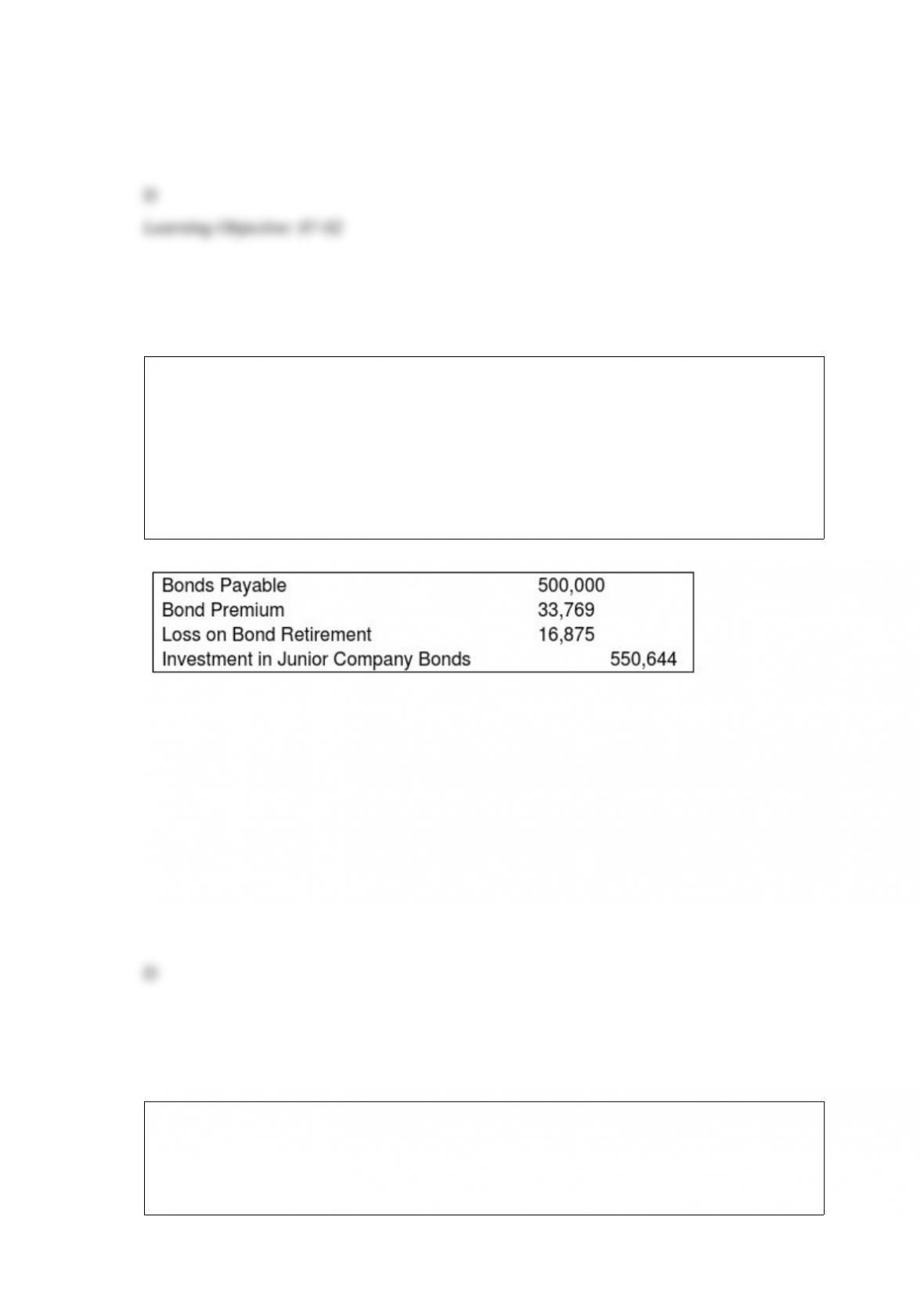

Senior Corporation acquired 80 percent of Junior Company’s voting shares on January

1, 20X8, at underlying book value. On Dec. 31, 20X8, it also purchased $500,000 par

value 8 percent Junior bonds, which had been issued on January 1, 20X5 to Partner

Corporation (unaffiliated with either Senior or Junior) at a $45,000 premium. The bonds

were originally issued with a 12-year maturity and pay interest annually on December

31. During preparation of the consolidated financial statements for December 31, 20X8,

the following consolidating entry was included in the consolidation worksheet:

Based on the information given above, what is the interest income that must be eliminated

in preparing the 20X9 consolidated financial statements?

A. $33,769

B. $27,957

C. $34,944

D. $16,894

Under Chapter 11 proceedings, what represents the fair value of the entity before

considering liabilities and approximates the amount a willing buyer would pay for the

entity’s assets?

A. Reorganization value

B. Fire sale value

C. Fresh start value

D. Excess value

ASC 805 requires contingent consideration in a business combination to be classified

as:

A. An asset

B. A liability or equity

C. An asset or equity

D. An asset or a liability

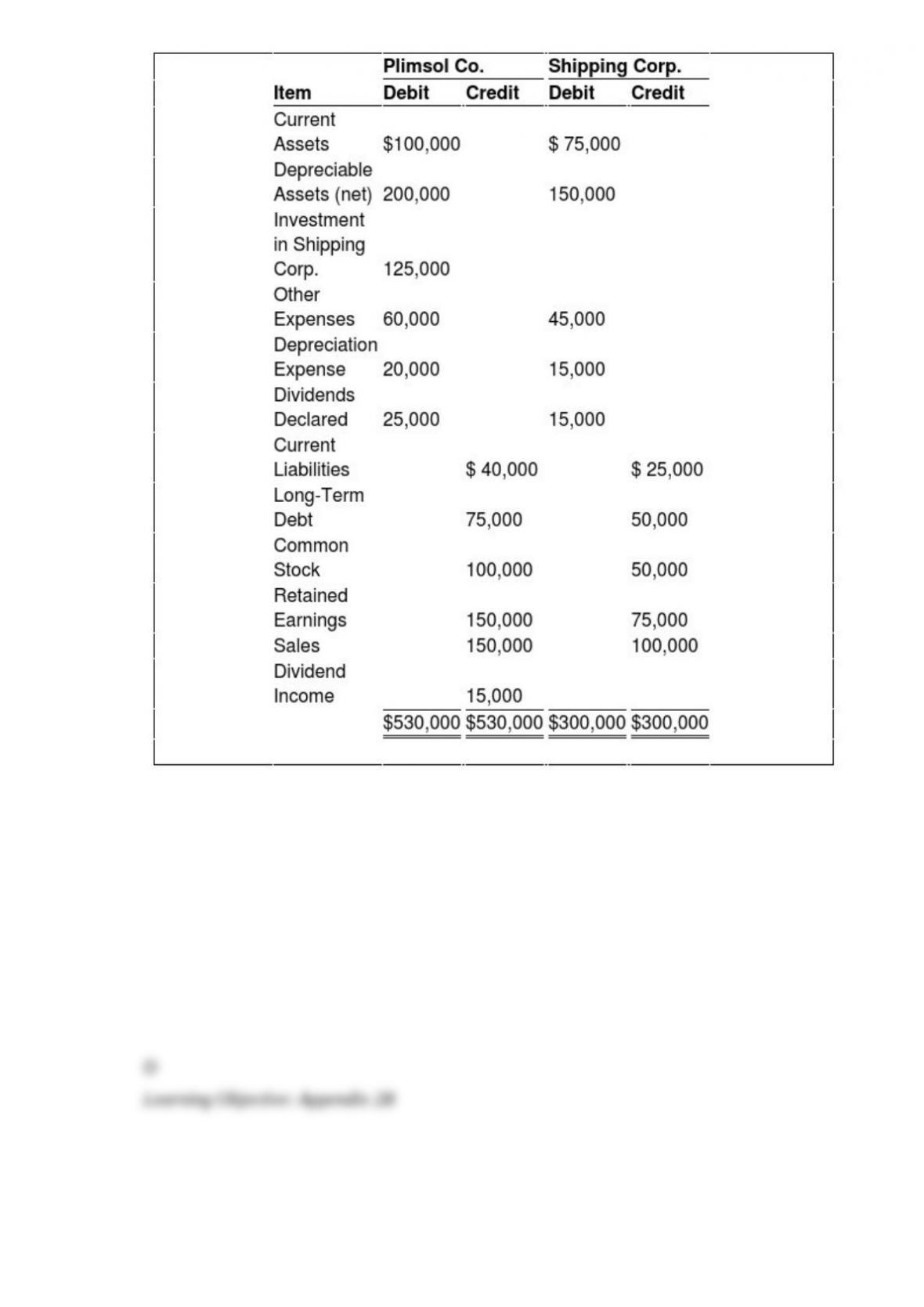

On January 1, 20X4, Plimsol Company acquired 100 percent of Shipping Corporation’s

voting shares, at underlying book value. Plimsol uses the cost method in accounting for

its investment in Shipping. Shipping’s retained earnings was $75,000 on the date of

acquisition. On December 31, 20X4, the trial balance data for the two companies are as

follows:

Based on the information provided, what amount of total liabilities will be reported in the

consolidated balance sheet prepared on December 31, 20X4?

A. $525,000

B. $115,000

C. $125,000

D. $190,000

Tanner Company, a subsidiary acquired for cash, owned equipment with a fair value

higher than the book value as of the date of combination. A consolidated balance sheet

prepared immediately after the acquisition would include this difference in:

A. goodwill.

B. retained earnings.

C. deferred charges.

D. equipment.

Which of the following observations concerning “goodwill” is NOT correct?

A. Once written down, it may be written up for recoveries.

B. It must be tested for impairment at least annually.

C. Goodwill impairment losses are recognized in income from continuing operations or

income before extraordinary gains and losses.

D. It must be reported as a separate line item in the balance sheet.

Which monthly report shows the results of the trustee’s fiduciary actions beginning at

the point the trustee accepts the debtor’s assets?

A. Statement of affairs

B. Statement of realization and liquidation

C. Statement of financial position

D. Statement of activities

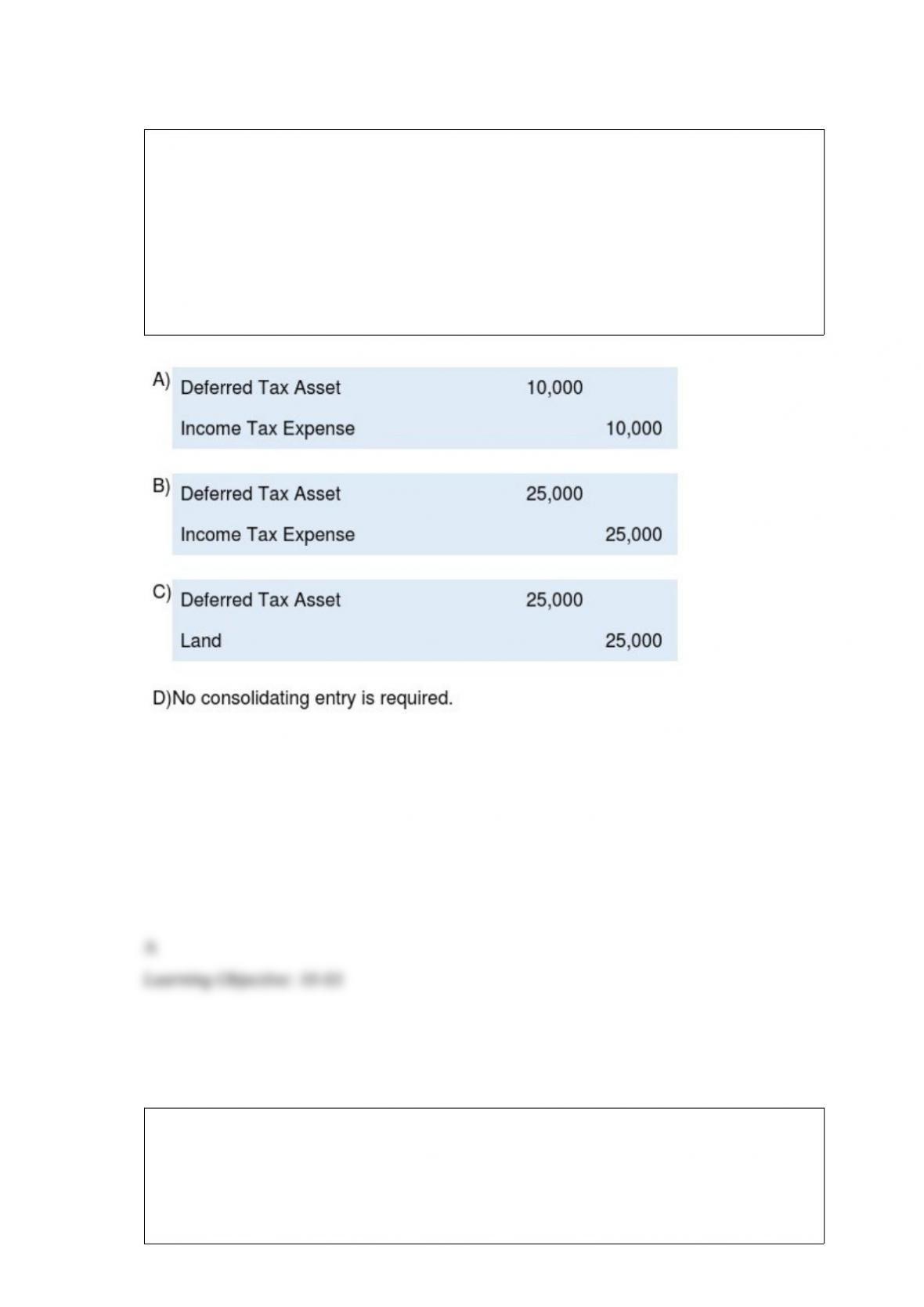

Company A holds 70 percent of the voting shares of Company B. During 20X8,

Company B sold land with a book value of $125,000 to Company A for $150,000.

Company A continues to hold the land at the end of the year. The companies file

separate tax returns and are subject to a 40 percent tax rate. Assume that Company A

uses the fully adjusted equity method in accounting for its investment in Company B.

Based on the information given, which consolidating entry relating to the intercorporate

sale of land is to be entered in the consolidation worksheet prepared at the end of

20X8?

