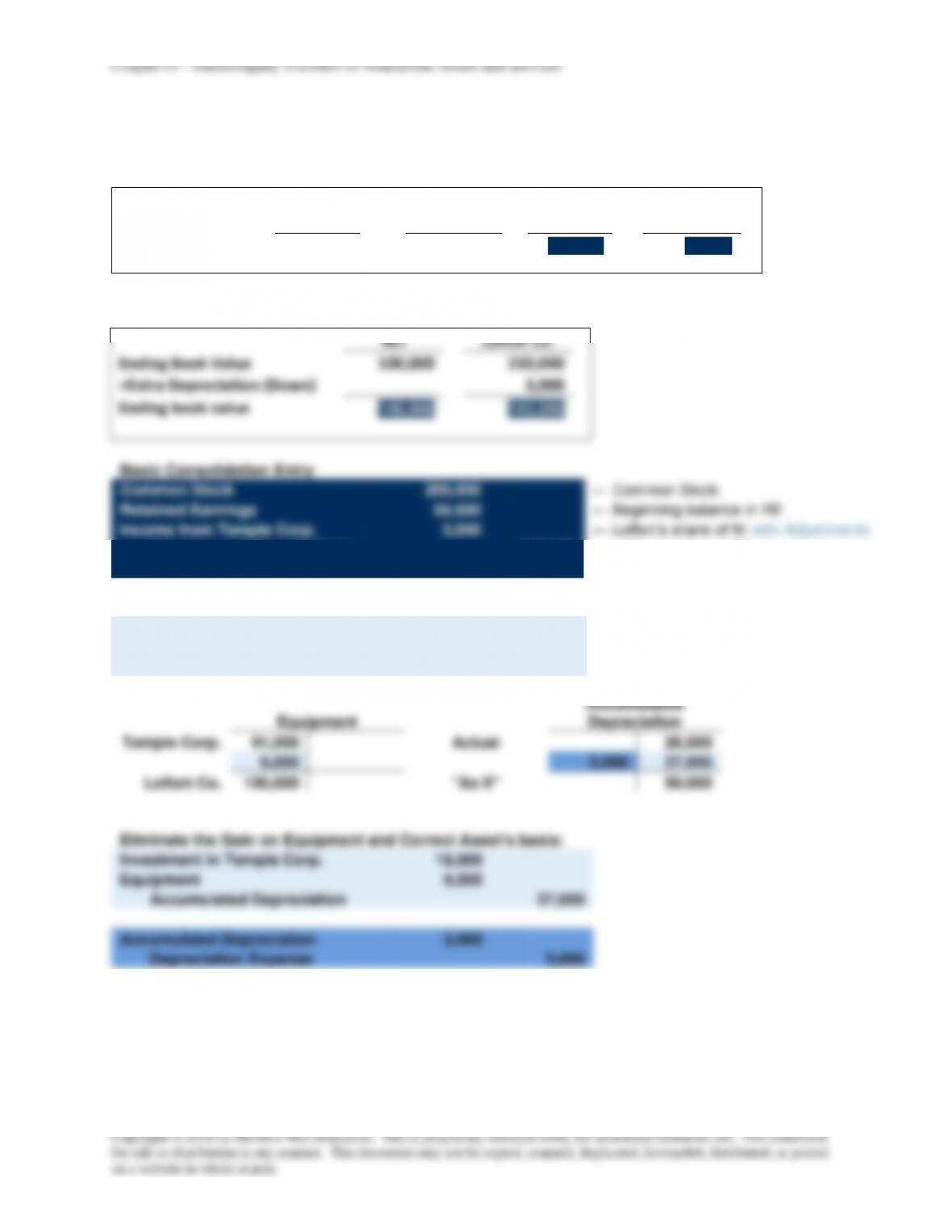

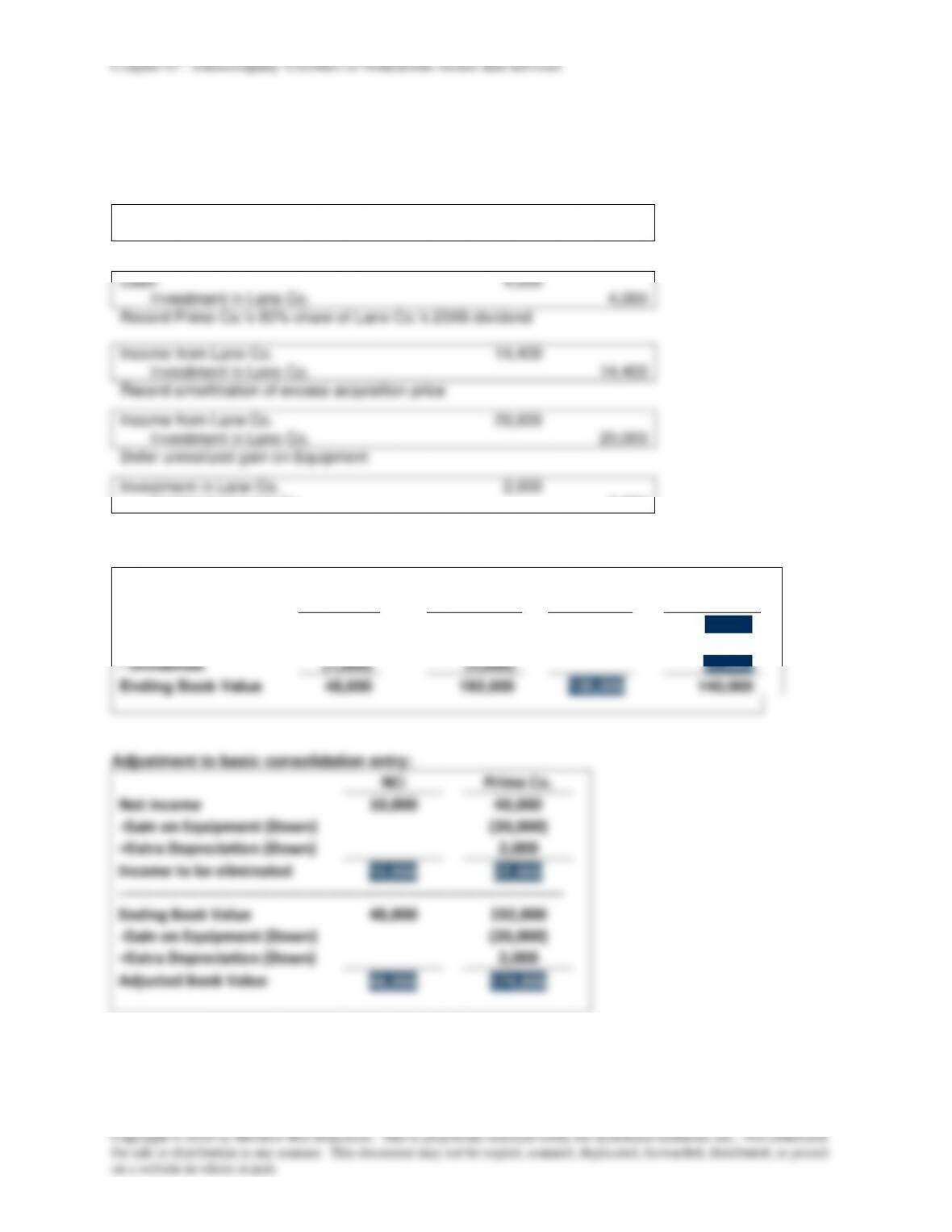

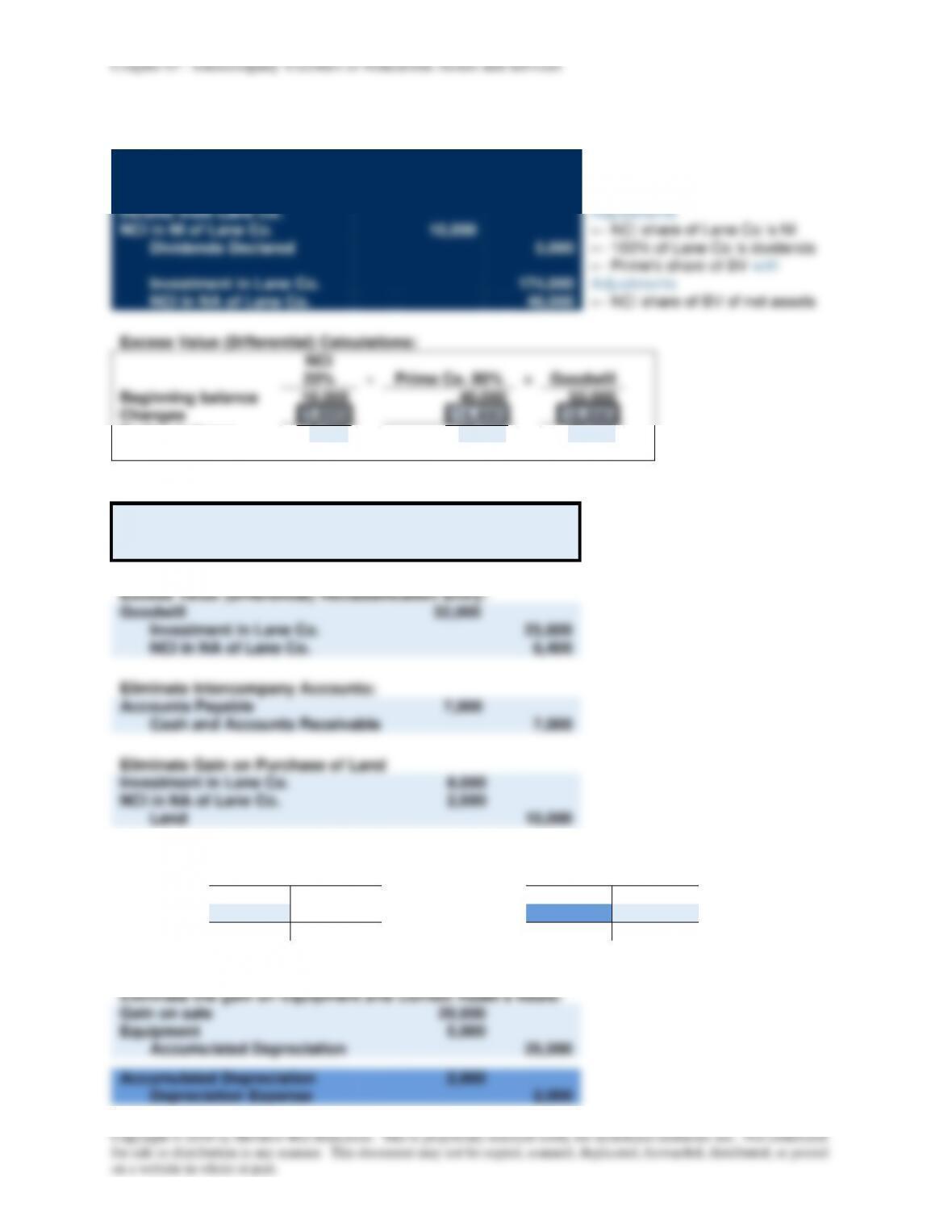

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

P7–25 (continued)

b.

Consolidated net income for 20X4 is $304,000:

Bold Corporation’s operating income

$234,000

Toll Corporation’s net income

94,400

Amortization of differential ($44,000 / 10 years)

(4,400)

Unrealized profit on building

(20,000)

Consolidated net income

$304,000

c.

