Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Janet Corporation holds 75 percent of Slider Corporation's voting common stock,

acquired at book value. The fair value of the noncontrolling interest at the date of

acquisition was equal to 25 percent of the book value of Slider Corporation. On

December 31, 20X8, Slider Corporation acquired 25 percent of Janet Corporation's

stock. Slider records dividends received from Janet as nonoperating income. In 20X9,

Janet reported operating income of $100,000 and paid dividends of $40,000. During the

same year, Slider reported operating income of $75,000 and paid $20,000 in dividends.

Based on the information provided, what amount will be reported as income assigned to

the controlling interest for 20X9 under the treasury stock method?

A. $18,750

B. $156,250

C. $175,000

D. $100,000

The personal financial statements of a partner include which of the following?

I. Statement of financial condition.

II. Statement of changes in net worth.

III. Statement of cash flows.

A. I and II

B. I and III

C. II and III

D. I, II, and III

Akron established an internal service fund for its data processing activities on July 1,

20X8. During the fiscal year ended June 30, 20X9, the following transactions and

events occurred:

1) On July 1, 20X8, the city council authorized the general fund to contribute

$1,000,000 to help establish the internal service fund on July 20, 20X8.

2) The internal service fund spent $900,000 of the contribution to acquire a mainframe

computer on July 25, 20X8.

3) During the year ended June 30, 20X9, the internal service billed other funds of the

city $300,000 for use of the computer. By year end, all of the billings were collected

except for $30,000.

4) The internal service fund incurred general operating expenses of $100,000, exclusive

of depreciation, during the year ended June 30, 20X9. All of the expenses were paid by

June 30, 20X9, except for $24,000.

5) Depreciation expense related to the computer was $180,000.

Required:

A) Prepare all journal entries that would be recorded by Akron's internal service fund

for the year ended June 30, 20X9. Explanations for journal entries are not necessary.

B) Prepare a statement of revenues, expenses, and changes in fund net assets for the

internal service fund for the year ended June 30, 20X9.

C) Calculate the amount of unrestricted net assets at June 30, 20X9.

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $0

B. $5,000

C. $25,000

D. $30,000

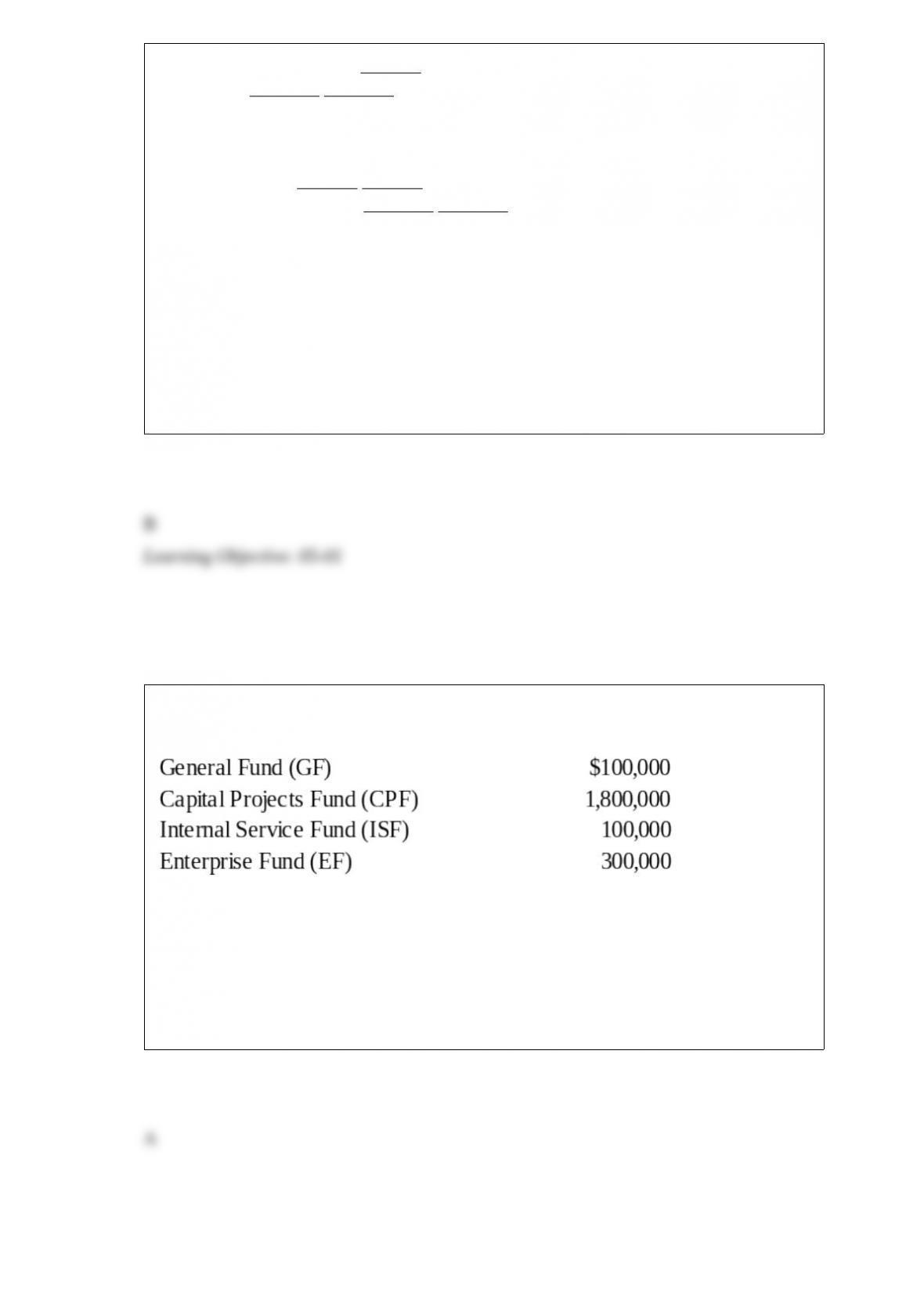

At June 30, 20X9, total assets for the various funds of a local municipality were as

follows:

Applying GASB 34 criteria, which of the above are major funds for reporting

purposes?

