolling Interest

151,750

158,500

Total Stockholders’ Equity

$983,250

$1,102,750

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-16 Consolidation entries for Subsidiary with Other Comprehensive Income

a.

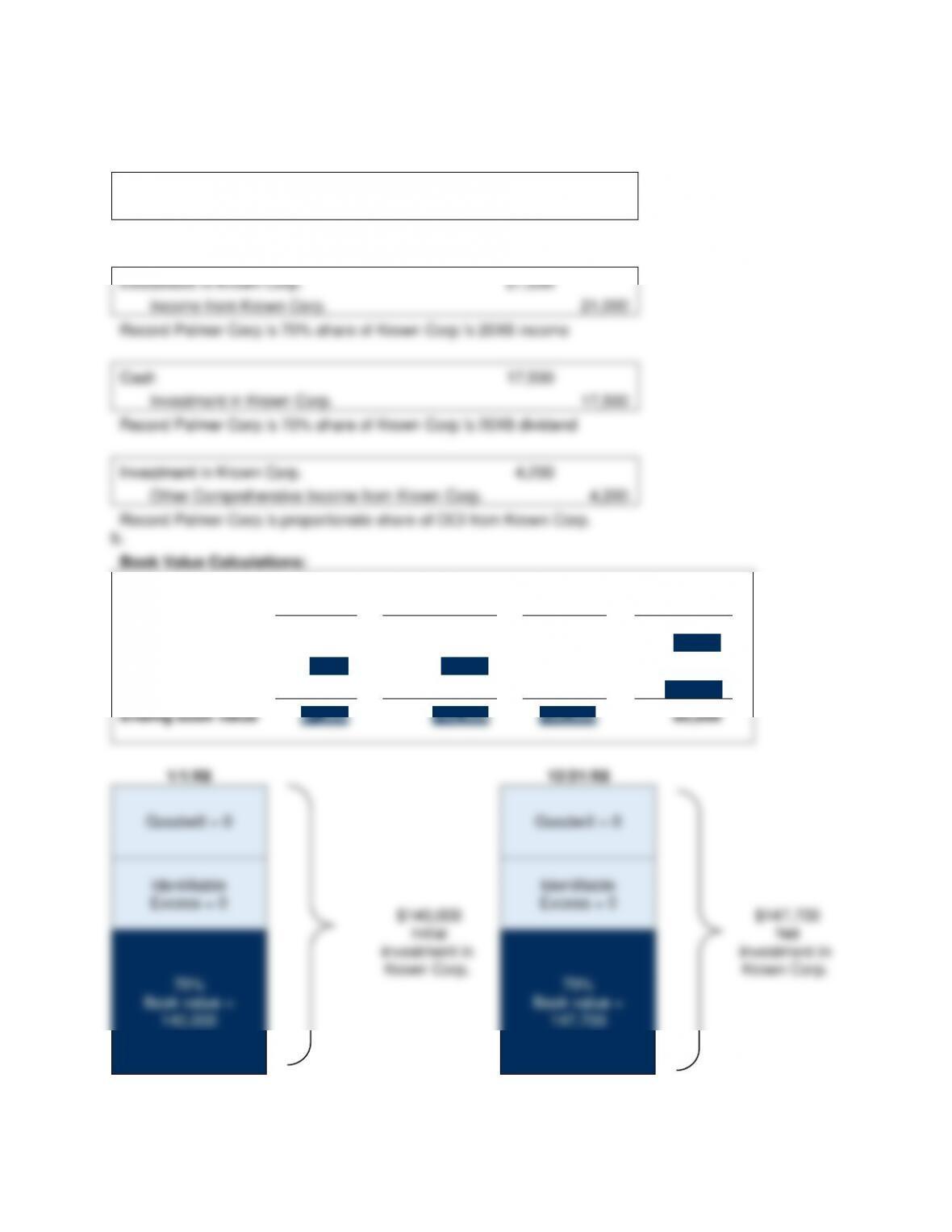

Equity Method Entries on Palmer Corp.’s Books:

Investment in Krown Corp.

140,000

Cash

140,000

Record the initial investment in Krown Corp.

Investment in Krown Corp.

21,000

Income from Krown Corp.

21,000

Record Palmer Corp.’s 70% share of Krown Corp.’s 20X8 income

Cash

17,500

Investment in Krown Corp.

17,500

Record Palmer Corp.’s 70% share of Krown Corp.’s 20X8 dividend

Investment in Krown Corp.

4,200

Other Comprehensive Income from Krown Corp.

4,200

Record Palmer Corp.’s proportionate share of OCI from Krown Corp.

Book Value Calculations:

NCI

30%

+

Palmer Corp.

70%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

60,000

140,000

120,000

80,000

+ Net Income

9,000

21,000

30,000

– Dividends

(7,500)

(17,500)

(25,000)

Ending book value

61,500

143,500

120,000

85,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-40

E5-16 (continued)

Basic Consolidation Entry

Common Stock

120,000

Retained Earnings

80,000

Income from Krown Corp.

21,000

NCI in NI of Krown Corp.

9,000

Dividends Declared

25,000

Investment in Krown Corp.

143,500

NCI in NA of Krown Corp.

61,500

Other Comprehensive Income Entry:

OCI from Krown Corp.

4,200

OCI to the NCI

1,800

Investment in Krown Corp.

4,200

NCI in NA of Krown Corp.

1,800

Investment in

Income from

Krown Corp.

Krown Corp.

Acquisition Price

140,000

70% Net Income

21,000

21,000

17,500

70% Dividends

4,200

70% OCI

Ending Balance

147,700

21,000

143,500

Basic

21,000

4,200

OCI Entry

0

0