Chapter 4 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES ACQUIRED AT MORE THAN BOOK

VALUE

CHAPTER 4

CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES ACQUIRED

AT MORE THAN BOOK VALUE

IMPORTANT NOTE TO INSTRUCTORS

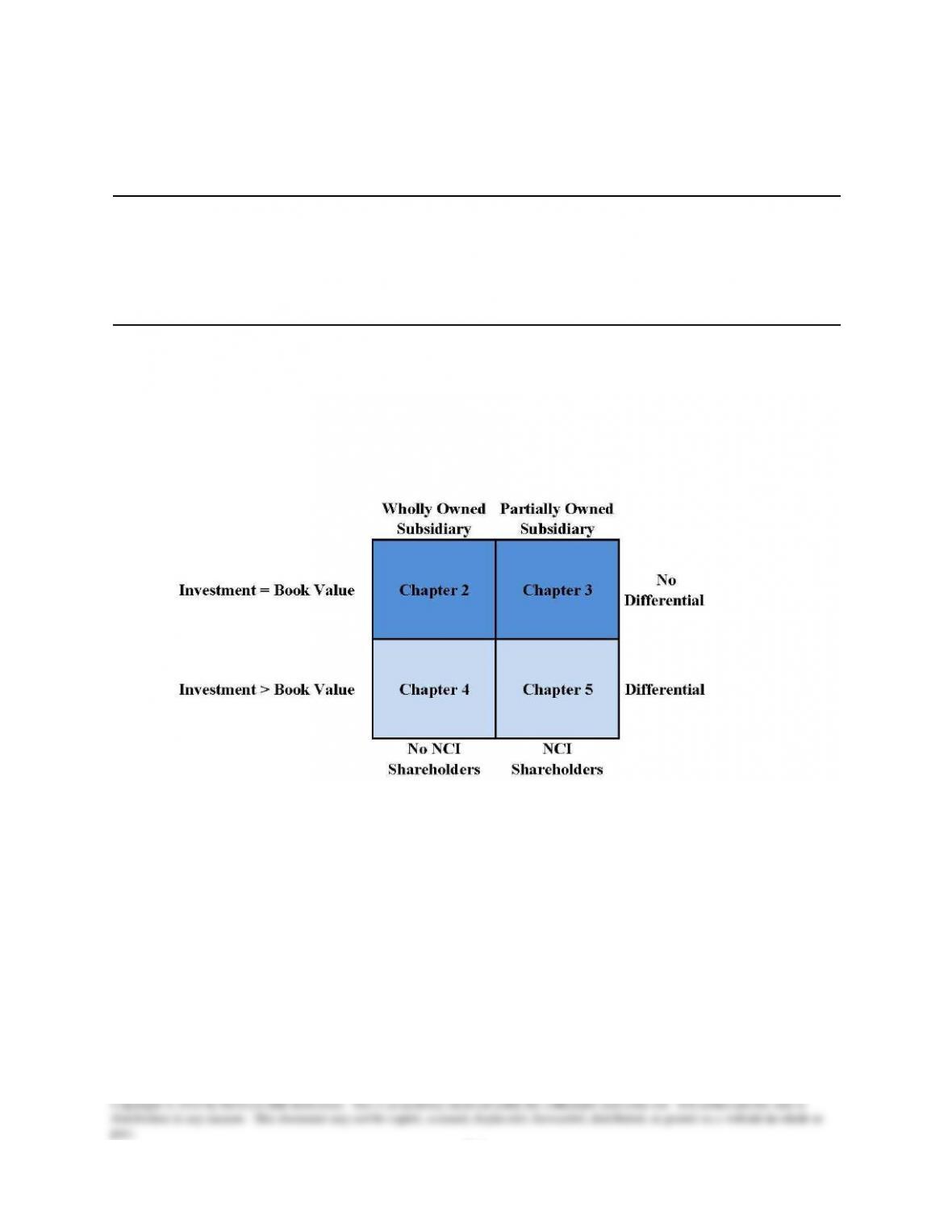

The 11th edition uses a building block approach to our coverage of consolidation in

chapters 2 through 5. Chapter 2 introduces our coverage of consolidation in the most basic

setting when the subsidiary is either created or purchased at an amount equal to the book value of

the subsidiary’s underlying net assets.

Chapter 3 explains how the basic consolidation process changes when the parent

company owns less than 100 percent of the subsidiary. Chapter 4 shows how the consolidation

process differs when the parent company acquires the subsidiary for an amount greater (or less)

than the book value of the subsidiary’s net assets. Finally, Chapter 5 presents the most complex

consolidation scenario (where the parent owns less than 100 percent of the subsidiary’s

outstanding voting stock and the acquisition price is not equal to the book value of the

subsidiary’s net assets). In order to facilitate this new approach, we emphasize that this edition

includes consolidation entries used in consolidation to facilitate the elimination of the investment

in a subsidiary in two steps: (1) first the book value portion of the investment and income from

the subsidiary are eliminated and (2) then the differential portion of the investment and income

from subsidiary are eliminated with separate entries. We believe that this approach is more

intuitive for students.