A. GF, CPF, EF

B. CPF, EF

C. CPF, ISF, EF

D. GF, CPF, ISF, EF

West, Inc. holds 100 percent of the common stock of Coast Company, an investment

acquired for $680,000. Immediately following the combination, West's net assets have a

book value of $1,150,000 and a fair value of $1,390,000. The book value and the fair

value of Coast's net assets on the date of combination are $400,000 and $550,000,

respectively. Immediately following the combination, a consolidated balance sheet is

prepared.

Based on the information given above, what will be the amount of net assets reported in

the consolidated balance sheet, prepared immediately following the combination?

A. $1,150,000

B. $1,550,000

C. $1,700,000

D. $1,830,000

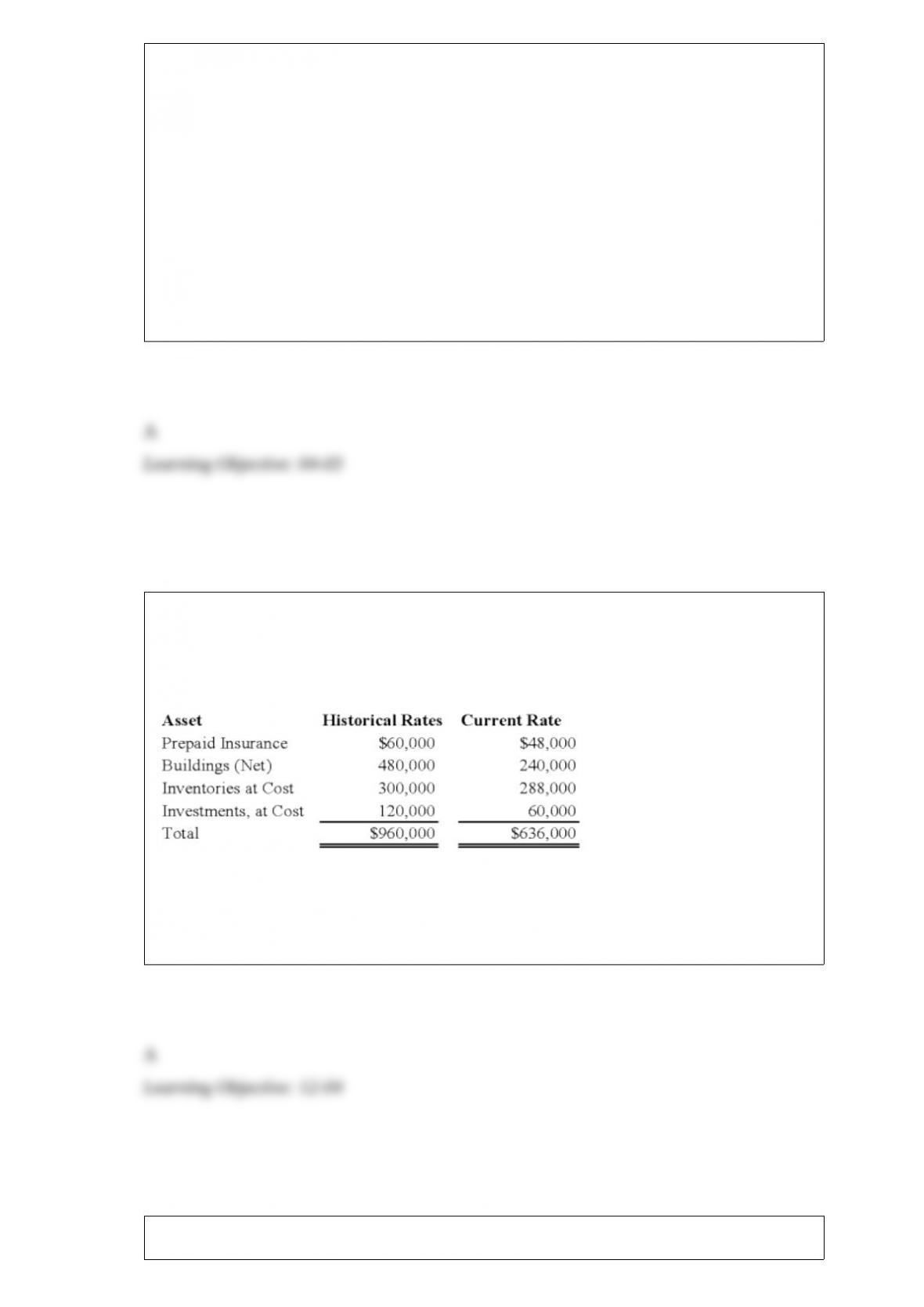

The assets listed below of a foreign subsidiary have been converted to U.S. dollars at

both current and historical exchange rates. Assuming that the local currency of the

foreign subsidiary is the functional currency, what total amount should appear for these

assets on the U.S. company's consolidated balance sheet?

