A not-for-profit private college in Virginia created a separate foundation responsible for

obtaining financial support from alumni and others. Foundation assets are used for the

benefit of the college. Donations made to the foundation and subsequently transferred

to the college should be:

A. recognized as revenues by the foundation when received, and as revenues of the

college when transferred.

B. recognized as revenues by the foundation when received and as expenses by the

foundation when transferred.

C. recognized both as a change in its interest in the foundation and as revenues by the

college when the donation is received by the foundation.

D. recognized as an increase in net assets of the foundation and as revenues of the

college when the donation is received by the college.

Which of the following statements is true regarding the SEC’s timeline for

convergence?

A. The SEC has no immediate plans to converge GAAP reporting with IFRS standards.

B. The SEC has a plan in place to allow firms to begin filing in the United States based

on IFRS during the next several years.

C. The SEC has a plan in place to allow companies to choose to file statements under

GAAP reporting or IFRS standards indefinitely.

D. The SEC currently allows domestic companies to choose to file financial statements

under either GAAP or IFRS reporting standards.

Identify the legal term that allows the general fund to make expenditures.

A. Exceptions

B. Appropriations

C. Encumbrances

D. Consumption

On a partner’s personal statement of financial condition, assets and liabilities are

presented:

I. As current and noncurrent.

II. In order of liquidity and maturity.

A. I

B. II

C. Both I and II

D. Neither I nor II

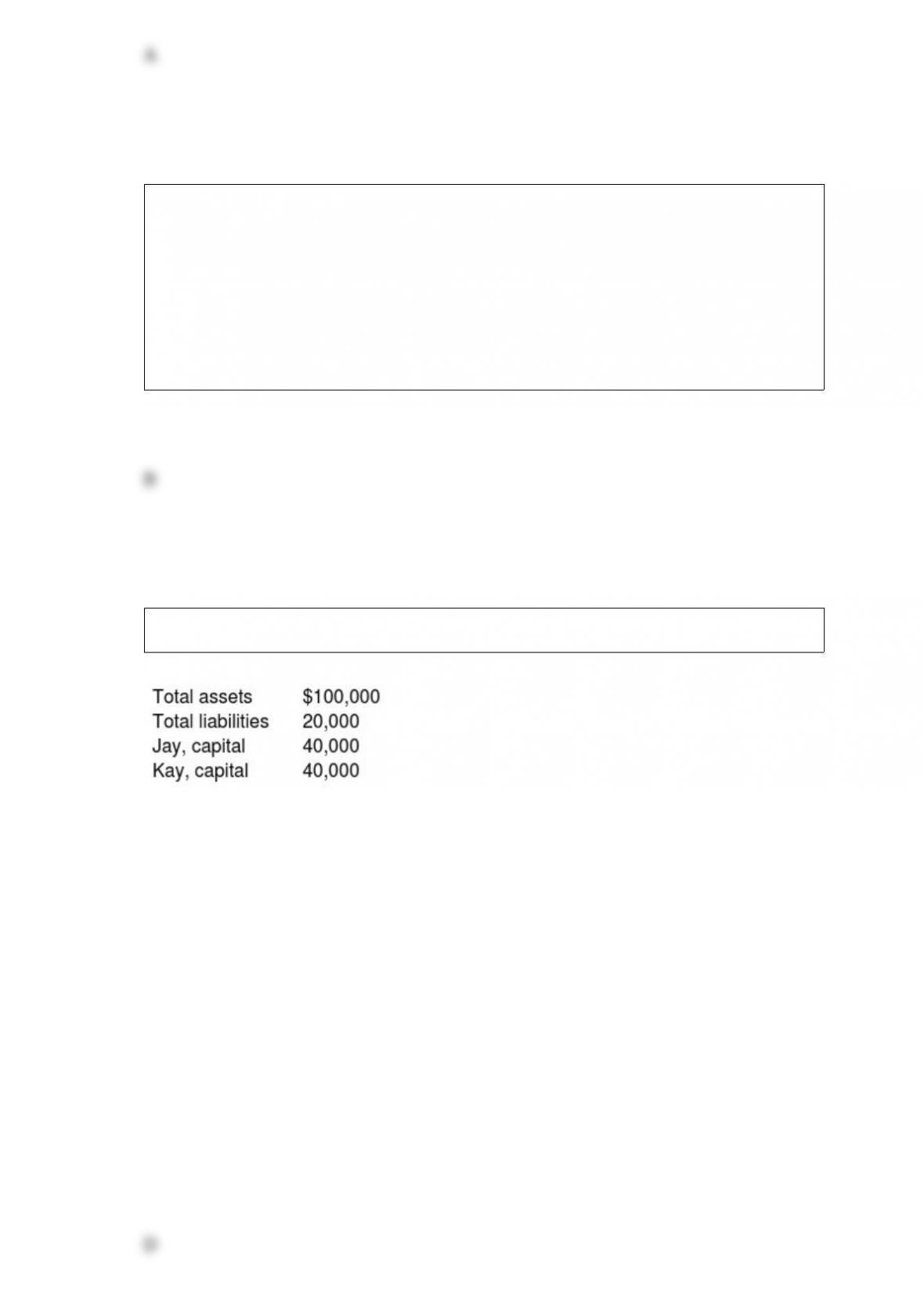

Jay & Kay partnership’s balance sheet at December 31, 20X1, reported the following:

On January 2, 20X2, Jay and Kay dissolved their partnership and transferred all assets and

liabilities to a newly-formed corporation. At the date of incorporation, the fair value of the

net assets was $12,000 more than the carrying amount on the partnership’s books, of which

$7,000 was assigned to tangible assets and $5,000 was assigned to goodwill. Jay and Kay

were each issued 5,000 shares of the corporation’s $1 par value common stock.

Immediately following incorporation, additional paid-in capital in excess of par should be

