On January 1, 20X8, William Company acquired 30 percent of eGate Company’s

common stock, at underlying book value of $100,000. eGate has 100,000 shares of $2

par value, 5 percent cumulative preferred stock outstanding. No dividends are in

arrears. eGate reported net income of $150,000 for 20X8 and paid total dividends of

$72,000. William uses the equity method to account for this investment.

Based on the preceding information, what amount would William Company receive as

dividends from eGate for the year?

A. $62,000

B. $21,600

C. $18,600

D. $54,000

West, Inc. holds 100 percent of the common stock of Coast Company, an investment

acquired for $680,000. Immediately following the combination, West’s net assets have a

book value of $1,150,000 and a fair value of $1,390,000. The book value and the fair

value of Coast’s net assets on the date of combination are $400,000 and $550,000,

respectively. Immediately following the combination, a consolidated balance sheet is

prepared.

Based on the information given above, goodwill will be reported in the consolidated

balance sheet in the amount of:

A. $240,000.

B. $130,000.

C. $150,000.

D. $270,000.

Tom, Dick, and Harry are partners in an equipment leasing business that has not been

able to generate the type of revenue expected by the partners. They share profits and

losses in a ratio of 5:3:2. They have decided to liquidate the business and have sold all

the assets except for one piece of heavy machinery. All partnership liabilities have been

settled and all the partners are personally insolvent. The machinery has a book value of

$85,000, and the partners have capital account balances as follows:

Each of the following are independent cases.

Refer to the information given above. What amount of cash will each partner receive as

a liquidating distribution if the machinery is sold for 21,100 dollars?

A. Option A

B. Option B

C. Option C

D. Option D

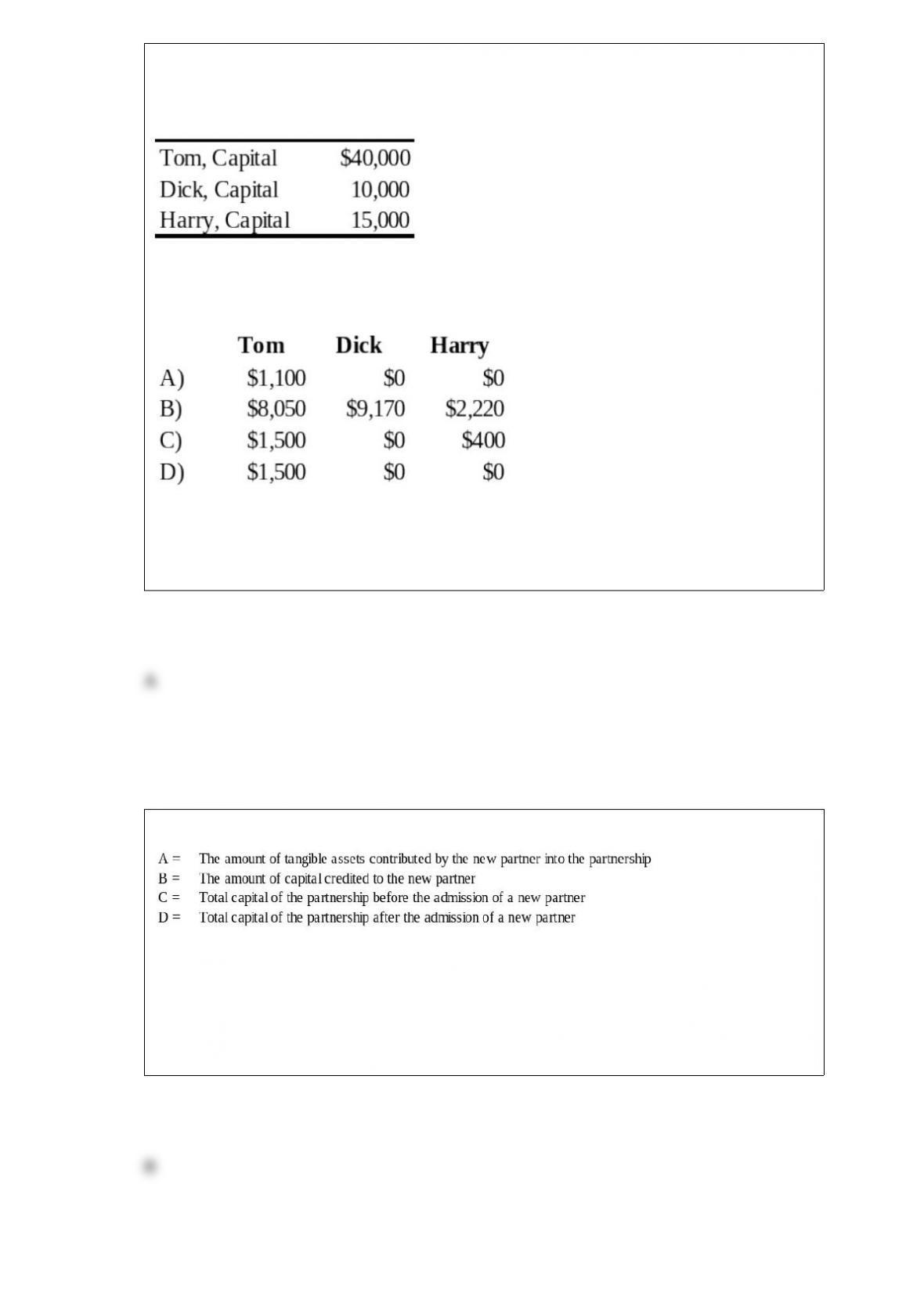

Refer to the above information. Which statement below is correct if a new partner

receives a bonus upon contributing assets into the partnership?

A. B < A and D = C – A

B. B > A and D = C + A

C. A = B and A = D + C

D. B > A and C = D + A

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite

for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment

is expected to have a 10-year useful life and no salvage value. Both companies

depreciate equipment on a straight-line basis.

Based on the preceding information, the gain on sale of the equipment recorded by

Mortar for 20X8 is:

A. $150,000

B. $65,000

C. $110,000

D. $40,000

When a partner retires from a partnership and the retiring partner is paid more than the

capital balance in her account, which of the following explains the difference?

I. The retiring partner is receiving a bonus from the other partners.

II. The retiring partner’s goodwill is being recognized.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for

equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is

expected to have a 10-year useful life and no salvage value. Both companies depreciate

equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X9 consolidated

income statement, depreciation expense will be:

A. Debited for $40,000 in the consolidating entries.

B. Credited for $10,000 in the consolidating entries.

C. Debited for $10,000 in the consolidating entries.

D. Credited for $40,000 in the consolidating entries.

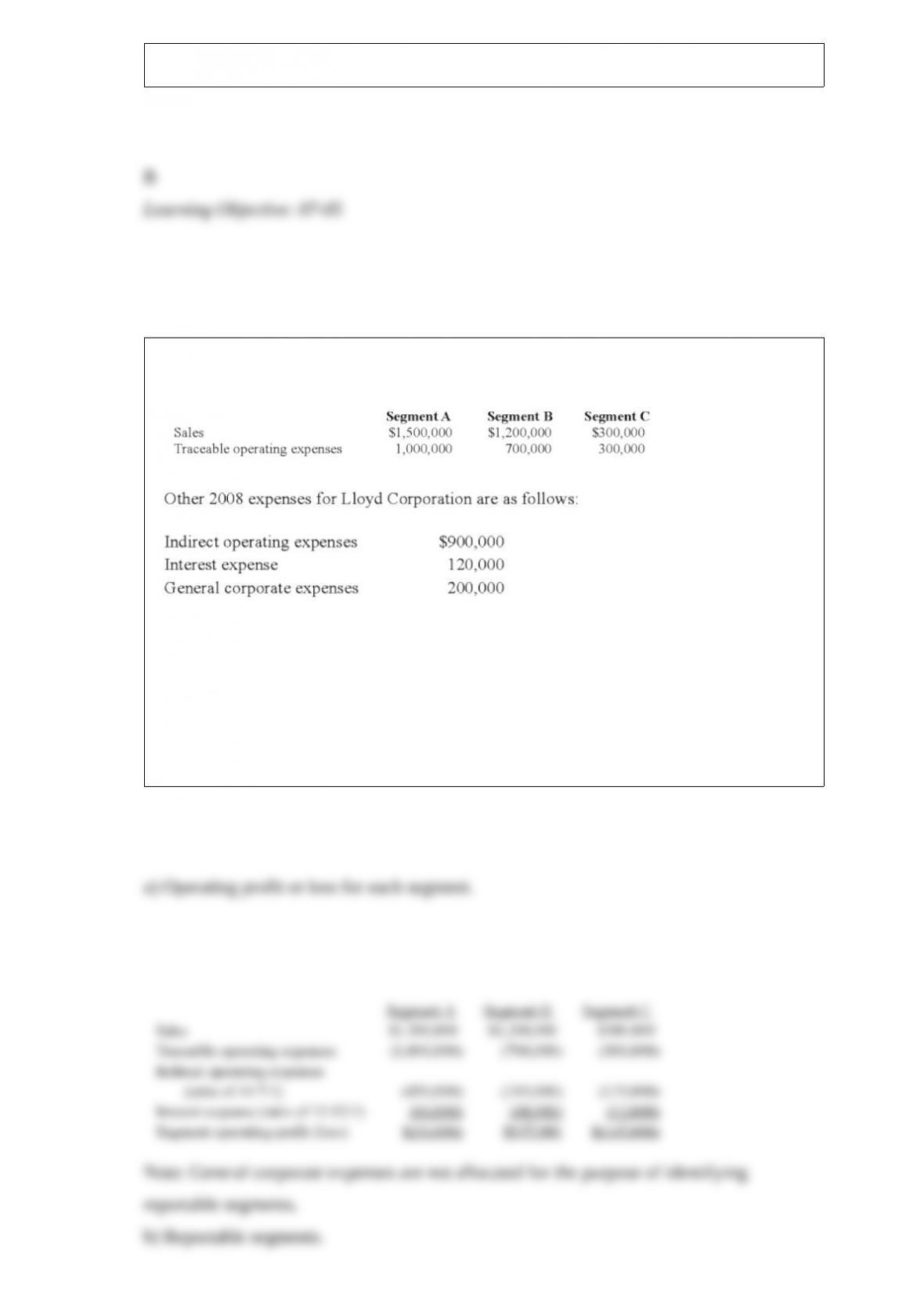

Lloyd Corporation reports the following information for 20X8 for its three operating

segments:

Indirect operating expenses are allocated to segments based upon the ratio of each

segment’s traceable operating expenses to total traceable operating expenses. Interest

expense is allocated to segments based upon the ratio of each segment’s sales to total

sales.

Required:

a) Calculate the operating profit or loss for each of the segments for 20X8.

b) Determine which segments are reportable, applying the operating profit or loss test.

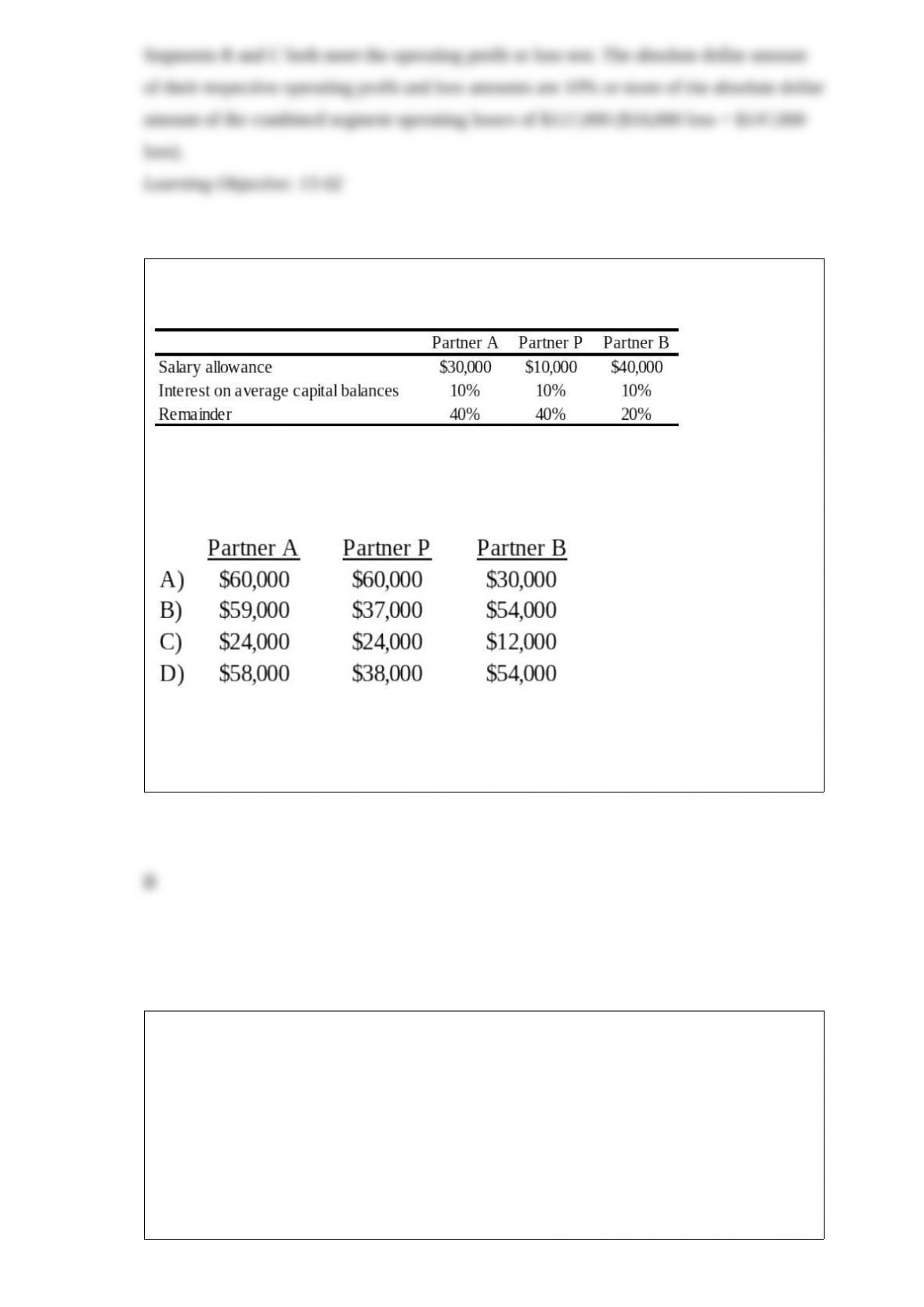

The APB partnership agreement specifies that partnership net income be allocated as

follows:

Average capital balances for the current year were $50,000 for A, $30,000 for P, and

$20,000 for B.

Refer to the information given. Assuming a current year net income of $150,000, what

amount should be allocated to each partner?

A. Option A

B. Option B

C. Option C

D. Option D

Parent Co. purchases 100 percent of Son Company on January 1, 20X1, when Parent’s

retained earnings balance is $520,000 and Son’s is $150,000. During 20X1, Son reports

$15,000 of net income and declares $6,000 of dividends. Parent reports $105,000 of

separate operating earnings plus $15,000 of equity-method income from its 100 percent

interest in Son; Parent declares dividends of $40,000.

Based on the preceding information, what is Son’s post-closing retained earnings

balance on December 31, 20X1:

A. $141,000

B. $150,000

C. $159,000

D. $165,000

Autumn Corporation acquired 90 percent of the stock of Spring Company on January 1,

20X2, for $360,000. At that date, the fair value of the noncontrolling interest was

$40,000. Spring’s balance sheet contained the following amounts at the time of the

combination:

Cash $20,000 Accounts Payable $25,000

Accounts Receivable 60,000 Bonds Payable 75,000

Inventory 70,000 Common Stock 100,000

Buildings and Equipment (net) 350,000 Retained Earnings 300,000

Total Assets $500,000 Total Liabilities & Equity $500,000

During each of the next three years, Spring reported net income of $70,000 and paid

dividends of $20,000. On January 1, 20X4, Autumn sold 3,000 shares of Spring’s $5

par value shares for $90,000 in cash. Autumn used the fully adjusted equity method in

accounting for its ownership of Spring Company.

Based on the preceding information, in the journal entry recorded by Autumn for the

sale of shares, Additional Paid-in Capital will be credited for

A. $240,000

B. $15,000

C. $9,000

D. $0

Under the equity method of accounting for a stock investment, the investment initially

should be recorded at:

A. cost.

B. cost minus any differential.

C. proportionate share of the fair value of the investee company’s net assets.

D. proportionate share of the book value of the investee company’s net assets.

GASB 34 specifies two criteria for determining major governmental funds to be

reported separately in the Governmental Fund Balance Sheet and Statement of

Revenues, Expenditures, and Changes in Fund Balances. To be considered a major

governmental fund, a fund must:

A. meet at least one criterion.

B. be the general fund or meet at least one criterion.

C. be the general fund or meet two criteria.

D. either A or C.

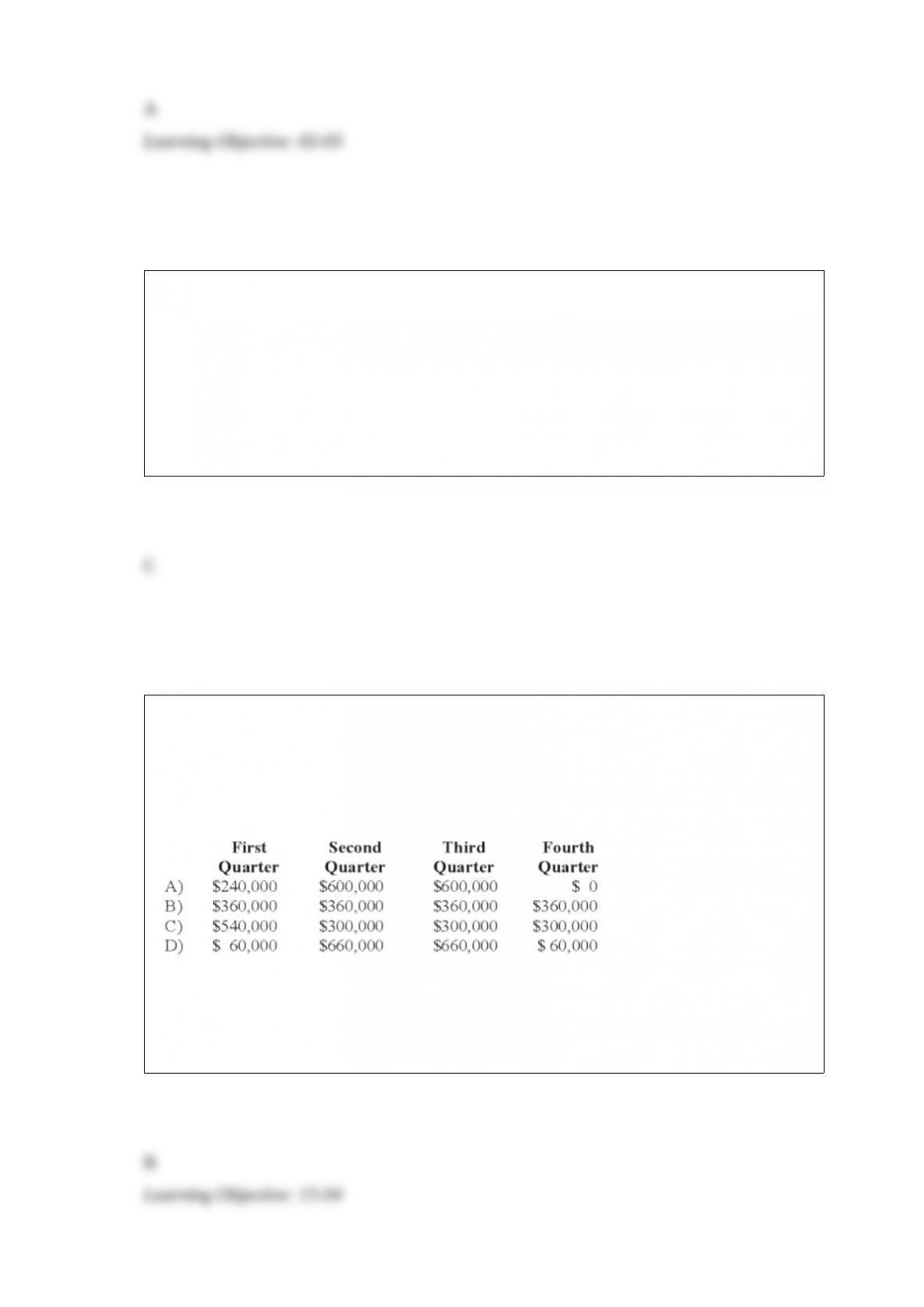

Mason Company paid its annual property taxes of $240,000 on February 15, 20X9.

Mason also anticipates that its annual repairs expense for 20X9 will be $1,200,000. This

amount is usually incurred and paid in July and August when operations are shut down

so that machinery and equipment can be repaired. What amount should Mason deduct

for property taxes and repairs in each quarter for 20X9?

A. Option A

B. Option B

C. Option C

D. Option D

Michigan-based Leo Corporation acquired 100 percent of the common stock of a

British company on January 1, 20X8, for $1,100,000. The British subsidiary’s net assets

amounted to 500,000 pounds on the date of acquisition. On January 1, 20X8, the book

values of its identifiable assets and liabilities approximated their fair values. As a result

of an analysis of functional currency indicators, Leo determined that the British pound

was the functional currency. On December 31, 20X8, the British subsidiary’s adjusted

trial balance, translated into U.S. dollars, contained $17,000 more debits than credits.

The British subsidiary reported income of 33,000 pounds for 20X8 and paid a cash

dividend of 8,000 pounds on October 25, 20X8. Included on the British subsidiary’s

income statement was depreciation expense of 3,500 pounds. Leo uses the fully

adjusted equity method of accounting for its investment in the British subsidiary and

determined that goodwill in the first year had an impairment loss of 25 percent of its

initial amount. Exchange rates at various dates during 20X8 follow:

January 1 1 = $2.10

October 25 1 = 2.25

December 31 1 = 2.20

Average for 20X8 1 = 2.21

Based on the preceding information, what amount should Leo record as “income from

subsidiary” based on the British subsidiary’s reported net income?

A. $72,930

B. $52,500

C. $72,600

D. $69,300

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company’s

common stock for $280,000 cash. At that date, Animation reported common stock

outstanding of $200,000 and retained earnings of $100,000, and the fair value of the

noncontrolling interest was $70,000. The book values and fair values of Animation’s

assets and liabilities were equal, except for other intangible assets which had a fair

value $50,000 greater than book value and an 8-year remaining life. Animation reported

the following data for 20X8 and 20X9:

Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

Based on the preceding information, what is the amount of comprehensive income

attributable to the controlling interest for 20X8?

A. $123,750

B. $118,750

C. $119,000

D. $104,000

Based on the information provided, what is the amount of consolidated retained

earnings as of December 31, 20X4?

A. $500,000

B. $710,000

C. $725,000

D. $760,000

On October 1, 20X3, Green Corporation paid $450,000 for all of Yellow Company’s

outstanding common stock. On that date, the book values and fair values of Yellow’s

recorded assets and liabilities were as follows:

Book Value Fair Value

Cash and Receivables $75,000 $75,000

Inventory 155,000 160,000

Buildings and Equipment (net) 260,000 320,000

Liabilities (150,000) (150,000)

Net Assets $340,000 $405,000

Based on the preceding information, what amount should be allocated to goodwill in

the consolidated balance sheet prepared immediately after the combination?

A. $110,000

B. $65,000

C. $45,000

D. $0

Princeton Company acquired 75 percent of the common stock of Sheffield Corporation

on December 31, 20X9. On the date of acquisition, Princeton held land with a book

value of $150,000 and a fair value of $300,000; Sheffield held land with a book value

of $100,000 and fair value of $500,000. Using the entity theory, at what amount would

land be reported in a consolidated balance sheet prepared immediately after the

combination?

A. $650,000

B. $500,000

C. $550,000

D. $375,000

Regulation S-X and Regulation S-K:

A. govern the preparation of financial statements and associated disclosures.

B. govern the registration requirements for private placements.

C. outline responsibilities for audit committees of publicly held companies.

D. prohibit artificial pyramids of capital in public utilities.

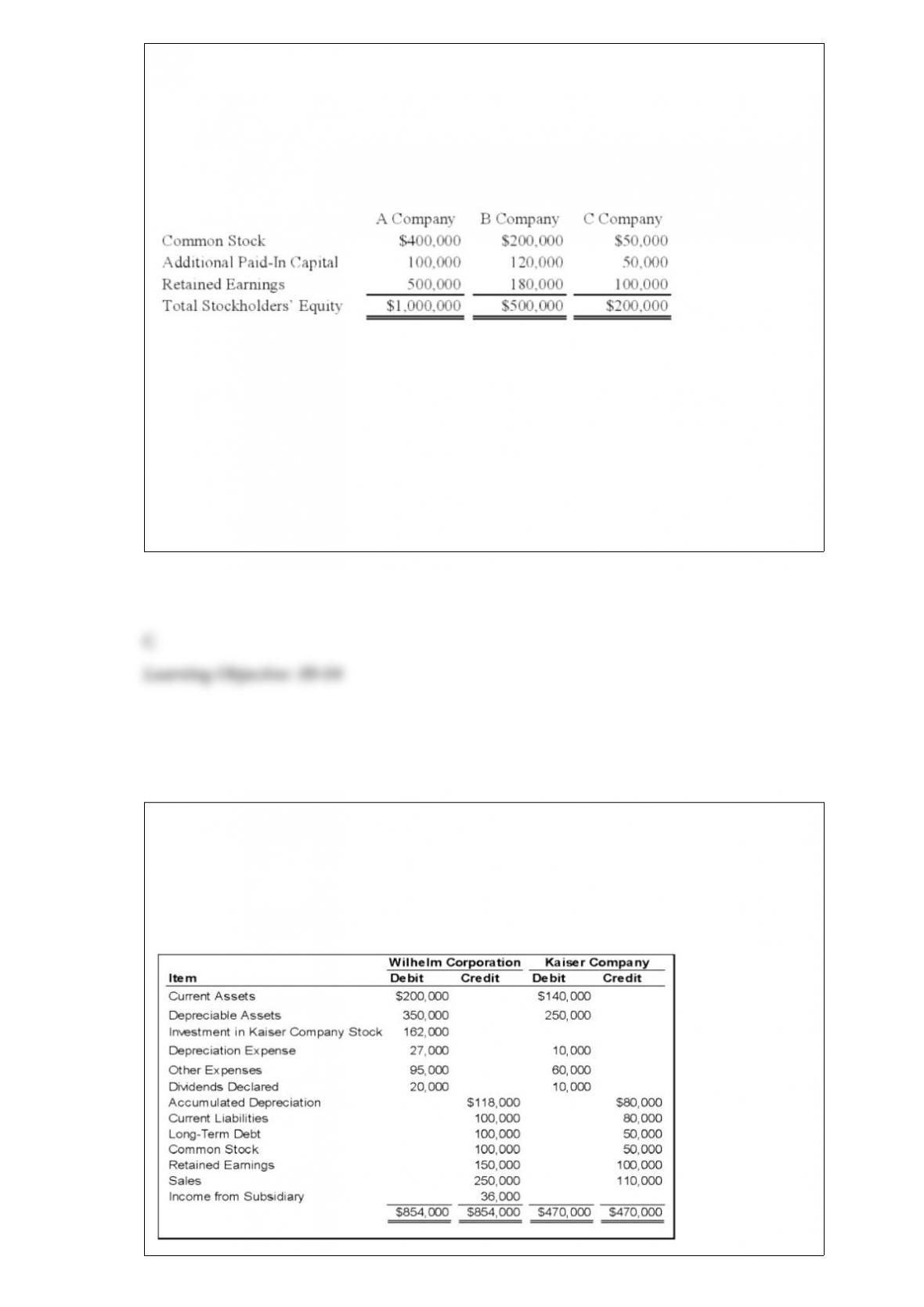

On January 1, 20X9, A Company acquired 85 percent of B Company’s voting common

stock for $425,000. At that date, the fair value of the noncontrolling interest of B