A. $636,000

B. $648,000

C. $708,000

D. $960,000

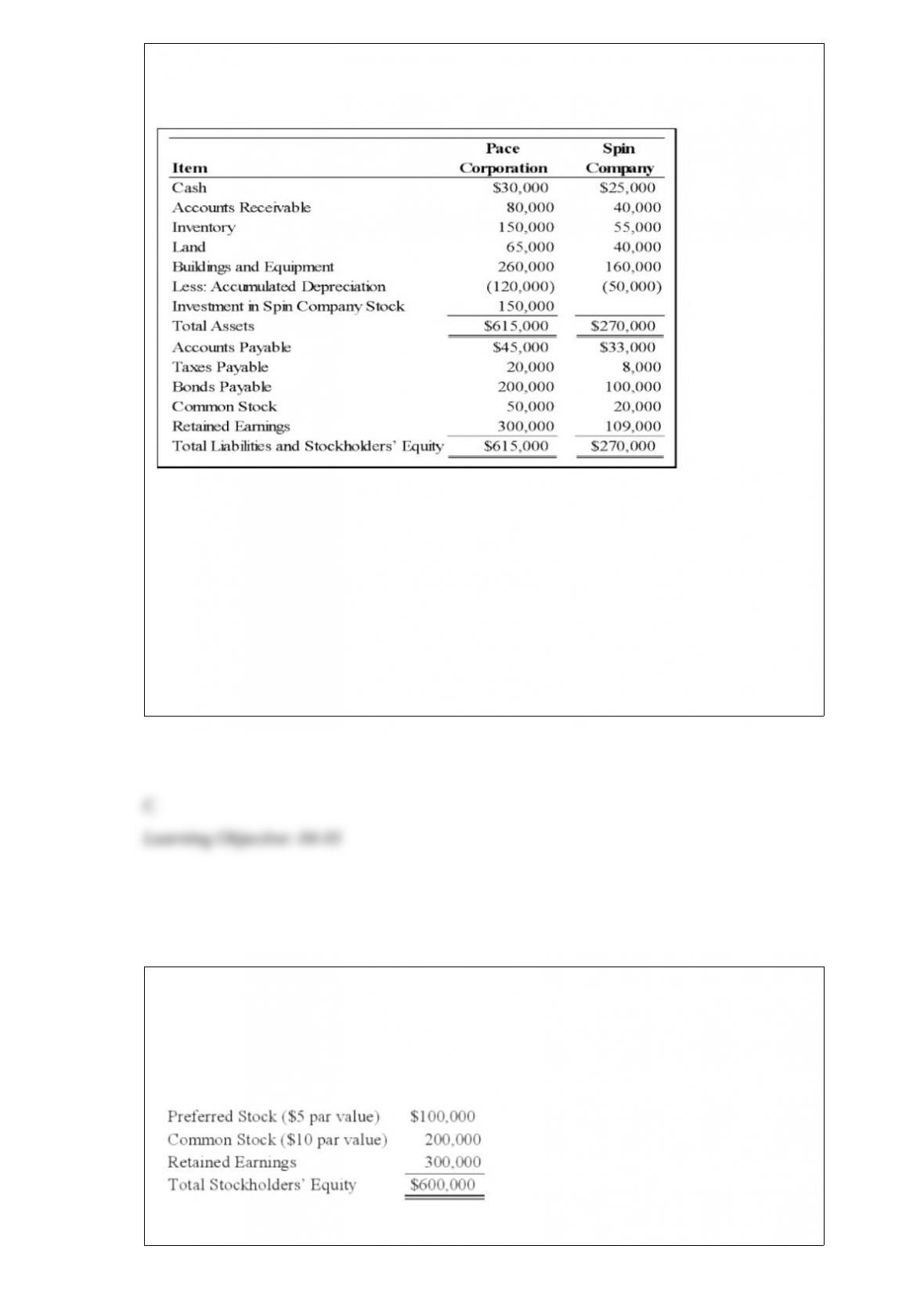

Pace Corporation acquired 100 percent of Spin Company's common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin's net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $0

B. $21,000

C. $6,000

D. $15,000

On January 1, 20X9, Company A acquired 80 percent of the common stock and 60

percent of the preferred stock of Company B, for $400,000 and $60,000, respectively.

At the time of acquisition, the fair value of the common shares of Company B held by

the noncontrolling interest was $100,000. Company B's balance sheet contained the

following balances:

For the year ended December 31, 20X9, Company B reported net income of $100,000

and paid dividends of $40,000. The preferred stock is cumulative and pays an annual

dividend of 10 percent.

Based on the preceding information, what will be the equity method income reported by

Company A from its investment in Company B during 20X9?