A. Option A

B. Option B

C. Option C

D. Option D

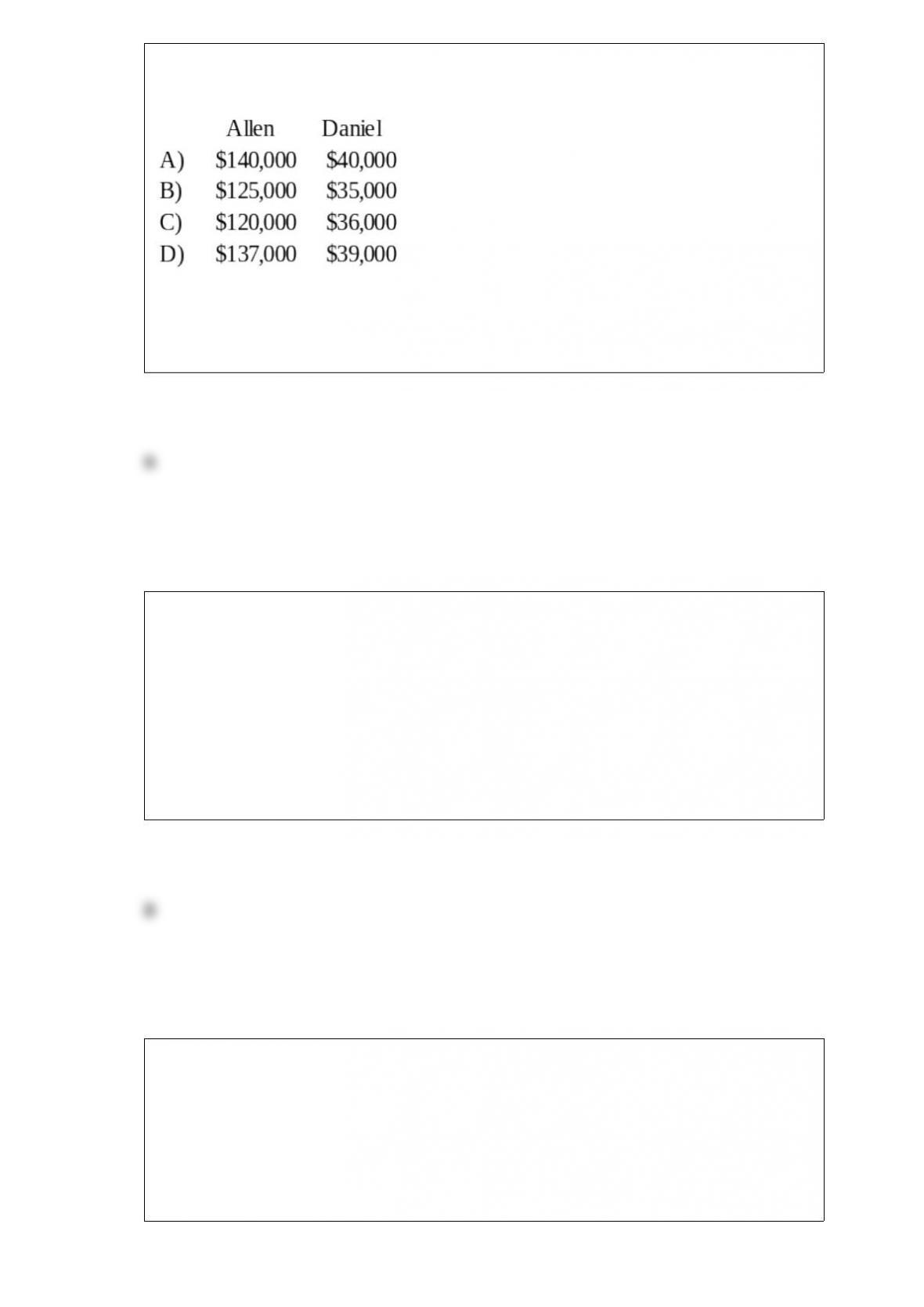

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. Allen and Daniel agree that some of the

inventory is obsolete. The inventory account is decreased before David is admitted.

David invests $40,000 for a one-fifth interest. What are the capital balances of Allen

and Daniel after David is admitted into the partnership?

A. Option A

B. Option B

C. Option C

D. Option D

Upon completion of construction and full payment of all construction costs in a capital

projects fund, the entry to record the transfer of any remaining cash should include a

debit to:

I. Contract Payable-Retained Percentage.

II. Transfer Out to Debt Service Fund.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Chapter 11 of the Bankruptcy Code provides for:

I. Reorganization.

II. Liquidation.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

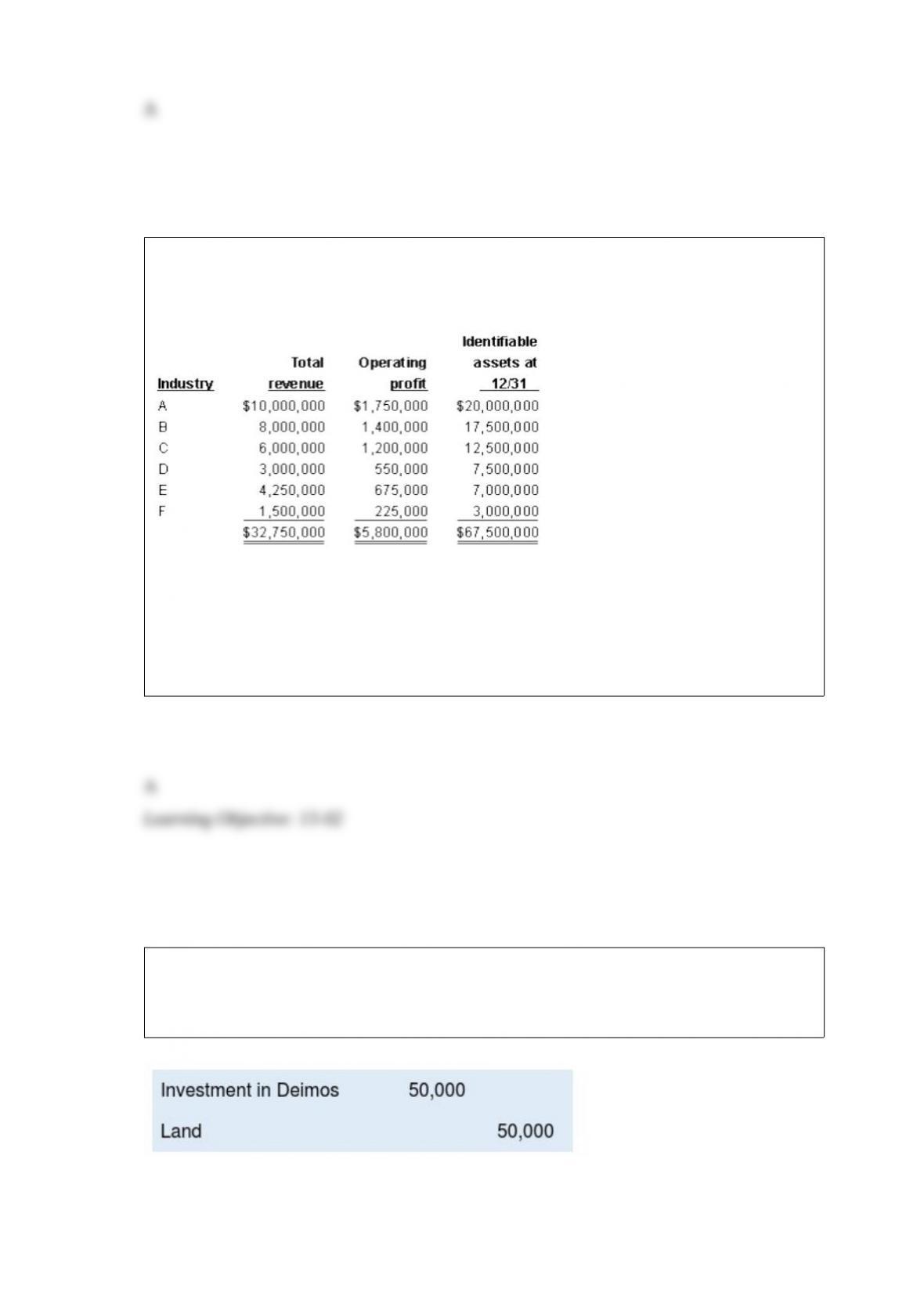

Correy Corp. and its divisions are engaged solely in manufacturing operations. The

following data (consistent with prior years’ data) pertain to the industries in which

operations were conducted for the year ended December 31st:

In its segment information for the year, how many reportable segments does Correy

have?

