Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3–10 Reporting for a Variable Interest Entity

Gamble Company

Consolidated Balance Sheet

Cash

$ 18,600,000(a)

Buildings and Equipment

$370,600,000(b)

Less: Accumulated Depreciation

(10,100,000)

360,500,000

Total Assets

$379,100,000

Accounts Payable

$ 5,000,000

Bonds Payable

20,300,000

Bank Notes Payable

140,000,000

Noncontrolling Interest

5,600,000

Common Stock

$103,000,000

Retained Earnings

105,200,000

208,200,000

Total Liabilities and Equities

$379,100,000

(a) $18,600,000

=

$3,000,000 + $5,600,000 + ($140,000,000 – $130,000,000)

(b) $370,600,000

=

$240,600,000 + $130,000,000

E3–11 Consolidation of a Variable Interest Entity

Teal Corporation

Consolidated Balance Sheet

Total Assets

$682,500(a)

Total Liabilities

$550,000(b)

Noncontrolling Interest

22,500(c)

Common Stock

$15,000

Retained Earnings

95,000

110,000

Total Liabilities and Equities

$682,500

(a) $682,500

=

$500,000 + $190,000 – $7,500

(b) $550,000

=

$470,000 + $80,000

(c) $22,500

=

($500,000 – $470,000) x 0.75

E3-12 Computation of Subsidiary Net Income

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

P3–19 Multiple-Choice Questions on Consolidated and Combined Financial Statements

1. d – While previously reported in the ‘mezzanine’ area between liabilities and equity, FASB

160 (ASC 810) makes it clear that NCI is an element of equity, not a liability.

2. c – Similar to consolidated statements, combined financial statements require the removal of

all intercompany loans and profits. Thus, neither amount is recorded in the combined

profits.

P3-20 Determining Net Income of Parent Company

Consolidated net income

$164,300

Income of subsidiary ($15,200 / 0.40)

(38,000)

Income from Tally’s operations

$126,300

P3-21 Consolidation of a Variable Interest Entity

Stern Corporation

Consolidated Balance Sheet

January 1, 20X4

Cash

$ 8,150,000

(a)

Accounts Receivable

$12,200,000

(b)

Less: Allowance for Uncollectibles

(610,000)

(c)

11,590,000

Other Assets

5,400,000

Total Assets

$25,140,000

Accounts Payable

$ 950,000

Notes Payable

7,500,000

Bonds Payable

9,800,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$ 700,000

Retained Earnings

6,150,000

Total Controlling Interest

$ 6,850,000

Noncontrolling Interest

40,000

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

P3-24 Parent Company and Consolidated Balances

a.

Balance in investment account, December 31, 20X7

$259,800

Cumulative earnings since acquisition

110,000

Cumulative dividends since acquisition

(46,000)

Total

$64,000

Proportion of stock held by True Corporation

x 0.75

Total Amount Debited to Investment Account

(48,000)

Purchase Amount

$211,800

b. $282,400 ($211,800 / 0.75) is the fair value of net assets on January 1, 20X5

c. $70,600 ($282,400 x 0.25) is the value assigned to the NCI shareholders on January 1,

20X5.

d. $86,600 = ($259,800 / 0.75) x 0.25 will be assigned to noncontrolling interest in the

consolidated balance sheet prepared at December 31, 20X7. Alternatively, this could be

calculated by adding the NCI’s portion of the cumulative earnings and dividends to the

balance of NCI shareholders at acquisition. $70,600 + (64,000 x .25) = $86,600.