A. $32,000

B. $30,000

C. $72,000

D. $48,000

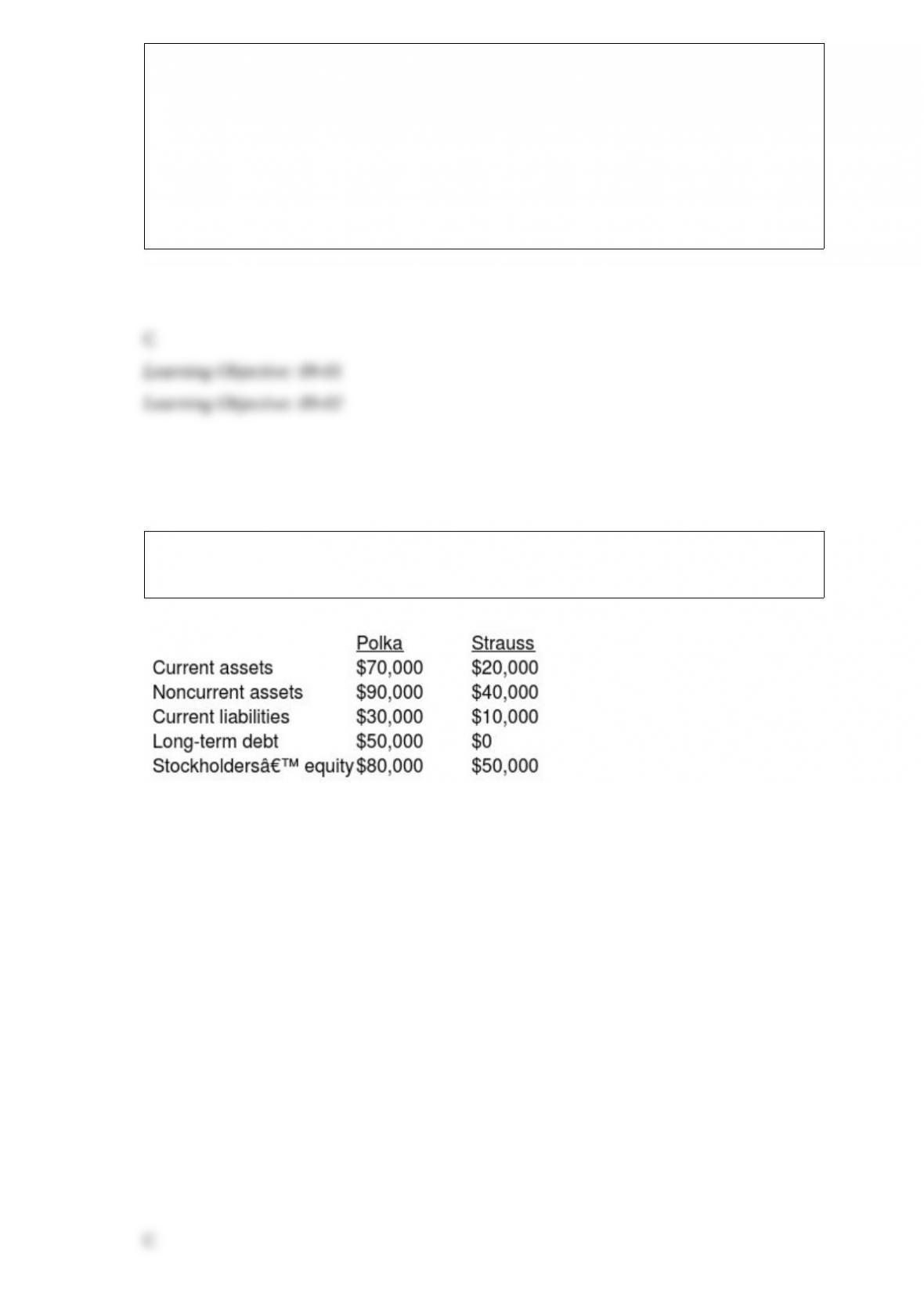

On January 1, 20X6, Polka Co. (Polka) and Strauss Co. (Strauss) had condensed

balance sheets as follows:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the

outstanding common shares of Strauss. This debt is payable in ten equal annual principal

and accrued interest payments beginning December 30, 20X6. On the acquisition date, the

fair value of Strauss was $100,000, and the excess cost of the investment over Strauss’s

carrying amount of acquired net assets should be allocated 60% to inventory and 40% to

goodwill.

Stockholders’ equity on the January 2, 20X6, consolidated balance sheet should be:

A. $85,000

B. $80,000

C. $90,000

D. $130,000

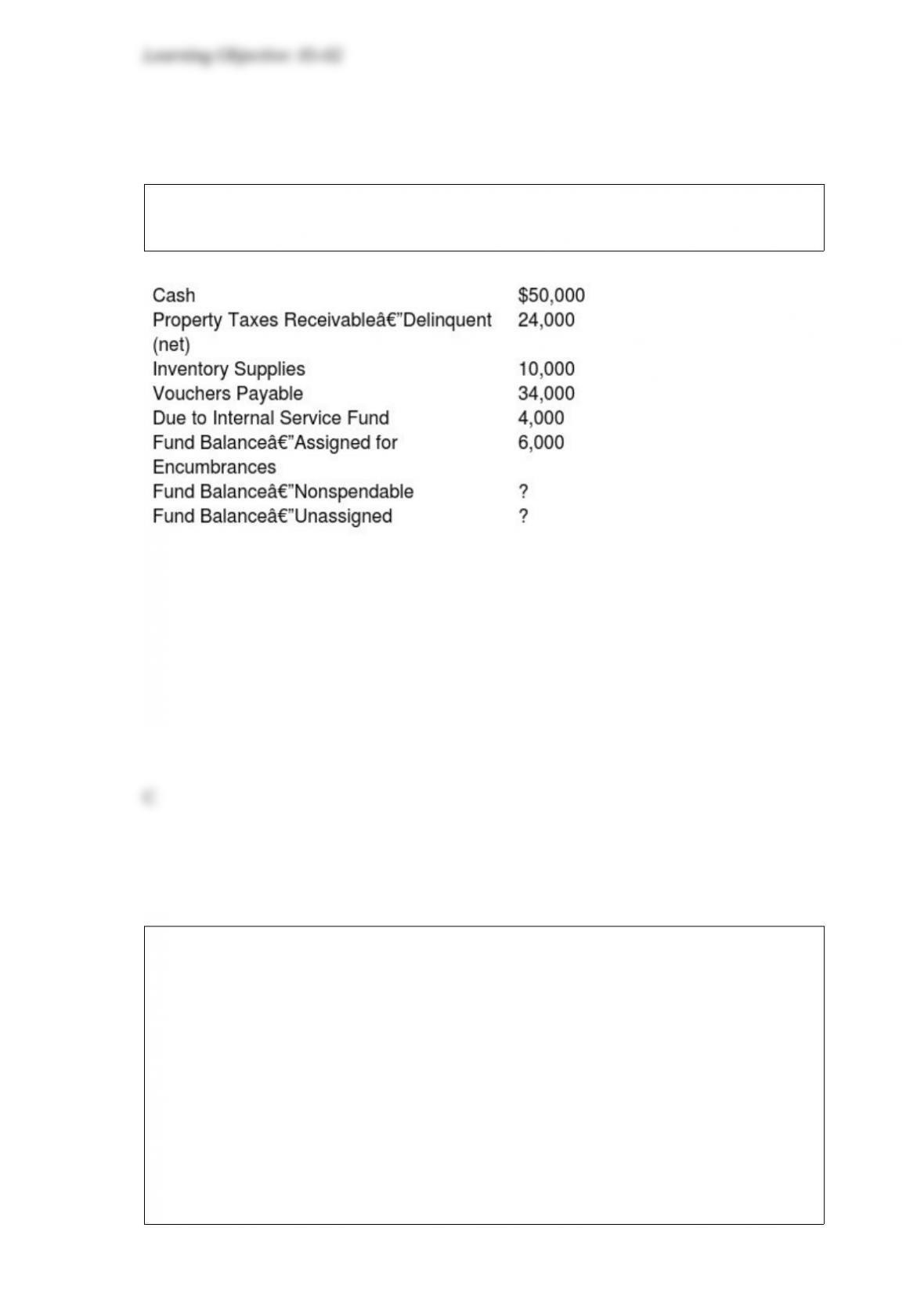

The Town of Baker reported the following items on the June 30, 20X9, balance sheet of

its general fund:

At June 30, 20X9, what amount should be reported for Fund Balance—Unassigned?