A. Five

B. Three

C. Four

D. Six

Phobos Company holds 80 percent of Deimos Company’s voting shares. During the

preparation of consolidated financial statements for 20X9, the following consolidating

entry was made:

Which of the following statements is correct?

A. Phobos Company purchased land from Deimos Company during 20X9.

B. Phobos Company purchased land from Deimos Company before January 1, 20X9.

C. Deimos Company purchased land from Phobos Company during 20X9.

D. Deimos Company purchased land from Phobos Company before January 1, 20X9.

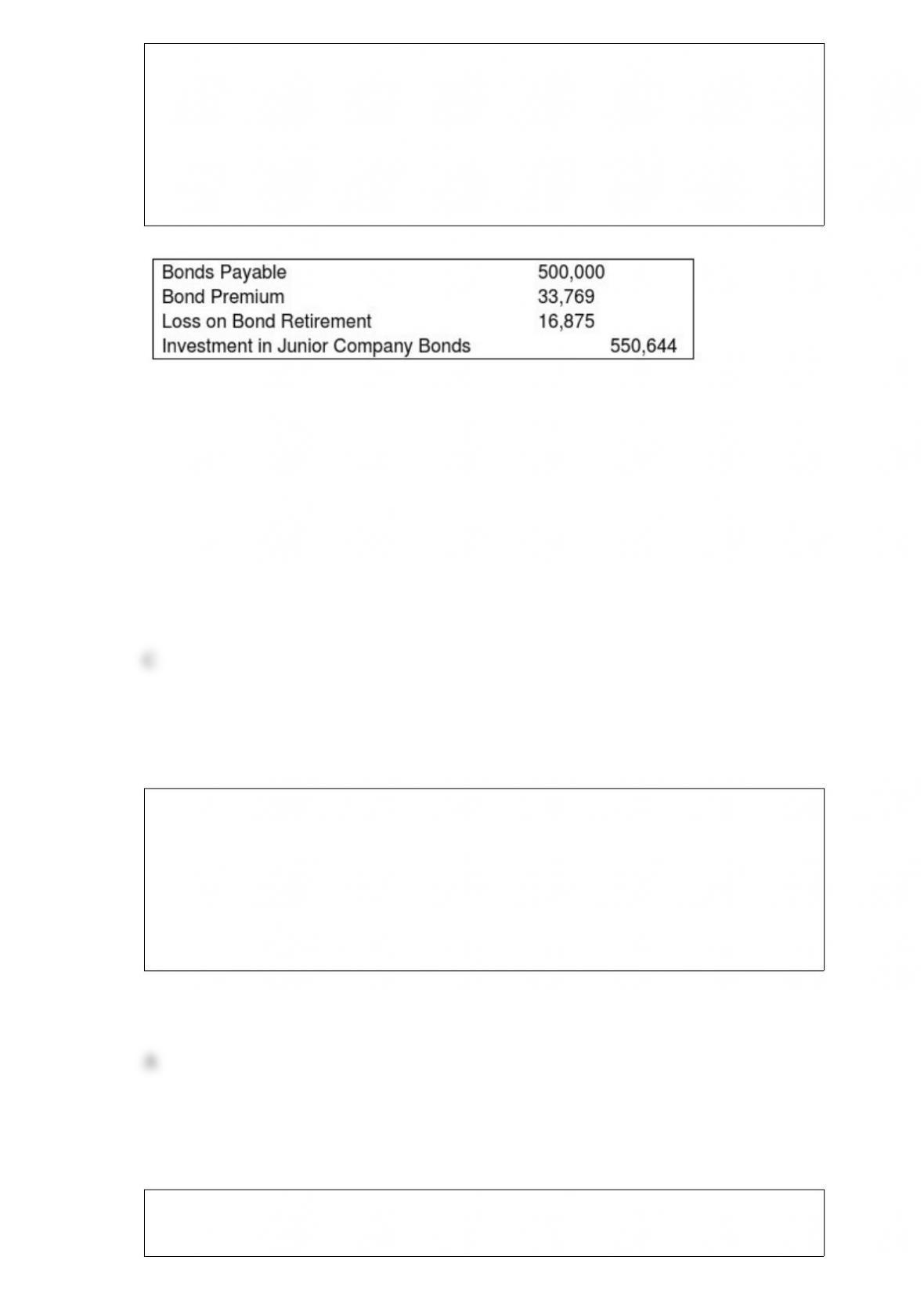

Senior Corporation acquired 80 percent of Junior Company’s voting shares on January

1, 20X8, at underlying book value. On Dec. 31, 20X8, it also purchased $500,000 par

value 8 percent Junior bonds, which had been issued on January 1, 20X5 to Partner

Corporation (unaffiliated with either Senior or Junior) at a $45,000 premium. The bonds

were originally issued with a 12-year maturity and pay interest annually on December

31. During preparation of the consolidated financial statements for December 31, 20X8,

the following consolidating entry was included in the consolidation worksheet:

Based on the information given above, what price did Senior pay to purchase the Junior

bonds?