credited for

A. $77,000

B. $68,000

C. $70,000

D. $82,000

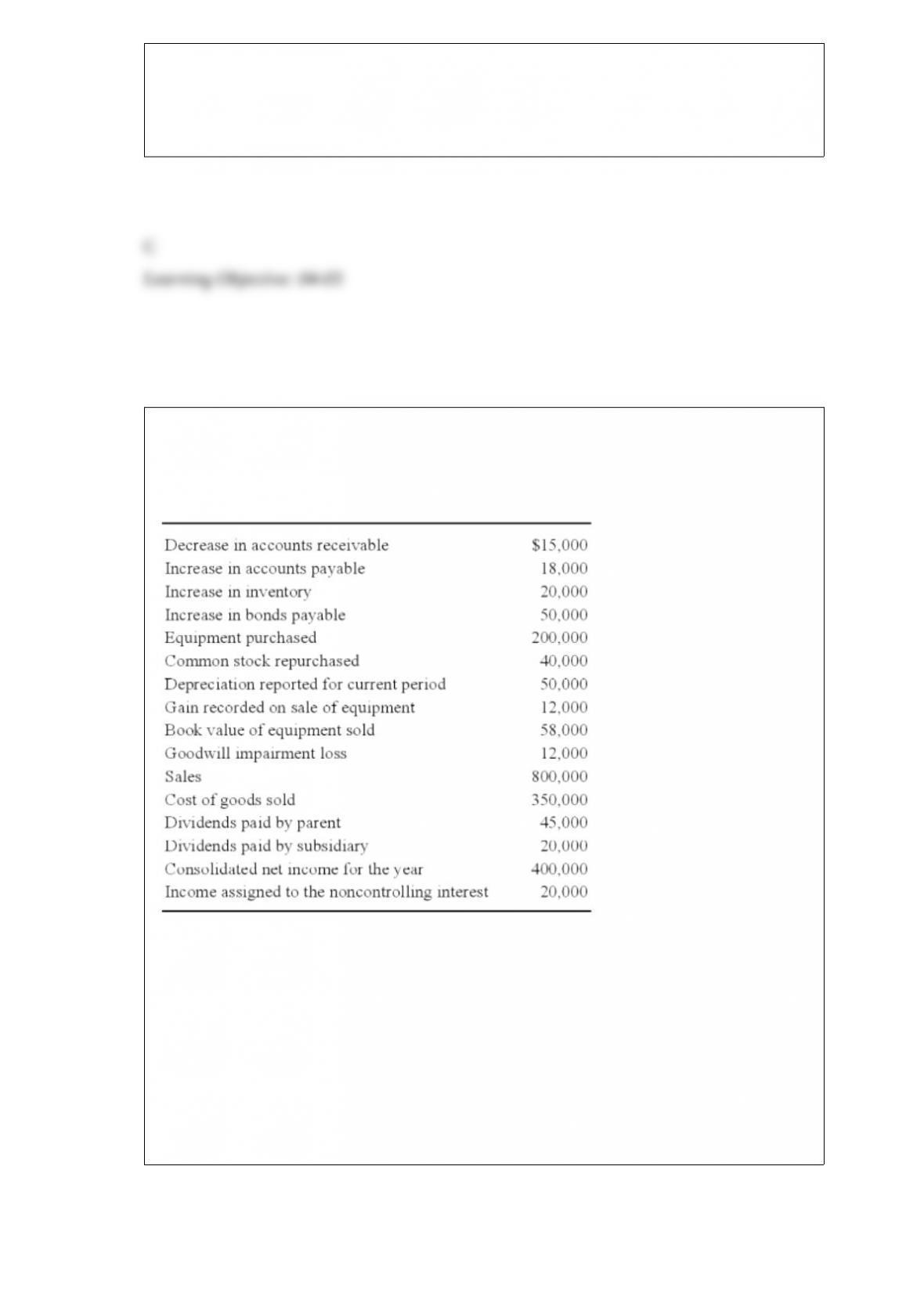

Based on the preceding information, what amount will be reported by the company as

cash flows from operating activities for 20X5?

A. $225,000

B. $227,000

C. $232,000

D. $257,000

Winner Corporation acquired 80 percent of the common shares and 70 percent of the

preferred shares of First Corporation at underlying book value on January 1, 20X9. At

that date, the fair value of the noncontrolling interest in First’s common stock was equal

to 20 percent of the book value of its common stock. First’s balance sheet at the time of

acquisition contained the following balances:

The preferred shares are cumulative and have a 10 percent annual dividend rate and are

four years in arrears on January 1, 20X9. All of the $5 par value preferred shares are

callable at $6 per share. During 20X9, First reported net income of $100,000 and paid

no dividends.

Based on the preceding information, what is First’s contribution to consolidated net

income for 20X9?

A. $80,000

B. $100,000

C. $90,000

D. $50,000

Grant, Inc. acquired 30 percent of South Co.’s voting stock for $200,000 on January 2,

20X4. Grant’s 30 percent interest in South gave Grant the ability to exercise significant

influence over South’s operating and financial policies. During 20X4, South earned

$80,000 and paid dividends of $50,000. South reported earnings of $100,000 for the six

months ended June 30, 20X5, and $200,000 for the year ended December 31, 20X5. On

July 1, 20X5, Grant sold half of its stock in South for $150,000 cash. South paid

dividends of $60,000 on October 1, 20X5.

In Grant’s December 31, 20X4, balance sheet, what should be the carrying amount of

this investment?

A. $224,000

B. $200,000

C. $234,000

D. $209,000

On January 2, 20X5, Well Co. purchased 10 percent of Rea, Inc.’s outstanding common

shares for $400,000. Well is the largest single shareholder in Rea, and Well’s officers are

a majority on Rea’s board of directors. As a result, Well is able to exercise significant

influence over Rea. Rea reported net income of $500,000 for 20X5, and paid dividends

of $150,000. In its December 31, 20X5, balance sheet, what amount should Well report

as investment in Rea?

A. $385,000

B. $450,000

C. $400,000

D. $435,000

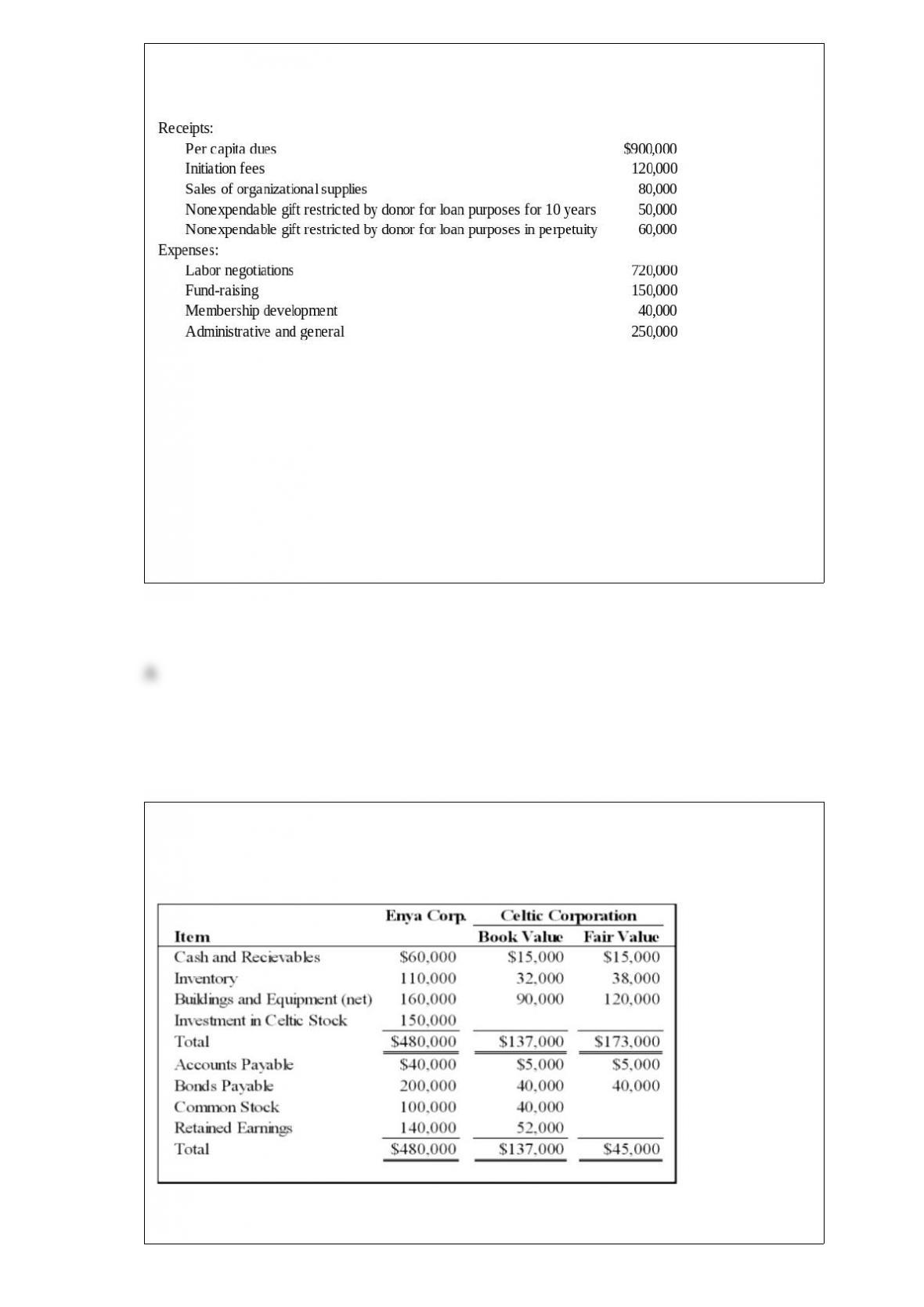

Golden Path, a labor union, had the following receipts and expenses for the year ended

December 31, 20X8:

The union’s constitution provides that 12 percent of the per capita dues be designated

for the strike insurance fund to be distributed for strike relief at the discretion of the

union’s executive board.

Based on the information provided, in Golden Path’s statement of activities for the year

ended December 31, 20X8, what amount should be reported under the classification of

program services?