A. $46,000

B. $40,000

C. $30,000

D. $16,000

At its inception, Peacock Company purchased land for $50,000 and a building for

$220,000. After exactly 4 years, it transferred these assets and cash of $75,000 to a

newly created subsidiary, Selvick Company, in exchange for 25,000 shares of Selvick’s

$5 par value stock. Peacock uses straight-line depreciation. When purchased, the

building had a useful life of 20 years with no expected salvage value. An appraisal at

the time of the transfer revealed that the building has a fair value of $250,000.

Based on the information provided, what amount would be reported by Peacock

Company as investment in Selvick Company common stock?

A. $125,000

B. $250,000

C. $301,000

D. $345,000

A business combination in which the acquired company’s assets and liabilities are

combined with those of the acquiring company into a single entity is defined as:

A. Stock acquisition

B. Leveraged buyout

C. Statutory Merger

D. Reverse statutory rollup

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, what amount of total stockholders’ equity will be

reported in the consolidated balance sheet prepared immediately after the business

combination?

A. $213,000

B. $350,000

C. $425,000

D. $638,000

Which of the following observations concerning interfund transfers is true?

A. They are expected to be repaid.

B. They are classified as fund revenues or expenditures.

C. The receiving fund recognizes these transfers as revenue.

D. These transfers are classified under “Other Financing Sources or Uses.”

According to ASC 958, Not-For-Profit entities should recognize

depreciation/amortization:

I. on all long-lived tangible assets.

II. on all long-lived intangible assets.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

What account should be debited in the debt service fund to recognize an installment

payment currently due on general obligation serial bonds?

I. Matured Bonds Payable.

II. Expenditures-Principal.

A. I

B. II

C. Either I or II

D. Neither I nor II

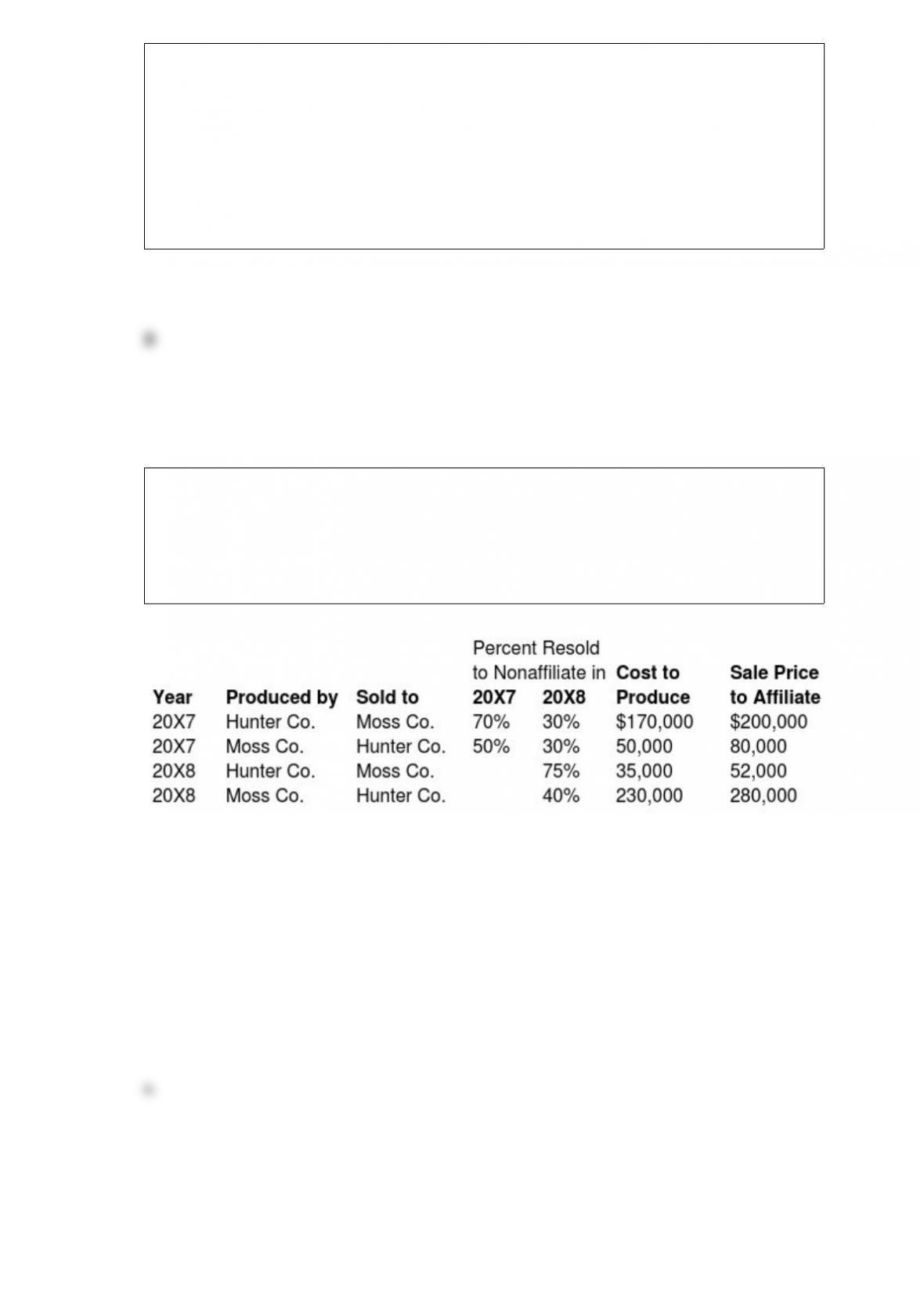

Hunter Company and Moss Company both produce and purchase fabric for resale each

period and frequently sell to each other. Since Hunter Company holds 80 percent

ownership of Moss Company, Hunter's controller compiled the following information

with regard to intercompany transactions between the two companies in 20X7 and

20X8:

Required:

a. Give the consolidating entries required at December 31, 20X8, to eliminate the effects of

the inventory transfers in preparing a full set of consolidated financial statements.

b. Compute the amount of cost of goods sold to be reported in the consolidated income

statement for 20X8.

