During its inception, Devon Company purchased land for $100,000 and a building for

$180,000. After exactly 3 years, it transferred these assets and cash of $50,000 to a

newly created subsidiary, Regan Company, in exchange for 15,000 shares of Regan’s

$10 par value stock. Devon uses straight-line depreciation. Useful life for the building

is 30 years, with zero residual value. An appraisal revealed that the building has a fair

value of $200,000.

Based on the information provided, at the time of the transfer, Regan Company should

record:

A. Building at $180,000 and no accumulated depreciation.

B. Building at $162,000 and no accumulated depreciation.

C. Building at $200,000 and accumulated depreciation of $24,000.

D. Building at $180,000 and accumulated depreciation of $18,000.

The computation of a safe installment payment for the XYZ partnership resulted in only

partner Z receiving cash. Which of the following statements is correct?

I. Partner Z lent the partnership cash, and the partnership had to pay back the loan to Z

before distributing cash to X and Y.

II. After assuming all noncash assets were potentially worthless and that assumed

capital deficits created in X’s and Y’s capital balances were losses to be allocated to Z;

Z’s capital balance was the only capital balance left with a credit.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

In the RST partnership, Ron’s capital is $80,000, Stella’s is $75,000, and Tiffany’s is

$50,000. They share income in a 3:2:1 ratio, respectively. Tiffany is retiring from the

partnership. Each of the following questions is independent of the others.

Refer to the above information. Tiffany is paid $60,000, and no goodwill is recorded.

What is the Ron’s capital balance after Tiffany withdraws from the partnership?

A. $74,000

B. $71,000

C. $75,000

D. $86,000

All of the following are differences between international standards and U.S. GAAP

regarding operating segments, except:

A. IFRS requires disclosures about geographical segments, not business segments.

B. IFRS requires two different bases of segmentation, a primary basis and a secondary

basis.

C. IFRS required more disclosure for primary segments

D. The amounts disclosed under IFRS are based on the same accounting policies as the

financial statements, not based on amounts reported to the chief operating decision

maker.

Assume that a private university collects tuition and fees at the beginning of summer

school, in which two weeks are offered in the first fiscal year and the remaining six

weeks are offered in the second fiscal year. According to the approach recommended by

the National Association of College and University Business Officers (NACUBO), the

university would:

A. record the collections as a debit to Cash and a credit to Deferred Revenue for the

entire amount of the collections.

B. record the collections as a debit to Cash and a credit to Restricted current revenue for

the entire amount of the collections.

C. account for the entire tuition and fees as revenue in the first fiscal period.

D. recognize revenue in the first fiscal period for two-eighths of the tuition and fees and

record six-eighths of the collections as a deferred revenue.

If the restatement method for a foreign subsidiary involves remeasuring from the local

currency into the functional currency, then translating from functional currency to U.S.

dollars, the functional currency of the subsidiary is:

I. U.S. dollar.

II. Local currency unit.

III. A third country’s currency.

A. I

B. III

C. II

D. Either I or II

Using the fully adjusted equity method, an intercompany gain on an upstream sale of

land is:

A. recognized by the parent and the deferral is shared between the controlling and

noncontrolling stockholders of the subsidiary.

B. recognized by the subsidiary and the deferral is shared between the controlling and

noncontrolling stockholders of the subsidiary.

C. deferred by the subsidiary until the land is sold to an entity outside the consolidated

group.

D. recognized by the subsidiary and the deferral is completely allocated to the

controlling stockholders of the subsidiary.

On March 15, 20X9, Clarion Company paid property taxes of $60,000 on its factory

building for calendar year 20X9. On July 1, 20X9, Clarion made $40,000 in

unanticipated repairs to its machinery. The repairs will benefit operations for the

remainder of the calendar year. What total amount of these expenses should be included

in Clarion’s quarterly income statement for the three months ended September 30,

20X9?

A. $55,000

B. $15,000

C. $35,000

D. $40,000

The general fund of Loveland ordered a new fire truck on November 12, 20X8, for

$150,000. The order was appropriately encumbered on this date. Loveland received the

fire truck on January 15, 20X9, and issued a voucher to the manufacturer for $148,600.

Loveland uses the calendar year for reporting, and outstanding encumbrances at

December 31, 20X8, are lapsing. On January 15, 20X9, the general fund of Loveland

should debit:

A. Fund Balance—assigned for Encumbrances for $148,600.

B. Expenditures for $148,600.

C. Expenditures-20X8 for $148,600.

D. Encumbrances for $148,600.

The governing board of a hospital operated by a religious organization designated

$3,000,000 of cash to be used for plant expansion. The cash was invested in stocks and

bonds which earned $250,000 of dividend and interest income. The income from

investments should be reported on the hospital’s statement of operations as an increase

in:

A. temporarily restricted net assets.

B. operating income.

C. either temporarily restricted net assets or unrestricted net assets, depending upon the

nature of the governing board’s restrictions.