A. $533,769

B. $516,875

C. $500,000

D. $550,644

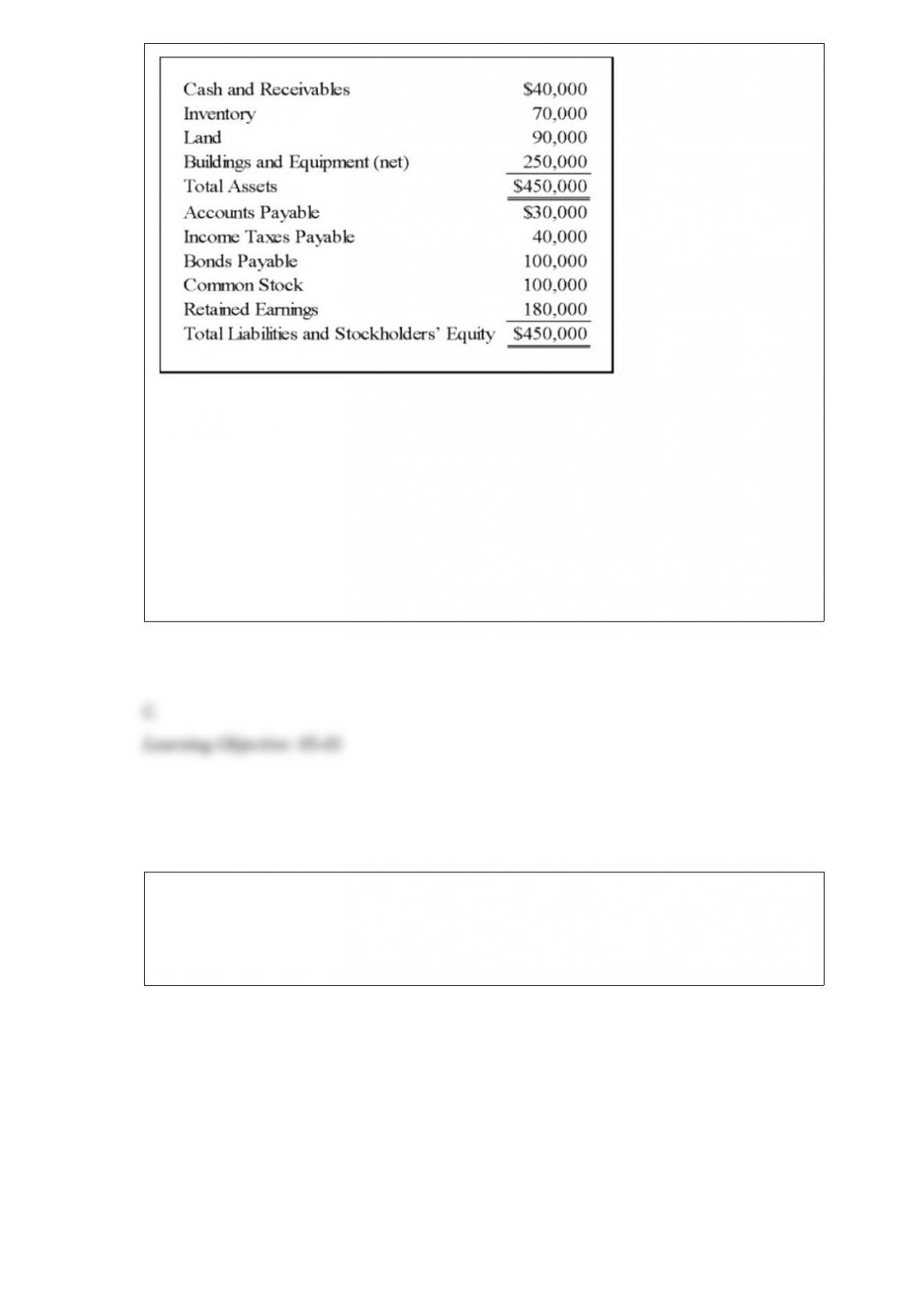

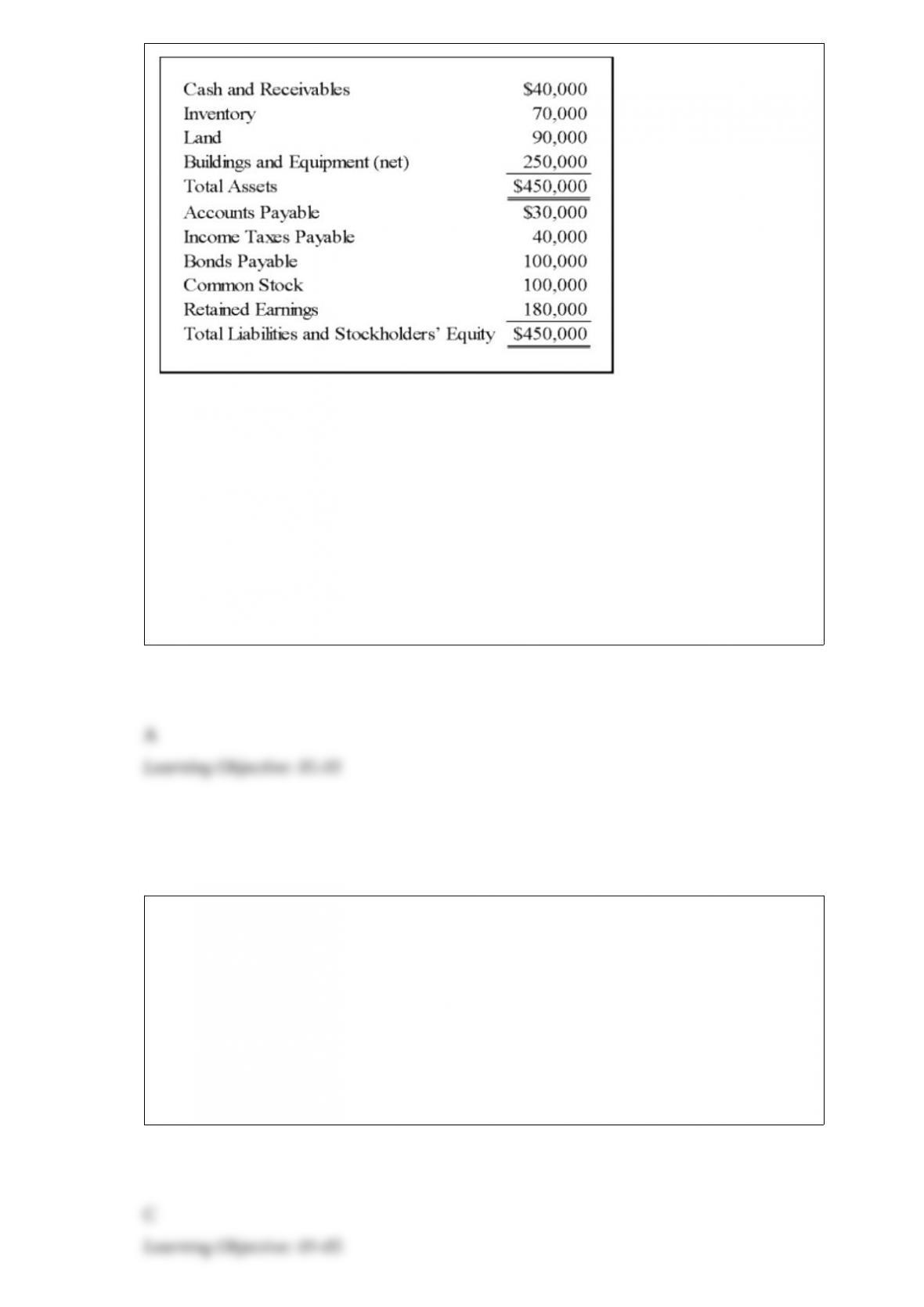

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet immediately following the acquisition?

A. $0

B. $120,000

C. $65,000

D. $20,000

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount will be reported as investment in

Silver Corporation stock in the consolidated balance sheet immediately following the

acquisition?

A. $0

B. $210,000

C. $300,000

D. $400,000

Mercury Corporation acquired 100 percent of the stock of Jupiter Company when the

book value of Jupiter’s net assets was $250,000. The fair value of Jupiter’s net assets

was $280,000 on the acquisition date.

Based on the preceding information, what amount will be recorded by Mercury as its

investment in Jupiter if it paid $275,000 for the acquisition?

A. $250,000

B. $275,000

C. $280,000

D. $300,000

On the statement of revenues, expenditures, and changes in fund balance prepared for a

debt service fund, the cash paid to retire matured serial bonds is reported as:

I. expenditures.

II. a direct deduction from unreserved fund balance.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Revenue and expense on a government-wide statement of activities for a municipality

should be measured on a(n)

A. cash basis.

B. modified accrual basis.

C. accrual basis.

D. reconciliation basis.

Which of the following acts requires that a trustee be appointed for sales of bonds,

debentures, and other debt securities of public corporations?

A. Securities Investor Protection Act

B. Trust Indenture Act

C. Investment Company Act

D. Investment Advisors Act

A citizen of Minersville purchased a truck in 20X1 for $120,000. On September 18,

20X6, she donated the truck to Minersville. The fair value of the truck on the date of

donation was $70,000. How should Minersville report the truck in its government-wide

Statement of Net Assets?

A. No asset should be reported because no expenditures were made to acquire the truck.

B. Machinery and equipment should be increased $50,000.

C. Machinery and equipment should be increased $70,000.

D. Machinery and equipment should be decreased $120,000.

Which of the following observations is consistent with the equity method of

accounting?

A. Dividends declared by the investee are treated as income by the investor.

B. It is used when the investor lacks the ability to exercise significant influence over the

investee.

C. It may be used in place of consolidation.

D. Its primary use is in reporting nonsubsidiary investments.

The City of Fargo issued general obligation bonds to finance construction of a new fire

station. The bonds were issued at a premium. In the fire station capital projects fund, the

premium should be transferred to:

A. an agency fund.

B. a special revenue fund.

C. a debt service fund.

D. an expendable trust fund.

Parent Company’s wholly-owned subsidiary, Son Corporation, maintains its accounting

records in Danish krone. However, because all of Son’s branch offices are in Sweden,

its functional currency is the Swedish krona. Remeasurement of Son’s 20X3 financial

statements resulted in a $3,200 loss, and translation of its financial statement resulted in

a $2,600 loss. What amount should Parent report as a loss in its income statement for

the year ended December 31, 20X3?