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES

2

OVERVIEW OF CHAPTER 4

Chapter 4 focuses on the preparation of the consolidated financial statements for a parent

and wholly owned subsidiaries acquired at more than book value. It first explains conceptually

how the consolidation process differs when there is a positive differential and shows the proper

accounting for a positive differential under the equity method. It then discusses consolidation

immediately following acquisition and one year after the acquisition for a subsidiary acquired at

more than book value.

Chapter 4 also introduces the treatment of intercorporate receivables and payables and

briefly explains the criteria for push-down accounting and its applications. Push-down

accounting is illustrated in more detail in Appendix 4A.

LEARNING OBJECTIVES

When students finish studying this chapter, they should be able to:

LO 4-1 Understand and make equity-method journal entries related to the differential.

LO 4-2 Understand and explain how consolidation procedures differ when there is a

differential.

LO 4-3 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex positive differential at the acquisition

date.

LO 4-4 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex bargain-purchase differential.

LO 4-5 Prepare equity-method journal entries, consolidation entries, and the consolidation

worksheet for a wholly owned subsidiary when there is a complex positive

differential.

LO 4-6 Understand and explain the elimination of basic intercompany transactions.

LO 4-7 Understand and explain the basics of push-down accounting.

SYNOPSIS OF CHAPTER 4

Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

How Much Work Does It Really Take to Consolidate? Ask the People Who Do It at

Disney

LO 4-1 Understand and make equity method journal entries related to the differential.

Dealing with the Differential

The Difference between Acquisition Price and Underlying Book Value

Additional Considerations

Disney’s 2006 Pixar Acquisition

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES

3

Disney’s 2012 Lucasfilm Acquisition

LO 4-2 Understand and explain how consolidation procedures differ when there is a

differential.

Consolidation Procedures for Wholly Owned Subsidiaries Acquired at More than Book

Value Treatment of a Positive Differential

LO 4-3 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex positive differential at the acquisition

date.

Illustration of Treatment of a Complex Differential

LO 4-4 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex bargain-purchase differential.

100 Percent Ownership Acquired at Less than Fair Value of Net Assets

Illustration of Treatment of Bargain-Purchase Differential

LO 4-5 Prepare equity-method journal entries, consolidation entries, and the consolidation

worksheet for a wholly owned subsidiary when there is a complex positive

differential.

Consolidated Financial Statements – 100 Percent Ownership Acquired a More than Book

Value

Initial Year of Ownership

Second Year of Ownership

LO 4-6 Understand and explain the elimination of basic intercompany transactions.

Intercompany Receivables and Payables

LO 4-7 Understand and explain the basics of push-down accounting.

Push-Down Accounting

Appendix 4A

Push-Down Accounting Illustrated

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES

4

NOTES ON POWERPOINT SLIDES

We have attempted to provide PowerPoint slides that will be useful to a broad set of users. Since

instructors often have different styles and preferences, we have attempted to include slides that

will accommodate different approaches and that can be adapted to classes with different levels of

preparation. For example, some instructors prefer to introduce the material before students have

read the chapter. We have tried to facilitate these types of introductory discussions by including

slides that replicate key points from the chapter. Other instructors expect students to have read

the chapter and attempted homework problems before coming to class. As a result, they may not

find it useful to review all of the topics in the chapter or to include slides that simply review

many of the details they expect students to study before class. However, instructors following

this approach often like to use sample exercises and problems built into the slides that allow

them to have extended discussions or to facilitate group interaction in class.

If instructors elect to spend two class periods on the same subject, they might find a combination

of both styles to be useful by first introducing foundational material before students have read

the chapter and studied the topic, followed by an extended discussion the next class period after

students have read the chapter and attempted homework problems.

We have tried to develop slides that can facilitate a flexible approach to allow instructors to

select the slides that best match their objectives and style for class discussions. This is the reason

we are including over 100 slides for some chapters in the text. We do not expect all instructors

to use all slides, but the slide files should help support different teaching approaches and allow

instructors to select the subset of slides that best matches their specific discussion objectives.

The slides are organized by learning objective. We have included a slide at the beginning of

each learning objective to show where the new material begins. Instructors may or may not want

to use these learning objective slides in class. We provide them primarily as a way of organizing

the material. We also include short multiple choice questions at the end of most learning

objectives. Some instructors find it useful to pause periodically during class to assess students’

level of understanding. For this reason, we include several “practice quiz questions” that can be

used throughout class discussions to engage students, help them focus on key points, or to

facilitate group interaction. Finally, we provide longer exercises and problems that many

instructors find useful in assessing understanding and encouraging group learning.

LO 4-1 Understand and make equity-method journal entries related to the differential.

• Slides 3-17 introduce concepts related to situations in which a differential is present.