D. fund balance in the general fund.

Big Corporation receives management consulting services from its 92 percent owned

subsidiary, Small Inc. During 20X7, Big paid Small $125,432 for its services. For the

year 20X8, Small billed Big $140,000 for such services and collected all but $7,900 by

year-end. Small’s labor cost and other associated costs for the employees providing

services to Big totaled $86,000 in 20X7 and $121,000 in 20X8. Big reported

$2,567,000 of income from its own separate operations for 20X8, and Small reported

net income of $695,000.

Based on the preceding information, what amount of consolidated net income should be

reported in 20X8?

A. $3,262,000

B. $4,050,000

C. $3,254,100

D. $3,122,000

Which of the following statements concerning Form 10-Q is NOT true?

A. It is filed for all four quarters.

B. It is the quarterly report to the SEC.

C. It contains an update on significant matters occurring since the last quarter.

D. It includes comparative financial statements prepared in accordance with APB 28.

Clark Co. had the following transactions with affiliated parties during 20X1:

•Sales of $60,000 to Dean, Inc., with $20,000 gross profit. Dean had $15,000 of this

inventory on hand at year end. Clark owns a 15% interest in Dean and does not

exert significant influence.

•Purchases of raw materials totaling $240,000 from Kent Corp., a wholly-owned

subsidiary. Kent’s gross profit on the sale was $48,000. Clark had $60,000 of this

inventory remaining on December 31, 20X1.

Before consolidating entries, Clark had consolidated current assets of $320,000. What

amount should Clark report in its December 31, 20X1, consolidated balance sheet for

current assets?

A. $303,000

B. $320,000

C. $317,000

D. $308,000

Quid Corporation acquired 75 percent of Pro Company’s common stock on December

31, 20X6. Goodwill (attributable to Quid’s acquisition of Pro shares) of $300,000 was

reported in the consolidated financial statements at December 31, 20X6. Parent

company approach was used in determining this amount. What is the amount of

goodwill to be reported under proprietary theory approach?

A. $300,000

B. $400,000

C. $150,000

D. $100,000

The items below are associated with the Securities and Exchange Commission.

Describe or explain each item as concisely as possible.

(a) Customary Review

(b) Comment Letter

(c) “Red Herring” Prospectus

(d) “Tombstone Ad”

(e) Financial Reporting Releases

(f) Staff Accounting Bulletins

(g) Accounting and Auditing Enforcement Releases

(h) Management’s Discussion and Analysis

Park Co.’s wholly-owned subsidiary, Schnell Corp., maintains its accounting records in

German marks. Because all of Schnell’s branch offices are in Switzerland, its functional

currency is the Swiss franc. Remeasurement of Schnell’s 20X1 financial statements

resulted in a $7,600 gain, and translation of its financial statements resulted in an

$8,100 gain. What amount should Park report as a foreign exchange gain in its income

statement for the year ended December 31, 20X1?