A. $720,000

B. $910,000

C. $440,000

D. $760,000

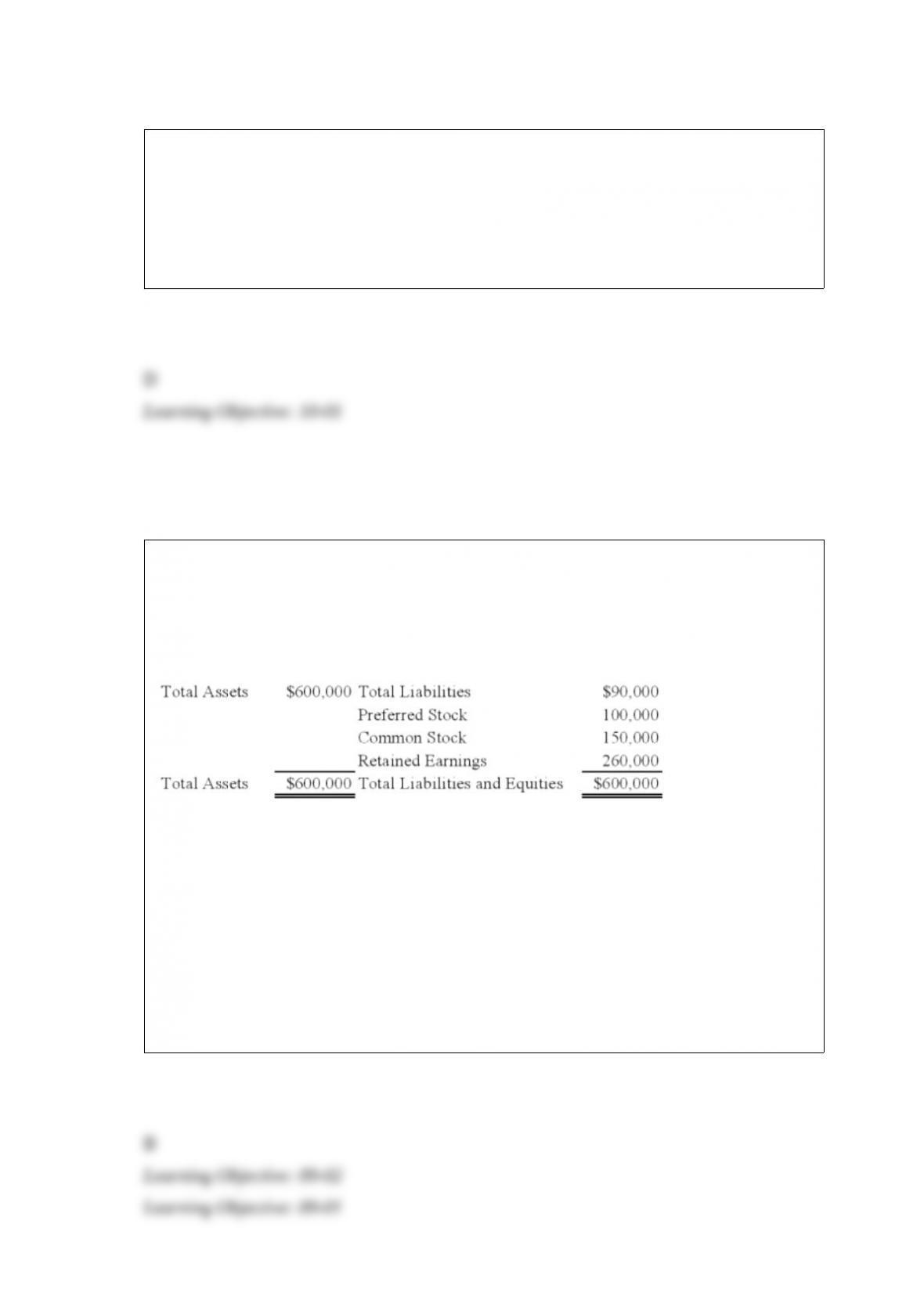

Enya Corporation acquired 100 percent of Celtic Corporation’s common stock on

January 1, 20X9. Summarized balance sheet information for the two companies

immediately after the combination is provided:

Based on the information provided, the consolidated balance sheet of Enya and Celtic

will reflect goodwill in the amount of:

A. $0.

B. $58,000.

C. $22,000.

D. $36,000.

New Life Corporation has just finished preparing a consolidated balance sheet, income

statement, and statement of changes in retained earnings for 20X9. The following items

are proposed for inclusion in the consolidated cash flow statement:

New Life holds 75 percent of the voting stock of Shane Pharmaceuticals, acquired at

book value on June 21, 20X6. On the date of the acquisition, the fair value of the

noncontrolling interest was equal to 25 percent of the book value of Shane.

Based on the preceding information, assuming that New Life uses the direct method of

computing cash flows from operating activities, what amount will be reported by the

company as cash received from customers during the year?

A. $815,000

B. $785,000

C. $800,000

D. $835,000

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units

from its LIFO-base inventory, which had originally cost $35 per unit. The replacement

cost is expected to be $45 per unit. The company is planning to reduce its inventory and

expects to replace only 1,500 of these units by December 31, the end of its fiscal year.

The company replaced 1,500 units in November at an actual cost of $50 per unit.

Based on the preceding information, in the entry to record the replacement of the 1,500

units in November, Inventory will be debited for:

A. $52,500.

B. $75,000.

C. $67,500.

D. $60,000.

The terms of a partnership agreement provide that one of the partners is to receive a

salary allowance of $30,000, plus a bonus of 20 percent of income after deduction of

the bonus and the salary allowance. If income is $150,000, the bonus should be:

A. $18,000

B. $20,000

C. $24,000

D. $30,000

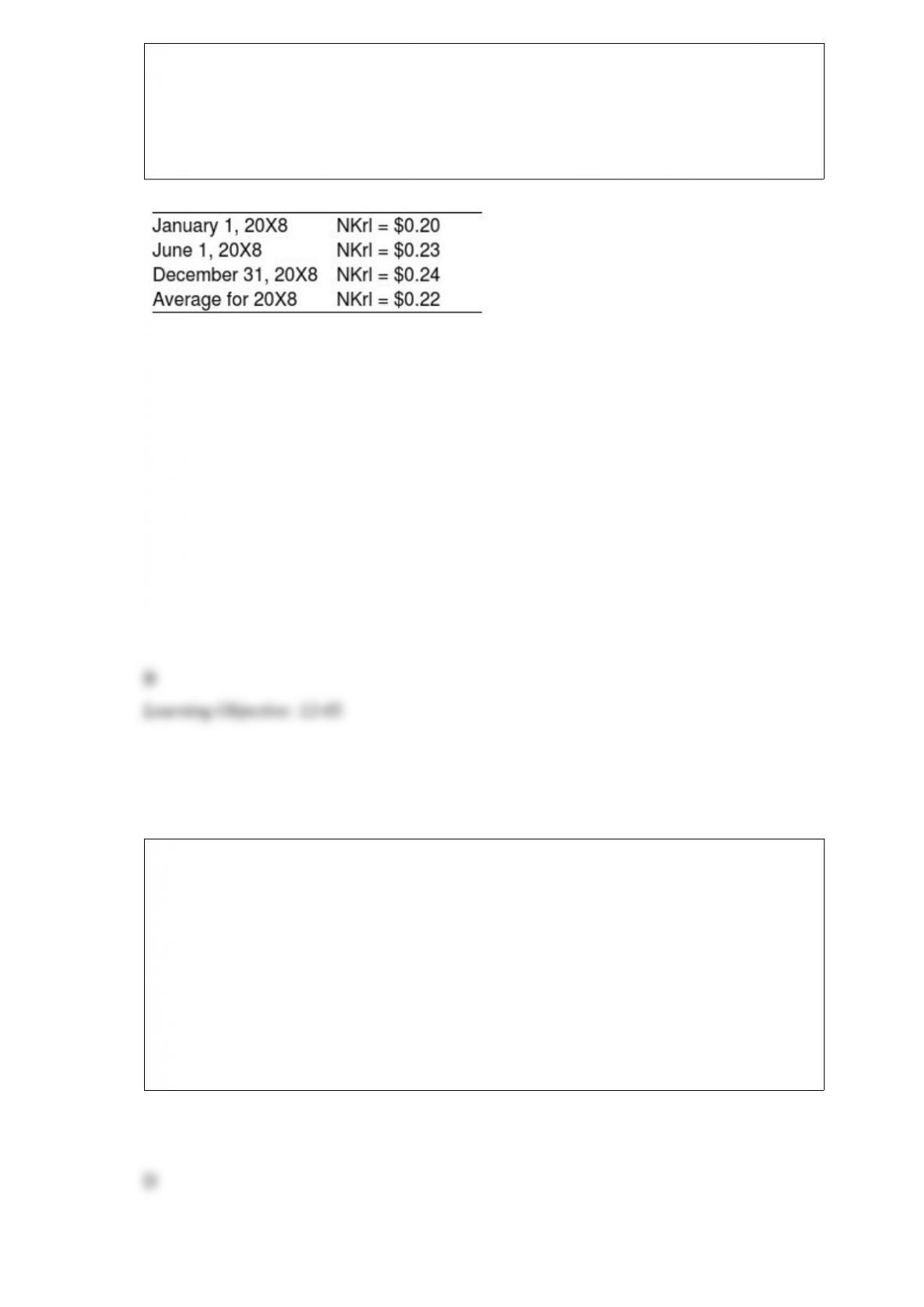

On January 1, 20X8, Transport Corporation acquired 75 percent interest in Steamship