Neptune Corporation owns 70 percent of Pluto Company’s stock. On July 1, 20X4,

Neptune sold a piece of equipment to Pluto for $56,350. Neptune had purchased this

equipment on January 1, 20X1, for $63,000. The equipment’s original 15-year

estimated total economic life remains unchanged. Both companies use straight-line

depreciation. The equipment’s residual value is considered negligible.

Based on the information provided, in the preparation of the 20X4 consolidated

financial statements, equipment will be ______ in the consolidation entries.

A. debited for $6,650

B. debited for $56,350

C. debited for $63,000

D. credited for $63,000

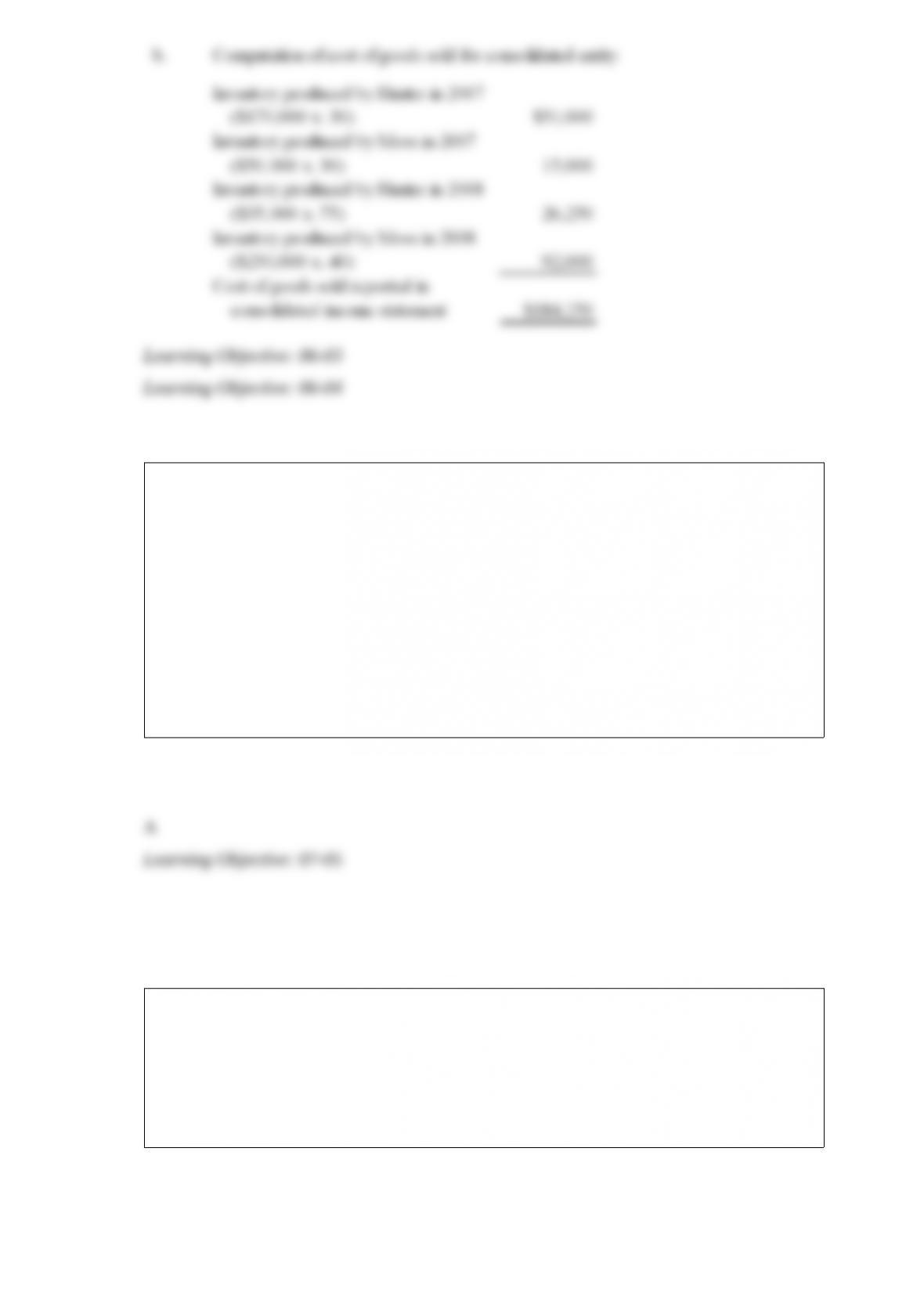

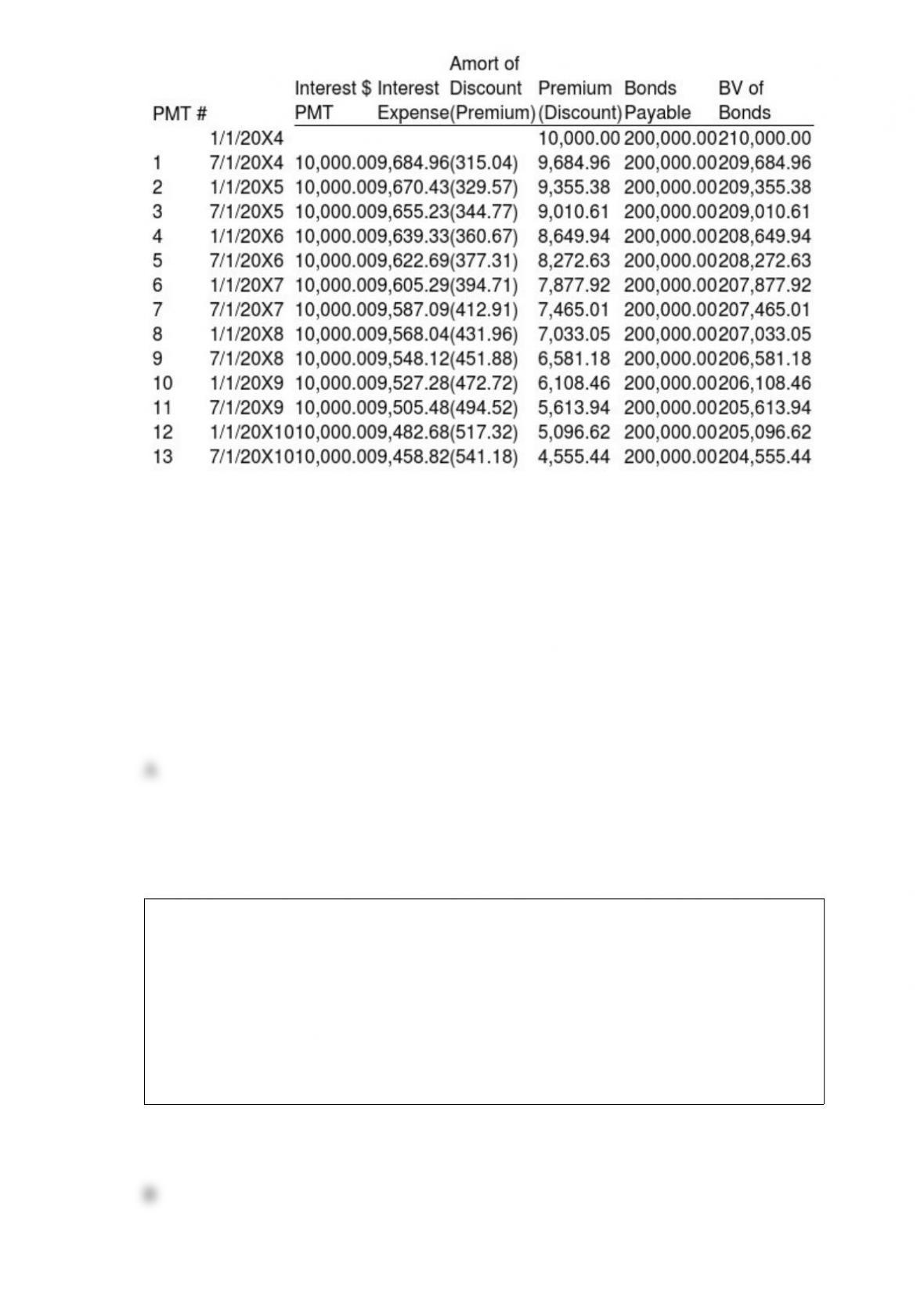

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite's bonds from the

original purchaser on January 1, 20X8, for $122,000. Mortar owns 75 percent of

Granite's voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of premium on bonds payable will be

eliminated in the preparation of the 20X8 year-end consolidated financial statements?

A. $4,276

B. $4,923

C. $6,108

D. $7,033

What account is debited in a debt service fund when it records matured interest

payable?

I. Interest Expense

II. Expenditures

A. I only

B. II only

C. Either I or II

D. Neither I nor II

The restricted funds of a not-for-profit hospital are often termed “______” funds

because they must hold the restricted assets and transfer expendable resources to the

general fund for expenditure.

A. specific

B. controlled

C. limited

D. holding

During the fiscal year ended June 30, 20X3, an enterprise fund of New Spring acquired

computer equipment costing $280,000 on account and issued $600,000 of long-term

bonds at par value. Revenues of the enterprise fund will be used to repay bond interest

and principal. What effect did these transactions have on New Spring's enterprise fund

assets and long-term debt?