Company was $75,000. Immediately after A Company acquired its ownership, B

Company acquired 75 percent of C Company’s stock for $150,000. The fair value of the

noncontrolling interest of C Company was $50,000 at that date. At January 1, 20X9, the

stockholders’ equity sections of the balance sheets of the companies were as follows:

During 20X9, A Company reported operating income of $175,000 and paid dividends

of $50,000. B Company reported operating income of $125,000 and paid dividends of

$40,000. C Company reported net income of $100,000 and paid dividends of $25,000.

Based on the information provided, the equity-method income recorded by A Company

is:

A. $125,000

B. $200,000

C. $170,000

D. $181,250

On January 1, 20X8, Wilhelm Corporation acquired 90 percent of Kaiser Company’s

voting stock, at underlying book value. The fair value of the noncontrolling interest was

equal to 10 percent of the book value of Kaiser at that date. Wilhelm uses the equity

method in accounting for its ownership of Kaiser. On December 31, 20X9, the trial

balances of the two companies are as follows:

Based on the preceding information, what amount would be reported as retained

earnings in the consolidated balance sheet prepared at December 31, 20X9?

A. 314,000

B. 294,000

C. 150,000

D. 424,000

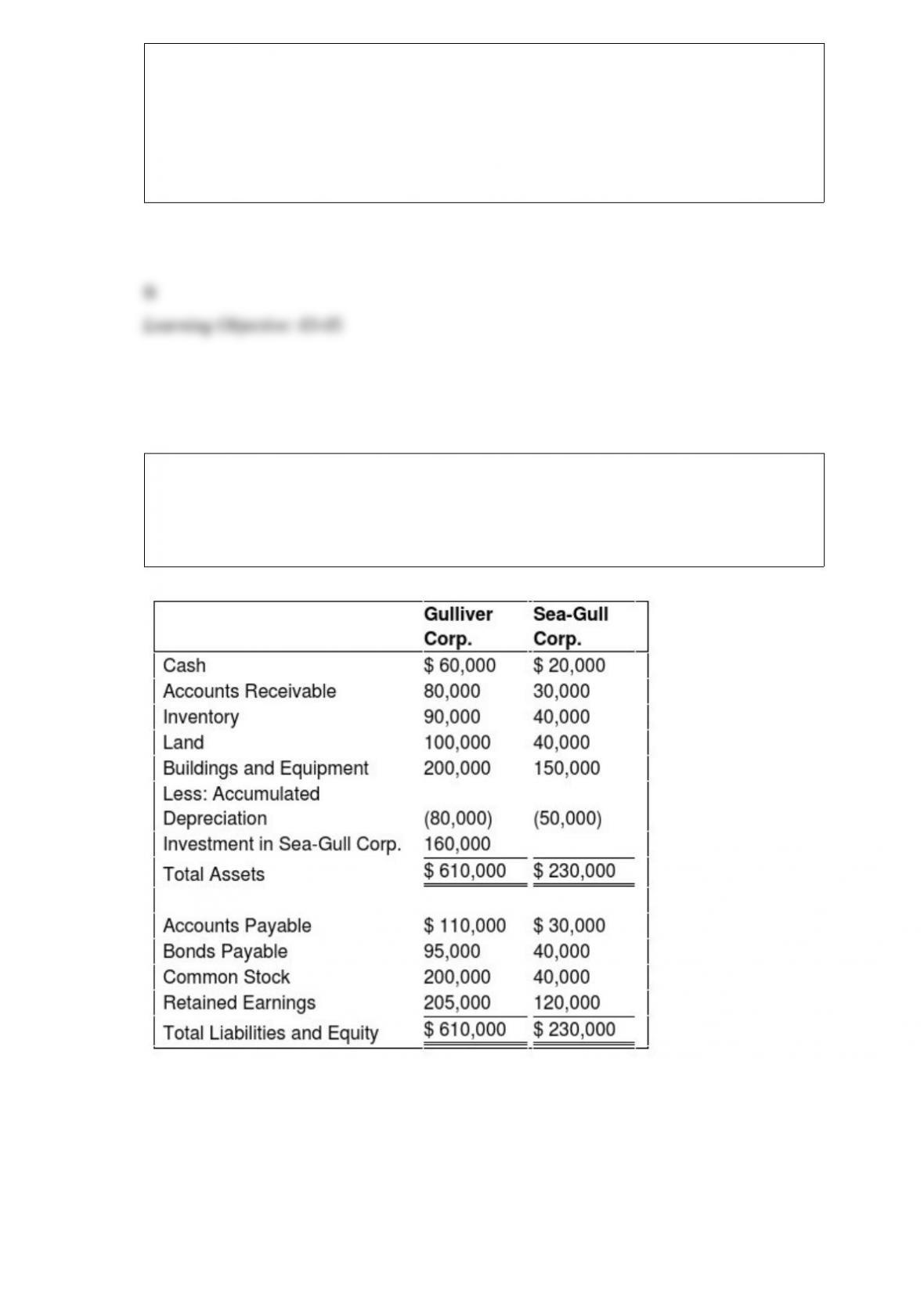

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount of consolidated retained earnings will be

reported immediately after the business combination?

A. $205,000

B. $120,000

C. $325,000

D. $310,000

ASC 280, Disclosure about Segments of an Enterprise and Related Information, has

taken what has been referred to as a “management approach” to the definition of a

segment and the allocation of costs to a segment.

Required:

a) What is meant by a management approach? How does this concept of a management

approach impact the decision to disclose information?

b) How are decisions about cost allocation handled in segment disclosures?

When the budget of a governmental unit, for which the estimated revenues exceed the

appropriations, is adopted and recorded in the general ledger at the beginning of the