Company for $300,000. Steamship is a Norwegian company. The local currency is the

Norwegian kroner (NKr). The acquisition resulted in an excess of cost-over-book value

of $25,000 due solely to a patent having a remaining life of 5 years. Transport uses the

fully adjusted equity method to account for its investment. Steamship’s December 31,

20X8, trial balance has been translated into U.S. dollars, requiring a translation

adjustment debit of $8,000. Steamship’s net income translated into U.S. dollars is

$35,000. It declared and paid an NKr 20,000 dividend on June 1, 20X8. Relevant

exchange rates are as follows:

Assume the kroner is the functional currency.

Based on the preceding information, in the journal entry to record the amortization of the

patent for 20X8 on the parent’s books, Investment in Steamship Company will be debited

for:

A. $5,000

B. $5,500

C. $4,500

D. $3,000

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Received contributions restricted by donors for research activities.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

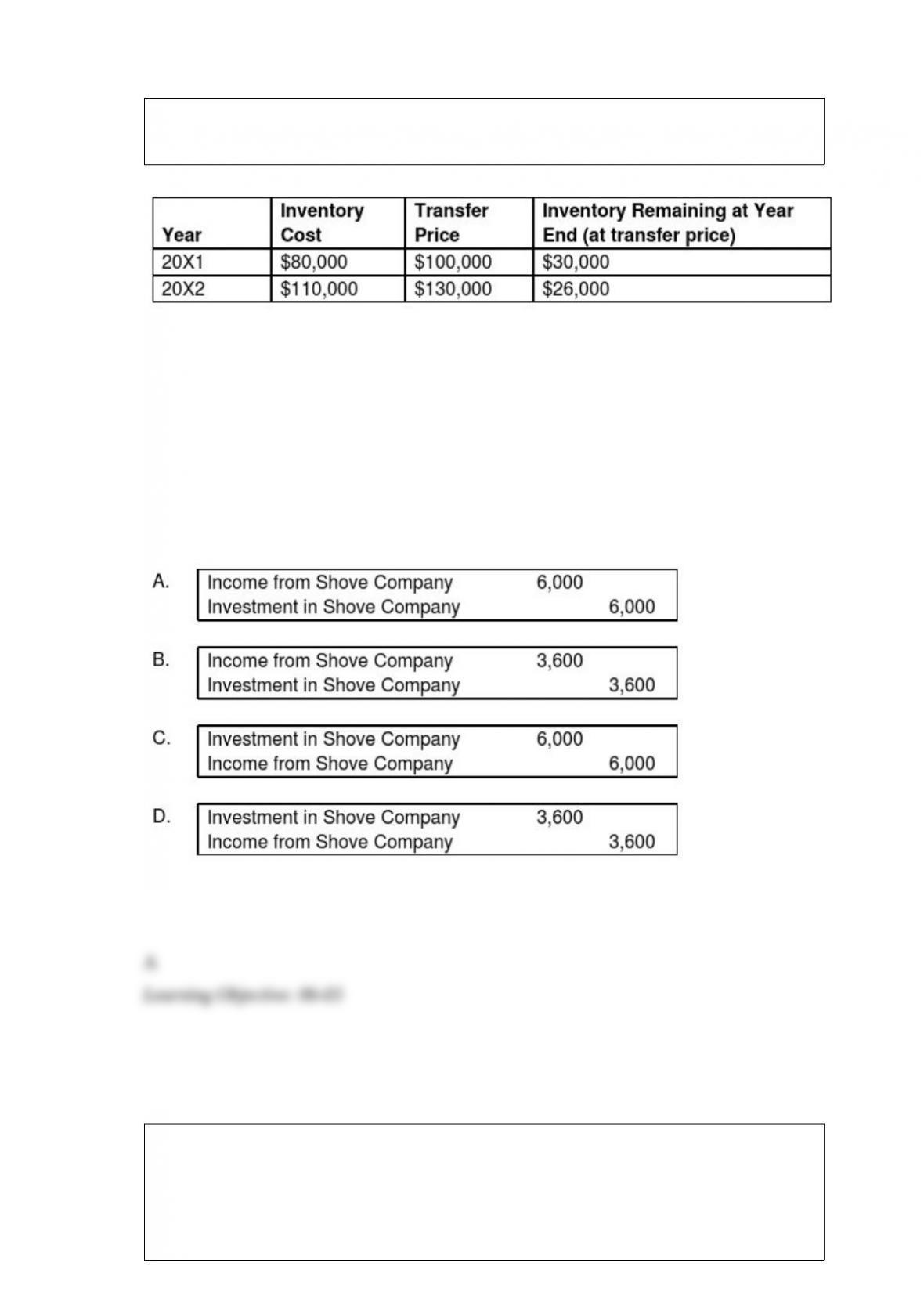

Push Company owns 60% of Shove Company’s outstanding common stock. Intra-entity

sales are as follows:

Assume Push sold the inventory to Shove. Using the fully adjusted equity method, what

journal entry would be recorded by Push to defer the unrealized gross profit on inventory

sales to Shove in 20X1?

The statement of changes in fiduciary net assets includes all of the following except:

A. employee benefit trust funds.

B. investment trust funds.

C. private-purpose trust funds.

D. agency funds.

When the local currency of the foreign subsidiary is the functional currency, a foreign

subsidiary’s inventory carried at cost would be converted to U.S. dollars by:

A. translation using historical exchange rates.

B. remeasurement using historical exchange rates.

C. remeasurement using the current exchange rate.

D. translation using the current exchange rate.

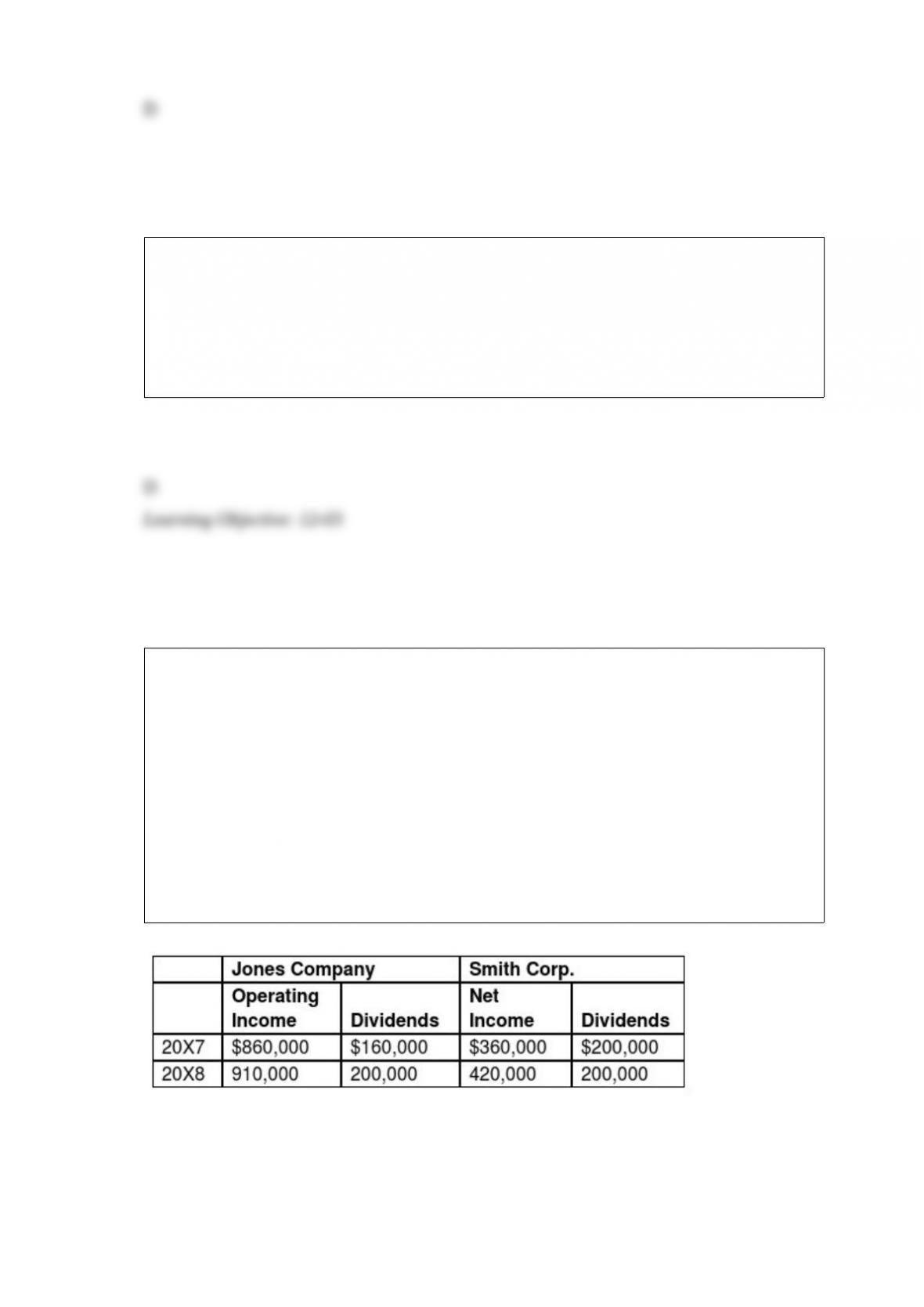

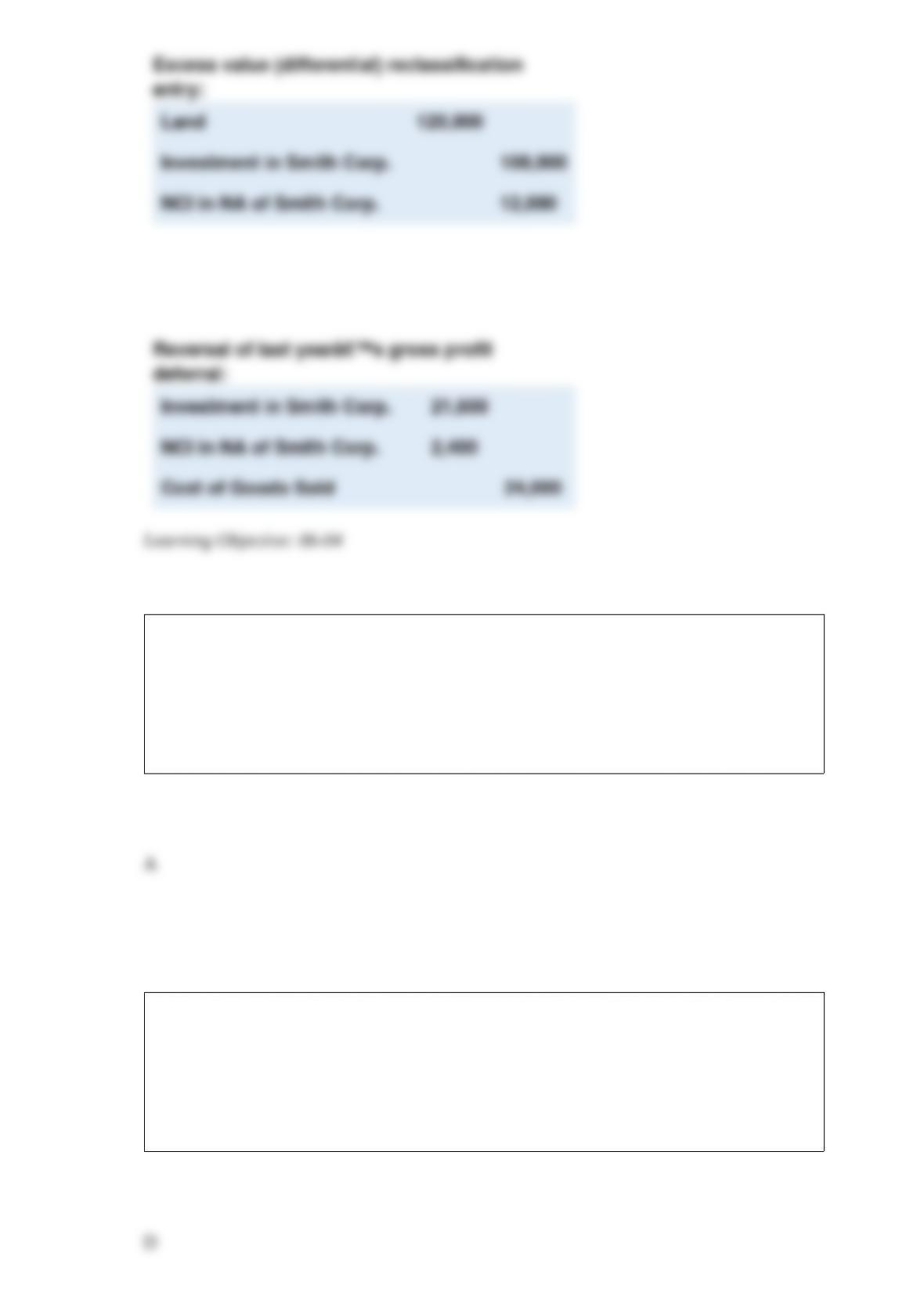

On January 1, 20X7, Jones Company acquired 90 percent of the outstanding common

stock of Smith Corporation for $1,242,000. On that date, the fair value of

noncontrolling interest was equal to $138,000. The entire differential was related to

land held by Smith. At the date of acquisition, Smith had common stock outstanding of

$520,000, additional paid-in capital of $200,000, and retained earnings of $540,000.

During 20X7, Smith sold inventory to Jones for $440,000. The inventory originally cost

Smith $360,000. By year-end, 30 percent was still in Jones’ ending inventory. During

20X8, the remaining inventory was resold to an unrelated customer. Both Jones and

Smith use perpetual inventory systems.

Income and dividend information for both Jones and Smith for 20X7 and 20X8 are as

follows:

Assume Jones uses the fully adjusted equity method to account for its investment in Smith.

Required:

a. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X7.

b. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X8.

In a town’s general fund operating budget for the year, the amount of its estimated

revenues exceeded the amount of its appropriations. This excess should be:

A. credited to Budgetary Fund Balance—Unassigned.

B. debited to Budgetary Fund Balance—Unassigned.

C. credited to Fund Balance—Unassigned.

D. debited to Fund Balance—Unassigned.

Which of the following stockholders equity accounts are eliminated during the

consolidation process?

A. Common Stock of the subsidiary

B. Preferred Stock of the subsidiary

C. Additional Paid-in Capital of the subsidiary

D. All of the above

Which of the following statements is (are) true?

I. In the calculation of the loss absorption power for a partner, a partner’s loan balance

(an amount that is owed by the partnership) should be added to the partner’s capital

balance.