• Slides 18-23 introduce the Pepper/Salt example, which we carry throughout chapters

4 and 5. These slides help students understand (using a concrete example) how a

differential affects the preparation of the consolidated balance sheet and income

statement.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 4-2 Understand and explain how consolidation procedures differ when there is a

differential.

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES

5

• Slides 27-43 discuss concepts related to LO2.

• Slide 27 once again reminds students of where we are in the “big picture” of learning

to account for consolidation.

• Slides 28-29 again help students to remember that the acquisition price includes three

different components.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students.

LO 4-3 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex positive differential at the acquisition

date.

• Slides 47-57 introduce the concepts in LO3.

• Slides 58-65 use the Prince/She-Ra example to illustrate how the acquisition price can

be viewed as paying for three separate components: the book value of net assets,

excess value associated with identifiable assets and liabilities, and goodwill. Note that

in this example the She-Ra had existing goodwill on its books from a prior acquisition

of another subsidiary. Slide 26 indicates that one way to view this situation is to

assume that it is difficult to correctly assess the value of old goodwill. One approach

is to assume it is worth zero and use the estimates of the fair values of all other assets

and liabilities to calculate a new aggregate goodwill “residual” amount. Obviously,

the new goodwill calculated would also include the old goodwill number from the

prior acquisition. Some instructors may want to assume that if She-Ra has correctly

tested for goodwill impairment in prior years that it is equal to exactly $110,000. In

this case, the new goodwill amount associated with this acquisition would be

$230,000 instead of $340,000. The end result is the same. The total amount in

goodwill after the completion of this acquisition is $340,000.

• In particular, slides 27-29 help students to see how the elimination of the book value

component and the excess value components takes place.

• Slides 63-65 once again walk students through the optional accumulated depreciation

entry. The point is that by using the accumulated depreciation consolidation entry, the

PP&E will appear on the consolidated financial statements as if these assets has been

acquired at their fair values on the acquisition date.

• Slides 66-76 return to the Pepper/Salt example to slowly walk students through the

consolidation on the acquisition date. Since the investment in Salt is acquired on the

balance sheet date, no income has been earned. Thus, there is no need for a

consolidated income statement or statement of retained earnings. We find that the

preparation of a consolidated balance sheet allows students to understand one aspect

of the differential (the balance sheet side) before getting too deep in the income

statement effects. We find it useful to provide full-page handouts (or an Excel

Template) for slides 33-34 so that students can walk through the analyses in small

groups. We often go through slides 68-76 slowly, pausing to allow students to work

one step at a time before showing them correct answers. We then have them complete

the worksheet while working in a small group. If we are short on time, we opt to

quickly go through this worksheet with the entire class and save “group time” for the

“full–blown” worksheet at the end of this set of slides.

Chapter 04 – CONSOLIDATION OF WHOLLY OWNED SUBSIDIARIES

6

LO 4-4 Make calculations and prepare consolidation entries for the consolidation of a wholly

owned subsidiary when there is a complex bargain-purchase differential.

• Slides 80-89 help students visualize how a bargain purchase would normally be just

the opposite of a positive differential situation.

LO 4-5 Prepare equity-method journal entries, consolidation entries, and the consolidation

worksheet for a wholly owned subsidiary when there is a complex positive

differential.

• Slides 93-106 introduce the concepts related to LO5.

• Slides 107-124 complete the Pepper/Salt example at the end of the first full year. This

is a critical example for helping students to understand all of the detail for the non-

push-down accounting for a positive differential. We like to provide a full page

handout of slides 109, 113, and 124 so students can work through the problem in

class or in small groups. We tend to have students work one step ahead of the slides

and reveal one portion of the solution at a time to make sure they stay on track. After

working through all of the foundational steps, we have students complete the

consolidation worksheet in their groups (and sometimes have them turn in their

solution as a “group quiz”). Note that the book value calculations on slide 54 lead

directly to the basic consolidation entry. The bottom row of the excess value

calculations on slide 58 leads to the excess value reclassification entry and the middle

row of the excess value calculations leads to the amortized excess value

reclassification entry.

LO 4-6 Understand and explain the elimination of basic intercompany transactions.

• Slides 126-129 provide a brief introduction to the elimination of intercompany

transactions. Some instructors like to introduce simple reciprocal accounts (like

payables and receivables) into their chapter 4 worksheets. These slides are useful in

illustrating this process. Other instructors skip this material here and provide a more

detailed introduction to intercompany transactions at the beginning of chapter 6.

LO 4-7 Understand and explain the basics of push-down accounting.

• Slides 135-140 summarize push down accounting.

TEACHING IDEA

1. Students could be asked to select an example of a business combination that has occurred

during the past year and was reported in The Wall Street Journal or the business section

of a major newspaper. The company could be selected by the students utilizing a key

word search of a business news data base available at their university or college. Students

should then research and report details regarding the business combinations, such as type

of combination, type of consideration given by the acquiring entity, number of shares

issued (if applicable), ownership percentage acquired, size of company, etc. Students

should be encouraged to utilize business news data bases, SEC filings, and company Web

sites to gather this information.