year, the budgetary fund balance account is

A. Credited at the beginning of the year and debited at the end of the year.

B. Credited at the beginning of the year and no entry made at the end of the year.

C. Debited at the beginning of the year and no entry made at the end of the year.

D. Debited at the beginning of the year and credited at the end of the year.

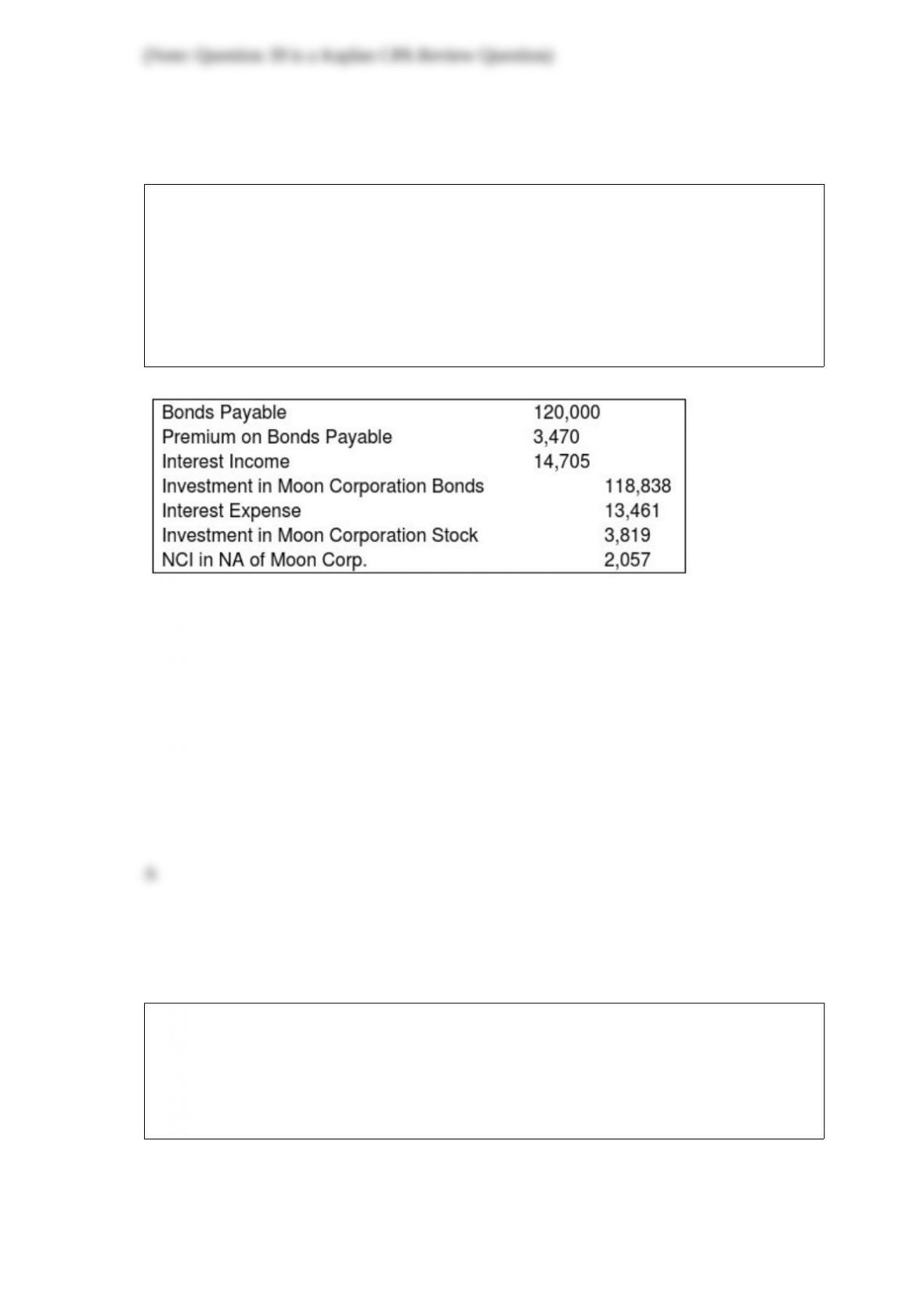

Moon Corporation issued $300,000 par value 10-year bonds at 107 on January 1, 20X3,

which Star Corporation purchased. Sun Corporation owns 65% of Moon’s voting

shares. On Jan 1, 20X7, Sun Corporation purchased $120,000 face value of Moon

bonds from Star for $118,020. On the date Sun purchased the bonds, the bonds’

carrying value on Moon’s book was $126,019. The bonds pay 12 percent interest

annually on December 31. The preparation of consolidated financial statements for

Moon and Sun at December 31, 20X9, required the following consolidating entry:

Based on the information given above, what amount of gain or loss on bond retirement is

included in the 20X7 consolidated income statement?

A. $8,000 gain

B. $5,200 gain

C. $8,000 loss

D. $5,200 loss

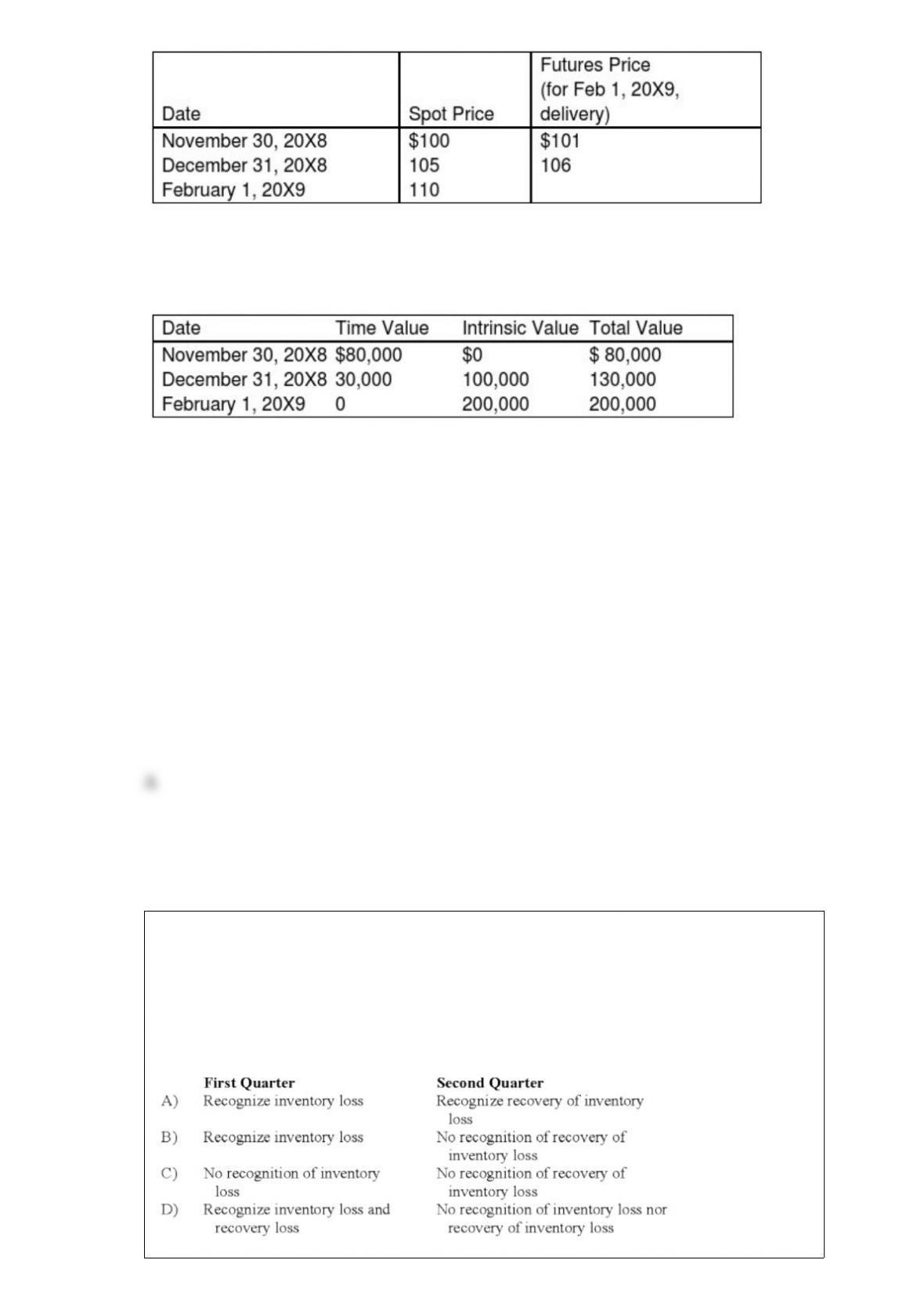

Spiralling crude oil prices prompted AMAR Company to purchase call options on oil as

a price-risk-hedging device to hedge the expected increase in prices on an anticipated

purchase of oil. On November 30, 20X8, AMAR purchases call options for 20,000

barrels of oil at $100 per barrel at a premium of $4 per barrel, with a February 1, 20X9,

call date. The following is the pricing information for the term of the call:

The information for the change in the fair value of the options follows:

On February 1, 20X9, AMAR sells the options at their value on that date and acquires

20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per

barrel.

Based on the preceding information, the entries made on April 1, 20X9 will include:

A. a debit to Other Comprehensive Income for $200,000.

B. a debit to Cost of Goods Sold for $2,240,000.

C. a credit to Oil Inventory for $2,240,000.

D. a credit to Cost of Goods Sold for $100,000.

Tyler Company incurred an inventory loss due to a decline in market prices during its

first quarter of operations in 20X8. At the end of the first quarter, management of the

company believed the decline in market prices to be permanent. In the second quarter,

the market prices of Tyler’s inventories increased above their acquisition cost. Market

prices remained higher than acquisition cost during the remainder of 20X8. How should

Tyler report the facts above on its first and second quarter income statements?

A. Option A

B. Option B

C. Option C

D. Option D

In order to avoid inequalities in the liquidation process the legal doctrine of setoff

effectively treats loans from partners to the partnership as:

A. outside debt that can offset a deficit capital account balance

B. inside debt that can offset a deficit capital account balance.

C. additional capital investments that can offset a deficit capital account balance.

D. additional capital investments that can offset a partnership loss.

Griffin and Rhodes formed a partnership on January 1, 20X9. Griffin contributed cash

of $120,000 and Rhodes contributed land with a fair value of $160,000. The partnership

assumed the mortgage on the land which amounted to $40,000 on January 1. Rhodes

originally paid $90,000 for the land. On July 31, 20X9, the partnership sold the land for

$190,000. Assuming Griffin and Rhodes share profits and losses equally, how much of

the gain from sale of land should be credited to Griffin for financial accounting

purposes?