II. In liquidation, a partner’s loan balance (an amount that is owed by the partnership)

should be paid to the partner as a creditor of the partnership after the outside creditors.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

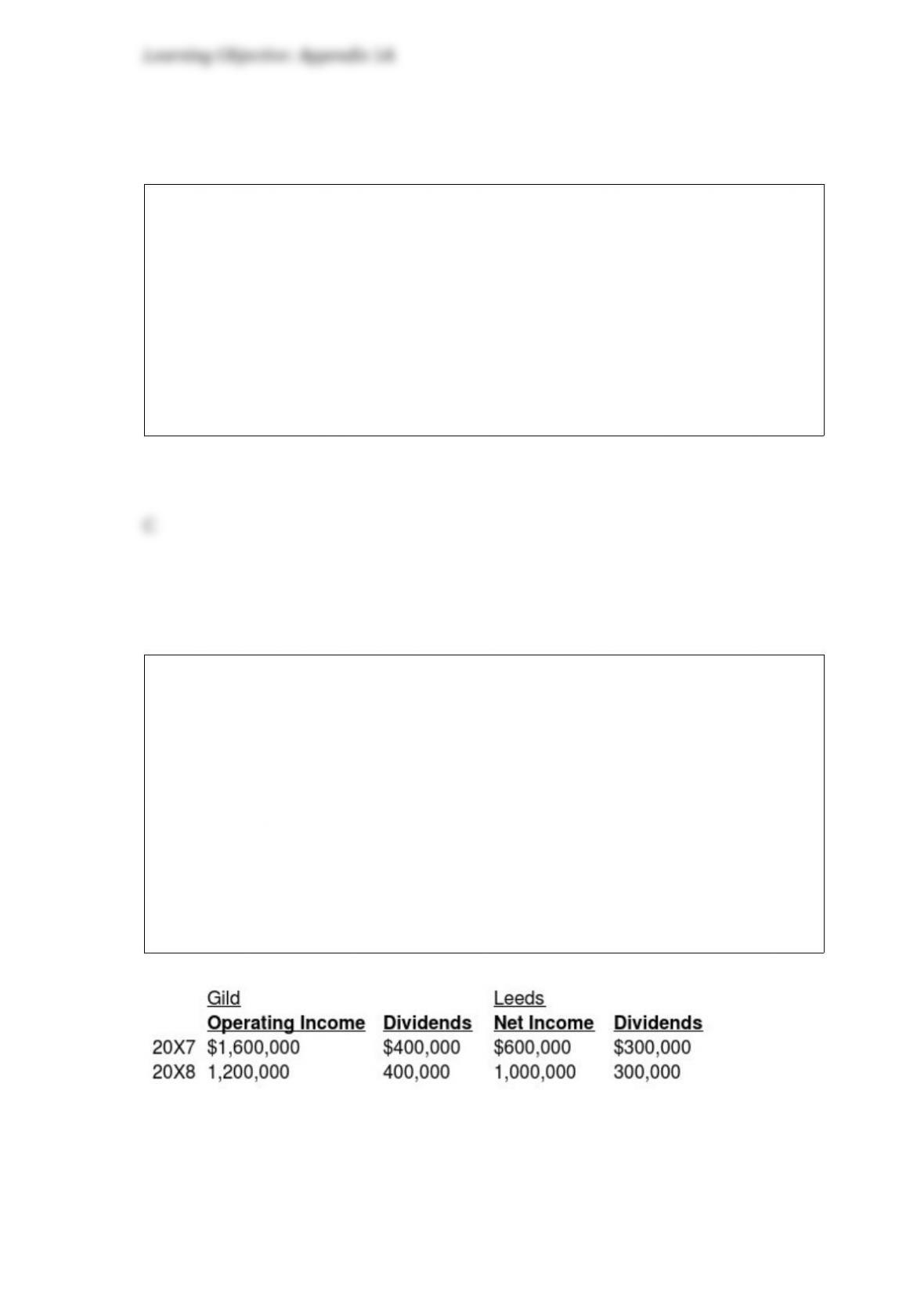

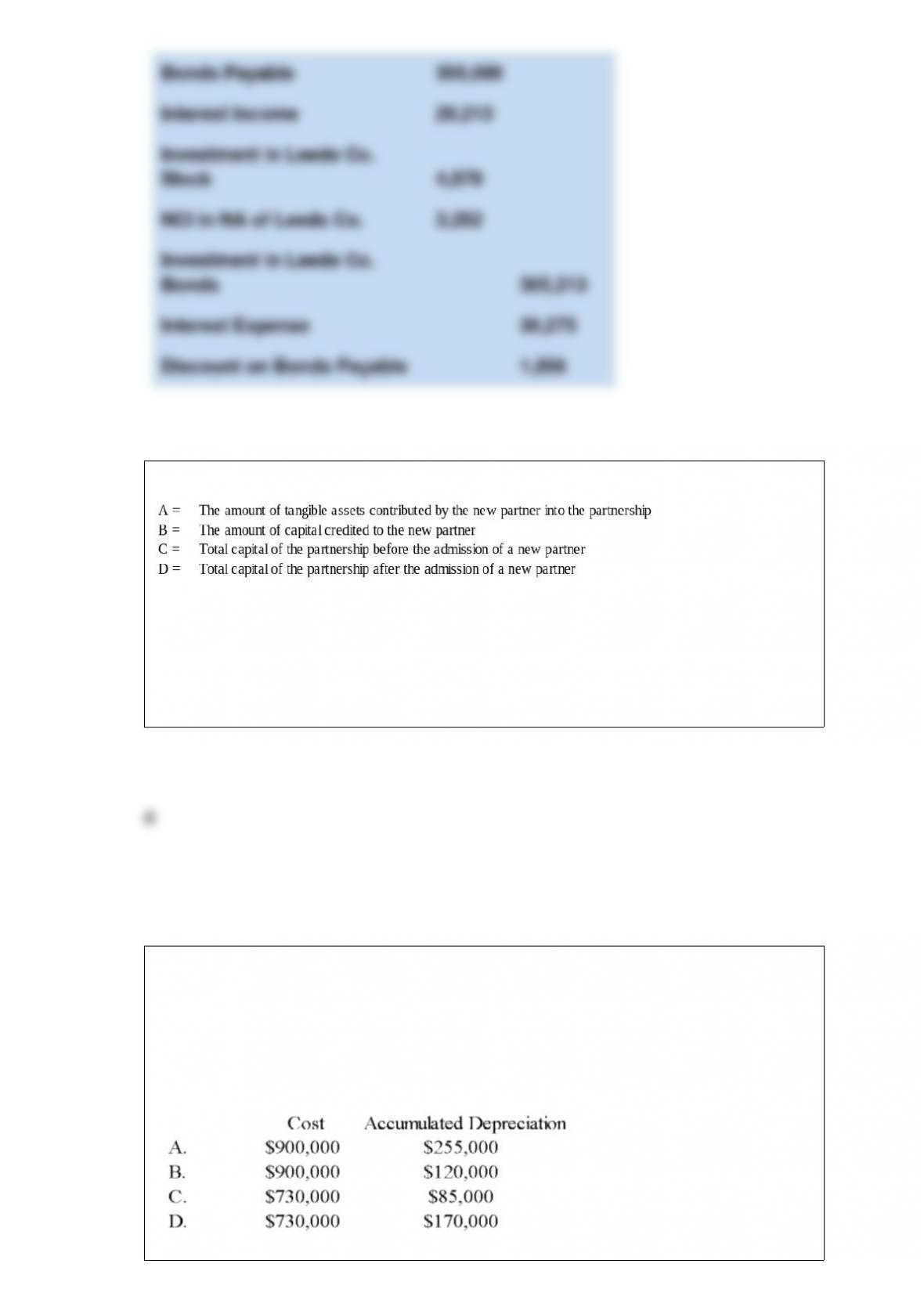

On January 1, 20X7, Gild Company acquired 60 percent of the outstanding common

stock of Leeds Company at the book value of the shares acquired. On that date, the fair

value of noncontrolling interest was equal to 40 percent of book value of Leeds. At the

time of purchase, Leeds had common stock of $1,000,000 outstanding and retained

earnings of $800,000.

On December 31, 20X7, Gild purchased 50 percent of Leeds’ bonds outstanding which

were originally issued on January 1, 20X4, at 99. The total bond issue has a face value

of $600,000, pays 10 percent interest annually, and has a 10-year maturity. Any

premium or discount is amortized using the effective interest method. Gild paid

$306,000 for its investment in Leeds’ bonds and intends to hold the bonds until

maturity.

Income and dividends for Gild and Leeds for 20X7 and 20X8 are as follows:

Assume Gild accounts for its investment in Leeds stock using the fully adjusted equity

method.

Required:

A) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X7.

B) Present the worksheet elimination entries necessary to prepare consolidated financial

statements for 20X8.

Refer to the above information. Which statement below is correct if a new partner

purchases an interest in capital directly from the old partners?