Assets Long-Term Debt

A. Increase of $880,000 Increase of $600,000

B. Increase of $280,000 Increase of $600,000

C. Increase of $880,000 No effect

D. Increase of $600,000 Increase of $600,000

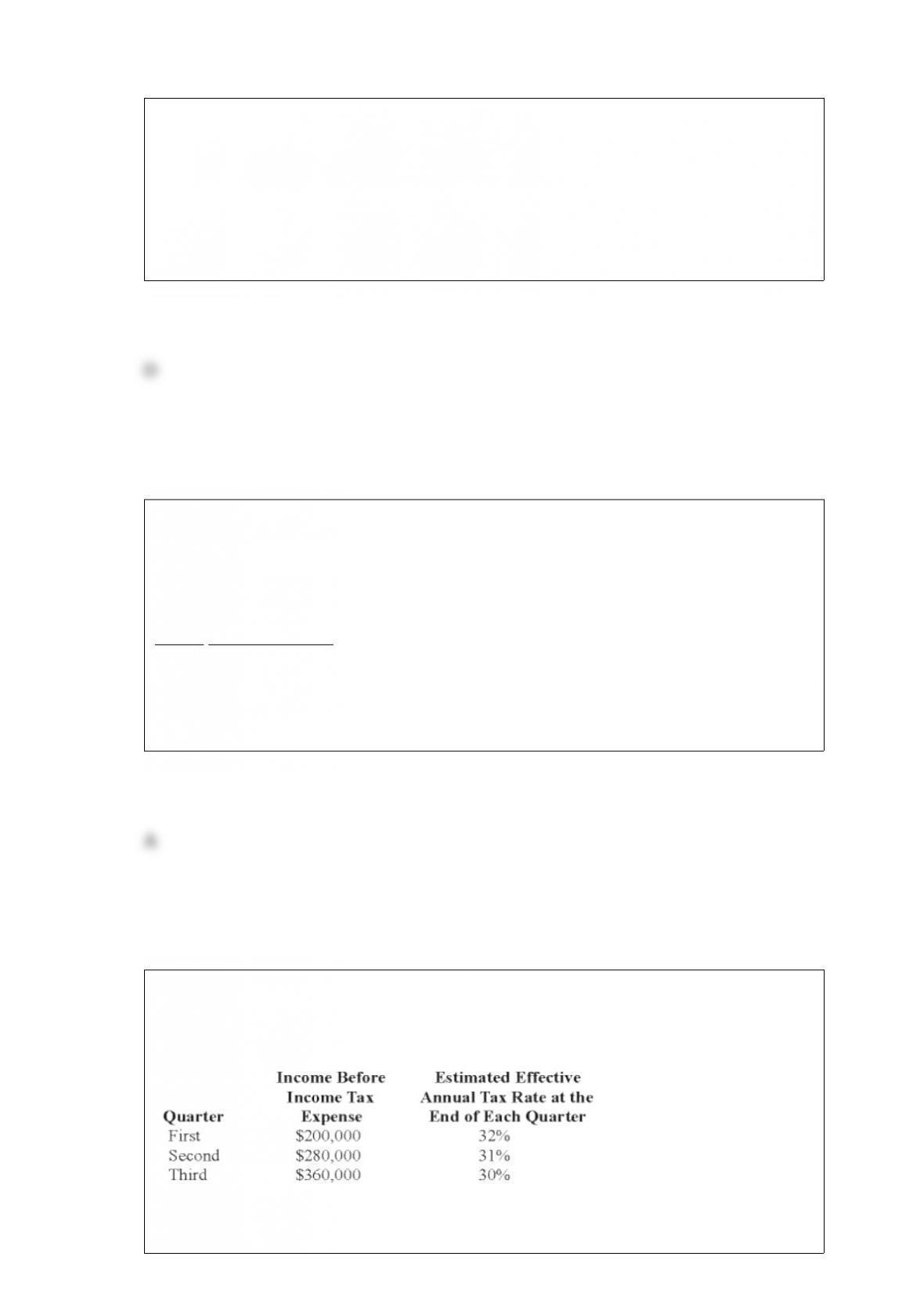

Toledo Imports, a calendar-year corporation, had the following income before tax

expense and estimated effective annual income tax rates for the first three quarters in

20X8:

Toledo's income tax expense in its interim income statement for the nine months ended

September 30 and for the third quarter, respectively, are:

A. $250,800 and $103,200.

B. $252,000 and $108,000.

C. $252,000 and $103,200.

D. $250,800 and $108,000.

For the year ended June 30, 20X9, a private college received contributions from alumni

which were restricted for faculty research stipends to be awarded during the next fiscal

year. For the year ended June 30, 20X9, these contributions should be disclosed on the

statement of activities of the private college as an increase in:

A. the fund balance of the restricted current fund.

B. temporarily restricted net assets.

C. deferred revenues.

D. temporarily restricted fund balance.

On July 25, 20X8, the city of Pullman, which reports on a calendar-year basis, ordered

five police cars at an estimated cost of $200,000. On August 26, 20X8, the police cars

were received, and the actual cost amounted to $197,000. Pullman encumbered the

appropriation for police cars in its general fund when the cars were ordered. When the

police cars were received, the general fund of Pullman should:

A. Credit Budgetary Fund Balance Assigned for Encumbrances for $197,000.

B. Debit Encumbrances for $200,000.

C. Debit Expenditures for $197,000.

D. Credit Budgetary Fund Balance Assigned for Expenditures for $200,000.

Blue Corporation holds 70 percent of Black Company's voting common stock. On

January 1, 20X3, Black paid $500,000 to acquire a building with a 10-year expected

economic life. Black uses straight-line depreciation for all depreciable assets. On

December 31, 20X8, Blue purchased the building from Black for $180,000. Blue

reported income, excluding investment income from Black, of $140,000 and $162,000

for 20X8 and 20X9, respectively. Black reported net income of $30,000 and $45,000

for 20X8 and 20X9, respectively.

Based on the preceding information, the amount to be reported as consolidated net

income for 20X8 will be:

A. $190,000.

B. $170,000.

C. $175,000.

D. $150,000.

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital's statement

of operations for the year ended December 31, 20X8.

Transaction: Received cash contribution from donor who stipulated the contribution be

permanently invested.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

On December 31, 20X5, Paris Corporation acquired 60 percent of Sanlo Company’s

common stock for $180,000. At that date, the fair value of the noncontrolling interest

was $120,000. Of the $45,000 differential, $5,000 related to the increased value of

Sanlo’s inventory, $15,000 related to the increased value of its land, and $10,000 related

to the increased value of its equipment that had a remaining life of five years from the

date of combination. Sanlo sold all inventory it held at the end of 20X5 during 20X6.

The land to which the differential related was also sold during 20X6 for a large gain. In

20X6, Sanlo reported net income of $40,000 but paid no dividends. Paris accounts for

its investment in Sanlo using the equity method.

Based on the preceding information, what amount of differential would Paris amortize

during 20X6 in its equity method journal entries?

A. $13,200

B. $15,000

C. $22,000

D. $30,000

ABC Corporation purchased land on January 1, 20X6, for $50,000. On July 15, 20X8,

it sold the land to its subsidiary, XYZ Corporation, for $70,000. ABC owns 80 percent

of XYZ's voting shares.

Based on the preceding information, what will be the worksheet consolidating entry to

remove the effects of the intercompany sale of land in preparing the consolidated

financial statements for 20X9?

A. Option A

B. Option B

C. Option C

D. Option D