Income assigned to controlling interest is $286,500:

Consolidated net income

$304,000

Income assigned to noncontrolling interest

(17,500)

Income assigned to controlling interest

$286,500

Alternate computation:

Operating income of Bold

$234,000

Income from Toll:

Net income of Toll

$94,400

Unrealized profit on building

(20,000)

Amortization of differential

(4,400)

Realized income

$70,000

Portion of ownership held

x 0.75

52,500

Income to controlling interest

$286,500

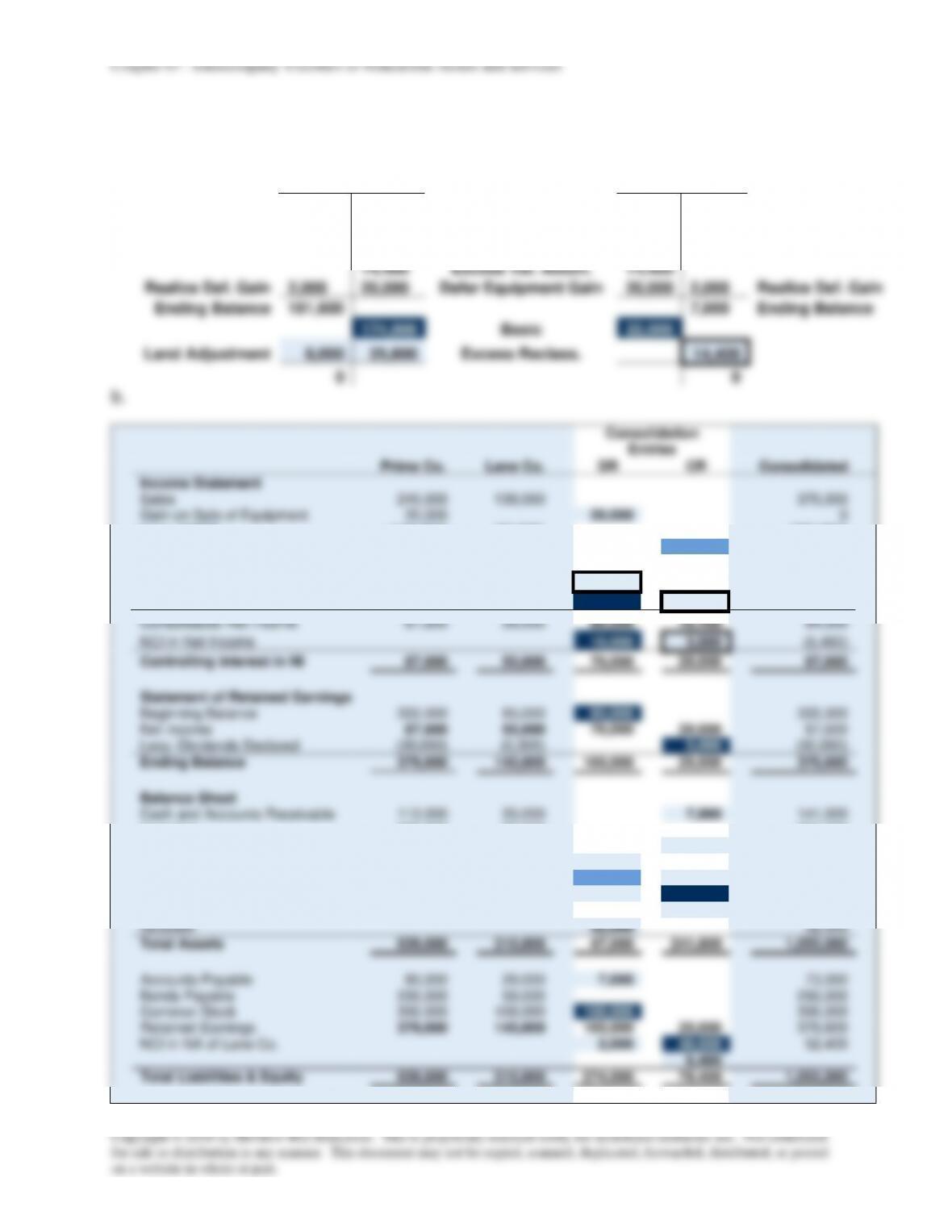

P7-26 Transfer of Asset from One Subsidiary to Another

Bugle

Cook Products

Consolidated

Corporation

Corporation

Entity

Depreciation expense

$ —

$ 3,000

$ 2,000

Fixed assets — Warehouse

—

45,000

40,000

Accumulated depreciation

—

3,000

12,000

Gain on sale of warehouse

15,000

—

—