A. C < D

B. C = D

C. C = D and B = A

D. C < D and B = A

On January 1, 20X9, Light Corporation sold equipment for $400,000 to Star

Corporation, its wholly owned subsidiary. Light had paid $900,000 for this equipment,

which had accumulated depreciation of $170,000. Light estimated a $50,000 salvage

value and depreciated the tractor using the straight-line method over 10 years, a policy

that Star continued. In Light’s December 31, 20X9, consolidated balance sheet, this

tractor should be included in fixed-asset cost and accumulated depreciation as:

A. Option A

B. Option B

C. Option C

D. Option D

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount of consolidated retained earnings

will be reported in the consolidated balance sheet prepared immediately after the

business combination?

A. $180,000

B. $200,000

C. $300,000

D. $380,000

Autumn Corporation acquired 90 percent of the stock of Spring Company on January 1,

20X2, for $360,000. At that date, the fair value of the noncontrolling interest was

$40,000. Spring’s balance sheet contained the following amounts at the time of the

combination:

Cash $20,000 Accounts Payable $25,000

Accounts Receivable 60,000 Bonds Payable 75,000

Inventory 70,000 Common Stock 100,000

Buildings and Equipment (net) 350,000 Retained Earnings 300,000

Total Assets $500,000 Total Liabilities & Equity $500,000

During each of the next three years, Spring reported net income of $70,000 and paid

dividends of $20,000. On January 1, 20X4, Autumn sold 3,000 shares of Spring’s $5

par value shares for $90,000 in cash. Autumn used the fully adjusted equity method in

accounting for its ownership of Spring Company.

Based on the preceding information, what was the balance in the investment account

reported by Autumn on January 1, 20X4, before its sale of shares?

A. $360,000

B. $450,000

C. $486,000

D. $500,000

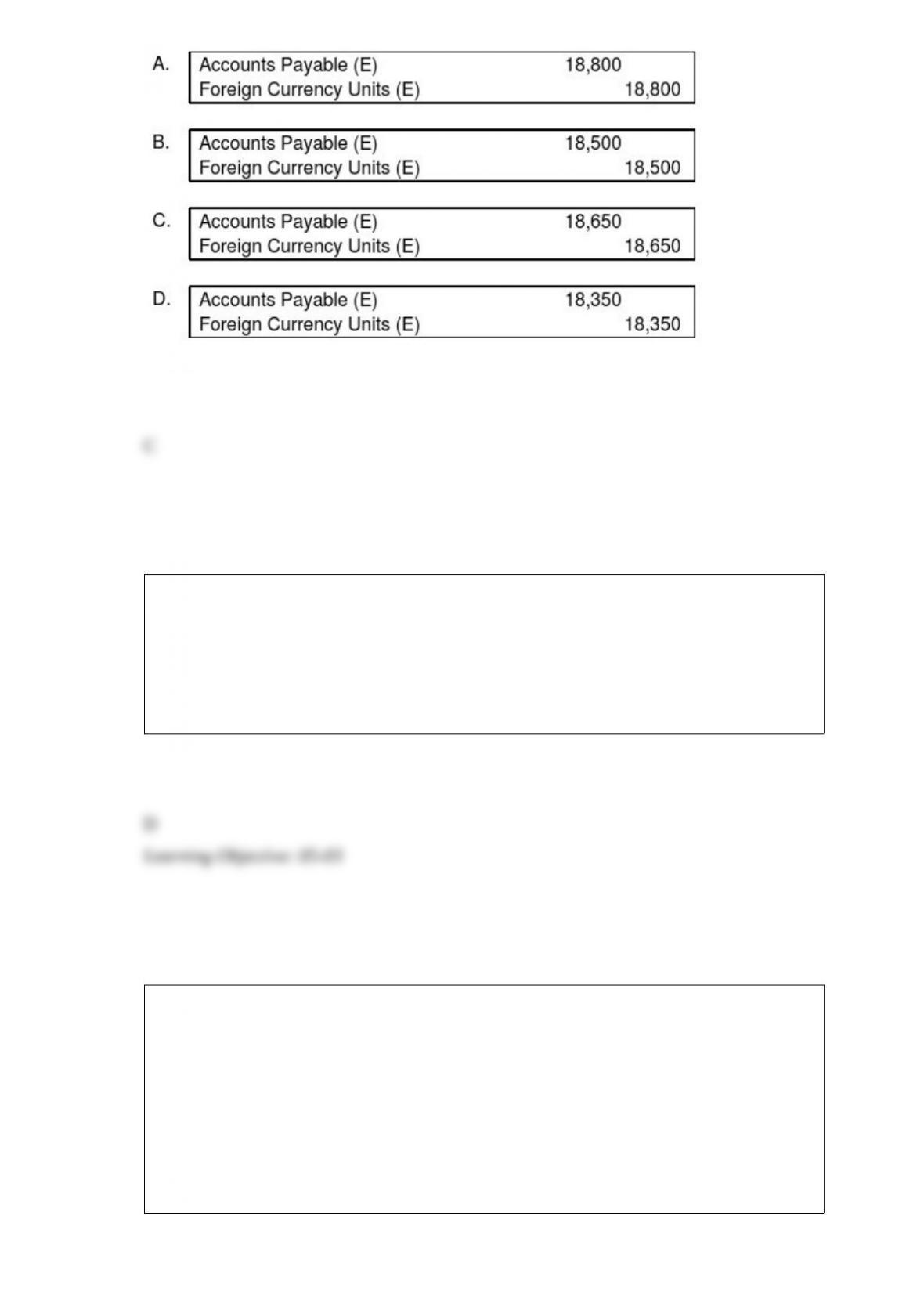

Spartan Company purchased interior decoration material from Egypt for 100,000

Egyptian pounds on September 5, 20X8, with payment due on December 2, 20X8.

Additionally, on September 5, Spartan acquired a 90-day forward contract to purchase

100,000 Egyptian pounds of E = $.1850. The forward contract was acquired to manage

the exposed net liability position in Egyptian pounds, but it was not designated as a

hedge. The spot rates were:

September 5, 20X8 E1 = $0.1835

December 2, 20X8 E1 = $0.1865

Based on the preceding information, what is the entry required to settle foreign

currency payable on December 2?

All of the following are examples of how a parent company may lose control over a

subsidiary and discontinue future consolidation, except:

A. The parent sells some of its interest in the subsidiary.

B. The subsidiary issues additional common stock.

C. The subsidiary comes under the control of the government or other regulator.

D. The subsidiary issues a stock dividend or a stock split.

Which of the following situations best describes a business combination to be

accounted for as a statutory merger?

A. Both companies in a combination continue to operate as separate, but related, legal

entities.

B. Only one of the combining companies survives and the other loses its separate

identity.

C. Two companies combine to form a new third company, and the original two

companies are dissolved.

D. One company transfers assets to another company it has created.

Light Corporation owns 80 percent of Sound Company’s voting shares. On January 1,

20X7, Sound sold bonds with a par value of $300,000 when the market rate was 7

percent. Light purchased two thirds of the bonds; the remainder was sold to

nonaffiliates. The bonds mature in ten years and pay an annual interest rate of 6 percent.

Interest is paid semiannually on June 30 and Dec 31.

Based on the information given above, what amount of interest expense will be

eliminated in the preparation of the 20X8 consolidated financial statements?