A. $0

B. $2,600

C. $3,200

D. $5,800

A private, not-for-profit hospital expended $35,000 of temporarily restricted assets to

acquire equipment. What account should be debited in the hospital’s plant replacement

and expansion fund as a result of the acquisition of the equipment?

A. Net Assets Released—Plant Acquisition.

B. Fund balance Released—Plant Acquisition.

C. Equipment.

D. Contribution Revenue Released—Plant Acquisition.

Catalyst Corporation acquired 90 percent of Trigger Corporation’s common stock on

September 30, 20X8 for $225,000. At that date, the fair value of the noncontrolling

interest was $25,000. On January 1, 20X8, Trigger reported the following stockholders’

equity balances:

Trigger reported net income of $80,000 in 20X8, earned uniformly throughout the year,

and declared and paid dividends of $10,000 on June 30 and $30,000 on December 31,

20X8. Catalyst reported retained earnings of $250,000 on January 1, 20X8, and had

20X8 income of $120,000 from its separate operations. Catalyst paid dividends of

$50,000 on December 31, 20X8. Catalyst accounts for its investment in Trigger

Corporation using the fully adjusted equity method.

Based on the information provided, what is the balance of Catalyst’s investment in

Trigger Corporation as of December 31, 20X8?

A. $216,000

B. $225,000

C. $213,000

D. $215,000

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units

from its LIFO-base inventory, which had originally cost $35 per unit. The replacement

cost is expected to be $45 per unit. The company is planning to reduce its inventory and

expects to replace only 1,500 of these units by December 31, the end of its fiscal year.

The company replaced 1,500 units in November at an actual cost of $50 per unit.

Assume that the replacement did not happen in November. In December, the company

decided not to replace any of the 1,500 units. The entry required on December 31 to

eliminate valuation accounts related to the inventory that will not be replaced will

include:

A. a debit to Excess of Replacement Cost over LIFO Cost of Inventory Liquidation for

$22,500.

B. a credit to Cost of Goods Sold for $15,000.

C. a debit to Inventory for $70,000.

D. a debit to Inventory for $15,000.

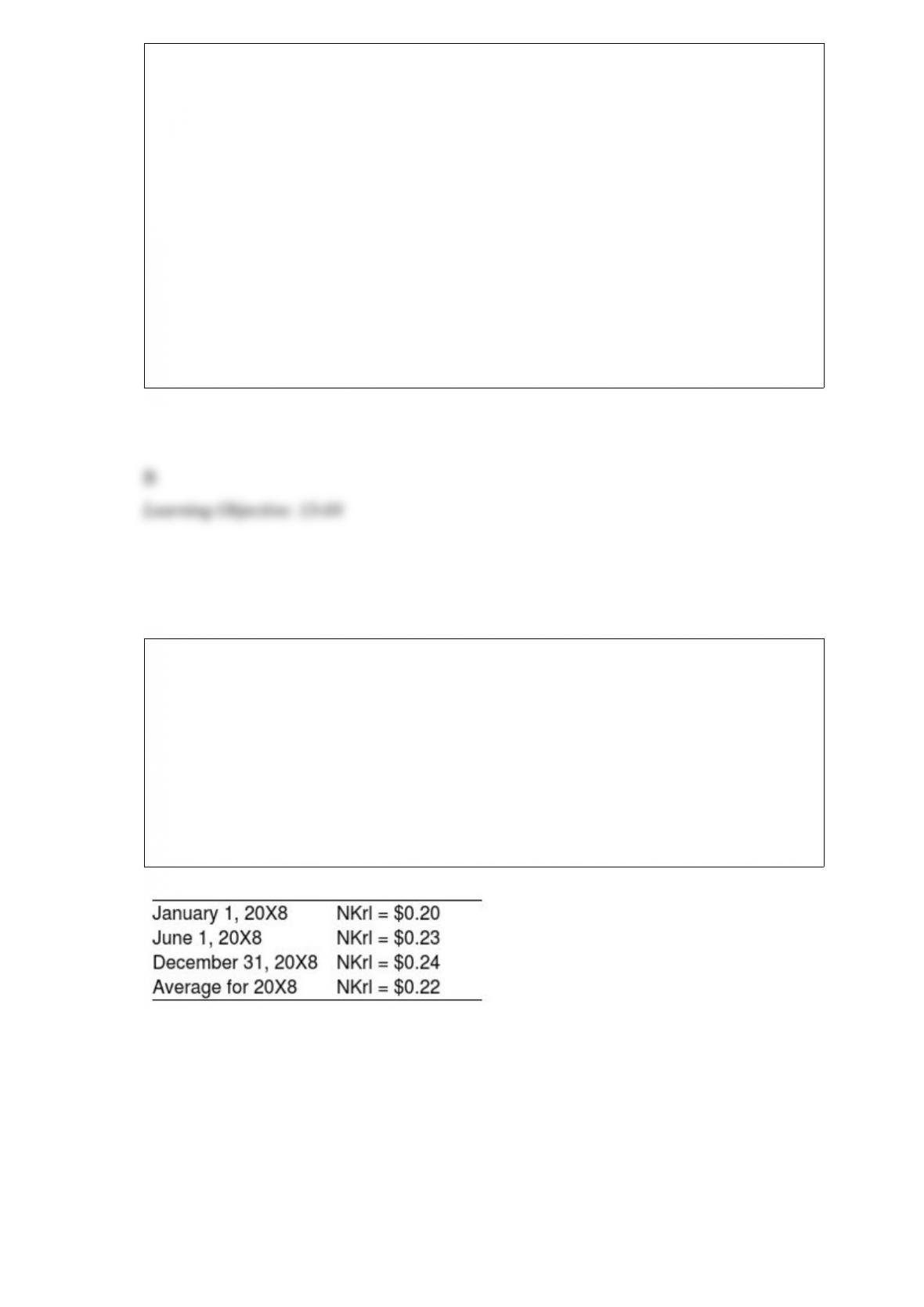

On January 1, 20X8, Transport Corporation acquired 75 percent interest in Steamship

Company for $300,000. Steamship is a Norwegian company. The local currency is the

Norwegian kroner (NKr). The acquisition resulted in an excess of cost-over-book value

of $25,000 due solely to a patent having a remaining life of 5 years. Transport uses the

fully adjusted equity method to account for its investment. Steamship’s December 31,

20X8, trial balance has been translated into U.S. dollars, requiring a translation

adjustment debit of $8,000. Steamship’s net income translated into U.S. dollars is

$35,000. It declared and paid an NKr 20,000 dividend on June 1, 20X8. Relevant

exchange rates are as follows:

Assume the kroner is the functional currency.