A. $15,700

B. $0

C. $8,100

D. $7,600

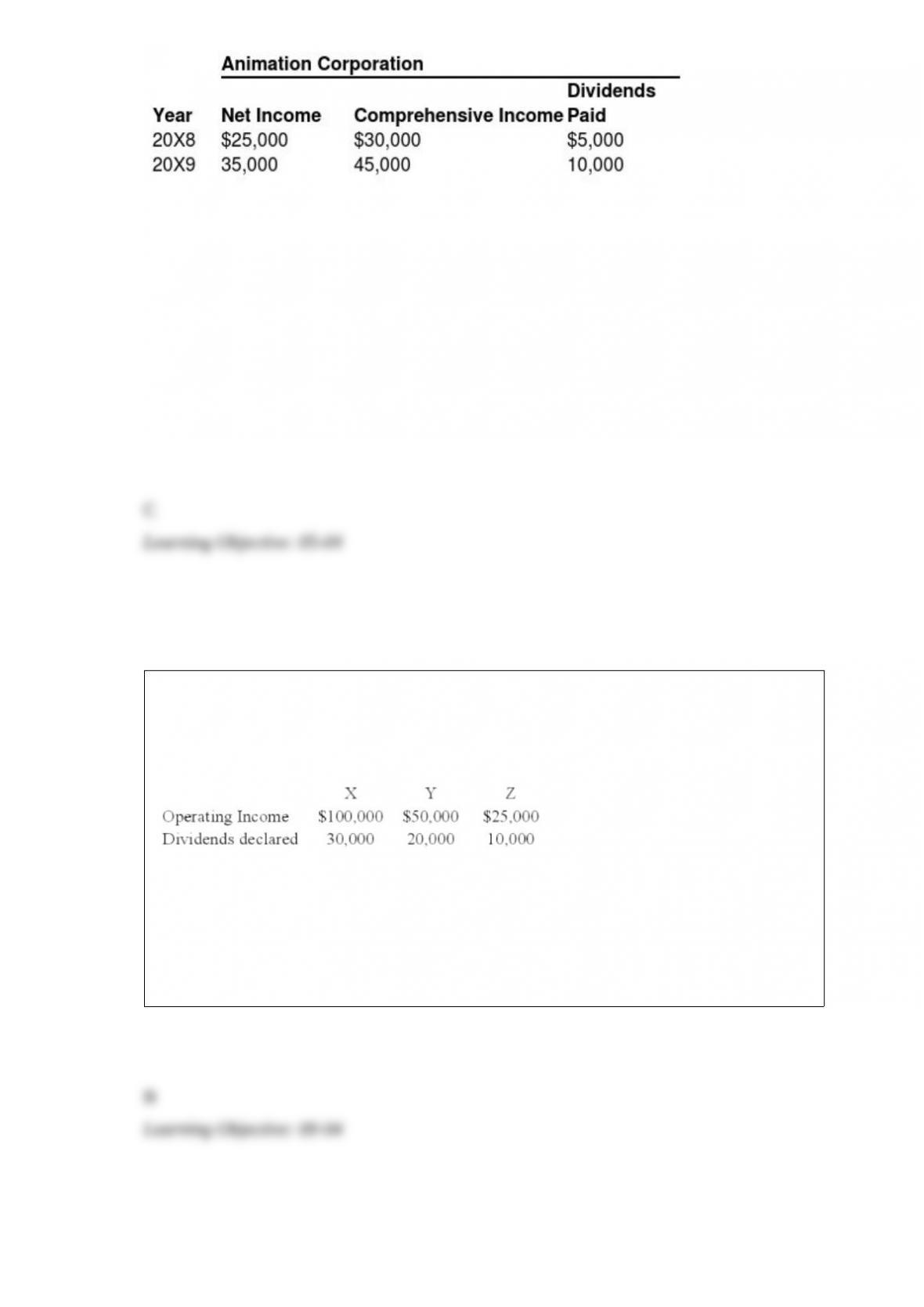

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company’s

common stock for $280,000 cash. At that date, Animation reported common stock

outstanding of $200,000 and retained earnings of $100,000, and the fair value of the

noncontrolling interest was $70,000. The book values and fair values of Animation’s

assets and liabilities were equal, except for other intangible assets which had a fair

value $50,000 greater than book value and an 8-year remaining life. Animation reported

the following data for 20X8 and 20X9:

Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

Based on the preceding information, what is the amount of consolidated comprehensive

income reported for 20X9?

A. $145,000

B. $135,000

C. $138,750

D. $128,750

X Corporation owns 80 percent of Y Corporation’s common stock and 40 percent of Z

Corporation’s common stock. Additionally, Y Corporation owns 35 percent of Z

Corporation’s common stock. The acquisitions were made at book values. The

following information is available for 20X8:

Based on the information provided, what amount of consolidated net income will X

Corporation report for 20X8?

A. $148,750

B. $175,000

C. $150,000

D. $158,750

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Form 10-K

The Greenpath Corporation’s (Greenpath) balance sheet shows assets of $800,000 and

liabilities of $300,000. In addition, the company has an unrecorded intangible asset with

a value of $100,000 and a 10-year useful life. On January 1, 20X1, the Montana

Corporation acquires 30% of Greenpath’s outstanding stock for $290,000. In 20X1,

Greenpath reported net income of $90,000 and paid dividends of $20,000. In 20X2,

Greenpath reported net income of $110,000 and paid dividends of $50,000. If the equity

method is being applied to this investment, what is the reported balance for the

investment account at the end of 20X2?

A. $311,000

B. $302,000

C. $323,000

D $317,500

GASB 34 requires budgetary comparison schedules

A. Be reported for the general fund and each major special revenue fund with a legally

adopted budget.

B. Be reported for all proprietary funds.

C. Be reported for the permanent funds.

D. Should not be reported.

Due to an error, the general fund of Pueblo did not record an encumbrance for police

equipment which had been ordered but not received on June 30, 20X9, the end of its

fiscal year. Pueblo’s outstanding encumbrances at year-end are nonlapsing. What was

the effect of this error on the balance sheet of Pueblo’s general fund?

A. Assets are overstated.

B. Liabilities are understated.

C. Total fund balance is overstated.

D. Unassigned fund balance is overstated.

Carlisle established a motor vehicle service and maintenance fund to service and

maintain all cars and trucks owned by the town. Revenues of the fund will only come

from billings to the funds which use the motor vehicle service and maintenance fund.

What type of fund is the motor vehicle service and maintenance fund?

A. An enterprise fund.

B. A special revenue fund.

C. An expendable trust fund.

D. An internal service fund.

A “debtor-in-possession” balance sheet is prepared for a company which:

A. is having its debts restructured.

B. is undergoing a liquidation under Chapter 7.

C. is undergoing a reorganization under Chapter 11.

D. is in bankruptcy reorganization but management still controls the company.