A. $13,096

B. $13,023

C. $8,730

D. $8,682

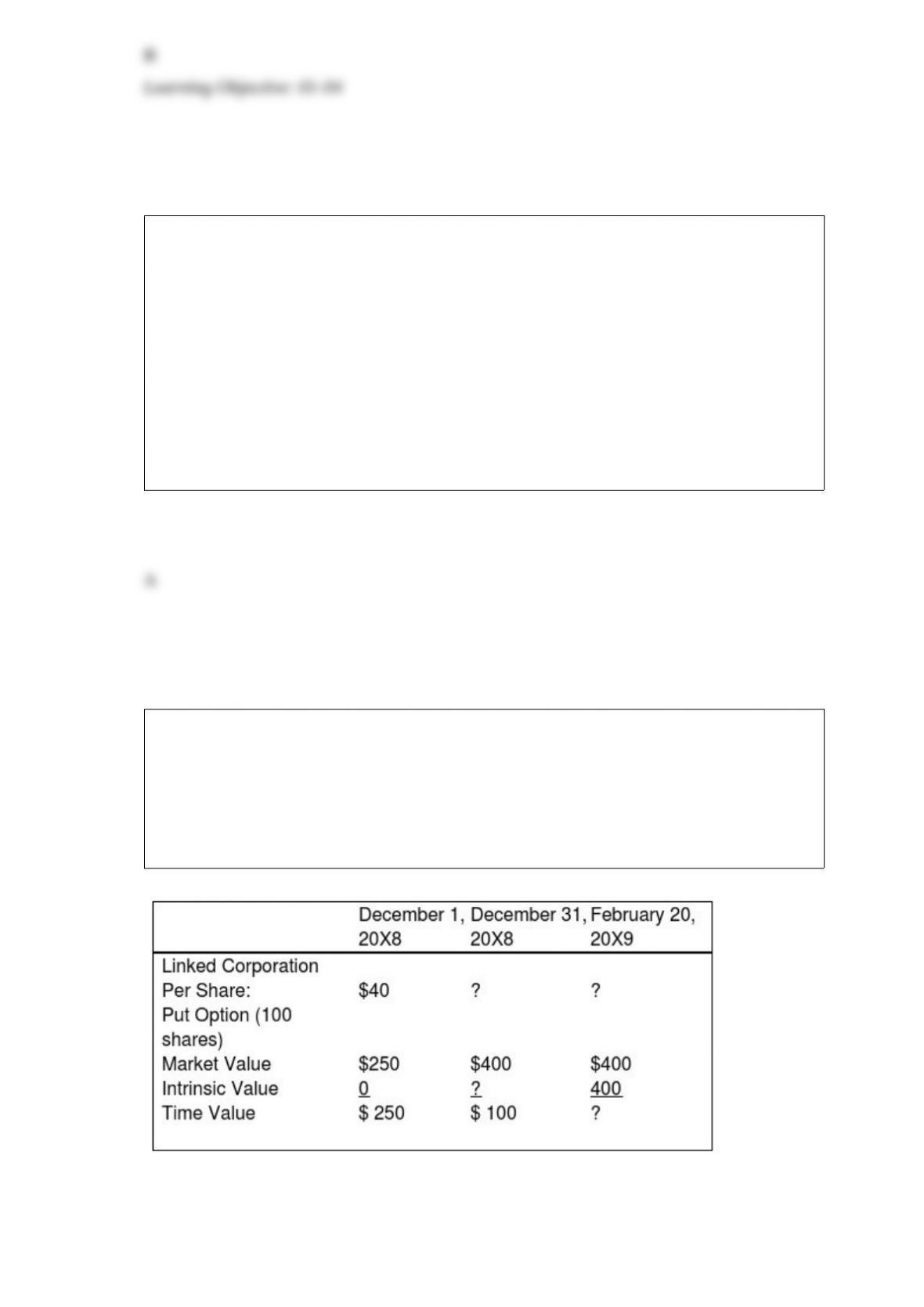

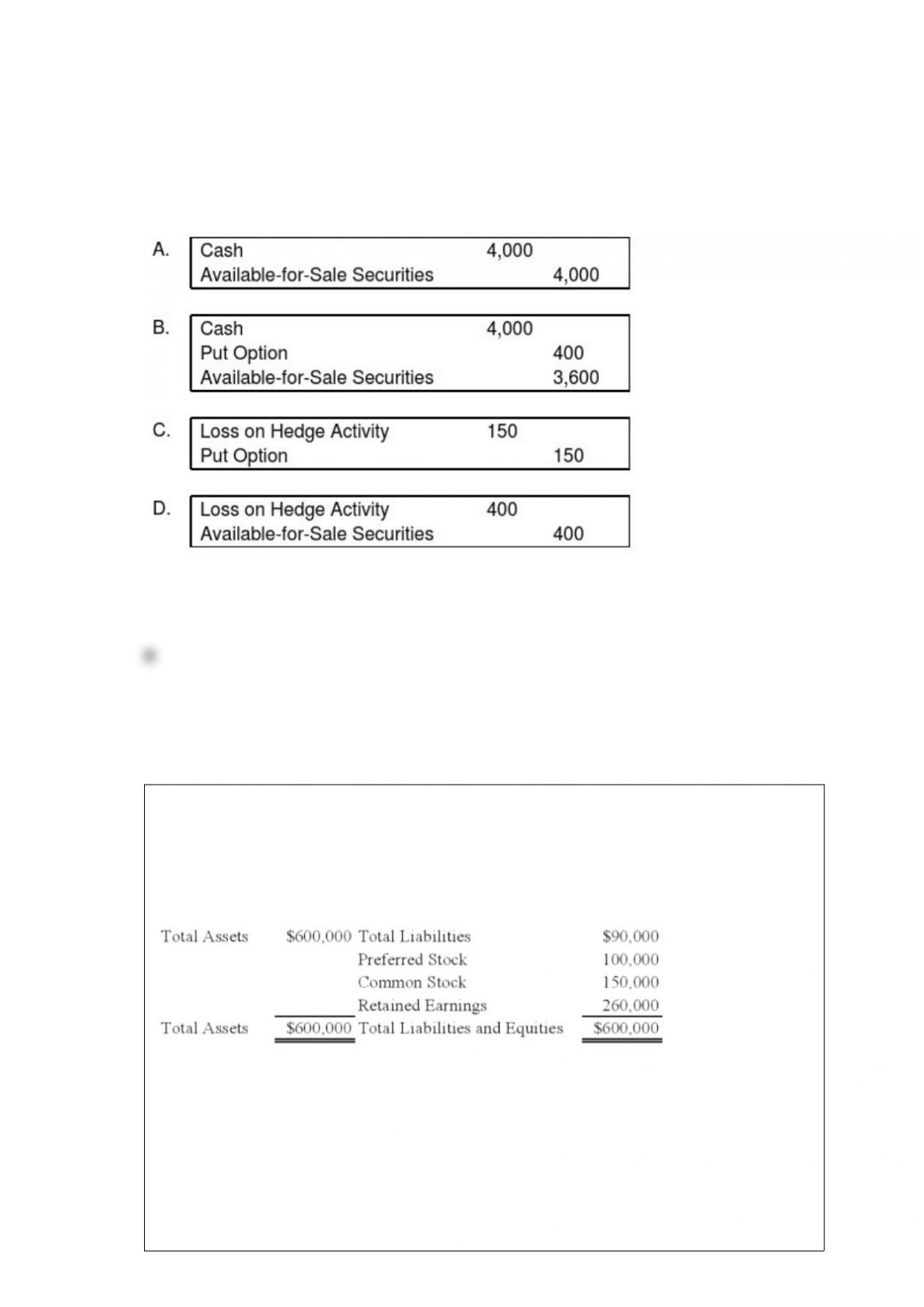

On December 1, 20X8, Winston Corporation acquired 100 shares of Linked

Corporation at a cost of $40 per share. Winston classifies them as available-for-sale

securities. On this same date, it decides to hedge against a possible decline in the value

of the securities by purchasing, at a cost of $250, an at-the-money put option to sell the

100 shares at $40 per share. The option expires on February 20, 20X9. Selected

information concerning the fair values of the investment and the options follow:

Assume that Winston exercises the put option and sells Linked shares on February 20,

20X9.

Based on the preceding information, which of the following journal entries will be made

on February 20, 20X9?

Winner Corporation acquired 80 percent of the common shares and 70 percent of the

preferred shares of First Corporation at underlying book value on January 1, 20X9. At

that date, the fair value of the noncontrolling interest in First’s common stock was equal

to 20 percent of the book value of its common stock. First’s balance sheet at the time of

acquisition contained the following balances:

The preferred shares are cumulative and have a 10 percent annual dividend rate and are

four years in arrears on January 1, 20X9. All of the $5 par value preferred shares are

callable at $6 per share. During 20X9, First reported net income of $100,000 and paid

no dividends.

Based on the preceding information, what will be the amount of income to be assigned

to the noncontrolling interest in the 20X9 consolidated income statement?

A. $21,000

B. $18,000

C. $23,000

D. $15,000