A. $0

B. $15,000

C. $35,000

D. $45,000

Under the modified accrual basis of accounting, revenue should be recognized when it

is:

A. measurable and earned.

B. received in cash.

C. available and earned.

D. measurable and available.

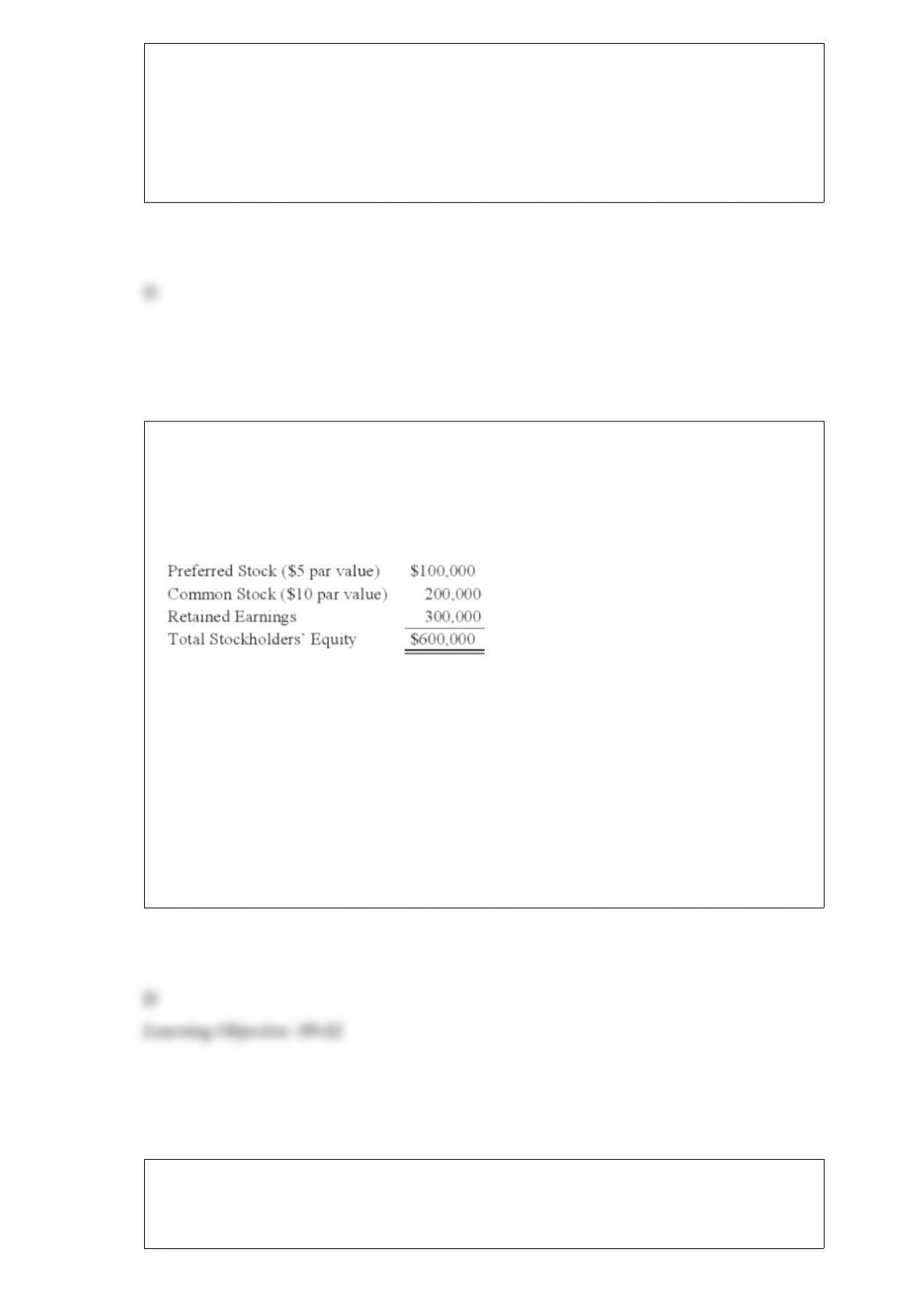

On January 1, 20X9, Company A acquired 80 percent of the common stock and 60

percent of the preferred stock of Company B, for $400,000 and $60,000, respectively.

At the time of acquisition, the fair value of the common shares of Company B held by

the noncontrolling interest was $100,000. Company B’s balance sheet contained the

following balances:

For the year ended December 31, 20X9, Company B reported net income of $100,000

and paid dividends of $40,000. The preferred stock is cumulative and pays an annual

dividend of 10 percent.

Based on the preceding information, the consolidating entry to prepare the consolidated

financial statements for Company A as of December 31, 20X9 will include a credit to

noncontrolling interest in net income of Company B for:

A. 140,000

B. 154,000

C. 152,000

D. 150,000

Reno Corporation disposed of one of its segments in the second quarter and incurred a

gain from disposal of discontinued segment of $300,000, net of taxes. What is the effect

of this gain from disposal of discontinued segment?

A. Increase each of the last three quarters’ net income by $100,000

B. Increase net income from operations for the year by $300,000

C. Increase second quarter net income by $300,000

D. Increase each quarter’s net income by $75,000

Based on the information given above, what amount of cost of goods must be

eliminated from the consolidated income statement for 20X4?

A. $3,596,000

B. $3,379,000

C. $806,000

D. $589,000

Biometric Corporation’s revenue for the year ended December 31, 20X6, was as

follows:

Consolidated revenue per income statement $400,000

Intersegment sales 30,000

Intersegment transfers 20,000

Combined revenue of all industry segments $450,000

Biometric has a reportable operating segment if that segment’s revenue exceeds

A. $40,000

B. $42,000

C. $43,000

D. $45,000

Binary Company acquired 75 percent ownership of Fordham Corporation in 20X5, at

underlying book value. On that date, the fair value of the noncontrolling interest was

equal to 25 percent of the book value of Fordham Corporation. Binary purchased

inventory from Fordham for $150,000 on July 24, 20X6, and resold 90 percent of the

inventory to unaffiliated companies on November 11, 20X6, for $160,000. Fordham

produced the inventory sold to Binary for $120,000. The companies had no other

transactions during 20X6.

Based on the information given above, what amount of cost of goods sold will be

reported in the 20X6 consolidated income statement?

A. $90,000

B. $108,000

C. $120,000

D. $135,000

Binary Company acquired 75 percent ownership of Fordham Corporation in 20X5, at

underlying book value. On that date, the fair value of the noncontrolling interest was

equal to 25 percent of the book value of Fordham Corporation. Binary purchased

inventory from Fordham for $150,000 on July 24, 20X6, and resold 90 percent of the

inventory to unaffiliated companies on November 11, 20X6, for $160,000. Fordham

produced the inventory sold to Binary for $120,000. The companies had no other

transactions during 20X6.

Based on the information given above, what inventory balance will be reported by the

consolidated entity on December 31, 20X6?

A. $3,000

B. $12,000

C. $15,000

D. $25,000

On June 30, 20X0, Bow Corporation incurred a $150,000 net loss from disposal of a

business component. Also on June 30, 20X0, Bow paid $50,000 for property taxes

assessed for the calendar year 20X0. What amount of the preceding items should be

included in the determination of Bow’s net income or loss for the six-month interim

period ended June 30, 20X0?

A. $100,000

B. $150,000

C. $175,000

D. $200,000

On January 1, 20X6, Joseph Company acquired 80% of Salt Company’s outstanding

stock for cash. The fair value of the noncontrolling interest was equal to a proportionate

share of the book value of Salt Company’s net assets at the date of acquisition. Selected

balance sheet data at December 31, 20X6 are as follows:

Joseph Salt

Total Assets $564,000 $241,000

Liabilities $180,000 $65,000

Common Stock 150,000 80,000

Retained Earnings 234,000 96,000

$564,000 $241,000

Based on the preceding information, what amount should be reported as noncontrolling

interest in net assets in Joseph Company’s December 31, 20X6, consolidated balance

sheet?

A. $35,200

B. $48,200

C. $76,800

D. $112,800

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Jacob and Katy agree that some of the

inventory is obsolete. The inventory account is decreased before Erin is admitted. Erin

invests $38,000 for a one-fifth interest. What is the amount of inventory written down?