Based on the preceding information, in the journal entry to record parent’s share of

subsidiary’s translation adjustment:

A. Other Comprehensive Income — Translation Adjustment will be debited for $8,000.

B. Other Comprehensive Income — Translation Adjustment will be credited for $6,000.

C. Investment in Steamship Company will be credited for $6,000.

D. Investment in Steamship Company will be debited for $8,000.

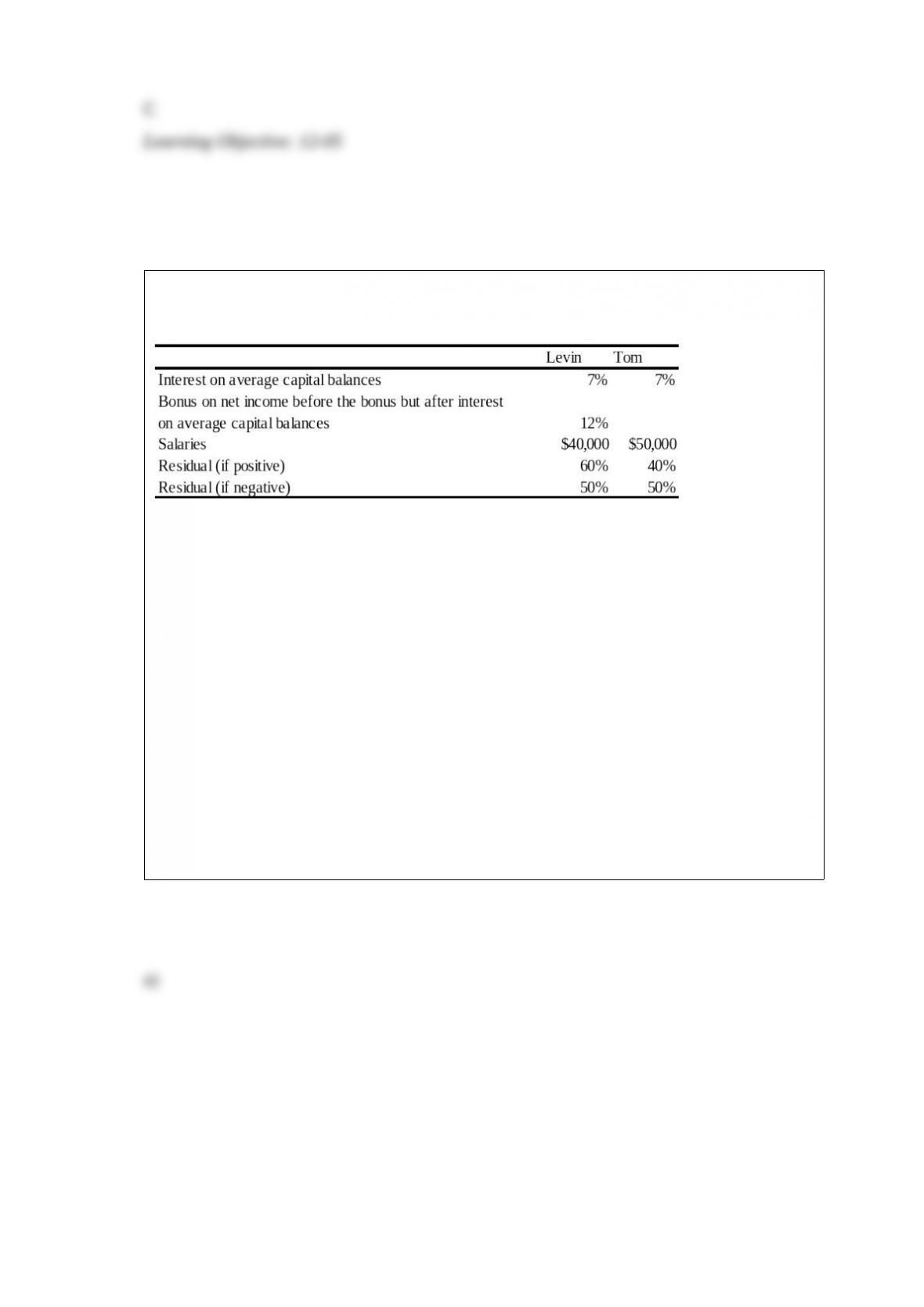

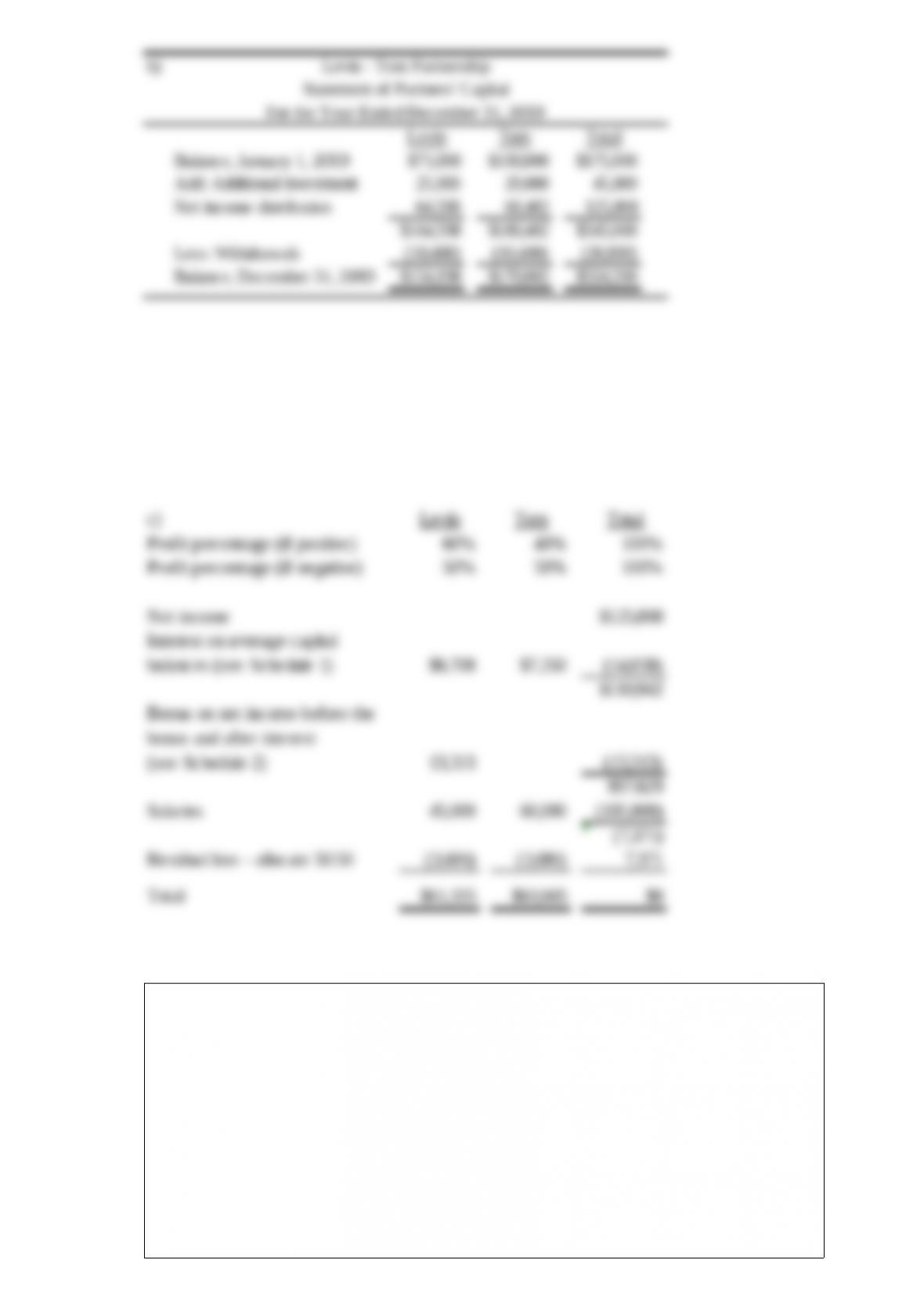

Net income for Levin-Tom partnership for 2009 was $125,000. Levin and Tom have

agreed to distribute partnership net income according to the following plan:

Additional Information for 2009 follows:

1) Levin began the year with a capital balance of $75,000.

2) Tom began the year with a capital balance of $100,000.

3) On March 1, Levin invested an additional $25,000 into the partnership.

4) On October 1, Tom invested an additional $20,000 into the partnership.

5) Throughout 2009, each partner withdrew $200 per week in anticipation of

partnership net income. The partners agreed that these withdrawals are not to be

included in the computation of average capital balances for purposes of income

distributions.