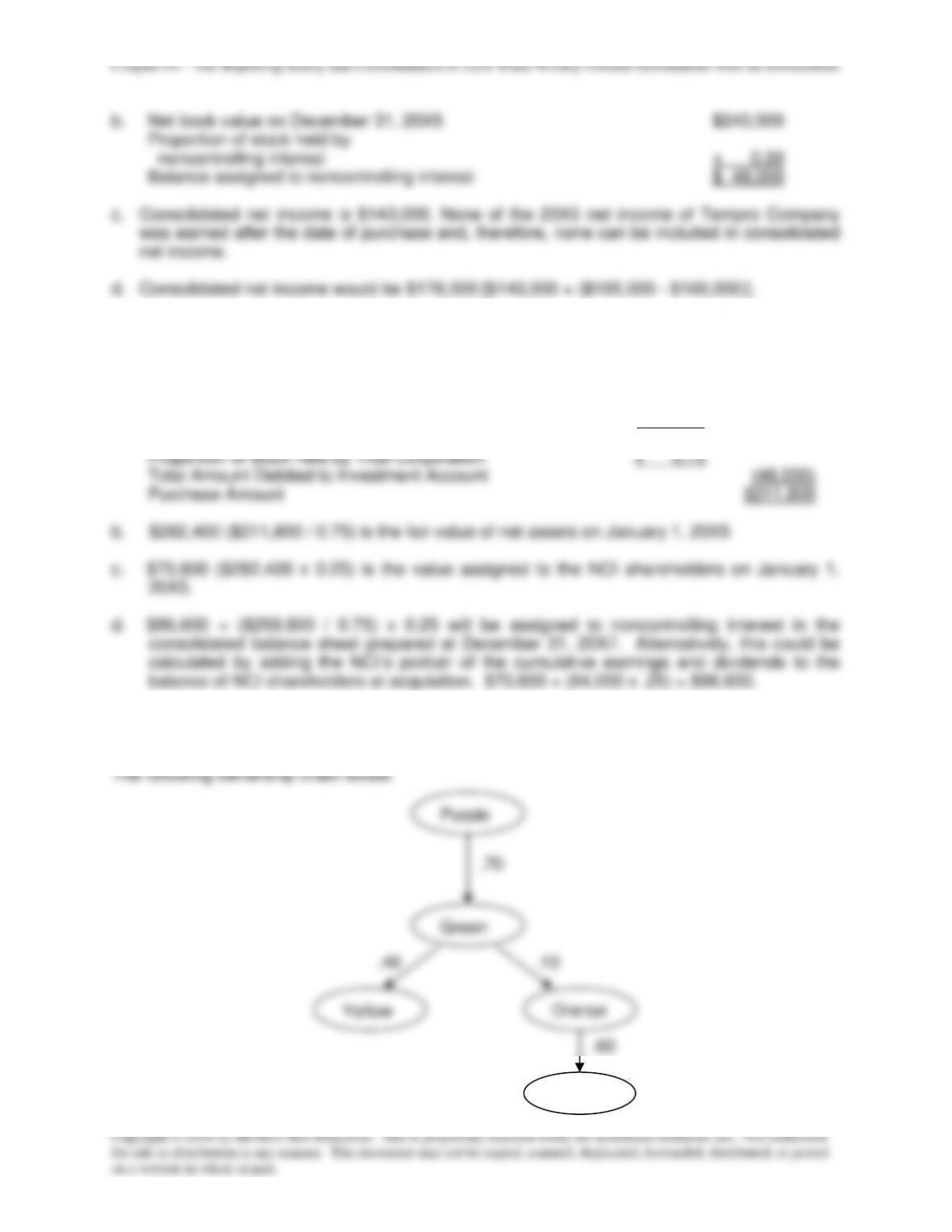

P3-25 Indirect Ownership

.10

.60

Blue

3-30

P3-26 Consolidated Worksheet and Balance Sheet on the Acquisition Date (Equity

Method)

a.

Equity Method Entries on Peanut Co.’s Books:

Investment in Snoopy Co.

270,000

Cash

270,000

Record the initial investment in Snoopy Co.

b.

Book Value Calculations:

NCI

10%

+

Peanut

Co.

90%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

30,000

270,000

200,000

100,000

Basic Consolidation Entry

Common stock

200,000

Retained earnings

100,000

Investment in Snoopy Co.

270,000

NCI in NA of Snoopy Co.

30,000

Optional accumulated depreciation consolidation entry

Accumulated depreciation

10,000

Building & equipment

10,000

Investment in

Snoopy Co.

Acquisition Price

270,000