A. $10,000

B. $20,000

C. $28,000

D. $36,000

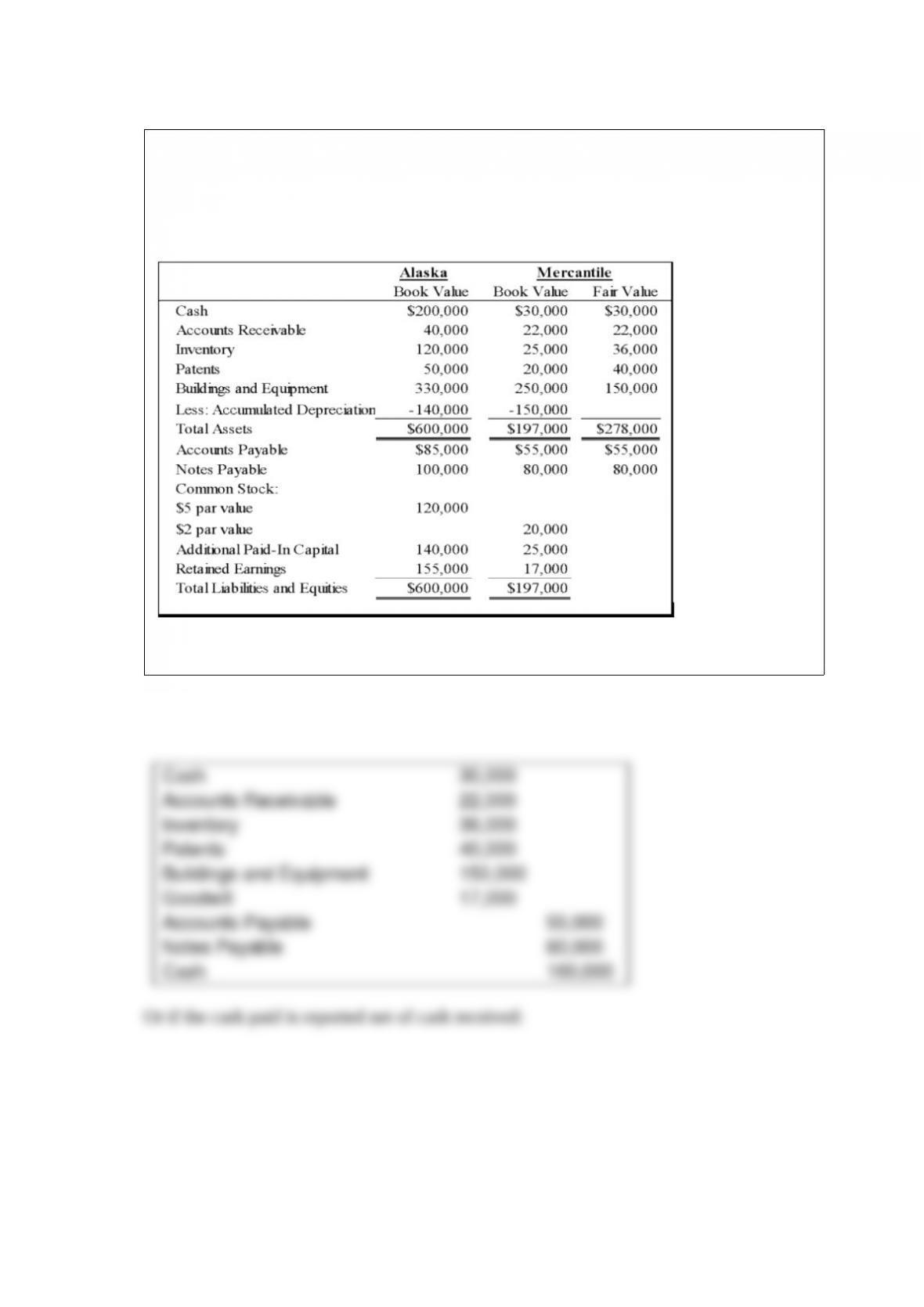

On January 1, 20X8, Alaska Corporation acquired Mercantile Corporation’s net assets

by paying $160,000 cash. Balance sheet data for the two companies and fair value

information for Mercantile Corporation immediately before the business combination

are given below:

Required:

Prepare the journal entry to record the acquisition of Mercantile Corporation.

Briefly explain the three classes of creditors specified in the Bankruptcy Code.

During the third quarter of 20X4, Ripley Company sold a piece of equipment at a

$10,000 gain. What portion of the gain should Ripley report in its income statement for

the third quarter of 20X4?

A. $10,000

B. $7,500

C. $2,500

D. $0

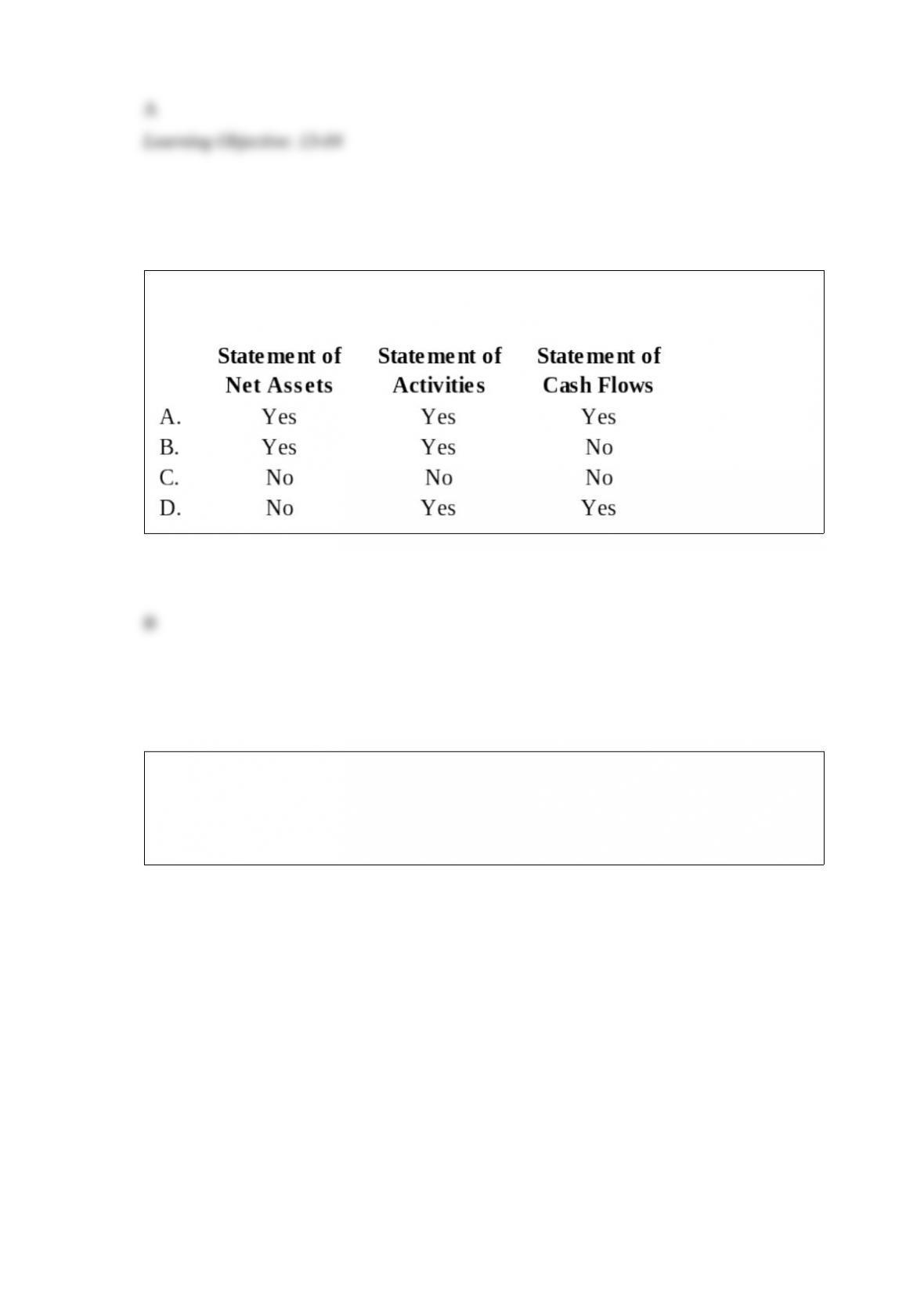

Government-wide financial statements prepared for a municipality include the

following:

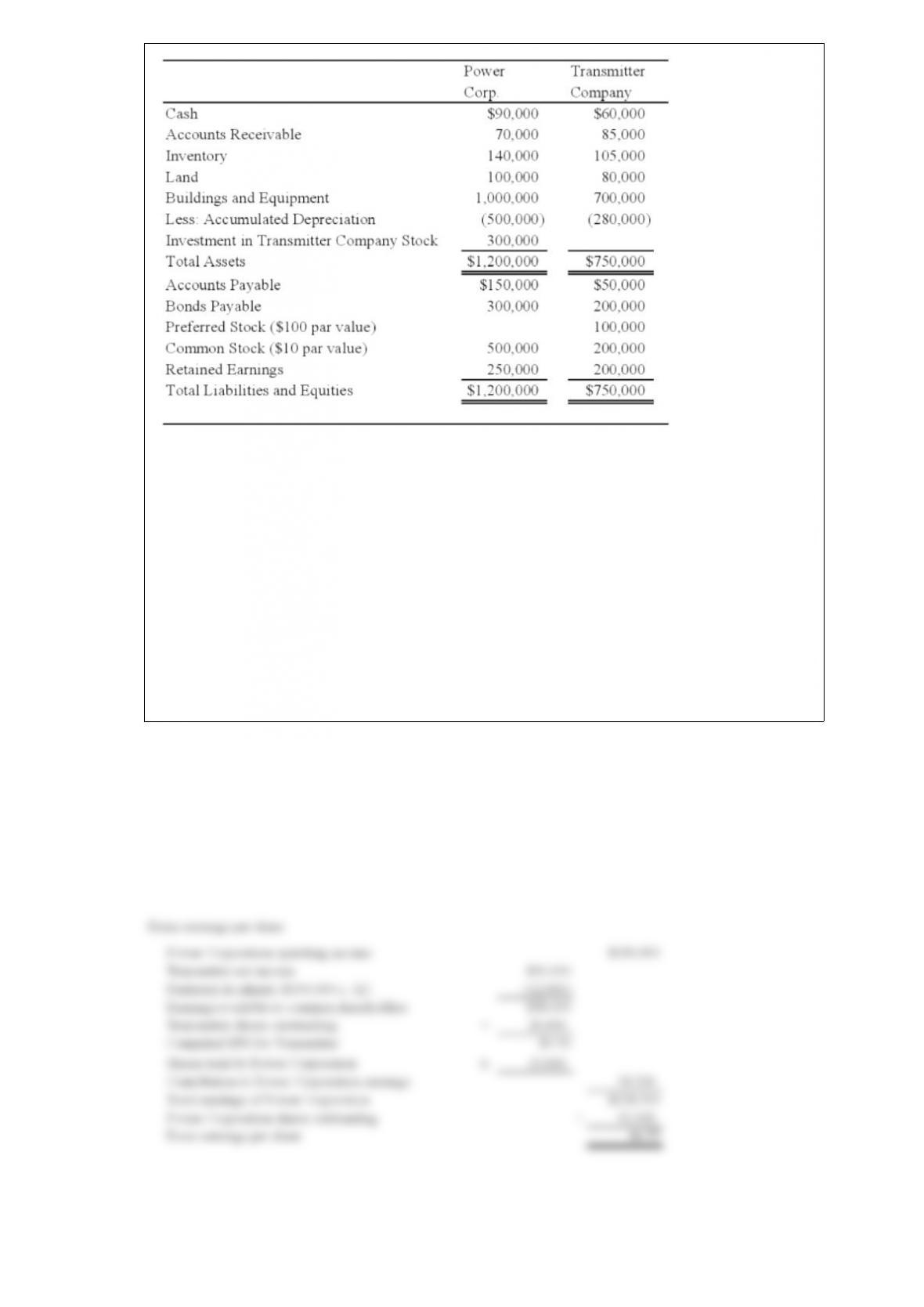

Power Corporation owns 75 percent of Transmitter Company’s common stock. At the

date of acquisition the fair value of the noncontrolling interest was equal to the book

value of Transmitter Company’s common stock. The following balance sheet data are

presented for December 31, 20X8:

Transmitter reported net income of $90,000 in 20X8 and paid dividends of $30,000. Its

bonds have an annual interest rate of 10 percent and are convertible into 12,000

common shares. Its preferred shares pay a 12 percent annual dividend and convert into

5,000 shares of common stock. In addition, Transmitter has warrants outstanding for

12,000 shares of common stock at $15 per share. The 20X8 average price of

Transmitter common shares was $25.

Power reported income of $180,000 from its own operations for 20X8 and paid

dividends of $40,000. Its 9 percent bonds convert into 8,000 shares of its common

stock. The companies file separate tax returns and are subject to income taxes of 40

percent.

Required:

Compute basic and diluted earnings per share for the consolidated entity for 20X8.

On January 1, 20X4, Timber Company acquired 25% of Johnson Company’s common

stock at underlying book value of $200,000. Johnson has 80,000 shares of $10 par

value, 6 percent cumulative preferred stock outstanding. No dividends are in arrears.

Johnson reported net income of $270,000 for 20X4 and paid total dividends of

$140,000. Timber uses the equity method to account for this investment.

Based on the preceding information, what amount would be reported by Timber

Company as the balance in its investment account on December 31, 20X4?

A. $200,000

B. $220,500

C. $232,500

D. $255,500

In the absence of other evidence, common stock ownership of between 20 and 50

percent is viewed as indicating that the investor is able to exercise significant influence

over the investee. What are some of the other factors that could constitute evidence of

the ability to exercise significant influence?

Phips Co. purchases 100 percent of Sips Company on January 1, 20X2, when Phips’

retained earnings balance is $320,000 and Sips’ is $120,000. During 20X2, Sips reports

$20,000 of net income and declares $8,000 of dividends. Phips reports $125,000 of

separate operating earnings plus $20,000 of equity-method income from its 100 percent

interest in Sips; Phips declares dividends of $35,000.

Based on the preceding information, what is Phips’ post-closing retained earnings

balance on December 31, 20X2?

A. $305,000

B. $410,000

C. $430,000

D. $465,000

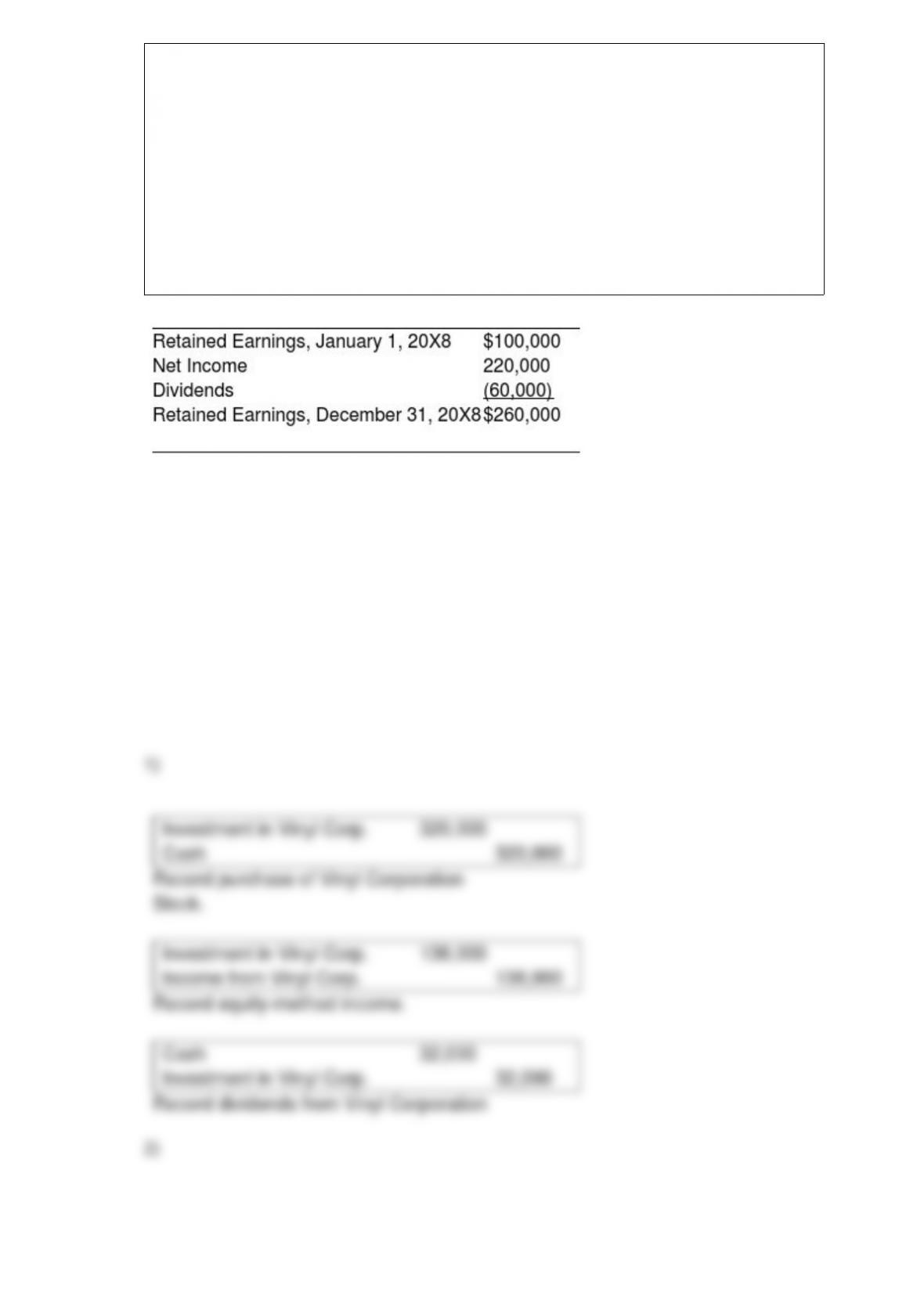

For the first quarter of 20X8, Vinyl Corporation reported sales of $150,000 and

operating expenses of $100,000, and paid dividends of $20,000. Vinyl Company

operates on a calendar-year basis. On April 1, 20X8, Signature Corporation acquired 80

percent of Vinyl’s common stock for $320,000. At that date, the fair value of the

noncontrolling interest was $80,000, and Vinyl had 20,000 shares of $5 par common

stock outstanding, originally issued at $12 per share. The differential is related to

goodwill. On December 31, 20X8, the management of Signature Corporation reviewed

the amount attributed to goodwill as a result of its acquisition of Vinyl common stock

and concluded that goodwill was not impaired. Vinyl’s retained earnings statement for

the full year 20X8 appears as follows:

Signature uses the fully adjusted equity method in accounting for this investment:

Required:

1) Prepare all entries that Signature would have recorded in accounting for its investment

in Vinyl during 20X8.

2) Present all consolidating entries needed in a worksheet to prepare a complete set of

consolidated financial statements for the year 20X8.

Alpha Company acquired 100 percent of the voting common shares of Gamma

Corporation by issuing bonds with a par value and fair value of $200,000. Immediately

prior to the acquisition, Alpha reported total assets of $600,000, liabilities of $370,000,

and stockholders’ equity of $230,000. At that date, Gamma reported total assets of

$500,000, liabilities of $300,000, and stockholders’ equity of $200,000. Included in

Gamma’s liabilities was an account payable to Alpha in the amount of $50,000, which

Alpha included in its accounts receivable.

Based on the preceding information, what amount of stockholders’ equity was reported

in the consolidated balance sheet immediately after acquisition?