Required:

a. Prepare a schedule that discloses the distribution of partnership net income for 2009.

Show supporting computations in good form.

b. Prepare the statement of partners’ capital at December 31, 2009.

c. How would your answer to part a change if all of the provisions of the income

distribution plan were the same except that the salaries were $45,000 to Levin and

$60,000 to Jack?

Michigan-based Leo Corporation acquired 100 percent of the common stock of a

British company on January 1, 20X8, for $1,100,000. The British subsidiary’s net assets

amounted to 500,000 pounds on the date of acquisition. On January 1, 20X8, the book

values of its identifiable assets and liabilities approximated their fair values. As a result

of an analysis of functional currency indicators, Leo determined that the British pound

was the functional currency. On December 31, 20X8, the British subsidiary’s adjusted

trial balance, translated into U.S. dollars, contained $17,000 more debits than credits.

The British subsidiary reported income of 33,000 pounds for 20X8 and paid a cash

dividend of 8,000 pounds on October 25, 20X8. Included on the British subsidiary’s

income statement was depreciation expense of 3,500 pounds. Leo uses the fully

adjusted equity method of accounting for its investment in the British subsidiary and

determined that goodwill in the first year had an impairment loss of 25 percent of its

initial amount. Exchange rates at various dates during 20X8 follow:

January 1 1 = $2.10

October 25 1 = 2.25

December 31 1 = 2.20

Average for 20X8 1 = 2.21

Based on the preceding information, in the stockholders’ equity section of Leo’s

consolidated balance sheet at December 31, 20X8, Leo should report the translation

adjustment as a component of other comprehensive income of:

A. $19,440

B. $17,000

C. $18,786

D. $19,380

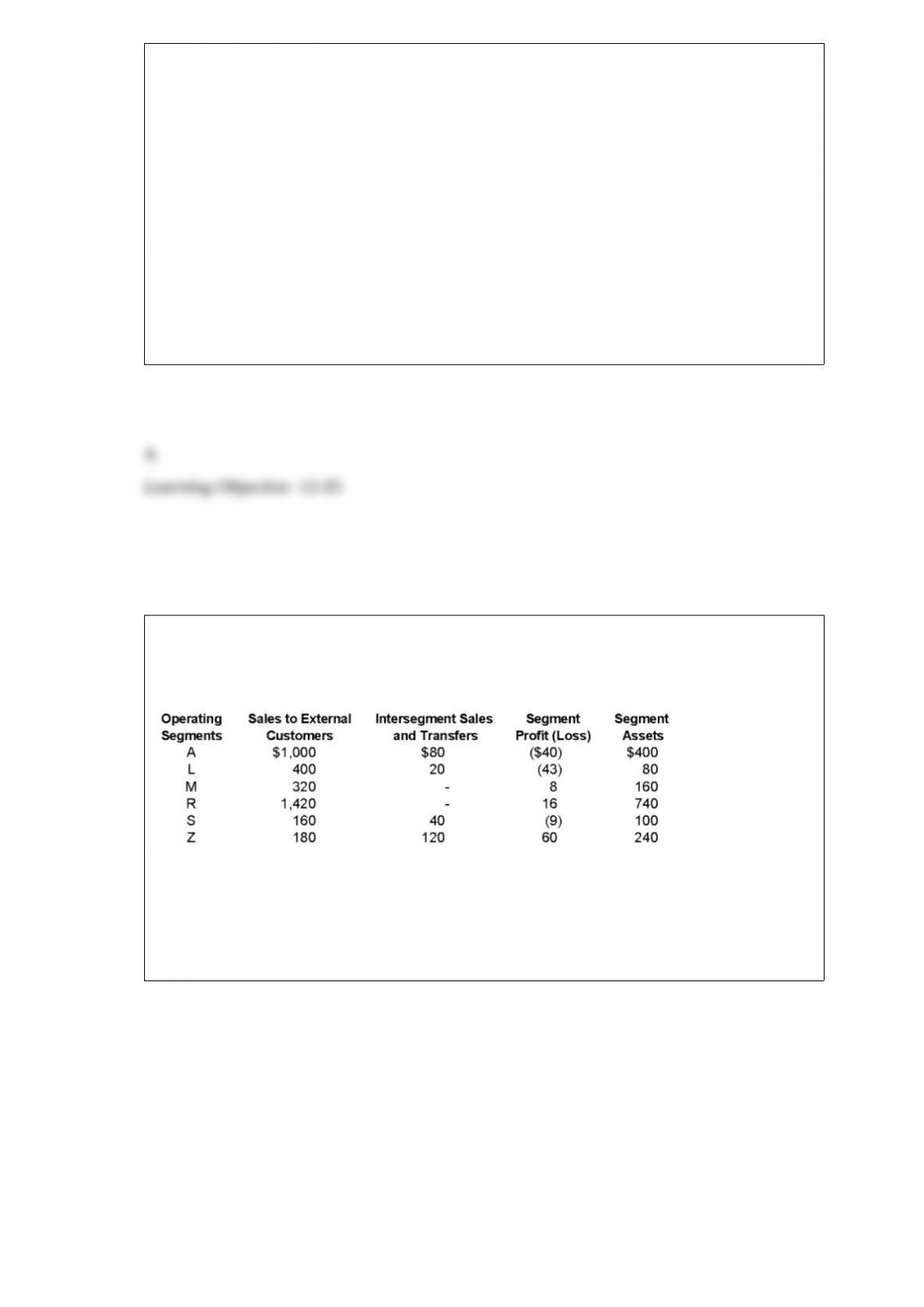

Ridge Company is in the process of determining its reportable segments for the year

ended December 31, 20X8. As the person responsible for determining this information,

you gather the following information:

Required:

a) Using the appropriate tests, determine which of the industry segments listed above

are reportable for 20X8. Show your supporting computations in good form.

b) Indicate whether or not Ridge’s reportable segments satisfy the 75 percent test. Show

your supporting computations in good form.

Which regulation created the Securities and Exchange Commission?

A. Securities Act of 1933

B. Securities Exchange Act of 1934

C. Investment Company Act of 1940

D. Garn-St. Germain Depository Institutions Act of 1982

Which of the following is an example of volunteer services received by a not-for-profit

entity that should be recognized as revenue?

I. Services requiring specialized skills, provided by individuals with those skills, that

otherwise would have to be purchased.

II. Services of lay faculty at a private university operated by a religious order.

III. Services that create or enhance non-financial assets, regardless of whether or not

they require specialized skills.

A. I only

B. I and III only

C. II and III only

D. I, II, and III

Tinitoys, Inc., a domestic company, purchased inventory from a Brazilian company for

500,000 Brazilian reals (Br. reals) on May 1, 20X2. Payment is due on June 30, 20X2.

On May 1, 20X2, Tinitoys also entered into a 60-day forward contract to purchase

500,000 Brazilian reals. The forward contract is not designated as a hedge. Tinitoys’

fiscal year ends on May 31. The direct exchange rates were as follows:

Spot Rate Forward Rate

May 1, 20X2 $0.523 $0.525 (60 days)

May 31, 20X2 $0.516 $0.52 (30 days)

June 30, 20X2 $0.508

Based on the preceding information, the entries on June 30, 20X2, include a

A. credit to Foreign Currency Transaction Gain, $6,000.B. debit to Dollars Payable to

Exchange Broker, $254,000.

C. debit to Foreign Currency Units (Br. reals), $254,000.

D. credit to Foreign Currency Receivable from Exchange Broker, $262,500.

Which of the following are examples of intercompany balances and transactions that

must be eliminated in preparing consolidated financial statements?

I. Security holdings

II. Interest and dividends

III. Sales and purchases

A. I, II

B. I, III

C. I, II, III

D. II